Do I need to maintain off-balance sheet accounts?

Some accountants ignore the need to maintain records. And in fact, the absence of these accounts does not have a significant impact on the company's fortunes. There is no liability for the absence of AP. However, it must be borne in mind that without off-balance sheet accounts, information about the property status of the company will be incomplete. Inventory of APs serves to obtain reliable information. Based on it, decisions can be made and special management can be appointed.

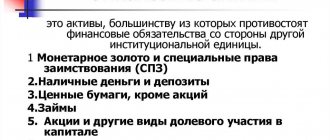

Information from the AP allows you to correctly evaluate all the company’s assets. If this information is missing, the auditor will not be able to correctly make an opinion about the state of the company. Full accounting of property is also necessary for tax authorities conducting audits. For example, account 001 may store information about leased assets. In this case, the company has the opportunity to justify the costs of repair work.

Information about property that is leased to third parties should be recorded on the property document. In this case, the appropriate accounts will be needed to draw up a financial plan and properly maintain management accounting. Based on the AP, accounting reports can be developed.

The procedure for assigning inventory numbers of fixed assets

The legislation does not provide for any specific procedure for generating an inventory number. Therefore, companies are given the right to develop it independently and consolidate it in the UE. As a rule, when compiling a sequence of digits of an inventory number, they are guided by the ease of working with the formatting object and the accepted production cipher algorithms. For example, in large companies with an extensive network of separate divisions and workshops, the number values must include information about the balance sheet account/sub-account, the branch where the facility is located, the digital designation of the workshop, department codes, etc.

When wondering how to assign an inventory number to a fixed asset, they rely on identifying the optimal variation of the number, which will make it easier and faster to track the use of the object in the company. For example, the sequence of numbers could be like this:

- balance account;

- company branch code;

- workshop number used in internal nomenclature;

- department where the object is located;

- serial number of the object.

Depending on the criteria in force in the company, other information can be encrypted in the inventory number: the depreciation group to which the object belongs, the territorial code of the unit’s location, etc.

If the company is small and only a few PF objects are used, then it would be correct to assign inventory numbers to them in order: 01, 02, 03, etc. They are registered in inventory journals, which are generated automatically or kept by hand.

Inventory of assets at the AP

Inventory is a procedure during which the status of a company's property and liabilities is monitored. In particular, their actual presence is established. In the process, information from accounting is compared with the actual availability of property. An inventory must be carried out before filling out the annual report.

Let's consider the features of inventory of off-balance sheet accounts:

- A firm rarely has accurate information about the value of property recorded in off-balance sheet accounts. The landlord or an independent appraiser usually has the relevant information. It is recommended to indicate the cost of the property in the rental agreement. The cost is then entered into an off-balance sheet account and then transferred to the inventory list.

- If a company leases an operating system, a separate inventory is drawn up for each tool. These funds should not be mixed with your own assets. The inventories record all the papers that confirm the arrival of funds to the company.

- It is not always possible to determine the exact cost of objects. For example, this is not possible with strict reporting forms. In this case, it is necessary to reflect the conditional value.

- Separate matching statements are prepared for off-balance sheet assets. The results of control activities are recorded in inventories.

Inventory of assets can be carried out not only by enterprises, but also by individual entrepreneurs.

How to correctly assign an inventory number

3459 Page contents The organization of accounting for any company requires strict accounting of fixed assets: the means of labor with the help of which products, work or services are produced.

One of the main mechanisms for monitoring the safety and movement of OSes is the assignment of inventory numbers to them: unique digital and symbol combinations that do not change throughout the entire operational life of the OS. When assigning an inventory number, certain techniques are used that allow you to encode in numbers and symbols all the basic information about each OS.

In addition to the operating system, inventory numbers are assigned to some other objects important for the functioning of the company.

An inventory number is assigned to a property at the time it is accepted for registration.

After this, it acquires the status of an inventory object - a control unit. The number is applied to the object using durable paint, barcode,

Order of conduct

Inventory is carried out in accordance with this order:

- Appointment of a commission that will conduct the inventory. She is appointed on the basis of an order from the manager and receives powers that will be valid for the entire year.

- Issuing an order on the procedure. The order specifies the timing of the procedure and its reasons. The members of the commission are indicated.

- Carrying out inventory. The event is carried out in the presence of commission members and financially responsible persons.

- Results of the event. The results are confirmed by inventories, which are signed by those present during the inventory. The information is summarized in the Statement of Results.

Inventory INV-1 is compiled in two copies. If discrepancies are found between reality and recorded data, comparison sheets are drawn up. They are created according to the forms INV-18 and INV-19. Form INV-5 is used in relation to property accepted for safekeeping.

Property inventory

Violation. When preparing annual reporting forms or when changing the head of an institution, an inventory of assets and liabilities was not made.

According to the provisions of Art. 11 of the Accounting Law No. 402-FZ, assets and liabilities are subject to inventory. During the inventory, the actual presence of the relevant objects is revealed, which is compared with the data of the accounting registers. The cases, timing and procedure for conducting an inventory, as well as the list of objects subject to inventory, are determined by the economic entity, with the exception of mandatory inventory. Mandatory inventory is established by the legislation of the Russian Federation, federal and industry standards. Thus, when conducting an inventory, state (municipal) institutions are guided by the provisions of Order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49 “On approval of the Guidelines for the inventory of property and financial obligations” (hereinafter referred to as the Guidelines). Note that Art. 12 of the Accounting Law No. 129-FZ contains the same list of cases when conducting an inventory is mandatory as clause 1.5 of the Methodological Instructions .