Notifying the bank about erroneous receipt of funds

A company that has received an erroneous payment must send a written notification to the bank within 10 days of receiving the bank account statement showing the excess funds. The form of such a written message to the bank is not established by law, therefore banks establish such forms with their own internal documents. If the bank does not have an approved form, the organization draws up a message in free form.

Bank, depending on the terms of the bank account agreement:

- if it is possible to write off erroneously credited amounts from the company’s bank account without acceptance, writes off the erroneously credited funds without a separate order from the organization;

- If there is no such possibility under the agreement between the bank and the organization, the erroneously transferred funds are written off only upon receipt of the corresponding order.

Refund based on payment order

Regardless of how the erroneous payment was made (SMS, ATM, Internet), first of all it is necessary to submit an application to the bank via an application (letter). It is worth remembering that in most cases it will not be possible to return the money in this way. The bank, according to its own laws and documents (bank secrecy), does not have the ability to cancel a monetary transaction without the consent of the person in whose favor the funds were transferred. And the recipient may well refuse to return the funds or simply ignore the request sent to him.

An organization or individual may learn about an erroneous receipt of funds to an account based on information from the bank (message, letter or account statement), as well as by receiving a message from the payer who made an error when sending funds.

As of August 6, 2019, amendments to PBU 1/2008 “Accounting Policies of Organizations” come into force. Thus, in particular, it has been established that in cases where federal standards do not provide for a method of accounting for a specific issue, a company can develop its own method. On September 1, amendments to the law on state registration of legal entities and individual entrepreneurs come into force.

In other words, when it became known that the agreement under which the funds were transferred was terminated, or the money arrived as a result of mistakes, etc. Also, the beginning of a reasonable period is considered the moment when it became known about the receipt of unexplained amounts; in some cases, the beginning of the calculation of a reasonable period is the moment of the beginning of using someone else’s unreasonably received funds.

Our organization uses the simplified tax system (D-R), and received funds in advance from buyer A on account for future deliveries of goods. After some time, it turned out that the funds should have been transferred to another counterparty and buyer A. (based on a letter) asks us to transfer these funds to his other supplier with the allocation of VAT. Can we carry out such a transaction and how can we reflect this in accounting and tax accounting?

N 02-04-09/3641 sends an updated mechanism for the return of the amount of payment (tax, fee and other payment administered by the tax authority), erroneously transferred by the taxpayer to the account of the Federal Treasury for the constituent entity of the Russian Federation (hereinafter referred to as the UFK), opened on the balance sheet account N 40101 “Revenue distributed by the bodies of the Federal Treasury between the budgets of the budget system of the Russian Federation” (hereinafter referred to as account N 40101), and intended for payment to account N 40101 of the Federal Tax Code of another constituent entity of the Russian Federation.

If the supplier subsequently transfers to the buyer goods that comply with the terms of the concluded contract, its sale will be considered to have taken place on the date of such transfer. For accounting and tax purposes of the seller, this sale will be reflected in the general manner.

Bank, depending on the terms of the bank account agreement:

- if it is possible to write off erroneously credited amounts from the company’s bank account without acceptance, writes off the erroneously credited funds without a separate order from the organization;

- If there is no such possibility under the agreement between the bank and the organization, the erroneously transferred funds are written off only upon receipt of the corresponding order.

Purpose of payment in case of erroneous transfer of the amount under the agreement If an erroneous transfer of funds was carried out under the agreement, then the funds are returned due to termination of the agreement. In this case, an agreement to terminate the contract is formed and, in accordance with this agreement, a refund is made. The purpose of payment indicates the number and date of the agreement to terminate the contract.

Important Why is the organization’s money transferred to the wrong address? There may be several reasons for this unpleasant situation:

- Firstly, there may be an error in the details of the counterparty. Such inaccuracies can creep into documents when they are received by fax, which is due to the specifics of this type of communication.

An accountant may also make a mistake when typing a payment order. With electronic document management, such errors are very rare, since the data can be immediately imported into a payment order.

- Secondly, there may be a mistake by the banking institution.

- The appeal itself is submitted to the general director (or other authorized person) of the bank. And in the header of the application the payer’s details are indicated: full name; - residential address; - passport details; - contact phone number.

- Next, the statement itself is written about the request for a refund or cancellation of the erroneously made payment.

Cancellation of an incomplete payment If an erroneous payment was made, but the person realized it in time and wrote an application to the bank to cancel the transfer of funds as soon as possible, the bank has the opportunity to cancel the transaction and return the funds to the previous account or send them to the newly specified details. To do this you need to fill out an application:

It is necessary to provide a statement that a person has received a sum of money that was transferred to him by mistake, and that he refuses to return (or ignores) the funds mistakenly transferred to his account or card. After which, the authority’s employees will make a request to the bank to obtain information regarding the owner of the card or account, followed by an investigation and a final court decision.

It’s quite difficult to make a mistake when transferring money to a card or account. The reason lies in the fact that the last digit in the number is randomly generated, but connected according to a special system with the previous numbers.

Following this information, accidentally indicating someone else’s number is quite difficult, but still possible.

NewsPermalink

Banking error, human factor - these are the main reasons for situations when payments are credited to completely different counterparties or there is an overpayment under contracts. In such situations, it becomes necessary to return the erroneously transferred funds.

There are two ways to get your money back:

- Voluntary. You send a standard application to the recipient with a request to return the erroneously transferred amounts within the agreed period and to the specified details. In this case, you depend on the honesty and integrity of another person.

- Judicial.

Accounting and tax accounting of cash return transactions

In accounting, when returning funds, a posting is used that mirrors the one with which the funds were accepted for accounting:

- Dt 51 K 62 - cash receipt;

- Dt 62 Kt 51 - refund.

In tax accounting:

- simplified tax system: crediting funds is reflected in taxable income on the date of receipt of funds to the current account; upon return, taxable income is reversed by the date of return;

- BASIC: crediting and returning funds transferred by mistake is not reflected.

How to return erroneously transferred money

How to return the money transferred by mistake?

Many organizations, as well as ordinary citizens, have to transfer funds daily.

Neither accountants, nor entrepreneurs, nor bank employees are insured against making an erroneous payment.

The situation is unpleasant, but not hopeless. How to return money paid by card by mistake?

List of conditions under which it is possible to return purchased products

The basis for the return procedure may be a violation of the client’s rights, in which he will receive either money back or a replacement product.

You should get to know them in more detail:

- If for some reason the product does not suit the client. Within 14 days, you can take the item back to the seller and get your money back. There is one “but”: this rule does not apply to the category of technically complex goods, as well as food products;

- If the product was sold of inadequate quality. This means that the product cannot be used in its usual way, or it does not meet numerous declared characteristics;

- Mechanical damage was detected. This fact must be confirmed and recorded properly. The client can make a special act in which it is necessary to describe point by point each drawback of the purchase;

- If the product often has to be sent for repairs, or it requires more expensive repair work. In this situation, it is necessary to compare the product itself with the price.

The client has the right to choose the option of exchanging goods, since not only a refund is possible.

The legislative framework

Refunds must be made within a reasonable time, although the legislation has not established an exact time frame.

Domestic courts, when considering cases on the return of erroneously transferred funds, mainly rely on a seven-day period.

In this case, points that may affect its duration are taken into account, namely:

- when the error was discovered;

- whether the recipient has started using these means.

If the recipient begins to spend someone else’s funds that were transferred to him by mistake, then the injured party has the right to demand interest for the use of this money. And the longer the funds are not returned, the more interest you will have to pay.

There are 2 ways to return funds transferred to the wrong address:

- Voluntary: the recipient independently transfers the required amount to the specified account.

- Compulsory: funds are returned by court order.

I mistakenly transferred money to someone else’s card: how to get the money back?

Nowadays, money transfers have become commonplace. But the downside of technological progress can be called incidental situations in which the money goes to another recipient.

Through inattention or because of haste, an incorrect recipient's card number is entered and the money ends up in someone else's account. What to do in this situation?

Let's consider 2 options for the development of further events:

How to return erroneously transferred money to a Sberbank card?

After this, you need to come to the nearest bank branch and leave an application addressed to the manager with a request for a refund, attaching a receipt or check. Such an application is considered within 30 days.

You can get your money back even in case of fraud, but you must notify the bank about it within 24 hours . First, call the hotline, then file a report with the police about fraudulent activities committed against you.

How to return a payment through Sberbank online?

The Sberbank website (https://online.sberbank.ru/) provides an additional payment return service.

When sending money to a card after 21:00, the payment transaction is performed only from 9:00 the next day . This gives the sender time to cancel the incorrect payment before it is processed.

You can identify a payment that has not yet been processed by the bank by the status “Executed by the bank.” Click on the payment line, then click the “Cancel” button. The money will be returned to the card before the payment document is processed by the bank.

Funds will also not be transferred in the following transaction statuses:

- "Interrupted";

- “Rejected by the bank”;

- "The application has been cancelled."

VAT upon return of advance payment to the buyer

The main criterion for the transition period is the rule: regardless of the size of the tax rate accrued on the advance payment (in 2018 - 18%, in 2021 - 20%) for shipments made in 2021, VAT is taken into account in the shipping invoice at the rate of 20%. There are no other innovations regarding VAT on prepayments.

The algorithm of operations remains the same: upon receipt of the advance, the supplier charges VAT and pays it, and no later than after 5 days, registers a “preliminary (advance) invoice” in the sales book and issues it to the buyer. The advance is recorded in the reporting quarter when it was received, and is reflected in the VAT return on page 070 of section 3.

When shipping goods and materials as an advance payment, the seller has the right to reimburse the amount of tax from the budget. But if the contract is terminated or its provisions are revised, and only part of the goods is shipped or the delivery is canceled completely, then the seller is obliged to return the previously received advance payment (or the unused balance). Its return is also associated with a VAT adjustment, since the seller has the right to claim a deduction from the amount of the unused advance payment if the basis for non-fulfillment of obligations was the termination of the contract or a change in its terms. In this case, the supplier issues an adjustment invoice, recording the refund.

The supplier can deduct VAT when returning the advance payment to the buyer on the date of return of the advance payment. VAT is calculated as the amount of the advance received multiplied by the rate that was applied when receiving the advance payment. The fact of a payment return must be reflected in accounting and confirmed by a payment document. You can claim the right to a deduction within one year from the date of return of payment for a failed (or partially failed) transaction. VAT on the return of the advance payment to the buyer in the declaration is reflected on page 120 of section 3.

How can I return erroneously transferred funds to my current account?

Incorrect crediting of funds to a current account may occur by mistake:

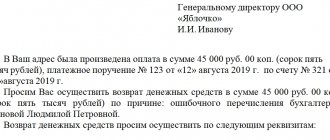

In the first case, the organization that received someone else's money is obliged to report this to its bank by submitting a written application, accurately indicating the amount.

The application is submitted within 10 days from the date of receipt of a bank statement, which confirms the fact of the error.

According to Art. 1102 of the Civil Code of the Russian Federation, the organization to whose account an erroneous credit was received is obliged to return the funds within a reasonable time.

Sometimes employees of an organization do not immediately notice that someone else’s funds have been transferred to the company’s account. In this case, 10 days are counted from the moment of receipt of information about the error, which usually comes in the form of a letter from the payer or bank.

How to write a return letter?

An application/letter for the return of erroneously transferred funds is drawn up according to the general rules. Such an appeal can be sent to various authorities: a bank, tax office, court or the Pension Fund.

Compilation rules:

- provided in writing;

- applicants can be individuals or legal entities;

- presented in one copy;

- brevity and clarity of presentation;

- no grammatical errors.

- the name of the organization that received the erroneous funds;

- Full name of the applicant;

- the reason for petition;

- the applicant's demands for return;

- date of document preparation;

- signature.

The application contains the following items:

Depending on the terms of the agreement, the bank must:

- write off money transferred by mistake without an order from the organization;

- write off money upon receipt of an order from the organization.

Incorrectly credited funds are not considered income of the organization, therefore, when returned, they are not reflected in expense accounting documents and are not taxed.

In accounting, the return of money is noted by posting:

Options requiring the return of the amount and the consequences of non-refund

The main mistakes associated with the transfer of funds are:

- Selecting the wrong counterparty for whom the payment was intended.

- Incorrect amount specified when generating the document.

- The purpose of the contribution itself contains the details of a document that does not exist in the relationship.

These kinds of mistakes can be noticed by two participants in the relationship. But the payer himself must notify in writing of his consent to carry out operations to return the funds.

The error can be corrected by adjusting the contribution assignment. This can be done if there is a supplier-buyer relationship between the counterparties.

The erroneous amount may be credited towards future payments. Such actions are prohibited unless there are contractual obligations between the companies. All money in this case is subject to mandatory return to the buyer.

This is important to know: Claim for poor quality services: what you need to know when filing and a sample document

Accounting for such contributions is carried out by the seller and the payer according to a typical scenario - a mirror image. It does not matter here why the erroneous payment was made.

Expert opinion

Mikhailov Evgeniy Alexandrovich

Teacher of civil law. Lawyer with 20 years of experience

Since unjustified contributions do not in any way relate to mutual settlements between organizations, value added tax on them is not charged either for payment or refund. But it is worth noting that if payments are made in foreign currency, then exchange rate differences may arise. The party that returns the amount must indicate in the purpose of payment that this is the return of an erroneous contribution. And also indicate the details of the document according to which the buyer asked for a refund.

If a mistake is counted as future payments, then it will be taken into account as a seller-buyer relationship. Then value added tax will also be taken into account here.

What to do if you transferred money to someone else's phone?

To return money to your phone, it is advisable to have a confirmation receipt, which will reflect all the necessary data. Further steps will depend on how you transferred the money.

You only have 14 days to make a refund . When contacting the office of your mobile operator, provide your passport and a receipt for the amount sent.

Once all data is confirmed, the technical service will cancel the transaction and the money will be returned to your account.

The following must be taken into account:

- The mobile number must be linked to the specified passport data.

- You must provide a bank statement when paying through online services or mobile applications.

- The receipt or check must be linked to the number if the payment was made through the terminal.

- If you paid via an electronic wallet, you can provide a printout of your payment history.

Beeline

What methods can you use:

- phone number of the recipient of funds;

In addition, you must write an application online or in the office, as well as provide a check or receipt for payment.

You can also return an erroneous MTS payment to a bank card, indicating in the application the card details and the full name of the banking organization.

The application form can be found on the official website of this operator (www.mts.ru/).

Megaphone

If you use this connection and mistakenly put money on someone else’s mobile phone, then contact the operators in the office or by calling 8 800 550 70 95.

The money can be returned to the card, in cash or to your phone number.

The chances of returning an erroneous payment are quite high if everything is done promptly.

Only 14 days are given to process refunds.

Tele 2

The error of sending money to a third-party phone number can also be corrected by users of Tele2 operator services.

In the absence of a receipt, it will be much more difficult to return the funds, since it is not always possible to check all the data only by phone number.

To simplify the task, the address of the terminal, indicating the exact amount and approximate time of sending funds will help.

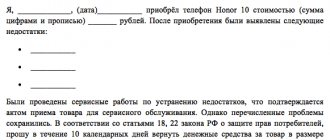

Buyer requirements

In the case of merchant acquiring, only the owner of the card with which the purchase was made can apply for a refund. Who actually purchased the product or service does not matter in this case.

Important ! According to current legislation, you can submit a return application no later than 14 days after making the purchase.

When contacting a retail outlet, the cardholder must present a certain package of documents:

- passport;

- the bank card itself;

- purchase receipt;

- written statement.

Important ! If it is not possible to present the payment card involved in the transaction to the seller (the card was lost, damaged, or expired), it is necessary to clarify the procedure with the acquiring bank.

In the case of Internet acquiring, everything is somewhat simpler. If an entrepreneur uses a full-fledged online store to make sales, all that is required from the buyer is to cancel the prepaid order on time. In this case, you need to act from the same profile from which this order was created. There are no more strict requirements for the buyer.

Important ! If the return occurs after the goods have been received, the requirements for the buyer are determined by the internal regulations of the online store.

How can I get my money back for an erroneously paid state fee?

State duty is a mandatory payment required for processing various documents, including passports . To pay the state fee, a receipt with details is required, according to which the money is credited to the current account.

But sometimes, due to an error by the cashier or payer, money is transferred to the wrong account number. Often the error occurs because the payer sent funds to outdated details that he found on the Internet.

To return funds, you must send an application/letter addressed to the head of the local tax authority. This letter will be handed over to the tax office against signature.

In addition, the payer must send an application for the return of the paid amount to the body authorized to perform legally significant actions. This may be the Federal Migration Service (in case of registration of a passport), in the registry office (in case of marriage), etc.

In general, returning erroneously transferred funds is a troublesome and responsible procedure, especially if the payer does not have a document confirming payment.

Therefore, when making payments yourself, try to at least temporarily save checks and receipts, which will greatly facilitate the task.

Refund of money mistakenly transferred to the organization's account

On the deduction of advance VAT when returning the advance payment to the buyer (Zaitseva S.

A payment order, in the “Purpose of payment” field, the basis for the transfer will be indicated “Return of advance payment under supply agreement N.”, and can serve as such a document-based basis for deducting “advance” VAT from the amount that falls on the withdrawn advance payment. If in the “payment” for a refund to the buyer the details of letters demanding the return of previously transferred money and a reference to the reasons for withdrawing the advance (part of the advance) are indicated, claims from controllers will generally be minimized. The capital's tax authorities, explaining a similar issue, indicated: in the event of a change in the terms of the supply contract or its termination, as well as the return of advance amounts against the upcoming supply of goods, the amounts of VAT calculated by the supplier of such goods and paid by him to the budget from the specified advance amounts are subject to full deduction in the amount after the corresponding adjustment transactions are reflected in the accounting in connection with the return of the advance, but no later than one year from the date of its return (Letter dated March 14, 2007 N 19-11/022386).

Clause 4 art. 172 of the Tax Code of the Russian Federation specifies: deductions of tax amounts specified in paragraph 5 of Art. 171 of the Tax Code of the Russian Federation, are carried out in full after the corresponding adjustment operations are reflected in the accounting in connection with the return of goods or refusal of goods (work, services), but no later than one year from the date of return or refusal.

But the wording (you will agree) is such that there is no doubt: clause 4 of Art. 172 is directly related only to paragraph. 1 clause 5 art. 171. Then it is not clear whether the annual limitation on the deduction of “advance” VAT applies to the cases provided for in paragraph.

2 clause 5 art. 171. If yes, then from what moment should the time be counted?

The agreement to terminate the contract, drawn up on 9.2013 (later than the deadline for submitting “clarifications” with the declared deductions - June 2013), did not save the situation: the company’s arguments that the right to deduct amounts of “advance” VAT arose only from the moment of termination of the contract (from the date of drawing up the agreement), were not accepted by the cassation authority. The court issued a verdict: by claiming deductions in June 2013, the company missed the deadline established by law for claiming these deductions.