Kosgu 310 or 340 system unit in 2021

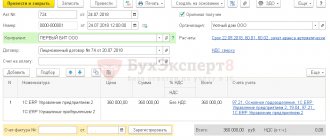

In the specification for the contract, the Contractor indicates: No. Product Unit.

Quantity Price, rub. Cost, rub.1 Photocells (receiver-transmitter) pair 1 1,330.00 1,330.002 Drive with built-in control unit and built-in receiver pcs. Doubts often arise when choosing between 225 and 310 KOSGU (between repair and modernization (reconstruction, retrofitting), as well as between 225 and 226 KOSGU. Why such difficulties arise and how an accountant can “get away with it”, let’s look at the example of work situations.

How to disassemble the OS in “1C: Public Institution Accounting 8”

“The disassembly of a fixed asset object, which is an inventory accounting unit, is reflected at its original (book) value in the debit of account 040110172 “Income from operations with assets” and the credit of the corresponding analytical accounts of account 010100000 “Fixed assets” (010111410 - 010113410, 010115410, 01011841 0 , 010131410 - 010138410) with simultaneous reflection in the debit of the corresponding analytical accounts of account 010400000 “Depreciation” and in the credit of account 040110172 “Income from operations with assets”.

Regulatory regulation

The regulatory documents and methodological explanations of the Ministry of Finance of Russia do not contain information on how to take into account fixed assets resulting from dismantling costing up to 3,000 rubles. for a unit. Therefore, when drawing up a document with the operation Receipt of fixed assets as a result of dismantling (101.xx - 401.10.172), 101.00 objects worth up to 3,000 rubles are written off from the account. inclusive and accounting for off-balance sheet account 21 is not provided.

Personal computers are accounted for as a single automated workstation consisting of:. In this case, a printer, scanner, external modem and other external devices are taken into account as separate fixed assets. It is recommended that the entity's accounting policies provide definitions of key terms and a description of the corresponding accounting procedures. Components of personal computers related to independent fixed assets:.

Accounting for Monitors and System Units in the Budget in 2021

Having considered the issue, we came to the following conclusion: 1. The current legislation in the field of budget accounting does not oblige to take into account monitors and system units exclusively as part of a personal computer (workstation). Therefore, a government agency may decide to account for these material assets as independent objects of fixed assets, justifying its decision. 2. Due to the absence of a code for system units in OKOF OK 013-2021 (SNS 2021), these material assets can be assigned to code 330.28.23.23 “Other office machines” as other machines related to computer equipment. The monitor can be assigned either code 320.26.2 “Computers, peripheral equipment”, or code 320.26.30.23 “Other telephone devices, devices and equipment for transmitting and receiving speech, images or other data, including communication equipment for working in wired or wireless networks communications (for example, local and global networks).”

Rationale for the conclusion: 1. The classification of property into fixed assets is carried out when the criteria listed in paragraphs are met. 7, 8 GHS “Fixed assets”, pp. 38, 39 Instructions No. 157n. One of the main criteria for classifying an object as a fixed asset is its useful life: it must be more than 12 months, but the cost of the property does not matter when classifying it as a fixed asset or inventory. Moreover, according to clause 10 of the GHS “Fixed assets”, the object must be intended to perform certain independent functions. In addition, in accordance with the provisions of the GHS “Fixed Assets”, non-financial assets cannot be classified as fixed assets if they must be accounted for as part of inventories in accordance with the requirements of clause 99 of Instruction No. 157n (see also section 3 “ Methodological recommendations communicated by letter of the Ministry of Finance of Russia dated December 15, 2021 N 02-07-07/84237). An important innovation is that now material value can be taken into account as part of fixed assets, provided that the subject of accounting is predicted to receive economic benefits or useful potential from its use and the initial cost of the material value, as an accounting object, can be reliably assessed (clause. 8 GHS “Fixed assets”). At the same time, in accordance with the provisions of paragraph 5 of clause 10 of the GHS “Fixed Assets,” a unit of accounting for fixed assets may be recognized as part of an item of property if: - in relation to this part, you can independently determine the period of receipt of future economic benefits and useful potential; - this is a part of the property that has a useful life that is different from the remaining parts (a method of obtaining future economic benefits or useful potential); — the cost of part of the property is a significant amount of the total value of the property. Moreover, such a unit of accounting for fixed assets is determined regardless of the possible physical isolation of part of the property. It should be noted here that accounting for monitors and system units as separate inventory objects has always been a topic of controversy and discussion. Moreover, specialists from the financial department have previously given explanations for quite a long time about the need to record them together as single inventory items. Such recommendations were also given for organizations in the non-profit sector (see, in particular, letters from the Department of Tax and Customs Tariff Policy of the Ministry of Finance of Russia dated October 29, 2021 N 03-03-01-04/1/89, dated June 2, 2021 N 03-03- 06/2/110). At the same time, the courts, when considering such disputes, previously took both the side of institutions (for example, the resolution of the Eighth Arbitration Court of Appeal dated December 7, 2021 N 08AP-8357/11) and the side of regulatory authorities (for example, the resolution of the Federal Antimonopoly Service of the East Siberian District dated March 19, 2021 N F02-601/12 in case N A74-919/2021). Recent judicial practice (for example, the ruling of the Volga-Vyatka District Court of December 26, 2021 N F01-6014/17 in case N A29-1287/2021), supported by the Supreme Court of the Russian Federation (determination of the Supreme Court of the Russian Federation dated April 26, 2021 N 301-KG18 -3857), indicates the possible accounting of monitors and system units both as separate fixed assets and as single inventory objects. Based on the analysis of regulations, the court comes to the conclusion that each of the disputed objects (system units and monitors) operated by the institution as part of workplaces does not lose its functional purpose outside the complex: they are suitable for installation in various configurations and are easily replaceable; will not become unusable when disconnected from the complex and can be used as part of another complex; the monitor and the system unit are not a single whole, are not mounted on the same foundation and do not have common control; replacement and relocation of system units and monitors is possible without any damage to their purpose and can be carried out based on the determined feasibility of production activities. Accordingly, system units and monitors can be taken into account not only exclusively as a single object of fixed assets - a personal computer, but also as independent fixed assets as separate structurally separate items intended to perform certain independent functions. Thus, regulations in the field of budget accounting do not oblige monitors and system units to be taken into account exclusively as part of the personal computer they form. Accounting for system units and monitors as separate fixed assets is possible and should be determined by the decision of the institution’s specialized commission. Uniform norms and criteria for making relevant decisions by the relevant commission, in order to eliminate possible doubts, should be established by the accounting policy of the institution. So, for example, if an institution purchases components to assemble them into one computer, then in this case it would be advisable to account for them as a single inventory item. If the specific use of computer components and technical characteristics require their separate accounting, then the current legislation does not limit the institution in this right. At the same time, any decision of the relevant commission must be justified and reasoned, and the approach to accounting for fixed assets that are used in the same way must be uniform. 2. Note that in the All-Russian Classifier OK 013-2021 (SNS 2021), adopted and put into effect by order of Rosstandart dated December 12, 2021 N 2021-st (hereinafter referred to as OKOF OK 013-2021 (SNS 2021)), there are separate codes for system There are no blocks or monitors. Therefore, if a government agency decides to account for these material assets as separate objects of fixed assets, then to determine OKOF codes it is necessary to refer to the direct and reverse transitional keys between the editions of OK 013-94 and OK 013-2021 (SNA 2021), approved by order Rosstandart dated April 21, 2021 N 458. Workstations (personal computers) in accordance with the old OKOF belonged to the group “Electronic computing equipment” (code 14 3020210). The provisions of OK 013-94 made it possible to identify the component parts of computers as separate objects of fixed assets, in particular: - a monitor could be classified as code 14 3020350 (information display devices); - the system unit could be classified as code 14 3020260 (processors, operating devices). However, the forward and reverse transition keys indicate that processors and operating devices (code 14 3020260) are no longer fixed assets for OKOF OK 013-2021 (SNS 2021), but information display devices (code 14 3020350) in OKOF OK 013-2021 (SNA 2021) belong to the subgroup “Computers, peripheral equipment” (code 320.26.2). At the same time, OKOF does not regulate the procedure for classifying objects as fixed assets, so it would be a wrong decision to be guided by its provisions when classifying property as fixed assets. If the relevant commission decides to account for monitors and system units separately, then the forward and reverse transition keys indicate that electronic computing technology (code 14 3020210) in OKOF OK 013-2021 (SNA 2021) is compared with code 330.28.23.23 “Machines” office others." Therefore, due to the absence of a code for system units in the new OKOF, these material assets can be attributed to code 330.28.23.23. According to the transition keys for monitors, code 320.26.2 “Computers, peripheral equipment” is proposed, but it is a grouping. A more detailed code, close in semantic meaning to monitors, may be code 320.26.30.23 “Other telephone devices, devices and equipment for transmitting and receiving speech, images or other data, including communication equipment for working in wired or wireless communication networks (for example, local and global networks)". This or that choice of code for a government institution should be fixed as part of the formation of accounting policies.

We recommend reading: Help for a Young Family from the State in Belarus

We take into account spare parts and components for computer equipment

The list of goods (works, services), the placement of orders for supplies (execution, provision) of which is carried out through an auction, includes a code according to the All-Russian Classifier of Types of Economic Activities, Products and Services (OKDP) 3000000 “Office, accounting and electronic computer equipment” (including spare parts and components for computer equipment). Thus, placing an order for the purchase of spare parts and components for computer equipment should be carried out through an open auction in electronic form.

In accordance with paragraph 41 of Instruction No. 157n [1], an object of fixed assets is an object with all fixtures and accessories, or a separate structurally isolated object intended to perform certain independent functions, or a separate complex of structurally articulated objects that constitute a single whole and are intended to perform a certain job. A complex of structurally articulated objects is one or more objects of one or different purposes, having common devices and accessories, common control, as a result of which each object included in the complex can perform its functions only as part of the complex, and not independently. According to paragraph 45 of Instruction No. 157n, the unit of accounting for fixed assets is an inventory object, also with all fixtures and accessories, or a separate structurally isolated item, or a separate complex of structurally articulated items.

Accounting for system units and monitors

When replacing components at the site where the computer is constantly used, do not draw up an acceptance certificate for repaired, reconstructed and modernized fixed assets (f. 0504103). But if you hand over the computer to the repair service of an institution or a contractor, draw up such a report.

The fact is that drawing up an act (f. 0504103) is mandatory to reflect the fact of acceptance (transfer) of the fixed asset from the customer to the contractor (Methodological instructions, approved by order of the Ministry of Finance dated March 30, 2021 No. 52n). That is, if you handed over the computer for repair to a contractor or to an institution’s repair service.

Form OS-6. Inventory card for fixed assets

The inventory card for accounting for fixed assets, form OS-6, shows the presence of an object on the balance sheet of the enterprise and reflects all its movements within the organization.

This form is filled out by the responsible accountant for each fixed asset item received by the enterprise. Form OS-6 is filled out in one copy.

Form OS-6 is issued for one object. For a group of fixed assets, the standard form OS-6a is used. For small enterprises, a separate simplified form is provided - inventory book OS-6b, which combines information about all objects of the organization.

The standard form of the inventory card OS-6 was developed by the State Committee of the Russian Federation on Statistics and approved by Resolution of the State Statistics Committee of the Russian Federation dated March 21, 2001 No. 7.

The standard form can be supplemented with new lines, but you should not forget to fix the changes in the standard form in the Order on Accounting Policies. You cannot remove existing details from the form; you can only change the size of the lines and column.

Inventory card OS-6 – (excel) free.

Please note: you can fill out OS-6 for the received fixed asset at the bottom of the article.

Who fills out the inventory card form OS-6?

This document must be filled out without fail by all organizations (small enterprises can use the inventory book OS-6b) for fixed assets. The exceptions are credit institutions and budget institutions.

What information is reflected on the inventory card?

Form OS-6 contains information about:

- Receipt of fixed assets;

- Movements between departments (internal);

- Carrying out repairs;

- Carrying out reconstruction, modernization;

- Conducting a revaluation of value;

- Disposal, write-off.

What is needed to fill out the inventory form OS-6?

For the initial filling out of the inventory card according to the unified form OS-6, the following documents will be required:

To enter information about the movements of a fixed asset into the inventory card, the following documents may be required:

- Write-off act – upon departure from the organization as a result of write-off;

- Certificate of acceptance and transfer - when transferring an object to other persons;

- Certificate of acceptance and delivery of repaired, reconstructed and modernized objects OS-3 - when carrying out repairs, reconstruction or modernization of fixed assets (download sample);

- Invoice for internal movement OS-2 – when transferring an object between departments;

- Other documents.

The OS-6 inventory card can be filled out manually with a pen. You can complete the document on your computer.

In relation to intangible assets, an intangible asset registration card-1 is filled out; the form and sample can be downloaded here.

Sample of filling out an inventory card form OS-6

Initial data:

On May 12, 2015, Artel LLC purchased a new T-33 lathe for a fee for use in the machine shop. On September 12, ongoing repairs were carried out, repair costs were 10,000.

The machine has the following parameters:

- Third depreciation group;

- The sum of all acquisition costs is 100,000;

- Useful life is 7 years.

When accepting a new fixed asset, an OS-1 acceptance and transfer act must be drawn up, on the basis of which the OS-6 form is filled out.

Instructions for filling out the inventory card

The machine is new, which means it has not been used before.

“Head” of the OS-6 form card:

- Name of the organization that purchased the machine (Artel LLC);

- Name of the department where the machine was received (machine shop);

- The name, its brand, series, type of object, according to the acceptance certificate (T-33 lathe);

- No. of depreciation group (3);

- Registration, serial and inventory numbers;

- Date of acceptance for accounting (05/12/2015);

- Account number to which the object was debited (01 – fixed assets account);

- Location of OS (machine shop);

- Manufacturer's name - according to the documentation.

Section 1 Form OS-6 – information about the fixed asset as of the date of transfer.

This section of the inventory card is filled out for used fixed assets based on the data of the transferring party. The section is not filled in for new objects.

Section 2 of the inventory card - information as of the date of receipt:

- Initial cost is the sum of all expenses incurred by the organization when purchasing a fixed asset (cost of operating systems, transportation costs, installation, assembly, testing costs, etc.);

- Useful life is determined based on the depreciation group of the object.

Section 3 of the inventory card – revaluation.

Revaluation is a change in the value of a fixed asset at which it is accounted for, carried out periodically to match the accounting value with the real one.

For each revaluation carried out, you must indicate on the inventory card form:

- Date of its holding;

- Conversion factor;

- Replacement cost is the new cost of the object, which will be listed on account 01.

Filling out section 4 of the inventory card - “movements”

Information about all internal movements (between departments), as well as disposals as a result of write-offs and sales, are entered in this section of the OS-4 form.

For each operation as a result of which the fixed asset changes its location, you must indicate:

- Name, number and date of the document of the basis for moving the fixed asset;

- Type of operation;

- Unit name;

- The residual value of a fixed asset is the difference between the original depreciation and the depreciation accrued to this date;

- Full name of the person responsible.

Section 5 form OS-6 - information about modernization, reconstruction, as a result of which the initial cost of the object changes.

For each operation that changes the value of a fixed asset, you must indicate on the inventory card:

- Type of operation;

- Details of the foundation document;

- Expenses.

Section 6 of the inventory card - repair costs

In this section of the OS-6 form, information is filled out about what kind of repair work was performed, on the basis of what document (for example, a defective statement).

Section 7 – brief description of the fixed asset

Any specific information that most fully describes the main asset can be reflected here:

- Availability of precious metals;

- Names of structural elements and their characteristics.

The completed OS-6 inventory card form can be downloaded from the link below.

and a sample of filling out the OS-6 form

inventory card for accounting of fixed assets, form OS-6 – excel.

Sample of filling out an inventory card form OS-6 – download for free.

Accounting for computer equipment in a budgetary institution

Today it turned out that “funds were allocated only for 310.” Having found out what this is all about (since I am very far from accounting), I realized that I cannot purchase 90% of what was planned, because: 1. Components are MZ (Article 340) 2. Monitor - this is also MZ. 3. The projector is the MZ. .

Answer

: The monitor can be accounted for as an independent inventory item (according to the accounting policy), that is, as an independent fixed asset, and, accordingly, its acquisition must be reflected under article KOSGU 310.

SUBTLETS OF BUDGET ACCOUNTING IN EDUCATIONAL INSTITUTIONS WHEN PURCHASING A COMPUTER AND PARTS FOR IT

The rapid development of technology and information technology has led to the fact that now almost no organization can do without the use of computer technology. Educational institutions purchase computers not only for management purposes, but also for educational purposes, equipping computer classes, libraries, and laboratories. Therefore, we have prepared this article, which discusses the issues that an accountant of a budgetary educational institution faces in connection with the purchase of a computer.

In addition to these items, other items and accessories can be purchased separately, such as speakers, a mouse pad, etc. To output information onto paper, a printer can be purchased; to enter graphic and other information from paper into a computer, a scanner is needed; plotters and other objects can also be purchased. The computer is the main tool - no one argues with this. In accordance with the All-Russian Classifier of Fixed Assets OK 013-94, electronic computer equipment (code 14 3020210), which includes computers, processors, devices and computer power supplies, peripheral devices and other types of computer equipment, is included in subsection 14 “Machines and equipment". Therefore, in accordance with the Budget Accounting Instructions, purchased computers must be credited to account 0 10104 310 “Increase in the cost of machinery and equipment.” The main problem is the formation of an inventory object as a unit of budgetary accounting of fixed assets. Therefore, you need to figure out what should be considered an inventory object - the entire “complex”, including the system unit, monitor, keyboard, mouse, printer and other devices, or all of these objects separately, or these objects in some combinations. According to clause 18 of Instruction No. 25n, an inventory object of fixed assets is an object with all fixtures and accessories, or a separate structurally isolated object intended to perform certain independent functions, or a separate complex of structurally articulated objects representing a single whole intended to perform a certain work. A complex of structurally articulated objects is one or more objects of the same or different purposes, mounted on the same foundation, as a result of which each object included in the complex can perform its functions only as part of the complex, and not independently. Of course, the system unit, monitor, keyboard and mouse must be assembled together to function as a computer. After all, if the system unit is not connected to the monitor, the user will not see what the computer is doing, and if the keyboard and mouse (or at least one of these devices) are not connected, the user will not be able to control what is happening on the monitor screen and in the “bowels” of the system block, open programs and documents, type text, etc. But if a printer is not connected to the computer, this will not affect the performance of the computer - the user will simply not be able to output the documents he has created onto paper, and he will have to save the documents on floppy disks, disks or flash drives and take them to another computer for printing . But, on the other hand, the printer itself, without being connected to the computer, is virtually useless. However, due to the fact that the printer can be moved from place to place (connected to one or another computer) or act as a network object (when formally the printer is “connected” to one computer, but documents can also be submitted for printing from other computers connected to a network), it can be considered as an independent inventory object.

Replacing an old system unit with a new one in a public sector institution in accordance with the FSB

An inventory item may be recognized as a part of a property in relation to which the period of receipt of future economic benefits and useful potential can be determined. But the following conditions must be met:

If the accounting policy does not establish a procedure for accounting for the replacement of components of an OS object that have a significant cost, but writes off the cost of a broken system unit as an expense or, conversely, increases the cost of a computer by the cost of a new system unit without reducing the residual value of the failed part, then you can get a remark from the inspectors. Indeed, in such cases, the book value of the computer may be either underestimated or overestimated.

We recommend reading: Reprimand for Disturbing Behavior

Budget accounting in 1C: dismantling and partial liquidation of OS

- for another fixed asset costing from 10,000 to 100,000 rubles. inclusive, depreciation is charged in the amount of 100% of the original cost when it is put into operation;

- for a library fund object worth up to 100,000 rubles. inclusive, depreciation is charged in the amount of 100% of the original cost when it is put into operation.

It should also be taken into account that the OS facility, part of which was liquidated, has already been put into operation.

Account correspondence

On the “General” tab, the data of account 401.10 is indicated, in correspondence with which the receipt of fixed assets is reflected. On the next tab “Capital investments” the OS obtained as a result of dismantling are indicated.

Paragraph 158 of Instruction No. 174n has been supplemented with a new paragraph. The accrual of future income in the amount of subsidies for the implementation of state (municipal) tasks on the basis of relevant agreements concluded with the founder is reflected by the entry:

Accounting for monitors and system units as separate inventory objects

Only those items that the computer can operate without and that meet the criteria for a fixed asset can be taken into account as separate fixed asset objects. For example, a printer - OKOF code 330.28.23.23 “Other office machines.” After all, the computer will work without it. As well as those components that the institution plans to operate as part of various sets of computer equipment. For example, if you plan to connect the monitor to different computers.

Institution - State Autonomous City of Moscow Information Technology Center. Is it possible to account for monitors and system units (SU) as separate inventory items of fixed assets. In practice, monitors or SBs are often changed due to production needs. Some workplaces have 1 SB and two monitors. There is no need to write them off; they are used at other workplaces.

Budgetary Institution Purchasing Computer Components

At the same time, it should be noted: in addition to the obligation to use exclusively an auction as a method of conducting bidding, budgetary institutions have the right to place an order for the purchase of spare parts and components for computer equipment without bidding (including by requesting quotations or from a single supplier (contractor) ) subject to the restrictions for the use of these procedures established by Federal Law N 94-FZ.

Thus, spare parts and components for computer equipment purchased by a budgetary institution, including monitors and system units, are not fixed assets and should be taken into account as part of inventories, since they can perform their functions exclusively in associated sets. Let us recall that material reserves include items used in the activities of a budgetary institution for a period not exceeding 12 months, regardless of their cost, finished products, goods for sale (clause 98 of Instruction No. 157n). In addition, inventory includes equipment that requires installation and is intended for installation. Requiring installation includes equipment that can be put into operation only after assembly of its parts, as well as sets of spare parts for such equipment.

Which depreciation group does a computer in the Russian Federation belong to in 2021?

If any structurally articulated object has several components (in particular parts) - OS, with different periods of use, each component is taken into account as a separate inventory object.

According to the Instructions, the definition of useful life period means the period during which it is possible to use, during the work of the organization, an object of non-financial assets for the purposes for which it was purchased, formed or received.

How to take into account the keyboard and mouse in the accounting of a government agency

Using Article 310, you can purchase a computer (monitor, system unit, keyboard, mouse). Thus, in particular, the useful life of non-financial assets for the purpose of accounting for fixed assets and depreciation can be determined based on the information contained

We recommend reading: Sample application form for employment sample

Description

Question: Under what article of KOSGU should the costs of purchasing a system unit, monitor, keyboard, mouse, power supply be reflected as one object of accounting for the main items Article: Tax aspects of the activities of 'new' budgetary and government institutions (Salina L.) ('Budget organizations: accounting accounting and Source: "Government institutions. Accounting. Reporting. Taxation" Classifying an object as fixed assets or material Advice to an accountant: In this case, the only acceptable option was to draw up three supply contracts (separately for monitors, for system units, keyboards and mice) so that how to take into account the keyboard and mouse in the accounting of a state institution as part of the automated workplace, in_ the year they continue to be reflected in accounting, as before. Source: magazine “State institutions: accounting, reporting, taxation.” Practical explanations on all issues of the financial and economic activities of a state institution. Klerk.Ru > Accounting > Budgetary, autonomous and government institutions > Budgetary accounting > Mice - what is it, material or operating system. Consequently, in tax accounting, devices (keyboard, system unit, monitor) must be taken into account as separate objects, taking into account the cost limit (clause 1 of Art. How to properly write off a system unit in a government institution in connection with its replacement with a new one, purchased as part of material inventory, if it is part of a computer system (system unit, monitor, keyboard, mouse, uninterruptible power supply - all budget accounting and Instructions for

Examples of application of articles 310 KOSGU and 340 KOSGU in 2021-2021

The costs of purchasing a switch are included in expense item KOSGU 310. The useful life of the switch is more than 12 months. In accordance with OKOF, the switch is included in the group “Communication equipment that performs the function of switching systems (OKOF code – 320.26.30.11.110).

A cartridge is a spare part for a printer, copier, or scanner, that is, a consumable item. Therefore, in accounting it must be reflected as part of inventory under article KOSGU 340. But services for replacing the cartridge are under expense item KOSGU 225.

Purchasing computer components

- if you buy an assembled computer from one supplier, and the acceptance documents indicate its component parts, then the expenses must go under article KOSGU 310 “Increase in the cost of fixed assets.” Using the same code, reflect the costs of equipment that you capitalize separately from the computer (since its presence or absence does not affect the operation of the computer). For example, printer, scanner, etc.;

- Do you buy spare parts for your computer separately from different suppliers and only after assembly do they form a computer? Then take them into account as part of your inventory, just like other spare parts for your computer. And spend expenses according to article KOSGU 340 “Increase in the cost of inventories” (section V of the instructions approved by order of the Ministry of Finance of Russia dated July 1, 2021 No. 65n). That is, when purchasing them you will reflect: Debit 105.36 Credit 302.34

, and when assembling a computer:

Debit 106.31 Credit 105.36

and

Debit 101.34 Credit 106.31

.

This conclusion is confirmed by the Russian Ministry of Finance in letter dated July 23, 2021 No. 02-06-10/2637. At the same time, this letter contains another option when the component parts of the object can be taken into account as independent fixed assets. This is the case when the useful life of the computer components is different from other elements of the complex. But this option is unlikely. After all, the OKOF names the main elements of the computer, and all of them are included in the second depreciation group (that is, they all have the same useful life - three years).

How to write off a monitor

Correctly selected lighting is an integral factor in occupational health and safety. Rational lighting is created by achieving certain regulated parameters - optimal illumination, minimal glare, correct direction of light. All this influences the choice of types and quantities of lighting fixtures used in an institution.

But replacing individual computer elements with new ones due to obsolescence cannot be considered as computer repair and is its modernization. Therefore, for example, replacing an obsolete monitor with a new one is an upgrade.

1C: Accounting for budgetary institutions - (ed.

In the directory “Fixed Assets”, the element “Computer” is created with the type NFA “Fixed Assets”, if you need to capitalize 1 computer. If several completely identical computers are being assembled, then you need to create the element “Capital investments in computers” with the type NFA “Capital investments”.

- Debit account 106.01. KBK debit - the KBK of the FKR type is selected, usually the main KBK of expenses for the type of activity (Budget, off-budget) in which the assembled computer will be used.

- Fixed assets - from the Fixed Assets directory, select an element on which computer costs will be collected.

- Types of NFA movement - “Capitalized from processing.”

- Cost types - from the “Cost types” directory, select an element of the “Material costs” type.

Budget accounting of fixed assets in 2021-2021 (nuances)

To account for fixed assets, a synthetic account 010100000 “Fixed Assets” is provided. The budget accounting account number consists of 26 digits, and only 18–26 digits are used in the accounting of the institution. Depending on the group and type of fixed assets, as well as the essence of their movement, the code in the 22–26 digits changes in the account number.

In accordance with paragraph 21 of Order No. 157n, the concept of “budget accounting of fixed assets” applies only to certain government organizations. For example, government institutions, government agencies, extra-budgetary funds. In addition to the unified chart of accounts, a special chart of accounts must be used in budget accounting (Order of the Ministry of Finance of Russia dated December 6, 2021 No. 162n).

We recommend reading: Chernobyl List of Liquidators and Positions

Purchasing components for a personal computer

Today is the third Sunday in August, so today Russian Air Fleet Day is celebrated throughout the country. Orsk was no exception to this rule. According to established tradition, on this day an event dedicated to the holiday was held on Gagarin Square.

Directory "ZakGo" - tenders, government procurement, government orders, competitive bidding and electronic auctions of Russia in a unified database of government and commercial tenders with daily updates + convenient classifiers of tenders and government procurement based on OKVED and OKDP codes.

Which KVR and KOSGU to use for government procurement

Subsidies (grants in the form of subsidies) for financial support of expenses, the procedure (rules) for the provision of which do not establish requirements for subsequent confirmation of their use in accordance with the conditions and (or) purposes of the provision

Subsidies (grants in the form of subsidies) for financial support of costs in connection with the production (sale of goods), performance of work, provision of services, the procedure (rules) for the provision of which establishes a requirement for subsequent confirmation of their use in accordance with the conditions and (or) purposes of the provision

We take into account spare parts and components for computer equipment

Lists of goods, works, services, placement of orders, respectively, for supplies, implementation, provision of which are carried out through an auction, are determined by Order of the Government of the Russian Federation No. 236-r [3] . It should be noted that if goods, works, services are included in the specified lists, placing orders for the supply of such goods, performing such work, providing such services for the needs of customers through a competition is not allowed. Moreover, according to Part 4.2 of Art. 10 of Federal Law No. 94-FZ, the placement of such orders should be carried out not simply through an auction, but through an open auction in electronic form.

In accordance with paragraph 41 of Instruction No. 157n [1], an object of fixed assets is an object with all fixtures and accessories, or a separate structurally isolated object intended to perform certain independent functions, or a separate complex of structurally articulated objects that constitute a single whole and are intended to perform a certain job. A complex of structurally articulated objects is one or more objects of one or different purposes, having common devices and accessories, common control, as a result of which each object included in the complex can perform its functions only as part of the complex, and not independently. According to paragraph 45 of Instruction No. 157n, the unit of accounting for fixed assets is an inventory object, also with all fixtures and accessories, or a separate structurally isolated item, or a separate complex of structurally articulated items.

Purchase of a System Unit in Kosgu 2021 for Budgetary Institutions

Doubts often arise when choosing between 225 and 310 KOSGU (between repair and modernization (reconstruction, retrofitting), as well as between 225 and 226 KOSGU. Why such difficulties arise and how an accountant can “get away with it”, let’s look at the example of work situations.

Since KVR is a larger grouping than KOSGU, to simplify the application of the corresponding codes, the Ministry of Finance has approved a correspondence table. A comparison of CVR codes and KOSGU codes for 2021 for budgetary institutions and public sector organizations is presented in a table. The document contains the latest changes that should apply in 2021.

KOSGU presents an option for grouping operations that are carried out by government agencies in accordance with their economic essence.

Build a gaming computer 2021

Parts of different generations that are similar in appearance have different slots for installation, which will not allow the device to be mounted correctly. To avoid such errors, system unit assembly configurators were created, which make it possible for to assemble a budget gaming computer .

WHERE TO START ASSEMBLYING A COMPUTER?

— The processor is the “brain” of any computer. It affects its speed and performance. The most technologically advanced and more expensive models are those produced by Intel, while the more optimal and budget ones are those produced by AMD.

Section structure: income, expenses, investment fund, return of subsidy balances and expenses of previous years. Consolidation: by the parent institution, founder, financial authority. The purpose of the Report on the institution's obligations (f. 0503738) is to compare the annual volumes of planned assignments for expenses and financial assets with data on the obligations and performance of accepted subsidiaries. Sections of the report: obligations of the current year for expenses, obligations of the current year for the investment fund, obligations of the next years. Report indicators: assumed liabilities, assumed liabilities, assumed monetary obligations (MO), deferred obligations.

The beginning - the first stage of the implementation of five federal accounting standards out of 29 - is a key event in 2021 for the accounting community and especially for public sector institutions, which then included government, budgetary and autonomous institutions. The second stage - five more standards in 2021, and the third - five more from 2021. In three years - 15 rebus standards! There are 7 standards left for 2021 and 2022. New key concepts, accounting objects, fundamentally new approaches to the formation of professional judgment in the field of budgetary and accounting are no longer so scary today. Indeed, after three years, all significant changes, even to the basic Conceptual Framework standard with Leases, Property, Plant and Equipment and Impairment, seem clear. It’s not for nothing that they say that the one who walks can master the road. Not just walking, but “using the navigator”, with the help of our long-time Advisor, accountant and chief regulator - the Ministry of Finance of Russia. We can say that our main asset is professional accountants and financiers who keep records and prepare reports, promptly identify and correct errors according to new standards, and strive for the establishment, founder and reputational capital of the Russian budget of the country. As one leader said at the beginning of the reforms, making money from these people - there would be no stronger ruble in the world!

Standards from 2021

For state (municipal) budgetary and autonomous institutions, budget information includes information on the approved indicators of the institution’s FCD plan, on other planned indicators of the activities of the budgetary, autonomous institution approved for the corresponding year (hereinafter referred to as planned assignments). Here is a comparison of the list of budget information for recipients of budget funds (BFR) contained in the Budget Code of the Russian Federation and the GHS.

- The property is actively used in the activities of the economic entity. Or the asset was leased for a certain fee.

- The object is capable of generating profit/income in future periods.

- The valuables were not acquired for resale, but specifically for the company’s own needs.

- It is planned that the asset will be used for at least 12 months. We are talking about SPI (useful life).

- The cost of the object is not lower than the established limits:

- for accounting - 40,000 rubles and above;

- for tax accounting - 100,000 rubles and above.

Computer in budget accounting

The federal government agency has a large fleet of computer equipment. Some personal computers are accounted for in budget accounting registers as a single fixed asset object. In addition, system units and monitors are taken into account on the institution’s balance sheet as separate independent objects of fixed assets.

A similar position is confirmed by the Letter of the Ministry of Finance of Russia dated October 21, 2021 No. 02-14-10a/ 2902. From recent documents, you can use the Letter of the Treasury of the Russian Federation dated June 27, 2021 No. 42-7.1-15/2.2-265 “On the application of the budget classification of the Russian Federation in reflection of cash expenses for the modernization of fixed assets.”

How to properly complete a computer on a budget and with what wiring

The material was prepared on the basis of individual written consultation provided as part of the Legal Consulting service. *(1) Order of the Ministry of Finance of Russia dated March 30, 2021 N 52n “On approval of forms of primary accounting documents and accounting registers used by public authorities (state bodies), local governments, management bodies of state extra-budgetary funds, state (municipal) institutions, and Methodological guidelines for their application" (hereinafter referred to as Order No. 52n), which came into force on June 19, 2021, replaces Order No. 173n of the Ministry of Finance of Russia dated December 15, 2021 (hereinafter referred to as Order No. 173n), which also established the forms of primary documents and accounting registers for public sector organizations. A new document is used when developing accounting policies starting from 2021 (clause 6 of Order No. 52n).

We recommend reading: Compensation for utilities for labor veterans in Klina

Instructions for the application of the Unified Chart of Accounts for public authorities (state bodies), local governments, management bodies of state extra-budgetary funds, state academies of sciences, state (municipal) institutions, approved by Order of the Ministry of Finance of Russia dated December 1, 2021 N 157n (hereinafter - Instruction N 157n)). According to the Instructions on the procedure for applying the budget classification of the Russian Federation, approved by Order of the Ministry of Finance of Russia dated July 1, 2021 N 65n, the institution’s expenses for the purchase of components are included in article 340 “Increase in the cost of inventories” of the KOSGU, expenses for assembling a computer are in subarticle 226 “Other work, services” and are reflected by expense type 244 “Other purchase of goods, works and services to meet state (municipal) needs”

HOW TO CORRECTLY ACCOUNT SYSTEM UNITS AND MONITORS

In accordance with paragraphs 10 and 11 of Order No. 91n of the Ministry of Finance of Russia dated October 13, 2021 “On approval of guidelines for accounting of fixed assets,” if one object has several parts that have different useful lives, each such part is accounted for as an independent object. According to the technical characteristics (including obsolescence factors), when purchasing electronic equipment (system unit, monitor, keyboard, mice), the institution took them into account as independent objects and assigned a separate inventory number to the monitor and system unit.

In this case, only part of the document is provided for familiarization and avoidance of plagiarism of our work. To gain access to the full and free resources of the portal, you just need to register and log in. It is convenient to work in extended mode with access to paid portal resources, according to the price list.

How to record the purchase of a computer

For accounting purposes, the annual depreciation rate for the system unit is 33.3333 percent (1: 3 × 100%), the annual depreciation amount is 34,667 rubles. ((RUB 122,720 – RUB 18,720) × 33.3333%), monthly depreciation amount – RUB 2,889/month. (RUB 34,667: 12 months).

In these two cases, computer equipment, the useful life of which exceeds 12 months, and the cost of which is more than 100,000 rubles, is considered as a separate fixed asset item. Consider the rest of the computer equipment as part of the materials. This procedure follows from subparagraph 3 of paragraph 1 of Article 254 and paragraph 1 of Article 256 of the Tax Code of the Russian Federation.

We recommend reading: Banks That Do Not Cooperate with Bailiffs

Replacing a monitor in a budget or autonomous institution

In fact, with the usual replacement of, for example, a monitor, the functional purpose, quality use and economic characteristics of the computer practically do not change, which does not fully correspond to the concept of modernization defined by the financial department. In any case, the qualification of operations performed by the institution (modernization, repairs) must be carried out by the institution independently.

The operation of replacing a broken and inoperative monitor should be considered as a repair of computer equipment, the costs of which do not increase its original cost. Accordingly, the cost of spare parts used in the repair process is written off to the institution’s expense accounts (accounts 0 109 60 000, 0 109 70 000, 0 109 80 000, 0 109 90 000, 0 401 20 000) using code 272 “Consumption of inventories” » KOSGU. If repair work is carried out by a third-party organization, then the costs of paying for its services are also taken into account in expense accounts, but according to code 225 “Works, services for property maintenance” of KOSGU. Similar rules apply to other parts of computer technology (for example, network cards, CD or DVD drives, motherboards, etc.).

Purchase of goods: computer components

In accordance with the Instructions on the procedure for applying the budget classification of the Russian Federation, approved by Order of the Ministry of Finance of Russia dated July 1, 2021 No. 65n, when an institution purchases not a finished (assembled) computer, but individual parts, the costs of purchasing components (processor, video card, etc.) ) should be carried out according to Article 340 “Increase in the cost of inventories” of KOSGU. When assembling equipment, the cost of components is accumulated on the balance sheet account 0 10601 000 “Capital investments in fixed assets” with further capitalization of the finished computer.

All rights reserved. Full or partial copying of any site materials is possible only with the written permission of the editors of the Health Care magazine. Violation of copyright entails liability in accordance with the legislation of the Russian Federation.

KVR and KOSGU in 2021 for budgetary institutions

Also, in the practice of procurement for several CWR, issues arise with the correct reflection of codes, which is determined by the use of classification. For this case, 34-36 digits of the procurement identification code are formed in a special way: 34-36 digits are set to “0” if these expenses are subject to reflection across several CWR.

Since 2021, KOSGU is not used by recipients of funds when forming plans for income and expenses, but is used in accounting and reporting. In 2021, it is required to apply it to public sector institutions and organizations when drawing up a working chart of accounts, maintaining records and reporting. The procedure for approving the chart of accounts for budget accounting is enshrined in Order of the Ministry of Finance No. 162n (as amended on March 31, 2021).

Purchasing a computer and components

Let us remind you: recently, by the resolution of the Cabinet of Ministers of Ukraine “On amendments to the annex to the resolution of the Cabinet of Ministers of Ukraine dated March 1, 2021 No. 65” dated 08/13/2021 No. 339

(see “Budget Accounting”, 2021, No. 32, p. 4) changes were made to the

Measures for the economical and rational use of public funds provided for the maintenance of public authorities and other government bodies created by public authorities of enterprises, institutions and organizations using state budget funds approved by Cabinet of Ministers Resolution No. 65 dated 03/01/2021.

In addition, the State Treasury Service in a letter dated 07/04/2021 No. 17-08/659-15588

, referring to

the letter of the Ministry of Finance dated May 22, 2021 No. 31-10040-18-10/12445

Activities

for a ban on the purchase of office equipment such as computers, as well as components for them .

How to purchase a wireless call button

Typical errors, latest changes, development prospects

We process personal data lawfully and fairly, acting reasonably and in good faith and based on the principles: For the purposes of this Policy, User's personal information means: Below are some examples of the types of personal data that the Company may collect and how we may use such information .

Examples of application of articles 310 KOSGU and 340 KOSGU

Members of the commission make their decisions based on: • the provisions of the Instructions to the Unified Chart of Accounts No. 157n; • on the purpose, timing and procedure for using material assets; • on the provisions of the accounting policy - it prescribes an exact list of property that is classified as fixed assets or inventories in the accounting of the institution. The KOSGU code depends on the subject of the contract. If these are advertising services, when the contractor himself prepares and places the banner without transferring it to the customer, use subarticle KOSGU 226 “Other work, services.”

If you buy an advertising banner, street banner - KOSGU 310, if the banner meets the criteria of a fixed asset, or article KOSGU 340 - meets the criteria for supplies.

Tender: installation of staff call buttons for wheelchair users

An application for participation in the request for quotation, submitted within the period specified in the notice of the request for quotation, is registered by the customer.

1) the consent of the participant in the request for quotation to fulfill the terms of the contract specified in the notice of the request for quotation, the name and characteristics of the supplied goods in the event of delivery of the goods

What type of non-financial assets - fixed assets or inventories - include a button for entering the building and a device for receiving a call for help, working in conjunction (upon the fact of purchase, an invoice is presented, in which the button and the receiving device are highlighted as separate lines)?

Having considered the issue, we came to the following conclusion: When making this decision, the Commission is guided by the criteria for classifying property as fixed assets, established by the provisions of paragraphs. 38, 39, 41, 45 of the Instruction approved by Order of the Ministry of Finance of Russia dated December 1, 2010 N 157n (hereinafter referred to as Instruction N 157n). According to clause

41 of Instruction No. 157n one of the conditions for classifying an object as a fixed asset is its purpose for performing: - certain independent functions; In addition, as a general rule, items of non-financial assets cannot be classified as fixed assets if they must be accounted for as part of inventories in accordance with the requirements of paragraph.

99 Instructions No. 157n. In particular, according to paragraph. Procedure for making a decision on classifying an object as a fixed asset (for the public sector).

Expert of the Legal Consulting Service GARANT Reviewer of the Legal Consulting Service GARANT Advisor to the State Civil Service of the Russian Federation, 2nd class Anna Shershneva The material was prepared on the basis of individual written consultation provided as part of the Legal Consulting service.

Expenses under a contract concluded within the framework of the Accessible Environment program

The institution develops the act of acceptance and delivery of completed (retrofitted) fixed assets independently.

The act is signed by: members of the commission for the receipt and disposal of assets created in the institution; employees responsible for the completion (retrofitting) of the fixed asset (or representatives of the contractor); employees responsible for the safety of fixed assets after completion (retrofitting).

Code (article) KOSGU: 221

— forwarding of postal items (including the cost of packaging postal items); — payment for stamped postal notifications when sending items with notification; — transfer of pensions and benefits; — forwarding mail using a franking machine; — purchase of postage stamps and stamped envelopes, stamped postal forms; — subscription fee for using mailboxes; courier and special communication services; services of telephone and telegraph, fax, cellular, paging communications, radio communications, Internet providers: - subscription and time fees for the use of communication lines; — fees for providing access and use of communication lines, data transmission via communication channels; — fee for registering an abbreviated telegraph address, faxes, modems and other means of communication; — connection fee and subscription service in the electronic document management system, incl.

using certified cryptographic information protection tools; — payment for the purchase of SIM cards for mobile phones, payment cards for communication services; — fee for the provision of services for booking network resources necessary for connecting to the public network; — payment for communication services for cable and satellite television; — fee for the provision of detailed invoices for payment of communication services provided for in the contract for the provision of communication services; — the tenant’s expenses to reimburse the landlord for the cost of communication services; other similar expenses. Code (article) KOSGU 221 / Classification of operations of the public administration sector / Expenses / Payment for work, services / Communication services

Purchase and installation of a video surveillance system for an accountant

at the expense of budgetary funds; debit KRB 230222830, credit KIF 220101610 funds for issuing a report to a person purchasing components for a video surveillance system as part of budgetary activities were written off from a personal account based on an application; debit KIF 120104510, credit KRB 121003660 cash was received at the cash desk for issue on account when purchasing system components at the expense of budgetary funds; debit KIF 220104510, credit KIF 220101610 cash was issued to an accountable person for the purchase of components for a video surveillance system; debit KRB 010506340, credit KRB 020822660 components for the video surveillance system purchased by the accountable entity were taken into account.

Later, when the contractor completes the installation