Is there a tax deduction for medicines?

Taxpayers have the right to reimbursement of expenses for the purchase of medicines prescribed by a doctor in the form of a social tax deduction.

This means that the amount of a citizen’s income spent on medicines is exempt from taxation at a rate of 13%. In monetary terms, the taxpayer will receive 13% of the cost of purchased drugs.

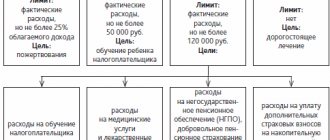

The legal limit for the social tax deduction is 120,000 rubles. This is the maximum cost incurred by which you can reduce your annual taxable income.

If the taxpayer’s annual earnings are less than 120,000 rubles, then the amount of the benefit will be limited to the amount of annual earnings.

You can receive a social deduction only for those medications that are included in the list of medications approved by law.

Return deadlines

Time intervals can be calculated in two main ways:

- When deducted through an employer. Collect the necessary package of documents and submit to the tax authority for verification. After 30 calendar days, collect a notice indicating the amount to be refunded. Bring it to the accounting department of the organization in which taxation is calculated, and receive a deduction in the form of a recalculation of the calculated tax.

- When returning through an authority. Collect the necessary package of documents and bring it to the inspectorate along with the 3-NDFL declaration. After 3 months, a desk audit will be carried out. Within 30 days after this, the social deduction funds will be transferred to the settlement account specified in the application.

With the correct and rational use of social benefits, you can compensate yourself for part of the costs and reduce the expenditure burden on purchasing necessary medicines. When using a tax deduction, the family budget can be replenished with money for more pleasant spending than medicines.

Requirements for receiving benefits when purchasing medicines

Who can apply for a tax deduction

A tax deduction for the purchase of medicines can be received by any citizen who has income taxed at a tax rate of 13% and has incurred actual costs for the purchase of medicines.

Benefits can be obtained both for the purchase of medicines for yourself and for your spouse, minor relatives or adopted children or parents.

Reasons for receiving

Expenses for medicines must be justified, i.e. medications must be purchased based on a doctor's prescription and with the taxpayer's personal funds.

If the medicines were purchased by another person, for example, an employer, then these amounts will not be reimbursed, because The taxpayer himself does not bear the actual expenses.

But if a citizen reimburses the employer for the purchase of medicines for him by deducting from wages or depositing cash in the cash register of the enterprise, in this case a deduction for personal income tax will be provided.

Law

The list of medications, the costs of which can be reimbursed in the form of a social deduction, was approved by Decree of the Government of the Russian Federation of March 19, 2001 No. 201.

This list contains international nonproprietary names of drugs; in a pharmacy, drugs of the same composition and action may differ in name.

A tax deduction will be provided for those medicines that contain the medicines specified in the List, regardless of their trade names (letter of the Ministry of Finance of Russia dated June 19, 2015 No. 03-04-07/35549).

Basic information

The legislation of the Russian Federation establishes the requirements that an applicant for a tax deduction must meet:

- presence of Russian citizenship;

- availability of a source of income that is subject to personal income tax of 13%;

- purchase of medicines, payment for medical services in the year of application minus deductions (from personal funds);

- the ability to provide checks, receipts and other documents that confirm expenses made;

- the purchase of medicines for which the taxpayer plans to receive a deduction, only with a doctor’s prescription, and the opportunity to provide the corresponding form;

- purchasing medications that are registered in the Russian Federation and obtained through a licensed pharmacy.

If you have no taxable income, you will not be able to take advantage of the deduction.

Our experts know the answer to your question

Do you want to solve your problem? Consult our lawyer for free the form or numbers :

- Moscow ext. 143

- St. Petersburg ext. 702

- RF ext. 684

List of medicines to apply for deduction

Anesthetics and muscle relaxants

Anesthesia:

- Halothane (solution for inhalation anesthesia in vials)

- Hexobarbital (powder for injection)

- Dinitrogen oxide (gas in cylinders)

- Ketamine (injection solution)

- Sodium oxybate (injection solution)

- Sodium thiopental (lyophilized powder for injection)

- Diethyl ether (liquid in bottles)

Local anesthetics:

- Bupivacaine (injection)

- Lidocaine (aerosol, solution for injection, gel, solution in capsules, eye drops)

Muscle relaxants:

- Atracurium besilate (injection solution)

- Botulinum toxin, albumin (lyophilized powder for injection)

- Vecuronium bromide (powder for injection)

- Pipecuronium bromide (powder for injection)

- Suxamethonium bromide (powder)

Analgesics, non-steroidal

Narcotic analgesics:

- Morphine (injection solution, tablets)

- Morphine + narcotine + papaverine + codeine + thebaine (injection solution)

- Pentazocine (injection solution, tablets)

- Piritramide (injection solution)

- Trimeperidine hydrochloride (injection solution, tablets)

- Fentanyl (injection solution)

Non-narcotic analgesics and non-steroidal anti-inflammatory drugs:

- Acetylsalicylic acid (tablets)

- Diclofenac sodium (tablets, dragees, injection solution, suppositories, gel, eye drops)

- Ibuprofen (capsules, tablets, syrup, cream)

- Ketoprofen (tablets, capsules, suppositories, gel, powder for solution)

- Lornoxicam (tablets, lyophilized powder for injection solution)

- Meloxicam (tablets, suppositories)

- Nalbuphine (solution for injection)

- Tramadol (injection solution, capsules, tablets, oral drops, suppositories)

- Allopurinol (tablets) as a treatment for gout.

Other means:

- Colchicine (tablets, dragees)

- Penicillamine (tablets, capsules, dragees)

Medicines used to treat allergic reactions

Antihistamines:

- Quifenadine (tablets)

- Ketotifen (tablets, capsules, syrup)

- Chloropyramine (tablets, solution for injection)

Drugs affecting the central nervous system

Anticonvulsants:

- Valproic acid (tablets, capsules, syrup, dragees, suspension, drops)

- Carbamazepine (tablets)

- Clonazepam (tablets, drops, injection solution)

- Lamotrigine (tablets)

- Phenytoin (tablets)

- Phenobarbital (tablets, oral solution)

- Ethosuximide (capsules)

Drugs for the treatment of parkinsonism:

- Amantadine (tablets, solution for injection)

- Biperiden (tablets, solution for injection)

- Levodopa + benserazide (capsules)

- Levodopa + carbidopa (tablets)

- Trihexyphenidyl (tablets)

Sedatives and anxiolytics, drugs for the treatment of psychotic disorders:

- Haloperidol (tablets, solution for injection)

- Diazepam (tablets, injection solution, suppositories)

- Zuclopenthixol (tablets, solution for injection)

- Clozapine (tablets, injection solution)

- Levomepromazine (tablets, solution for injection)

- Lorazepam (tablets)

- Medazepam (tablets, granules, capsules)

- Nitrazepam (tablets)

- Periciazine (drops, capsules)

- Perphenazine (tablets)

- Pipothiazine (solution for injection, drops)

- Sulpiride (tablets, injection solution, capsules, oral solution)

- Thioproperazine (tablets, solution for injection)

- Thioridazine (tablets, dragees)

- Trifluoperazine (tablets, solution for injection)

- Phenazepam (tablets, solution for injection)

- Fluspirilene (solution for injection)

- Fluphenazine (solution for injection)

- Chlorpromazine (tablets, injection solution, dragees)

- Chlorprothixene (tablets)

Interesting information: Documents required for tax deduction

Antidepressants and mood stabilizers:

- Amitriptyline (tablets, injection solution, dragees)

- Imipramine (tablets, dragees, solution for injection)

- Clomipramine (tablets, dragees, solution for injection)

- Lithium carbonate (tablets, capsules)

- Maprotiline (tablets, dragees, solution for injection)

- Mianserin (tablets)

- Moclobemide (tablets)

- Sertraline (tablets)

- Tianeptine (tablets)

- Fluoxetine (tablets, capsules)

- Citalopram (tablets)

Medicines for the treatment of sleep disorders: Zolpidem in tablet form.

Medicines for the treatment of multiple sclerosis:

- Glatiramer acetate (lyophilized powder for injection)

- Interferon beta (lyophilized powder for injection)

Means for the treatment of alcoholism and drug addiction:

- Naloxone (injection solution)

- Naltrexone (tablets, capsules)

Anticholinesterase drugs:

- Distigmine bromide (tablets, solution for injection)

- Neostigmine methyl sulfate (tablets, solution for injection)

- Pyridostigmine bromide (tablets, dragees, solution for injection)

Other drugs affecting the central nervous system:

- Vinpocetine (tablets, solution for injection)

- Hexobendine + etamivan + etophylline (tablets, solution for injection)

- Nimodipine (tablets, solution for infusion)

Means for the prevention and treatment of infections

Antibacterial:

- Azithromycin (tablets, powder, syrup)

- Amikacin (powder for injection, solution for injection)

- Amoxicillin + clavulanic acid (solution for injection)

- Ampicillin (tablets, capsules, powder for injection)

- Benzathine benzylpenicillin (powder for injection)

- Benzylpenicillin (powder for injection)

- Vancomycin (powder for injection)

- Gentamicin (ointment, cream, injection solution, eye drops)

- Josamycin (tablets, suspension)

- Doxycycline (tablets, capsules, powder for injection)

- Imipenem (powder for injection)

- Carbenicillin (powder for injection)

- Clarithromycin (tablets)

- Co-trimoxazole (tablets, suspension, solution for injection)

- Lincomycin (capsules, ointment, solution for injection)

- Meropenem (powder for injection)

- Mesalazine (suspension)

- Mupirocide (ointment)

- Norfloxacin (tablets, eye drops)

- Pefloxacin (tablets, solution for injection)

- Spiramycin (tablets, granules for suspension)

- Sulfacetamide (eye drops)

- Chloramphenicol (tablets, capsules, powder for injection, eye drops)

- Cefaclor (capsules, granules, syrup, suspension)

- Cefaperazone (powder for injection)

- Cefipime (powder for injection)

- Cefotaxime (powder for injection)

- Ceftazidime (powder for injection)

- Ceftriaxone (powder for injection)

- Cefuroxime (powder for injection)

- Ciprofloxacin (tablets, injection solution, eye drops)

- Erythromycin (tablets, ointment, syrup, ampoules)

Anti-tuberculosis drugs:

- Isoniazid (tablets, solution for injection)

- Lomefloxacin (tablets)

- Pyrazinamide (tablets)

- Prothionamide (tablets)

- Rifabutin (capsules)

- Rifampin (capsules, powder for injection)

- Streptomycin (powder for injection)

- Ethambutol (tablets, dragees)

- Ethionamide (dragée)

Antiviral agents:

- Acyclovir (tablets, ointment, cream, powder for injection)

- Ganciclovir (capsules, powder for injection)

- Didanosine (tablets, powder for oral solution)

- Zidovudine (capsules, syrup, solution for injection)

- Indinavir (capsules)

- Ifavirenz (capsules)

- Lamivudine (tablets, solution for internal use)

- Nevirapine (tablets, suspension)

- Stavudine (capsules, powder for oral solution)

Antifungal agents:

- Amphotericin B (ointment, powder for injection)

- Amphotericin B + methylglucamine (tablets)

- Griseofulvin (tablets, liniment, suspension)

- Itraconazole (capsules)

- Clotrimazole (vaginal tablets, cream, aerosol, solution)

- Terbinafine (tablets, cream)

- Fluconazole (capsules, solution for injection)

Antiprotozoal and antimalarial drugs:

- Hydroxychloroquine (tablets)

- Metronidazole (tablets, injection solution, suppositories)

- Chloroquine (tablets, injection solution)

- Bifidumbacterin in the form of tablets and powders for the preparation of suspension.

Vaccines and serums:

- Immunobiological preparations (for the diagnosis and prevention of infectious diseases in accordance with the epidemiological situation in the constituent entities of the Russian Federation)

- AIDS diagnostic system test

Antineoplastic, immunosuppressive and related drugs

Cytostatic agents:

- Azathioprine (tablets)

- Aranose (powder for injection)

- Asparaginase (powder for injection)

- Bleomycin (powder for injection)

- Busulfan (tablets)

- Vinblastine (lyophilized powder for injection)

- Vincristine (lyophilized powder for injection, solution for injection)

- Vinorelbine (solution for injection)

- Gemcitabine (lyophilized powder for injection)

- Hydroxyurea (capsules)

- Dacarbazine (powder for injection)

- Dactinomycin (powder for injection, solution for injection)

- Daunorubicin (powder for injection)

- Doxorubicin (powder for injection)

- Docetaxel (concentrate for injection solution)

- Idarubicin (capsules, lyophilized powder for injection)

- Irinotecan (solution for infusion)

- Ifosfamide (powder for injection)

- Calcium folinate (solution for injection)

- Carboplatin (powder for injection, solution for injection)

- Carmustine (lyophilized powder)

- Clodronic acid (capsules, concentrate for the preparation of infusion solution)

- Melphalan (tablets, powder for injection)

- Mercaptopurine (tablets)

- Methotrexate (tablets, powder for injection, solution for injection)

- Mitoxantrone (solution for injection, concentrate for infusion)

- Mitomycin (powder for injection)

- Oxaliplatin (powder for the preparation of infusion solution)

- Paclitaxel (solution for injection, concentrate for infusion)

- Procarbazine (capsules)

- Prospidia chloride (lyophilized powder, ointment)

- Thioguanine (tablets)

- Thiotepa (lyophilized powder for injection)

- Tretinoin (capsules)

- Fludarabine (powder for injection)

- Fluorouracil (solution for injection, concentrate for infusion)

- Chlorambucil (tablets)

- Cyclophosphamide (tablets, dragees, solution for injection)

- Cisplatin (lyophilized powder for injection, solution for injection)

- Cytarabine (powder for injection, solution for injection)

- Epirubicin (lyophilized powder for injection)

- Etoposide (solution for injection)

Hormones and antihormones:

- Aminoglutethimide (tablets)

- Anastrozole (tablets)

- Ganirelix (solution for injection)

- Goserelin (depot capsules)

- Medroxyprogesterone (tablets, granules, injection suspensions)

- Tamoxifen (tablets)

- Triptorelin (injection solution, lyophilized powder for injection solution)

- Flutamide (tablets)

- Cetrorelix (lyophilized powder for injection solution)

Related products:

- Interferon alpha (powder for injection, solution for injection, suppositories)

- Lenograstim (lyophilized powder for injection)

- Molgramostim (lyophilized powder for injection)

- Ondansetrion (tablets, solution for injection)

- Filgrastim (solution for injection)

Drugs for the treatment of osteoporosis

Stimulators of osteoformation:

- Alendronic acid (tablets)

- Alfacalcidol (capsules)

- Calcitonin (powder for injection)

- Calcium carbonate + ergocalciferol (tablets)

Drugs affecting blood

Antianemic drugs:

- Iron hydroxide sucrose complex (solution for injection)

- Ferrous sulfate (tablets, dragees)

- Iron sulfate + ascorbic acid (tablets)

- Folic acid (tablets)

- Cyanocobalamin (injection solution)

- Epoetin beta (solution for injection)

Drugs affecting the blood coagulation system:

- Alpostadil (powder for solution for injection)

- Alteplase (lyophilized powder for injection)

- Heparin sodium (solution for injection)

- Nadroparin calcium (syringes with solution for injection)

- Pentoxifylline (tablets, solution for injection)

- Protamine sulfate (solution for injection)

- Streptokinase (powder for injection)

- Ticlopidine (tablets)

- Phenindione (tablets)

- Enoxaparin sodium (syringes with solution for injection)

Solutions and plasma substitutes:

- Amino acids for parenteral nutrition (parenteral nutrition solution)

- Hemin (concentrate for the preparation of infusion solution)

- Dextrose (solution for injection, solution for infusion)

- Pentastarch (solution for infusion)

Plasma preparations:

- Albumin (solution for infusion)

- Coagulation Factor VIII (powder for injection)

- Clotting factor IX (powder for injection)

Lipid-lowering drugs:

- Simvastatin (tablets)

- Phospholipids + pyridoxine + nicotinic acid + adenosine monophosphate (solution for injection)

Drugs affecting the cardiovascular system

Antianginal agents:

- Isosorbide dinitrate (tablets, capsules, injection solution, aerosol)

- Isosorbide mononitrate (tablets, capsules)

- Nitroglycerin (tablets, capsules, patch, solution for injection)

Interesting information: Tax deduction for pensioners when buying an apartment. Documents and registration procedure

Antiarrhythmic drugs:

- Allapinin (tablets, solution for injection)

- Amiodarone (tablets, solution for injection)

- Atenolol (tablets)

- Metoprolol (tablets)

- Procainamide (tablets, solution for injection)

- Propafenone (tablets)

- Quinidine (tablets)

- Ethacizin (tablets)

Antihypertensive drugs:

- Azamethonium bromide (injection solution)

- Amlodipine (tablets)

- Betaxolol (tablets, eye drops)

- Verapamil (tablets, capsules, dragees, solution for injection)

- Doxazosin (tablets)

- Methyldopa (tablets)

- Nifedipine (tablets, capsules)

- Propranolol (tablets, solution for injection)

- Fosinopril (tablets)

Medicines for the treatment of heart failure:

- Valsartan (tablets)

- Digoxin (tablets, drops, solution for injection)

- Irbesartan (tablets)

- Captopril (tablets)

- Quinapril (tablets)

- Perindopril (tablets)

- Enalapril (tablets, solution for injection)

Vasopressors:

- Dobutamine (lyophilized powder for injection, concentrate for infusion)

- Dopamine (solution for injection, concentrate for infusion)

- Phenylephrine (injection solution, eye drops)

- Ephedrine (injection solution)

Diagnostic tools

X-ray contrast agents:

- Sodium amidotrizoate (solution for injection)

- Barium sulfate + sodium citrate + sorbitol + antifomsilan + nipagin (powder)

- Gadodiamide (injection solution)

- Gadopentetic acid (injection solution)

- Galactose (granules for injection solution)

- Iohexol (solution for injection)

- Iopromide (injection solution)

Fluorescent agents: Sodium fluorescein in the form of a solution for injection.

Radioisotope agents:

- Albumin microspheres, 99mTs (reagent for preparation, lyophilized powder for solution preparation)

- Bromezide, 99Tc (reagent for preparation, lyophilized powder for solution preparation)

- Pentatekh, 99mTs (reagent for preparation, lyophilized powder for solution preparation)

- Pirfotech, 99mTs (reagent for preparation, lyophilized powder for preparing solution)

- Strontium 89 chloride isotonic solution (solution for injection)

- Technefit, 99Ts (reagent for preparation, lyophilized powder for preparing solution)

- Technefor, 99mTs (reagent for preparation, lyophilized powder for solution preparation)

Antiseptics and disinfectants

Antiseptics: Iodine (alcohol solution)

Disinfectants:

- Hydrogen peroxide (solution)

- Chlorhexidine (solution)

- Ethanol (solution)

Drugs for the treatment of diseases of the gastrointestinal tract

Antacids and other antiulcer drugs:

- Omeprazole (capsules)

- Pirenzepine (tablets, solution for injection)

- Famotidine (tablets, solution for injection)

Antispasmodics:

- Atropine (eye drops, solution for injection)

- Drotaverine (tablets, solution for injection)

- Platyfillin (solution for injection)

Pancreatic enzymes: Pancreatin in the form of tablets, capsules or dragees.

Medicines for the treatment of liver failure:

- Artichoke leaf extract (tablets, syrup, injection solution)

- Lactulose (syrup)

Antienzymes: Aprotinin in the form of lyophilized powder and solution for injection.

Hormones and agents affecting the endocrine system

Non-sex hormones, synthetic substances and antihormones:

- Betamethasone (tablets, ointment, cream, drops, solution for injection)

- Bromocriptine (tablets, capsules)

- Hydrocortisone (lyophilized powder for injection, solution for intravenous injection, ointment, lotion)

- Chorionic gonadotropin (powder for injection)

- Desoxycortone (tablets)

- Dexamethasone (tablets, eye drops, injection solution)

- Desmopressin (solution for injection, drops)

- Dihydrotachysterol (capsules, powder for injection solution, drops)

- Clomiphene (tablets)

- Levothyroxine sodium (tablets)

- Levothyroxine + potassium iodide (tablets)

- Liothyronine + levothyroxine + potassium iodide + sodium propyloxybenzoate (tablets)

- Lutropin alfa (lyophilized powder for injection solution)

- Menotropins (powder for solution)

- Methylprednisolone (tablets, powder, ointment, suspension for injection, solution for injection)

- Nandrolone (oil solution for injection)

- Octreotide (injection solution)

- Prednisolone (tablets, powder for injection, ointment, eye drops, solution for injection)

- Somatropin (powder for injection)

- Tetracosactide (injection suspension)

- Thiamazole (tablets)

- Triamcinolone (ointment, tablets, injection suspension)

- Fludrocortisone (tablets, eye ointment)

- Follitropin alfa (lyophilized powder for injection solution)

- Follitropin beta (solution for injection, lyophilized powder for the preparation of injection solution)

- Choriogonadotropin alfa (lyophilized powder for injection solution)

- Cyproterone (tablets, oil solution for injection)

Androgens: Methyltestosterone in tablet form.

Estrogens:

- Hydroxyprogesterone (injection solution, solution in oil)

- Dydrogesterone (tablets)

- Norethisterone (dragés)

- Progesterone (oil solution for injection)

- Ethinyl estradiol (tablets)

Insulin and drugs used for diabetes:

- Acarbose (tablets)

- Glibenclamide (tablets)

- Gliquidone (tablets)

- Gliclazide (tablets)

- Glimepiride (tablets)

- Glipizide (tablets)

- Glucagon (powder for injection)

- Insulin DLD (injection solution)

- Insulin KD (solution for injection, suspension for injection)

- Insulin – Comb (suspension for injection)

- Insulin SRD (suspension for injection)

- Metformin (tablets)

- Pioglitazone hydrochloride (tablets)

- Repaglinide (tablets)

Drugs for the treatment of kidney and urinary tract diseases

Medicines for the treatment of prostate adenoma:

- Alfuzosin (tablets)

- Creeping palm extract (capsules)

- Tamsulosin (capsules)

- Finasteride (tablets)

- Treatments for kidney failure and organ transplantation

- Antithymocyte immunoglobulin (solution for infusion)

- Keto analogues of amino acids (tablets)

- Peritoneal dialysis solution (solution)

- Cyclosporine (capsules, solution, concentrate for infusion)

Diuretics:

- Hydrochlorothiazide (tablets)

- Indapamide (dragées, tablets)

- Mannitol (solution for injection)

- Spironolactone (tablets)

- Furosemide (tablets, solution for injection)

Medicines used for ophthalmological diseases, not listed in other sections

Anti-inflammatory drugs:

- Azapentacene (solution)

- Lodoxamide (eye drops)

- Pyrenoxine (tablets)

- Cytochrome + sodium succinate + adenosine + nicotinamide + benzalkonium chloride (eye drops)

Miotics and glaucoma treatments:

- Dorzolamide (eye drops)

- Pilocarpine (eye drops)

- Timolol (eye drops)

Regeneration stimulants and retinoprotectors: Emoxipine in the form of an injection solution.

Drugs affecting the uterus

Hormonal agents that affect the muscles of the uterus:

- Methylergometrine (tablets, solution for injection, drops)

- Oxytocin (injection solution)

- Pituitrin (solution for injection)

- Ergometrine (tablets)

Other drugs that affect the muscles of the uterus:

- Hexoprenaline (tablets, solution for injection, concentrate for infusion)

- Dinoprost (solution for injection)

- Dinoprostone (injection solution, gel)

Drugs affecting the respiratory system

Antiasthmatic drugs:

- Ambroxol (solution for inhalation and oral administration)

- Aminophylline (tablets, solution for injection)

- Beclomethasone (capsules, aerosol, spray)

- Budesonide (powder for inhalation)

- Ipratropium bromide (inhalation solution)

- Ipratropium bromide + fenoterol hydrobromide (inhalation solution, aerosol)

- Disodium cromoglicate (capsules for inhalation, powder, eye drops)

- Nedocromil (aerosol, eye drops, spray)

- Salbutamol (aerosol, tablets, solution for injection)

- Theophylline (tablets, capsules)

- Terbutaline (aerosol, tablets, powder for inhalation, solution for injection)

- Fenoterol (aerosol, solution for inhalation)

- Epinephrine (injection solution)

Other drugs for the treatment of respiratory diseases not listed in other sections: Acetylcysteine in the form of tablets, granulates, injection solution or aerosol.

Solutions, electrolytes, acid balance correction agents, nutritional products

Nutrient mixtures:

- Lofenalac (nutrition powder)

- Phenyl-free (powder for preparing nutritional mixture)

Electrolytes, acid balance correction agents:

- Potassium aspartate (tablets, solution for injection)

- Potassium iodide (tablets, mixture, solution)

- Potassium chloride (solution for injection)

- Calcium chloride (tablets, solution for injection)

- Magnesium aspartate (tablets, solution for injection)

- Sodium bicarbonate (solution for injection)

- Sodium citrate (powder, solution)

- Electrolyte solutions (solutions for infusion)

Interesting information: Filling out the correct application for a tax deduction for children (Sample)

Vitamins and minerals

Vitamins:

- Menadione (solution for injection)

- Thiamine (tablets, solution for injection)

The mechanism for implementing tax deductions

Required documents

To receive a social tax deduction for the purchase of medicines, you must prepare the following package of documents:

- Tax return in form 3-NDFL for the year in which the taxpayer incurred expenses for the purchase of medicines.

- Certificate from the employer in form 2-NDFL for the corresponding year.

- Documents confirming reasonable expenses for the purchase of medicines (original doctor's prescription and copies of documents confirming the purchase: cash receipts, bank card balance statements, cash receipt orders).

- Application for a tax deduction indicating the bank details of the applicant for transferring the amount of compensation.

Making a deduction for medications

Tax deductions can be obtained in two ways:

- at the end of the year in which the expenses were incurred - at the tax office at the place of residence;

- during the current year - from the employer.

If a taxpayer applies to the tax office, he receives the difference in the amount of tax withheld by the employer, without applying a social deduction and taking it into account using the details specified by him.

When contacting the tax office, it is important to remember that the deadline for applying a social deduction is three years after the end of the year in which the expenses were incurred.

That is, in 2021 you can submit documents for reimbursement of expenses for 2015, 2021 and 2021, and in 2021 - for 2021, 2021 and 2018.

If the taxpayer does not want to wait until the end of the current year, then he can contact the accounting department of his enterprise and reimburse the expenses from the current personal income tax.

First of all, he needs to obtain a notification from the tax office at his place of residence that he has the right to receive a social tax deduction.

To do this, he must provide the tax authority with:

- application for notification;

- copies of the doctor's prescription and cash receipts for payment for medicines.

The tax office is required to issue a notification within 30 days of the right to receive a social deduction, which the employee provides to his employer.

Based on this notification, the accounting department will apply the tax benefit to the ratio of his salary until the end of the current year.

How to return 13% of the cost of any medicines from 2021?

From 2021, you can now receive a social tax deduction for medicines and return 13% of their cost without restrictions. Previously, there was a restriction - drugs had to be on the list established in Decree of the Government of the Russian Federation No. 201. But this list did not include many drugs and patients could not partially return their cost. And now this restriction has been lifted.

Important:

despite the fact that the law came into force on June 17, 2021, you can return 13% of income for the entire 2021, that is, for the entire tax period.

What are the conditions for receiving a social tax deduction for medicines:

1. A person has income subject to personal income tax at a rate of 13% (he receives a salary or, for example, rents out housing). If there is no income, then there is nothing to return.

2. In the same year, when there is income, medications were purchased,

3. Payment for the medications was from one’s own funds (i.e., it is impossible for these medications to be paid for, for example, by the employer).

4. Expenses for medicines are confirmed by documents (sales and cash receipts).

5. The medications were prescribed by a doctor on a special prescription form, and not simply purchased at your own discretion.

Can parents get back 13% of the cost of medicines they buy for their children?

Can spouses return personal income tax when purchasing medicines for each other?

Yes, parents have the right to return personal income tax when buying medicines for a child under 18 years of age, just as spouses can return personal income tax when buying medicines for each other, but in this case, the medicines for the child (or, accordingly, the spouse) must be prescribed by a doctor.

By the way, even when purchasing medications, parents can also return 13% of their cost.

Are vitamins considered drugs?

– the answer to this question usually interests parents.

Yes, vitamins are also medicines, which means that in order to receive a tax deduction and return 13% of the cost of purchased vitamins, you must obtain a prescription for them from a doctor.

The concept of medicines is disclosed in Article 4 of the Federal Law of April 12, 2010 N 61-FZ “On the Circulation of Medicines”, from which it follows that such drugs include substances that come into contact with the human body, penetrate into its organs and tissues, are used including for the prevention and treatment of disease. And vitamins come into contact with the human body and are often used not only for treatment, but also for prevention. Therefore, feel free to ask your doctor for a prescription for vitamins, so that at the end of the year you can return 13% of the cost of the vitamins.

Now comes the hard part for patients and taxpayers.

In practice, not all clinics and not all doctors know how to write prescriptions correctly so that after purchasing medications a person can return 13% of their cost. I know this for sure, because just the other day my mother (Tula) went to the doctor for such a prescription. And it turned out that no one at the clinic really knew anything about it. It was big news for doctors that you can write a prescription for any medicine and get back 13% of its cost. Therefore, be prepared to educate doctors.

So, when you contact your doctor for a prescription, check:

1. The prescription must be written out on prescription forms according to form N 107-1/у (form N 107-у was previously in force, but it has long ceased to be valid).

If a doctor tries to write you a “prescription” on a piece of paper or on some clinic letterhead, do not agree to this, but demand that he draw up the document in the prescribed form. Otherwise, you will not be able to receive a tax deduction and return 13% of the cost of medicines.

2. The attending physician must write a prescription to the patient in two copies, one of which must be presented at the pharmacy when purchasing medications, and the second when applying for a tax deduction to the tax authority (Federal Tax Service at the place of residence).

3. On a copy of the prescription intended for submission to the tax authority, the attending physician affixes the stamp “For the tax authorities of the Russian Federation, Taxpayer INN” in the center of the prescription form; the prescription is certified by the signature and personal seal of the doctor, the seal of the healthcare institution.

Now, after receiving a prescription, do not forget to take not only the cash register receipt, but also the sales receipt when purchasing medications from the pharmacy!

And one last thing that is important to say.

You can receive a social tax deduction for an amount of no more than 120 thousand rubles for one calendar year. This means that the sum of the cost of all medications that you bought for yourself, children under 18 years of age, your spouse or parents for the purpose of receiving a personal income tax refund will not exceed 120 thousand rubles per year. You can buy medicines for a much larger amount, but you can only get a tax refund up to this amount. And the unused balance will not be carried over to the next year.

13% of 120 thousand rubles is 15 thousand 600 rubles. This is the maximum that can be returned when purchasing medications.

Take note of the information and bookmark the site page.

And I wish you and your loved ones health!

Still have questions?

Write or call me!

What you need to know about prescription forms

The prescription form presented when applying for a deduction for the purchase of drugs differs from the pharmacy form. The doctor must write out a prescription for taking medications on two types of prescription forms: for the pharmacy and for the tax authority.

A prescription intended for deduction must be stamped “For the tax authorities of the Russian Federation, Taxpayer INN” (clause 3 of Appendix No. 3 to Order No. 289 of the Ministry of Health of Russia, letter of the Federal Tax Service of Russia dated August 31, 2012 No. ED-4-3/ 14 [email protected] ).

Procedure for receiving a deduction

A taxpayer has the right to apply for START:

1. To the tax authorities at the place of residence (electronically through the portal of the Federal Tax Service or State Services, through Russian Post).

List of documents:

- declaration in form 3-NDFL (in addition to the deduction amount, the form must include information about income and the amounts of accrued and withheld tax received from the employer);

Note: taxpayers who submit a declaration solely for the purpose of obtaining a deduction (i.e., are not required to independently declare their income) are not bound by the deadlines for filing reports established by the Tax Code of the Russian Federation. At the same time, you need to remember that you can apply for START no later than 3 years from the date of the end of the tax period in which the right to the deduction arose.

- prescription from the attending physician in form No. 107-1/u with the stamp “For submission to the Federal Tax Service”;

- checks (payment orders) confirming payment for medicines;

Please note: payment documents must be issued to the person actually paying for the purchase of the medicine, and not to the patient who will take these drugs.

- a document confirming the degree of relationship of the applicant with the family member to whom the medications were prescribed (birth (adoption) certificate of the child, act establishing guardianship of the child, birth certificate of the taxpayer himself, marriage certificate);

- application for a personal income tax refund in the form approved by order of the Federal Tax Service of Russia dated February 14, 2017 No. ММВ-7-8/ [email protected] (Appendix No. 8).

If medicines are purchased as part of a service for receiving expensive treatment, the following must be additionally presented:

- agreement for the provision of paid medical services (if concluded);

- certificate of payment for treatment for submission to the Federal Tax Service.

2. To the employer , having previously confirmed the right to a deduction with the inspectorate.

List of documents to apply to the Federal Tax Service:

- application for receipt of notification in the recommended form given in the letter of the Federal Tax Service of Russia dated January 16, 2017 N BS-4-11/ [email protected] ;

- the documents listed in the previous paragraph confirming the right to deduction (the 3-NDFL declaration is not submitted).

After 30 days, the tax authority will issue a notice of eligibility for START.

List of documents for the employer:

- application for the provision of strategic offensive arms in any form;

- notification of the right to apply a deduction received from the Federal Tax Service.

Subtleties of receiving a deduction when paying by relatives

The law establishes that the person in whose name a doctor’s prescription was written and who purchased the medicines can receive a deduction. However, this rule does not apply to spouses.

A husband or wife can receive a tax benefit for their spouse, regardless of which of them purchased the medications.

As for the purchase of medicines by other relatives, it will be possible to obtain the right to deduction only if you have a notarized power of attorney to perform such actions.

How to get a deduction

To receive a deduction, you must first collect all the necessary documents:

- Doctor's prescriptions (for this you need to obtain two copies of the document from the attending physician, since one of them will remain in the pharmacy). The prescription must have a doctor's seal, as well as a stamp for the Federal Tax Service.

- Checks or other payment documents for the purchase of medicines and payment for medical services, contracts with medical institutions . Also, the completion of treatment can be proven by extracts from medical records and epicrisis. All these documents must be certified by the attending physician.

- Certificate 2-NDFL.

- Declaration 3-NDFL.

- Copy of passport.

- Application for deduction.

Peculiarities of using deductions for medications for expensive treatment

If a citizen receives expensive treatment, then the limit on the amount of tax deduction of 120,000 rubles does not apply. A citizen can receive a treatment benefit in the full amount of his annual income.

Expensive treatment includes operations of various kinds, with the exception of cosmetic ones, organ transplantation, implantation of prostheses or pacemakers.

When carrying out such treatment, it may be necessary to purchase medicines or consumables, in which case their cost can also be counted towards the amount of personal income tax benefits without restrictions.

In order to receive a deduction for the purchase of drugs and consumables for expensive treatment, their cost must be indicated as part of the medical services provided and included in the contract and a certificate from the medical institution.

Non-standard situations

When receiving a deduction for the treatment of children, spouses or parents, the taxpayer is required to confirm the degree of relationship with the relevant documents: marriage certificate, birth certificate.

Non-working pensioners are not entitled to a social deduction. The state pension is not earnings and is not subject to personal income tax; therefore, a non-working pensioner cannot take advantage of the tax benefit for the purchase of medicines.

An elderly person who continues to work in retirement and receives wages from which income tax is withheld has the right to take advantage of a social deduction.

Conditions for obtaining START

You can take advantage of the deduction if certain conditions are met:

1. A citizen must have official income subject to personal income tax at a rate of 13% in the year in which he paid for the medicines.

It should be understood that a deduction is a refund (not a withholding) of tax that has already been paid (to be paid in the near future) to the state on the income of an individual. If a citizen does not have such income, then he is not entitled to a deduction.

In this case, income means not only wages, but also other sources of income. For example: renting out housing.

Important: deductions are not applied to income in the form of dividends (Part 2, Clause 3, Article 210 of the Tax Code of the Russian Federation).

Accordingly, if the pensioner’s only source of income in the year when he paid for medicines is a pension, which is legally exempt from personal income tax, there can be no talk of any deduction. But his employed spouse or child has the right to declare START.

2. The organization (IP) that sold medicines to the citizen is located on the territory of the Russian Federation and has the appropriate license.

3. The deduction is provided for medications from the List approved by Decree of the Government of the Russian Federation dated March 19, 2001 No. 201 (hereinafter referred to as the List).

Implementation of refunds for medicines through the tax office in practice

Before making a decision to reimburse the applicant for the amounts spent on the purchase of medicines, the tax office checks the documents provided within 90 days from the date of receipt. The tax office will notify the applicant by mail of the decision.

Documents can be submitted in person or sent to the tax office by a valuable letter with a list of attachments. If copies of documents are sent by letter (for example, cash receipts for the purchase of medicines, copies of children’s birth certificates), the tax inspector will call the taxpayer with the original documents to confirm the authenticity of the copies provided.

Return algorithm

In order to apply for a refund for compensation or a tax deduction when purchasing medicines, a citizen needs to collect a certain package of documents, fill out the appropriate application and submit it to one of the authorities.

Documents and return application

To receive compensation, you need to collect certain documents for each authority:

- To submit an application to the Social Insurance Fund, you must attach copies of : passport or birth certificate, if the payment is for medicine for children; doctor's prescriptions and receipts for medications; certificate from a medical institution; certificate from work confirming tax payment.

- The employer must provide a medical examination report, doctor's prescriptions and receipts for the purchase of medications. You also need to write an application for a refund of social tax deduction.

- For the tax service, you need to fill out a declaration, provide checks, prescriptions and a certificate of receipt of medical services, a certificate of employment 2-NDFL and an application for a refund.

An application for reimbursement of the cost of medicines or obtaining a tax deduction for them can be written either in free form or on the letterhead of the organization to which it is submitted. It must contain the following information:

- the “header” of the application indicates the name and details of the organization to which the application is being submitted; passport and contact details of the applicant and TIN;

- the main text indicates the reason for the return, the amount spent and the date of the event;

- the appendix contains a list of attached documents;

- At the end of the application the date and signature of the applicant are placed.

A sample application for a tax deduction for treatment can be viewed here.

Application methods

For different categories of citizens, documents are submitted to different authorities:

- Pensioners, disabled people and legal representatives of children can submit an application to the territorial office of the Social Insurance Fund or send it by registered mail.

- Working citizens at their place of registration or residence can contact the tax service . You can also send a registered letter with declared value.

- You can apply for a tax deduction through the accounting department at the citizen’s place of work.

Sample documents

“Application for notification of the right to a social tax deduction.”

“Application to the tax office for a social tax deduction.”

“An application to an employer for a social tax deduction.”

Thus, a working citizen has the right to reimburse the costs of purchasing medicines for himself, his spouse, parents or minor children in the form of a reduction in taxable income for the year in which the costs for medicines were incurred.

The personal income tax benefit can only be applied to medicines included in a special list.

You can receive a tax deduction this year by contacting your employer, or within three years after the end of the year in which the medicines were purchased, at the tax office.

Personal income tax refund

There are 2 ways to return personal income tax:

- To apply for a deduction by contacting the employer: you must send an application to the tax authorities and receive a certificate after 1 month, after which the employer will not withhold personal income tax from the subordinate’s salary;

- Send a declaration next year and receive funds from the budget: the declaration is verified within 3 months, and the transfer of money takes 1 month (you need to fill out an application to receive it).

You can use both methods on the government services portal. Regardless of the deduction option, the package of documents is similar. People who are not employed can apply for a deduction only using the second method.