What is the inventory procedure?

This is the name of the procedure for checking the quantitative and qualitative characteristics of an institution’s property and the state of its financial obligations on a set date, ensuring control over the safety of fixed assets.

This action is carried out by reconciling actual data with accounting registers, and in the process, a sample order for conducting the annual inventory of 2021 is drawn up. The following regulations regulate the conduct of a property inventory in an organization:

- 402-FZ “On Accounting” dated December 6, 2011;

- Order of the Ministry of Finance No. 49 dated June 13, 1995, approving methodological guidelines for this procedure and regulating the procedure for its implementation.

The institution sets the timing of inventory control independently either in its accounting policies or by separate management orders. So, you will definitely need a sample order for inventory for 2021. As a general rule, the inventory is carried out annually, but not earlier than November 1 (regulations for fixed assets).

Carrying out an inventory and recording its results. Example

→ → Update: February 13, 2021

Inventory is one of the organization’s tools for monitoring its values and obligations. Inventory is carried out at the enterprise annually to adjust accounting information.

Carrying out an inventory and recording its results are approved by orders of the head of the organization. The inventory regulations were approved for inventory (approved by Order of the Ministry of Finance No. 49 of June 13, 1995). The obligation to conduct an inventory is established annually.

The rules for conducting an inventory and recording its results are established in each organization independently and are fixed by orders of the director. Inventory is a procedure for auditing an enterprise’s property, valuables, liabilities and comparing it with accounting data.

Inventory results allow you to adjust accounting information and tax obligations. Identification of inventory results occurs in several stages. Initially, the head of the organization announces the start of an inventory at the enterprise and approves the inventory commission.

The commission may include:

- chief accountant, his deputy, accountant for a certain area of the enterprise;

- members of the administration, representatives of the organization’s management;

- other employees of the organization who are specialists in certain fields (for example, a lawyer, a financial department employee, etc.).

The commission does not include persons responsible financially, but they are present during the audit.

The inventory commission must consist of at least two people. She will be responsible for documenting the inventory results. Before carrying out the audit, the commission must have the latest receipts and expenses documents.

They allow you to record balances before starting the inventory. Receipts

Inventory before annual reporting

Conducted in the 4th quarter. The start date is usually October 1st. The goal is to check the availability of the organization’s property and compare it with accounting data. All assets and liabilities are verified. To carry out this, a sample order for conducting the annual inventory 2021 is drawn up.

If the annual procedure is not carried out, the information in the financial statements will be unreliable. For this, a fine is imposed on both the organization and its officials (Article 120 of the Tax Code of the Russian Federation, Article 15.11 of the Code of Administrative Offenses of the Russian Federation).

Be sure to check:

- property;

- cash;

- obligations;

- settlements with debtors;

- reserves;

- loan balances;

- settlements with personnel.

IMPORTANT!

Conduct an inventory of fixed assets every 3 years, and library collections - once every 5 years.

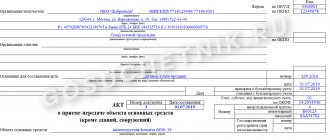

Filling out the fields of the INV-22 form

Drawing up an order (resolution) for inventory is an extremely simple procedure. You will need to include OKPO and the name of the structural unit in the header if we are not talking about general inventory or revaluation, but about reporting on the property of a separate branch. If you plan to conduct inspections in several departments, then INV-22, as well as associated forms, will be compiled for each.

The inventory object can be fixed assets, inventories, liabilities, completed or unfinished construction objects, objects in safekeeping, etc.

We indicate “control check” or, more directly, “scheduled inventory” as the reason for the planned inventory. If personnel changes occur - “change of financially responsible persons” or “reorganization”. The resolution is also completed for cases of revaluation.

In the event of a change in responsible persons, storekeepers, cashiers and other specialists employed at the time of the inspection are indicated.

The timing of the assessment must be precise. The start date cannot be earlier than the document date.

After the INV-22 is completed, it should be entered into the journal using the INV-23 form. But the results of the inspection are entered into the journal using the INV-25 form. These documents can remain in the structural unit or be transferred (in the case we discussed above).

How it goes

The procedure for conducting a property inventory takes place in four stages:

- Preparation. During the preparatory stage, the organization develops a sample order for inventory before the annual report, for example, and also creates an inventory commission, sets the deadlines for the process and determines the OS objects that will be checked.

- Direct verification activities. Members of the commission study the quantitative and qualitative properties of OS objects, check their actual condition and availability, and draw up an inventory.

- The analytical stage, during which accounting data is compared with the results of the assessment process. If discrepancies are discovered by members of the commission, statements are drawn up and results are summed up.

- Registration of the results of checking the availability and current condition of property. Accounting brings accounting data into conformity with the commission's reports, those responsible for the errors are identified, and a measure of responsibility is established.

Please note that during the procedure it is necessary to issue not only an order for inventory according to the new standards, but also other orders. We will also talk about them in the article.

Sample order for inventory

On our website you can fill out the INV-22 form.

An administrative document that launches the procedure for checking the availability of property can be created either in a free form or on a unified form of the INV-22 form. It contains all the basic data necessary to carry out an inventory. Its details will be present in all documents drawn up during the audit.

Be the first to know about important tax changes

Have questions? Get quick answers on our forum!

nalog-nalog.ru

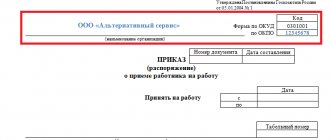

How to draw up an order to conduct an inspection

Before directly assessing an institution’s property, it is necessary to develop a sample order for an inventory of 2021. The manager’s order can be prepared either in any form on the organization’s own letterhead, or using the unified form INV-22 (Resolution of the State Statistics Committee of the Russian Federation No. 88 of August 18, 1998).

In the sample order for inventory 2021, it is necessary to include the details of the document, its name, number and date, information about verification activities, the reason for the assessment of property objects, indicate those values that will be subject to control, and set the deadlines for this process. The document also defines the composition of the commission with the name and job description of each member. One of the common questions is how to correctly indicate the reason for inventory in the order; an example for an annual audit could be: “the need to prepare annual financial statements.” For another case, you can write, for example, “control check”.

A sample order for inventory 2021 is signed by the head of the institution, and then information about it is entered into the INV-23 registration log.

Each employee must put next to his full name. and his/her signature confirming the fact of familiarization with the assessment order. Maximum responsibility for the control activities carried out lies with the chairman of this council.

Inventory order: sample 2021

If the contents of the administrative document for carrying out inventory activities are brought into compliance with the requirements of the law, then the inventory order (sample 2021 is given below) must contain the following information:

- full name of the business entity;

- name of the document (Order), its registration number and date of publication;

- an order to carry out inventory activities, indicating the units where they will be carried out (for example, a general inspection of all units, or a specific warehouse or unit);

- the purpose of the audit is to take an inventory of tangible assets, fixed assets, inventories, accounts receivable, etc.;

- the composition of the audit commission and the appointment of the Chairman of the commission (when external auditors are involved in activities, their role in the commission is indicated. For example: “Ivanov I.I. – member of the commission, invited auditor”);

- timing of the inventory, with an exact indication of its start, end, and date of submission of the Inventory Report;

- information about the person signing the order - position, surname, initials.

We offer you a free-form sample of an inventory order.

How to form a commission

The commission includes:

- representatives of the organization's management;

- accounting staff;

- financially responsible persons.

If for any reason one of the members of the commission cannot perform his duties (illness, business trip), then an order is issued to make changes to the composition of the inventory commission. All other employees participating in the council must put their introductory signatures under the administrative document.

Inventory automation

Used to replace manual comparison with information collection using equipment. Such an audit helps reduce the likelihood of inaccuracies associated with the human factor. The labeling process is labor intensive. offers updated programs, for example, Warehouse 15 - for working under new reporting conditions, as well as projects for labeling different product groups.

Special mobile readers are used to read stickers and barcodes. Balances are recalculated through the database terminal. Information is entered into the database automatically for each item of goods. The advantages of the Cleverens automated check include:

- reducing the time for collecting and processing information by 2 times;

- there is no requirement to close the warehouse during the audit period;

- there are no errors due to human factors;

- the costs of introducing automation will pay off within 2 years;

- the risk of information distortion is minimized.

The implementation of automation is carried out in stages. Initially, a database is formed, in the appropriate sections of which information on property, goods, inventories and other material assets in the enterprise is entered. Each reporting unit is marked with a sticker or barcode, allowing you to find the position in the database. A scanner is used to read data from such stickers. The information is processed and stored in the database.

Matches are recorded immediately, and information about missing copies or missing items becomes available after the verification is completed. The terminal automatically notifies you of a shortage. The obtained data is recorded in electronic format and used for calculations and analysis. The Cleverence company offers software for automating business processes that allows you to label products and track statistics on which brands for a given item are delivered to the warehouse complex.

How to submit inspection results

Upon completion of verification activities, the IC analyzes the information received and draws up an inventory (inventory act) based on it. The financially responsible persons must sign the acts, thereby confirming their presence and agreement with the results of the reconciliation process.

If during the audit, surpluses or shortages were identified that lead to discrepancies with accounting data, a matching statement is generated. For fixed assets, unified forms of final documentation will be recorded in the INV-1 inventory and the INV-18 statement.

After completing the process of analyzing the final information, a meeting of the inventory commission is held, at which the results of the assessment are recorded and possible options for correcting the detected violations are determined. After the meeting, a protocol and statement INV-26 are drawn up (Resolution of the Civil Code No. 26 of March 27, 2000), illustrating the absence (presence) of discrepancies and options for eliminating errors.

Documents drawn up at the meeting are sent to the head of the organization. Next, management reviews the initial materials of the assessment and makes decisions on the fact of control activities. The manager expresses his verdict by means of an order on the results of the reconciliation.

Types of inventory

Full inventory control involves recalculation and comparison of all property in the enterprise. Objects that the company rents are also subject to inspection.

Partial audit is a study of only some goods and values. If a shortage is identified during the event, the scope of inspection expands.

Selective - implies the recalculation of only certain types of stocks or values.

Scheduled – assigned according to the approved schedule. The list of objects to be studied is determined by the director.

Features of inventory in a budgetary institution

It is important to note that inventory is carried out both in private institutions and in budgetary ones without fail, since any company has certain property, for the safety of which individuals and legal entities are responsible.

Inventory in a budgetary organization has a number of features. Firstly, the company’s cash position is recalculated and analyzed on the basis of the legislative framework. When deviations are identified, the question arises as to which individuals’ mistakes led to the fragmentation of facts. In this case, all employees of the institution will be responsible for the discrepancy, regardless of whether they are an ordinary accountant or a manager.

Secondly, in budget companies, before the actual implementation of this event, an assessment of the objects that will be subject to inspection is carried out. This can be either all property with a detailed census of the institution’s assets, or selected areas. It should be noted that once a year, each organization is required to conduct a full status check, compare the results with the data specified in regulations, and then send reports for certification.

It is important to note that a partial inventory can be carried out much more often than an inspection of all assets, but it is not mandatory and is carried out only in the event of theft of property or unforeseen natural disasters.

When is inventory needed?

Legislative acts, in addition to the rules for holding an event, indicate situations in the event of which the company must necessarily and immediately organize an inventory. These include the following:

The emergence of new persons responsible for the material safety of property- Change of management (in case of sale of the company while maintaining specific activities)

- Closure of the institution

- Natural disasters that affected the state of the organization

- Certification of the fact of theft of property

How to form a commission

The audit commission is approved by issuing an appropriate order. It may include:

- persons holding senior positions in the company;

- accounting department employees;

- financially responsible employees;

- employees of third-party audit organizations.

If, on the start date of the inventory, one of the approved members of the commission cannot begin to perform the assigned duties, for example, due to a business trip or temporary disability, then the manager is obliged to issue a document appointing a replacement for him. All other members of the commission must be familiarized with it and signed.

Sample order to create a commission

Sample order for the creation of an inventory commission:

After completing the main verification activities, the commission is obliged to prepare and document reports on the audit results. All detected inaccuracies, errors and violations must be indicated in a specialized accounting sheet. To maintain it, the resolution of the State Statistics Committee, issued number 26, provides for a universal standard form. It is recorded under the number INV-26 ().

Ultimately, after discussing the results and assigning penalties against the officials responsible for violations, the manager is obliged to issue an order on the results of the audit. It is compiled in free form. Typical sample document:

What not to do when taking inventory of inventories

During the audit, it is not allowed to mix items or transfer them for storage to other sections or premises. During the inspection period, the release of inventories and consumables to production is prohibited, except in situations where the need for release is confirmed by written permission from the manager.

If the inventory is being carried out over a long period of time, employees, including the head of the department, are not allowed to enter the territory without the presence of a commission. At the end of the working day, the object is sealed with the exact time indicated on the seal.

The inventory commission is carried out before drawing up the annual final documentation.

The results of the event are subject to mandatory documentation. At the end of the inspection, a protocol is drawn up, which is endorsed by the signature of the manager and the company’s seal. Inventory of goods in a warehouse is the only way to confirm the integrity of the storage of material assets in the company’s warehouse. Number of impressions: 18442

Warehouse inventory

?Sample order for inventory taking at a warehouse

The company's inventories are stored in warehouses. Their receipt, disposal, and safety are documented and reflected in accounting data. The relevance and reliability of this data is ensured by inventories. In this article we will talk about how inventory is carried out in a warehouse.

The inventory procedure is regulated by orders of the Russian Ministry of Finance:

- dated June 13, 1995 No. 49 on approval of the Methodological Instructions for Inventory of Property and Financial Liabilities;

- dated December 28, 2001 No. 119n on approval of the Guidelines for accounting of inventories.

- reason for inventory;

- timing of its implementation;

- personal composition of the commission;

- objects to be checked and other information as necessary.

- when property arrives at the warehouse during inventory, such property is accepted in the presence of the inventory commission and is entered into a separate statement in the INV-3 form;

- with the consent of the head of the company and the chief accountant, disposal of inventory items from the warehouse during its inventory is allowed; in this case, members of the inventory commission must be present;

- if the commission leaves the warehouse premises before the inspection is completed, the premises must be sealed, and the actual number of inspected valuables must be recorded in inventory labels (INV-2), which remain in the sealed premises.

In the latest order (119n), the special rules by which the inventory of goods in the warehouse is carried out are set out in section 1 (clauses 21 - 35).

How to take inventory in a warehouse

On the one hand, such checks are carried out according to rules common to all inventories. On the other hand, there are some features that need to be taken into account.

Thus, warehouse inventory can be mandatory or proactive. Cases when inventory is carried out without fail are the same as during other inspections (preparation of annual reports, emergency situations, theft, change of responsible persons, etc.). It should be noted that, according to paragraph 258 of Order 119n, storekeepers or warehouse managers can be relieved of their positions only after conducting a complete inventory of the property assigned to them.

Initiative inventory is carried out on behalf of the head of the company. In warehouses, such checks may occur more often than in other structural divisions, which is due to the large number of material assets stored there, as well as their frequent movement (arrival at the warehouse and disposal).

Thus, a warehouse inventory should be carried out at least once a year (before preparing financial statements for the year), but in practice it happens much more often.

Warehouse inventory: instructions for carrying out

As with other inventories, an order must be issued to carry out an inspection at the warehouse. It can be prepared in a form approved by the State Statistics Committee. You can also develop your own form.

This order specifies:

When conducting an inventory at a warehouse, such an order reflects that the place of its conduct is the corresponding warehouse.

?order to carry out inventory at the warehouse

Before conducting an inspection, those responsible for the safety of property must submit receipts to the accounting department or inventory commission confirming that all documents for the property have been submitted to the accounting service, and all material assets have been recorded or written off.

The financially responsible persons being inspected cannot be included in the commission, but their presence during the inventory is mandatory.

During the inventory, the movement of inventory items in the warehouse should be suspended. However, depending on the size of the warehouse and the amount of property stored there, the inventory process may take several days. In this case, a number of additional measures should be taken:

The results of the warehouse inventory are reflected in the inventory lists (INV-1, INV-3), and if there are discrepancies, in the statements (INV-18 and INV-19