What is meant by “exemption” from the use of cash register equipment?

Indeed, “exemption” from the use of CCT may in this case involve several interpretations. Namely:

- “Exemption” - as a legal requirement not to use online cash registers.

That is, we are talking about the fact that a business entity should not use cash register systems. Even if he is, in principle, ready to use it, he cannot, the “liberation” is “compulsory” in nature.

- “Exemption” - as a legislative permission not to use online cash registers.

At the same time, such a permit can be established for one or another type of business entity:

- on an ongoing basis;

- on a temporary basis.

At the same time, “voluntary” exemption from online cash registers may be characterized by the presence or absence of an obligation for a business entity to issue documents to its customers that replace a cash receipt. Such documents could be, for example, a sales receipt or a strict reporting form.

- The “exemption” from the “full use” of online cash registers is, in fact, a partial exemption in which cash registers are used according to one or another “simplified scheme.”

A striking example of such a “simplified scheme” is when an online cash register can be used in a mode without transferring data to the OFD (and, as a result, save on the services of the Fiscal Data Operator) in the manner prescribed by paragraph 7 of Article 2 of Law No. 54-FZ. There are other “simplified” options for using cash registers - related, in particular, to the possibility of not issuing a cash receipt to the buyer or client.

But in essence, all these options and others like them reflect the fact that it is necessary to use an online cash register in principle, and they can hardly be called a full-fledged “exemption” from cash registers.

Let us consider in more detail how Russian entrepreneurs can use one or another scheme for exemption from the use of cash registers in the context of the above interpretations - having agreed that we will talk about the possibility not to apply in principle (without adjusting for the need for their use in a “preferential” regime - as in the case with the option not to enter into an agreement with the OFD).

Who needs to install an online cash register and is it possible to work without using it?

According to the current version of the law “On the use of cash registers” dated May 22, 2003 No. 54-FZ (Article 1.1, 1.2):

- All companies and individual entrepreneurs are required to use cash registers when making payments not only in cash, but also by bank transfer;

IMPORTANT! Cash register systems do not need to be used for non-cash payments between organizations among themselves or with individual entrepreneurs (with the exception of settlements using an electronic means of payment with sight). This is provided for in paragraph 9 of Art. 2 of Law 54-FZ).

- There may be exceptions to the above requirement (if such situations are provided for by law 54-FZ).

Moreover, it is necessary to use cash register systems not only when receiving payment or advance payment for goods, work, or services. In some cases, it is necessary to punch a check when paying out money, for example, when returning goods by the buyer or for refundable prepayment amounts.

The bulk of sellers had to purchase and begin using cash registers by July 1, 2021.

For a table with transition deadlines for different groups of sellers, see here.

Administrative liability is established for violating the procedure for using cash registers or failing to use an online machine in cases established by law. As a rule, these are fines. Moreover, sanctions can be imposed on both legal entities and officials. ConsultantPlus experts explained in detail what fines are established for violating the procedure for using cash register systems and whether sanctions can be reduced or avoided altogether. Get trial access to the K+ system and upgrade to the Ready Solution for free.

We will tell you further about who does not need to use online cash registers.

Exemption as a ban on the use of CCP

“Forcibly exempt” from the use of cash registers (clauses 1, 9, 10, 11 of Article 2 of Law No. 54-FZ - LINK):

- Banks.

In addition, online cash desks are not used by authorized representatives of banks who carry out payment transactions in accordance with orders from a financial institution.

- Individual entrepreneurs and legal entities selling through automatic devices that do not consume electricity in any way (through an outlet, battery, battery).

For example, through candy vending machines equipped with a scrolling lever, which you can start turning after placing a 5-ruble or 10-ruble coin in a special slot.

- Individual entrepreneurs and legal entities that make non-cash payments to each other.

However, if a representative of an individual entrepreneur or a legal entity (employee, authorized representative) came to pay the counterparty in cash, he must issue them a cash receipt upon receipt of funds to pay for goods or services.

- Business entities that exercise the powers of state or municipal authorities as part of the provision of paid parking for use to citizens and organizations on public roads and on land plots owned by the authorities.

Actually, for now this is all a case of “forced” exemption from the use of online cash registers. Next, we will consider a “softer” version of the exemption, in which a business entity is given the right to choose whether to use an online cash register or not.

Let's start with those users for whom the law has established an indefinite (valid until the law establishes otherwise) right to refuse to use cash register systems.

Online cash registers for working in markets - what to choose?

Before choosing a suitable device, you need to find out whether the online cash registers in the market will be connected to the power grid. Not all such platforms can provide access to a power outlet, so it is better to opt for stand-alone terminals, which are compact in size and can operate for up to 10 hours of continuous receipt printing on a single charge.

Among such cash registers with a fiscal drive, there are three most popular models. These are MSPos K online cash register (litebox 5) , Evotor 5 smart terminal and online cash register Neva 01F Litebox 7 .

Externally, these devices are not fundamentally different and resemble a smartphone: a capacitive touch display, compact dimensions, smooth shapes and a powerful battery. For a comparative overview, the main characteristics of the three online cash registers can be presented in table form.

| Characteristics | MSPos K (litebox 5) | Evotor 5 | Neva 01F Litebox 7 (with acquiring) |

| Appearance | |||

| Dimensions and weight | Length 21.5 cm, width 9 cm, height 6 cm. 900 grams | Length 21 cm, width 8.6 cm, height 5 cm. 400 grams | Length 26 cm, width 12 cm, height 8 cm. 700 grams |

| Display | Touchscreen 5.5 inches, IPS with LED backlight and resolution 1280×720 | Capacitive touch 5.5 inches with a resolution of 1280x720. Screen density 267 DPI | Touch 7 inches with a resolution of 1024×600 |

| Battery | 3.7V/5200 mAh | 2 batteries 2600 mAh | 7.4V, 2500mAh |

| Operating time on one charge | Up to 10 hours of continuous operation, standby time - up to 5 days | Up to 12 hours of continuous operation | Up to 14 hours of continuous operation, standby time - up to 5 days |

| Channels of connection | 3G, Wi-Fi, Bluetooth | Wi-Fi, Bluetooth 4.0, GSM 2G, 3G | 3G, Wi-Fi, Bluetooth, Ethernet |

| Connectors | 1 USB (Type-C) | 1 USB port | 2 USB, 1 micro-USB, LAN |

| Connecting external devices | PC, acquiring terminal | USB barcode scanners, scales, cash drawer, etc. | Acquiring terminal, scanner, scales, label printer, etc. |

| operating system | Android 6.0 | Evotor OS version 3 | Android 7.0 |

| EGAIS support | Yes | Yes | Yes |

| Compatibility with external software | Integrates with inventory systems 1C, MoySklad, 1C-Bitrix, etc. | Compatible with the cloud-based commodity accounting program MoySklad, can be connected to various programs on the 1C platform. | Connection to the Litebox cloud system. Built-in commodity accounting system and the ability to access your personal account from anywhere in the world. |

| Printing receipts | A 57 mm receipt tape is used. Thermal printing method | A 57 mm receipt tape is used. Thermal printing method | A 57 mm receipt tape is used. Thermal printing method |

| Receipt printing speed | 90 mm/s | 50 mm/s | 100 mm/s |

| Cost in the Multikas company with connection of a fiscal drive for 15 months | 17990 rubles | 17990 rubles | 20990 rubles |

Why do you need a fiscal drive at the cash desk and an agreement with the OFD?

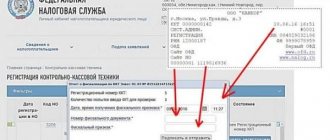

Any cash register, in accordance with the updated 54 Federal Law, must have a fiscal registrar and send data to the OFD and the Federal Tax Service. You will not be able to use the cash register without a fiscal registrar. The fiscal accumulator is available for 13 and 36 months. Which type to use in your case depends on what you trade and what form of taxation your business has. OFD - fiscal data operator is required to transfer data on cash settlement transactions to the tax office. Be sure to enter into an agreement with the OFD. It will not be possible to use the cash register without the OFD.

Advantages of online cash desks for trading in the market

|

Who and what types of activities are exempt from online cash registers indefinitely

They can decide at their own discretion whether to use an online cash register or not (clauses 2, 2.1, 3, 5, 8, 12 of Article 2 of Law No. 54-FZ):

- Individual entrepreneurs and legal entities that carry out the types of activities named in paragraph 2 of Article 2 of the law.

In particular, these types of activities include:

- sale of newspapers and magazines in paper form (and related products, the list of which is determined by the law of the subject of the Russian Federation);

- sale of tickets in public transport (but only until July 1, 2021, after which you will need to use an online ticket office for this type of activity);

- providing meals to students of educational institutions;

- retail trade in markets (unless it occurs outside a store, kiosk, tent), unless such trade is related to the sale of non-food products according to the list reflected in the order of the Russian government dated April 14, 2017 No. 698-r;

- peddling (in the open air, on trains, on airplanes) trade in goods that are not technically complex and require special conditions for storage and sale, as well as those that are not classified as goods subject to labeling;

- sale of ice cream, soft drinks (including kvass and milk from tanks);

- sale of bottled vegetable oil, live fish, vegetables, fruits;

- sale of kerosene;

- acceptance of glass containers and waste materials (except scrap metal) from individuals;

- provision of various household services;

- renting out your own residential premises (only individual entrepreneurs and legal entities must use cash register systems when carrying out this type of activity).

An important nuance: if an individual entrepreneur or legal entity sells excisable goods (for example, alcohol or tobacco products), then you will not be able to take advantage of the preference in question. The same applies if payments are made automatically (for example, through a vending machine, which in this case should have an automatic online cash register built into it).

Business entities carrying out the above types of activities have the right not to issue the buyer or client with any documents confirming the purchase, instead of a cash receipt. But it’s still useful to do this - consumer confidence will increase. An alternative document to a cash receipt can be the same sales receipt, BSO - as an option, printed using a receipt printer.

- Individual entrepreneurs on PSN, carrying out activities that do not relate to those named in subparagraphs 3, 6, 9 - 11, 18, 28, 32, 33, 37, 38, 40, 45 - 48, 53, 56, 63 of paragraph 2 Article 346.43 of the Tax Code of the Russian Federation - LINK.

Please note that the types of activities that are subject to an indefinite exemption from CCP do not include such large segments as retail trade and public catering. There, in general, you need to use an online cash register.

Individual entrepreneurs on PSN, who may refuse to use online cash registers, in turn, need to issue clients with a document alternative to a cash register receipt. This document must have the details named in paragraphs 4-12 of paragraph 1 of Article 4.7 of Law No. 54-FZ.

Namely:

- name of the document, its serial number from the beginning of the cashier’s shift;

- date, time, place of receipt of funds from the buyer or client;

- name of the business entity (or full name of the individual entrepreneur), TIN;

- the tax regime that the company applies;

- information about the content of the payment transaction (receipt, expense);

- a list of goods or services for which the buyer or client pays;

- price for selected goods or services including VAT (or highlighting those goods sold without VAT) - final, taking into account discounts and markups;

- information about the method of accepting payment - in cash or through acquiring (with a division of the amounts accepted by each method);

- Full name and position of the person who accepted the payment.

The document replacing the cash receipt must be signed by the seller.

From a technical point of view, the document in question can be generated in any way convenient for the seller - on a receipt printer, on a computer, or even manually.

The IP document in question on the PSN must be issued to the client or buyer without waiting for a request from him.

- Individual entrepreneurs and legal entities that operate in hard-to-reach areas.

In each region, the authorities themselves determine which localities these are and publish the relevant regulations (more details about this can be found in THIS ARTICLE). Such areas cannot include:

- cities;

- regional centers (unless they are the only settlements in their municipality);

- PGT.

At the same time, you need to take into account the same rule as in the case of “exceptional” types of activities above - preference is not available when selling excisable goods or using automatic devices.

As in the case of the exemption from the use of cash registers for entrepreneurs on a “patent,” those firms that operate in hard-to-reach areas are required to issue clients and customers with a document alternative to an online cash register receipt.

In the scenario under consideration, a number of special requirements are established for this document in terms of the procedure for issuance and accounting. These requirements are determined by Decree of the Government of Russia dated March 15, 2017 No. 296.

The company has the right to issue a document alternative to a cash register receipt only if the client or buyer themselves requests it.

- Pharmacies operating as legal entities located in paramedic and obstetric centers in rural areas (and separate divisions of medical institutions located in rural areas).

Note that in the scenario under consideration, it is necessary to use an online cash register when using vending machines or selling excisable goods.

There are no requirements for the use of documents alternative to cash receipts for pharmacists and rural hospitals.

- Religious organizations.

There are no requirements for the use of alternatives to cash receipts for such organizations.

- State, municipal libraries belonging to the Russian Academy of Sciences (and other academies, institutes, educational institutions) - when providing paid services within the framework of the main type of activity.

At the same time, the list of such services should be established by the Russian Government.

The list of cases when you can not use the online cash register is listed in the table (the table does not indicate situations when a temporary exemption applies):

Accountant

1. Who is obliged to use cash register systems ? All organizations and individual entrepreneurs are required to use cash register systems when making payments in cash and (or) by bank transfer (Article 1.1, paragraph 1, Article 1.2 of the Law on the use of cash register systems): • when accepting (receiving) payment, including prepayment (advance payment) for goods (work, services). Such an obligation also arises when funds are withheld from employees’ salaries to pay off debts to the organization and individual entrepreneurs for purchased goods (work, services) (see, for example, Letter of the Federal Tax Service of Russia dated August 14, 2018 N AS-4-20/15707). If settlements (in cash or with presentation of an electronic means of payment) between organizations and (or) individual entrepreneurs for goods (works, services) are carried out through an accountable person, then the cash register system is used by the organization (individual entrepreneur) that sells the goods (performs work, provides services), that is, one cash register is used (see, for example, Letter of the Federal Tax Service of Russia dated August 10, 2018 N AS-4-20 / [email protected] (clause 2)); • payment of money for goods (work, services), for example: - in connection with the buyer returning the purchased goods; — purchasing goods from individuals, including with the involvement of accountable persons, for resale; • return of prepayment (advance); • provision and repayment of loans to pay for goods (works, services); • organizing and conducting gambling and lotteries, for example, accepting bets, paying out funds in the form of winnings. CCT should be used by pawnshops: • when lending to citizens secured by things; • storage of things. Calculations also mean (Article 1.1 of the Law on the Application of CCP): • offset of prepayment (advance payment); • providing or receiving other consideration for goods (work, services), for example, providing goods as compensation. CCT must be used, in particular, by the following persons: • commission agent (agent) when selling goods of the principal (principal) (Letters of the Ministry of Finance of Russia dated 04.07.2018 N 03-01-15/46377, dated 11.10.2017 N 03-01-15/ 66398); • a payment agent accepting payments from individuals, including through payment terminals (Clause 12, Article 4, Clause 1, Article 6 of the Law on accepting payments, Article 1.1, Clause 2, Article 4 of the Law on the application of cash register systems) .

Thus, in most cases, in the calculations specified in Art. 1.1 of the Law on the Application of CCP, CCP must be applied. However, there are exceptions to this rule.

For information on the stages of transition to the use of online cash register systems, see Letter of the Ministry of Finance of Russia dated July 18, 2018 N 03-01-15/50059.

2. Who and in what cases can work without a cash register (not use cash register) The following are exempt from using cash register: 1) the types of activities listed in clause 2 of Art. 2 of the Law on the Application of CCP; 2) activities in remote and hard-to-reach areas; 3) services for conducting religious rites and ceremonies, as well as the sale of religious objects (Clause 6, Article 2 of the Law on the Application of CCP); 4) the activities of pharmacy organizations and separate divisions of medical organizations located in rural settlements (clause 5 of Article 2 of the Law on the Application of CCP). Such organizations may refuse to use CCP if a number of conditions are met; 5) non-cash settlements (except for settlements using an electronic means of payment with presentation) between organizations and (or) individual entrepreneurs (clause 9 of article 2 of the Law on the application of cash register systems). For example, cash register is not used for settlements by payment orders; 6) settlements under loan agreements provided for purposes not related to payment for goods (works, services), since they are not included in settlements in Art. 1.1 of the Law on the application of CCP (clause 1 of Article 1.2 of this Law); 7) sale of goods (work, services), for which payments to buyers (clients) are made by an agent (paying agent) (Article 1.1, Clause 2, Article 1.2 of the Law on the Application of CCP, Clause 12, Article 4 of the Law on Acceptance of Payments ). In this case, the cash register is used by the agent (paying agent); activities on the territories of military installations, facilities of federal security service agencies, state security agencies, foreign intelligence agencies (Clause 7 of Article 2 of the Law on the Application of CCP); 9) provision for a fee of the right to use parking lots (parking spaces) subject to the fulfillment of the conditions specified in clause 10 of Art. 2 of the Law on the Application of CCP; 10) provision of paid services to the population related to library science on the premises of state and municipal libraries, as well as libraries of the Russian Academy of Sciences, other academies, research institutes, educational organizations (clause 12 of Article 2 of the Law on the Application of CCP); 11) activities of individual entrepreneurs who use PSN (with the exception of individual entrepreneurs carrying out types of business activities established by paragraphs 3, 6, 9 - 11, 18, 28, 32, 33, 37, 38, 40, 45 - 48, 53, 56 , 63 clause 2 of article 346.43 of the Tax Code of the Russian Federation), if the buyer (client) has been issued (sent) a document confirming the fact of payment (clause 2.1 of article 2 of the Law on the application of cash register systems); 12) activities of credit institutions (clause 1, article 2 of the Law on the application of cash register systems). In addition, organizations and individual entrepreneurs do not use CCT (see, for example, Letters of the Federal Tax Service of Russia dated August 14, 2018 N AS-4-20/15707, dated August 10, 2018 N AS-4-20/ [email protected] (clause p. 1, 3)): • when paying money to an individual within the framework of obligations under a civil contract (with certain exceptions), including under a lease agreement; • payment of wages, including if part of it is paid in goods; • payment of financial assistance to an employee; • issuance of funds on account; • return by the employee of unspent funds issued on account. Also, cash register systems are not used by organizations and individual entrepreneurs when making payments exclusively using Bank of Russia coins through machines that are not powered by electrical energy (including from electric batteries or batteries) (Clause 1.1, Article 2 of the Law on the use of cash register machines). Until July 1, 2021, the following persons may not use CCT: 1) organizations and individual entrepreneurs paying UTII, as well as individual entrepreneurs using PSN, subject to a number of conditions; 2) individual entrepreneurs who sell goods through vending machines and do not have employees with whom employment contracts have been concluded (Part 11.1, Article 7 of the Federal Law of July 3, 2016 N 290-FZ); 3) organizations and individual entrepreneurs that perform work and provide services to the public with the issuance of BSO to customers. However, when providing public catering services, they cannot refuse to use cash registers (Part 8, Article 7 of Federal Law No. 290-FZ of July 3, 2016): - organizations; — Individual entrepreneurs who have employees with whom employment contracts have been concluded.

2 of the Law on the Application of CCP; 2) activities in remote and hard-to-reach areas; 3) services for conducting religious rites and ceremonies, as well as the sale of religious objects (Clause 6, Article 2 of the Law on the Application of CCP); 4) the activities of pharmacy organizations and separate divisions of medical organizations located in rural settlements (clause 5 of Article 2 of the Law on the Application of CCP). Such organizations may refuse to use CCP if a number of conditions are met; 5) non-cash settlements (except for settlements using an electronic means of payment with presentation) between organizations and (or) individual entrepreneurs (clause 9 of article 2 of the Law on the application of cash register systems). For example, cash register is not used for settlements by payment orders; 6) settlements under loan agreements provided for purposes not related to payment for goods (works, services), since they are not included in settlements in Art. 1.1 of the Law on the application of CCP (clause 1 of Article 1.2 of this Law); 7) sale of goods (work, services), for which payments to buyers (clients) are made by an agent (paying agent) (Article 1.1, Clause 2, Article 1.2 of the Law on the Application of CCP, Clause 12, Article 4 of the Law on Acceptance of Payments ). In this case, the cash register is used by the agent (paying agent); activities on the territories of military installations, facilities of federal security service agencies, state security agencies, foreign intelligence agencies (Clause 7 of Article 2 of the Law on the Application of CCP); 9) provision for a fee of the right to use parking lots (parking spaces) subject to the fulfillment of the conditions specified in clause 10 of Art. 2 of the Law on the Application of CCP; 10) provision of paid services to the population related to library science on the premises of state and municipal libraries, as well as libraries of the Russian Academy of Sciences, other academies, research institutes, educational organizations (clause 12 of Article 2 of the Law on the Application of CCP); 11) activities of individual entrepreneurs who use PSN (with the exception of individual entrepreneurs carrying out types of business activities established by paragraphs 3, 6, 9 - 11, 18, 28, 32, 33, 37, 38, 40, 45 - 48, 53, 56 , 63 clause 2 of article 346.43 of the Tax Code of the Russian Federation), if the buyer (client) has been issued (sent) a document confirming the fact of payment (clause 2.1 of article 2 of the Law on the application of cash register systems); 12) activities of credit institutions (clause 1, article 2 of the Law on the application of cash register systems). In addition, organizations and individual entrepreneurs do not use CCT (see, for example, Letters of the Federal Tax Service of Russia dated August 14, 2018 N AS-4-20/15707, dated August 10, 2018 N AS-4-20/ [email protected] (clause p. 1, 3)): • when paying money to an individual within the framework of obligations under a civil contract (with certain exceptions), including under a lease agreement; • payment of wages, including if part of it is paid in goods; • payment of financial assistance to an employee; • issuance of funds on account; • return by the employee of unspent funds issued on account. Also, cash register systems are not used by organizations and individual entrepreneurs when making payments exclusively using Bank of Russia coins through machines that are not powered by electrical energy (including from electric batteries or batteries) (Clause 1.1, Article 2 of the Law on the use of cash register machines). Until July 1, 2021, the following persons may not use CCT: 1) organizations and individual entrepreneurs paying UTII, as well as individual entrepreneurs using PSN, subject to a number of conditions; 2) individual entrepreneurs who sell goods through vending machines and do not have employees with whom employment contracts have been concluded (Part 11.1, Article 7 of the Federal Law of July 3, 2016 N 290-FZ); 3) organizations and individual entrepreneurs that perform work and provide services to the public with the issuance of BSO to customers. However, when providing public catering services, they cannot refuse to use cash registers (Part 8, Article 7 of Federal Law No. 290-FZ of July 3, 2016): - organizations; — Individual entrepreneurs who have employees with whom employment contracts have been concluded.

For information on the stages of transition to the use of online cash register systems, see Letter of the Ministry of Finance of Russia dated July 18, 2018 N 03-01-15/50059.

2.1. Types of activities for which it is possible not to use cash registers In clause 2 of Art. 2 of the Law on the Application of CCTs names the types of activities for which CCTs may not be used. In this case, an automatic device for payments should not be used (except for vending machines intended for sale in bottling drinking water) (Clause 8 of Article 2 of the Law on the Application of CCP). These types of activities include the following.

| Type of activity for which CCT may not be used | Additional conditions for non-use of cash registers |

| 1. Trade (except for trade in excisable goods - clause 8 of Article 2 of the Law on the application of CCP) | |

| Sale of newspapers and magazines on paper, as well as sale of related products at newsstands | 1) the share of sales of newspapers and magazines is at least 50% of turnover; 2) the range of related products is approved by the executive authority of the constituent entity of the Russian Federation; 3) accounting for trading revenue from the sale of newspapers and magazines and from the sale of related products is kept separately |

| Trade at retail markets, fairs, exhibition complexes, as well as in other areas designated for trade | 1) trade is carried out not in stores, pavilions, kiosks, tents, auto shops, auto shops, vans, container-type premises and other similarly equipped trading places (premises and vehicles, including trailers) located in the specified trading places and ensuring the display and safety of goods and semi-trailers); 2) trade is not carried out on open counters inside covered market premises with non-food products; 3) the goods sold are not on the List of non-food products, for the sale of which the use of cash registers is mandatory |

| Hand-held trade in food and non-food products outside the stationary retail network (including in passenger train cars and on board aircraft): - from hand; - from hand carts, baskets; - from other special devices for demonstrating, conveniently carrying and selling goods | The goods sold do not relate to: 1) technically complex goods; 2) food products requiring certain storage and sale conditions; 3) goods subject to mandatory marking with identification means |

| Trade in ice cream kiosks, bottled soft drinks, milk and drinking water | |

| Trade from tank trucks with kvass, milk, vegetable oil, live fish, kerosene | |

| Seasonal trading of vegetables, including potatoes, fruits and melons | |

| Sales of folk arts and crafts by the manufacturer | |

| 2. Works and services | |

| Providing meals for students and employees of educational organizations | 1) the educational organization implements basic general education programs; 2) food is provided during training sessions |

| Shoe repair and painting | |

| Manufacturing and repair of metal haberdashery and keys | |

| Supervision and care for children, the sick, the elderly and the disabled | |

| Plowing gardens and cutting firewood | |

| Porter services at railway stations, bus stations, air terminals, airports, sea and river ports | |

| Sale by the driver or conductor in the vehicle cabin of travel documents (tickets) and coupons for travel on public transport until July 1, 2021. | |

| 3. Other | |

| Sale of securities | |

| Renting residential premises to individual entrepreneurs | The premises must belong to the individual entrepreneur on the right of ownership |

| Reception of glassware and waste materials from the population | We accept from the public non-scrap metal, non-precious metals and non-precious stones |

2.2. CCP for settlements in remote and hard-to-reach areas Settlements in remote and hard-to-reach areas can be carried out without the use of CCP if the following conditions are met (clauses 3, 8, Article 2 of the Law on the application of CCP): 1) settlements are carried out in areas designated by regional authorities to remote and hard to reach. Exceptions are cities, district centers (except for the administrative centers of municipal districts, which are the only populated area of the municipal district), urban-type settlements; 2) the buyer (client) is issued, upon his request, a document confirming the fact of payment. The document must contain the required details, as well as the signature of the person issuing it; 3) an automatic device for calculations is not used; 4) there is no trade in excisable goods.

2.3. Conditions for exemption from the use of CCT for pharmacies and separate divisions of medical organizations To be exempt from the use of CCT, the following conditions must be met.

| Who is freed | Conditions for the non-use of cash registers (clauses 5, 8, Article 2 of the Law on the use of cash register systems) |

| Pharmacy organizations | 1) are located in paramedic and paramedic-obstetric centers, which are located in rural settlements; 2) do not use an automatic device for calculations; 3) do not sell excisable goods |

| Separate divisions of medical organizations (outpatient clinics, paramedic and paramedic-obstetric stations, centers (departments) of general medical (family) practice) | 1) located in rural settlements where there are no pharmacy organizations; 2) the organization has a license for pharmaceutical activities; 3) do not use an automatic device for calculations; 4) do not sell excisable goods |

2.4. CCT when providing services to the public Until July 1, 2019, it is possible not to use CCT, issuing BSO instead, only when providing services to the public, that is, citizens, including individual entrepreneurs (Part 8, Article 7 of Federal Law dated July 3, 2016 N 290-FZ , clause 4 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 31, 2003 N 16 “On some issues of the practice of applying administrative liability provided for in Article 14.5 of the Code of the Russian Federation on Administrative Offenses for non-use of cash registers”). Services to the public mean services: • named in the Collective Classification Group “Paid Paid Services to the Population” based on OKPD2; • not directly named in collective groups, but by their nature providing services to the population. They cannot refuse to use cash register systems when providing public catering services (Part 8, Article 7 of Federal Law No. 290-FZ of July 3, 2016): • organizations; • Individual entrepreneurs with employees with whom employment contracts have been concluded. From July 1, 2021, it is possible not to use cash register systems when providing services to the public only on general grounds.

2.5. CCT in case of payment of UTII and when applying the patent taxation system The procedure for switching to the use of CCT for UTII or PSN is the same as for other taxpayers.

However, for these persons, specific features of the use of cash registers are provided. Individual entrepreneurs who use PSN may not use cash registers if the following conditions are met (clause 2.1 of article 2 of the Law on the use of cash register systems). 1. Individual entrepreneurs carry out types of business activities that are not classified as types of activities established by paragraphs. 3, 6, 9 - 11, 18, 28, 32, 33, 37, 38, 40, 45 - 48, 53, 56, 63 p. 2 art. 346.43 Tax Code of the Russian Federation. In particular, CCT may not be used in relation to such activities as: - repair, cleaning, painting and sewing of shoes (clause 2, clause 2, article 346.43 of the Tax Code of the Russian Federation); — dry cleaning, dyeing and laundry services (clause 4, clause 2, article 346.43 of the Tax Code of the Russian Federation); — services of photo studios, photo and film laboratories (clause 8, clause 2, article 346.43 of the Tax Code of the Russian Federation); — services for training the population in courses and tutoring (clause 15, clause 2, article 346.43 of the Tax Code of the Russian Federation). 2. The buyer (client) is issued (sent) a document confirming the fact of payment. The document must contain mandatory details. From July 1, 2021, all UTII payers cannot work without a cash register. Until July 1, 2021, provided that at the request of the buyer (client) a sales receipt, receipt or other document confirming the fact of payment is issued, cash register systems may not be used (Part 7.1 Article 7 of Federal Law dated 07/03/2016 N 290-FZ): 1) organizations and individual entrepreneurs - payers of UTII that provide services, with the exception of public catering services (clause 1, part 7.1, article 7 of the Federal Law of July 3, 2016 N 290-FZ); 2) individual entrepreneurs who apply PSN in relation to the types of activities specified in clause 3, part 7.1 of art. 7 Federal Law dated July 3, 2016 N 290-FZ; 3) individual entrepreneurs paying UTII (using PSN), who sell goods at retail or provide catering services in the absence of employees with whom employment contracts have been concluded (clause 2, 4, part 7.1, article 7 of the Federal Law of 03.07 .2016 N 290-FZ). For information on the stages of transition to the use of online cash register systems, see Letter of the Ministry of Finance of Russia dated July 18, 2018 N 03-01-15/50059. Important! Individual entrepreneurs selling retail goods or providing public catering services that do not have employees working under employment contracts, if such an agreement is concluded, are required to register a cash register within 30 calendar days from the date of its conclusion (Part 7.3 of Article 7 of the Federal Law of 03.07 .2016 N 290-FZ). When selling a number of goods, it is mandatory to issue a sales receipt, regardless of whether the buyer requested it or not. Violation of this rule is subject to administrative liability. 2.6. Other reasons not to use cash registers until July 1, 2019. Until July 1, 2021, organizations and individual entrepreneurs may not use cash registers (Part 4, Article 4 of the Federal Law of July 3, 2018 N 192-FZ): 1) for non-cash payments with individuals persons who do not belong to individual entrepreneurs (except for settlements using electronic means of payment); 2) accepting payments for residential premises and utilities, including contributions for major repairs; 3) offset and return of prepayment (advance payment); 4) when providing loans to pay for goods (work, services); 5) providing or receiving other consideration for goods (work, services). Date of publication: 08/30/2018

Who is exempt from online cash register until 2021

The following business entities are temporarily exempt from using online cash registers until July 1, 2019:

- Individual entrepreneurs on PSN and UTII, legal entities on UTII, which, having employees on staff, carry out activities not related to retail and catering - here sellers and restaurateurs are again “in the wings”).

- Individual entrepreneurs on PSN and UTII, which, without employees, carry out any activities permitted under the relevant tax regimes (including retail and catering - there is a loophole here, but the business owner will have to rely on his own strength).

A complete list of permitted activities for which online cash registers may not be used in both cases is given in paragraph 7.1 of Article 7 of Law No. 290-FZ of July 3, 2016 - LINK.

The specified categories of business entities under special regimes are required to issue a sales receipt instead of an online cash register receipt - at the request of the buyer or client.

- Individual entrepreneurs and legal entities providing services, having employees, in any field of activity, except for public catering (under any taxation system - if not in a special regime, then in the OSN, simplified tax system, unified agricultural tax).

- Individual entrepreneurs and legal entities performing work and providing services to the public without having employees - in any field of activity (and regardless of the applied tax regime).

It is worth keeping in mind that a legal entity without employees will most likely not be able to function in practice, since in order for a business company to enter into legal relations, it must at least have a director appointed. Even if he does not have an employment contract (that is, if the director is the founder himself), then he, nevertheless, can be considered as an employee - since he will be considered an insured person in the pension, social and health insurance system.

The specified categories of business entities providing services are required to issue strict reporting forms to clients instead of online cash register receipts - in the manner prescribed by Decree of the Government of Russia dated May 6, 2008 No. 359.

- Individual entrepreneurs and legal entities that, without employees, conduct sales through vending machines.

There are no requirements for issuing documents alternative to checks.

How to work without an online cash register

At the time of preparation of the material, the third wave of connecting cash register equipment is taking place. Considering that only a few follow current innovations, the vast majority do not know who does not need to install online cash registers in 2021. In order to fully operate on the Russian market without using a cash register, you need to pay attention to the current list of exceptions. Now it looks like this.

- A businessman sells ice cream at a kiosk.

- Trade in kvass, beer, milk, fish, kerosene and sunflower oil. Here it is necessary to clearly understand that the exception applies to organizations distributing goods from mobile tanks. If, for example, you sell a similar product in packaging or plastic/glass containers, to provide such a service you will have to install a new cash register.

- Sales of food products in canteens on the territory of educational institutions - schools, lyceums, universities and so on.

- Tea break on the train. But there is an exception here too - starting from July 1, 2021, the seller will be required to use the cash register if we are talking about dispensing tea in bags, and not in the form of a ready-made drink.

- Conducting activities inside a specially equipped kiosk, if magazine issues and newspapers provide more than 50 percent of the total turnover. It is noted that revenue from the sale of such products is taken into account separately.

Expert opinion

Irina Smirnova

Online checkout expert

Ask a Question

To fully provide services, you will need to submit a strict reporting form at the request of the client. This must be done - if a refusal is received, the client has every right to complain to tax officials, which will later entail sanctions.

Postponement of the use of cash register until July 1, 2021 for individual entrepreneurs without employees

Federal Law 129-FZ dated 06.06.2019 On amendments to the Federal Law “On the use of cash register equipment when making payments in the Russian Federation” provides an exemption from the use of online cash registers until July 1, 2021 for individual entrepreneurs without employees when selling goods of their own production. , performance of work, provision of services. Comments on this topic are given in a SEPARATE ARTICLE.

Video - who can be exempt from online checkout until July 1, 2021:

Are online cash registers needed at markets?

Non-food products that cannot be traded at the market without using an online cash register include:

- carpet products;

- wardrobe items (except for underwear);

- leather products;

- wood products;

- furniture;

- chemical substances;

- medications;

- computer equipment and electronics;

- cars;

- musical instruments;

- sporting goods (except for fishing goods);

- orthopedic products.

Online cash desks at markets are needed if you trade indoors:

- market shop;

- van, van or trailer;

- pavilion, kiosk, tent;

- trading inside a covered market premises;

- container.

Deferments, benefits, exemptions

And so, at the end of May 2021, literally a month before the moment when all individual entrepreneurs and organizations caught up in the “third wave” were supposed to switch to online cash registers, further amendments to the law on the use of cash registers were adopted. The corresponding bill was adopted by the State Duma, approved by the Federation Council and sent to the President of the Russian Federation for signature.

This time, legislators exempted certain categories of entrepreneurs and organizations from using cash registers (permanently or temporarily), and also relaxed the rules for using online cash registers for those caught up in the “third wave.”

So, entrepreneurs who work without hired personnel will not be able to apply the CCP until July 1, 2021. They will not need a cash register either when performing work, or when providing services, or when selling goods of their own production. But the resale of goods is not subject to deferment - you will have to go online. This benefit will also disappear if the individual entrepreneur enters into an employment contract with the employee. In this case, you will need to register an online cash register within 30 calendar days.

Important

Entrepreneurs who perform work or provide services exclusively on their own may not rush to purchase online cash registers until July 1, 2021. Until the same date, entrepreneurs without employees who sell goods of their own production have the right to work without CCP.

Some organizations have received a complete exemption from the use of online cash registers when making non-cash payments, including using bank cards remotely (via the Internet or online banks). These include:

— partnerships of real estate owners (including partnerships of homeowners, horticultural and gardening non-profit partnerships), housing, housing-construction cooperatives and other specialized consumer cooperatives. Payments for the provision of services to its members within the framework of statutory activities, as well as when accepting payment for residential premises and utilities, are exempt from CCP;

- educational, physical education and sports organizations, as well as various houses, palaces and cultural and leisure centers that provide relevant services to the population.

If these services are paid for in cash or “with the presentation of an electronic means of payment, subject to direct interaction between the buyer (client) and the user” (in other words, with bank cards upon presentation), then you will have to punch out cash receipts.

In addition, entrepreneurs who sell entrance tickets and subscriptions to theaters that are state or municipal institutions from hand and (or) trays will be able to do without online ticket offices completely. The exemption is provided regardless of the form of payment (cash, cards, non-cash, online). But at the same time, the sale of the same tickets or subscriptions via the Internet is not exempt from cash register operations.

Relaxations have also been introduced regarding the use of cash register equipment in a number of cases. In particular, it is allowed not to print paper cash receipts when selling travel tickets in public transport. It is enough for the driver or conductor to issue the passenger a ticket or coupon, which will indicate how to receive the check in electronic form (for example, a link to the website is provided). Such a receipt must be created before the end of the day on which the ticket was sold. This means that, in fact, the driver or conductor can still do without a cash register - receipts will be generated after the fact based on data on tickets sold.

On a note

A relaxation has been introduced for online stores. Now the courier can not punch the receipt upon delivery, but show it in the form of a QR code, which the buyer scans on his phone. This code is equivalent to a paper check and has all the necessary details.

Another simplification concerns the issuance of cash receipts by companies that accept payments for housing and utilities, and do not fall under the above exemption (i.e., are not cooperatives, partnerships, etc.). For “absentee” payments (i.e., for any payments other than cash and card payments upon presentation) for housing and housing and communal services, an electronic check may not be sent at all, unless a corresponding request has been received from the client. The client has the right to send a request for the issuance of a check no later than three months from the moment the check is generated (by law, the check must be generated no later than five business days from the date the money is received in the account). After this three-month period, the obligation to issue a check is considered fulfilled, even if a request to issue a check has not been received.

Who was “covered”?

It's time to summarize. What do we have left in the bottom line? That is, who should ultimately switch to online cash registers from July 2019? So, taking into account all the amendments, from July 1, 2021, the following categories of organizations and individual entrepreneurs should start using online cash registers (provided that they are not, in principle, exempt from cash registers on the basis of Article 2 of Law No. 54-FZ, incl. in connection with the use of PSN and NAP):

- organizations performing work and providing services directly to the population;

- companies that are payers of UTII, regardless of the type of activity transferred to “imputation”;

- Individual entrepreneurs performing work and providing services, if they have employees;

- Individual entrepreneurs selling purchased goods;

- Individual entrepreneurs selling goods of their own production, if they have employees;

- Individual entrepreneurs trading using vending machines;

- companies and individual entrepreneurs carrying out non-cash payments with individuals who are not entrepreneurs. An exception is made for educational, physical education and sports organizations, various houses, palaces and cultural centers when providing relevant services to the population. And also for individual entrepreneurs selling entrance tickets and subscriptions to theaters that are state or municipal institutions by hand and (or) from a tray;

- companies and individual entrepreneurs when accepting payment for residential premises and utilities, including contributions for major repairs, in cash or by bank cards upon presentation;

- companies (except for specialized consumer cooperatives and partnerships of real estate owners) and individual entrepreneurs when accepting payments for residential premises and utilities, including contributions for major repairs, by bank transfer, incl. by bank cards remotely;

- companies and individual entrepreneurs when offsetting and returning prepayments and (or) advances;

- companies and individual entrepreneurs when providing loans to pay for goods, works, services;

- companies and individual entrepreneurs when providing or receiving other consideration for goods, work, services;

- companies and individual entrepreneurs when selling tickets and coupons for travel on public transport in a vehicle (it is acceptable to have one cash register per enterprise).