2-NDFL for 2021: sample form

Officials have updated the format for reporting on the income of working citizens.

Employers are now required to fill out new reporting forms. Please note that two forms of 2-NDFL have been introduced at once. Fill out one for the Federal Tax Service. The second format will be required for the employee. For example, to apply for a loan. Let's figure out which 2-NDFL form to use for reporting in 2021.

We will define new rules and instructions for filling out.

Forms of the new form 2-NDFL in 2021

The new form and the procedure for filling it out were approved by Order of the Federal Tax Service of Russia dated October 2, 2021 No. ММВ-7-11/ [email protected]

The new form has two forms:

To submit to the Federal Tax Service (looks like a declaration):

To hand over to the employee:

The Bukhsoft program has updated the electronic version of the certificate taking into account the new order. See how to prepare and print your new form. Please note that there are now two forms.

One to give to the employee:

2-NDFL for issuance to employees online

Another for the Federal Tax Service:

2-NDFL for the Federal Tax Service online

If you filled out an old form and want to quickly convert it into a new one, use the free service in the Bukhsoft program.

Convert old 2-NDFL to new

Changes in Earnings Reporting

The updated structure of the 2-NDFL certificate form was introduced by Order of the Federal Tax Service of Russia dated October 2, 2021 N ММВ-7-11/ [email protected] Tax authorities have complicated the income reporting form. The old report had a condensed structure and was placed on one standard page.

The new form has become larger. The document consists of a title page consisting of three sections and a separate appendix. A monthly breakdown was included in the additional sheet of the application:

- accrued income;

- the deduction provided;

- withheld income tax.

In addition to the new reporting format for the Federal Tax Service, officials approved a new form. A form for a certificate of earnings is provided for employees. The employer will issue the form only upon an individual request from a subordinate. An employee may need such a document to obtain a loan or, for example, apply for government benefits and deductions.

The structure of the income certificate for employees is presented in Appendix No. 5 to the Order of the Federal Tax Service of Russia dated 10/02/2021 N ММВ-7-11/ [email protected] Note that this form is practically no different from the old 2-NDFL form. Officials removed only a few codes and fields filled in exclusively for the Federal Tax Service.

Structure of the new form

The updated form, in comparison with the old certificate, contains fewer sections. For example, the 2021 form had five sections. Now there are only three of them. However, additional fields and columns have been introduced that were not previously provided.

Form 2-NDFL 2021 has the following structure:

- Introductory part, which discloses general data and identification details of the tax agent.

- Section No. 1 - discloses information about the taxpayer - the employee who directly received income in the reporting period.

- Section No. 2 – reflects generalized indicators of the amounts of earnings accrued to the employee. Also, the new form 2-NDFL for 2021 in section 2 records data on the calculated tax and advance payments paid.

- Section No. 3 – deciphers information about tax deductions that the taxpayer received from a specific tax agent.

- The appendix to the 2-NDFL certificate 2021 deciphers information about charges, deductions and deductions. Data is reflected monthly.

General filling rules

You can prepare reports on paper. For example, by filling out information by hand. Either use printed media or a computer.

It is allowed to generate reports in electronic form using specialized accounting programs. You can also prepare new 2-NDFL certificates using a free application from the Federal Tax Service.

You can download the “Taxpayer” program on the official website of the Inspectorate.

Important! If the organization has 25 or more people on staff, then it is not possible to submit certificates on paper. Companies with fewer than 25 employees are entitled to submit paper reports.

The report prohibits:

- You cannot print a report on a sheet of paper on both sides.

- It is also prohibited to staple certificates together, as this will lead to damage to the forms.

- Marks and corrections are not allowed.

- Correction products (tape, putty, pencils) are prohibited.

Enter the text in capital block letters, from left to right. Place dashes in empty cells. When filling out the 2-NDFL certificate by hand, use only black or blue paste.

Please note that you will have to submit the report on paper with an additional accompanying inventory. The register of income certificates in the KND form 1110306 is required to be provided.

Filling example

Let's look at the step-by-step instructions for filling out the new 2-NDFL certificate 2021 using a specific example. The conditions for filling out are as follows:

Pugachev Philip Pedrosovich in 2021, while working at “Beautiful Day” LLC, received the following income:

Month of the reporting period Amount and type of income

| January | RUB 21,000: salary; |

| February | RUB 21,000: salary pay; |

| March | 21,000 rubles: Including earnings – 16,000 rubles; payment of sick leave benefits – 5,000 rubles; |

| April | RUB 21,000: salary; |

| May | RUB 21,000: earnings; |

| June | 51,000 rubles: Including salary 21,000 rubles. bonus 10,000 rub. vacation pay 20,000 rubles; |

| July | 1,000 rub.: charge. pay; |

| August | RUB 21,000: salary; |

| September | RUB 21,000: earnings; |

| October | RUB 21,000: salary; |

| November | RUB 21,000: salary; |

| December | 21,000 rubles: earnings. |

| Total | RUB 262,000 |

For each month of 2021, “Beautiful Day” LLC provided Pugachev F.P. with a standard deduction for the first child (clause 4, clause 1, article 218 of the Tax Code of the Russian Federation).

In the “Sign” field of the 2-NDFL income certificate of F.P. Pugacheva for 2021, the number 1 is indicated.

In the fields “Income Code” and “Deduction Code” of the certificate, the values are indicated from Appendices No. 1 and No. 2 to the Order of the Federal Tax Service of Russia dated September 10, 2016 N ММВ-7-11/ [email protected]

Step-by-step instructions for filling out the reporting certificate 2-NDFL 2021:

- In the header of the title page we indicate the INN and KPP of the tax agent. That is, the employer.

- Report number – indicate the serial number of the report certificate.

- The reporting year is according to the conditions of the example 2021.

- Certificate attribute: “1” – tax withheld, “2” – tax cannot be withheld, “3” – tax was withheld by the successor during reorganization, “4” – personal income tax was not withheld by the successor.

- We fill in the adjustment number only when preparing adjusting statements. When filling out 2-NDFL, we put a dash for the first time.

- Code of the tax authority (IFTS) to which reporting is submitted. For example, “7727”.

- Full name of the employer or organization that accrued earnings to the individual.

- Information on reorganization - we fill out only if the reporting is prepared by the legal successor.

- OKTMO and phone number - indicate the relevant information.

Next, fill out the first section of the 2-NDFL 2021 certificate. Registers the data of the taxpayer - an individual who received income. We indicate the citizen's TIN (if available), full name, payer status (resident of the Russian Federation - 1, non-resident - 2), date of birth, citizenship (Russian - code 643). Type of document, its series and number. For example, a passport of a citizen of the Russian Federation is indicated by the code “21”.

Let's move on to the second section. Based on the company’s accounting data, we enter the following information:

- Total amount of charges. Check that the amount of the application's income must match the amount.

- The tax base is calculated as the difference between accrued income and provided deductions.

- The calculated tax amount is calculated as the base multiplied by the tax rate.

- Amount of tax withheld – we indicate only the amount of income tax that the employer actually withheld.

- Fixed advance payments - we fill out only if there are any.

- Tax transferred – enter the amount paid into the budget.

- If personal income tax is withheld excessively, then reflect the difference in the appropriate line.

- If it is impossible to withhold tax, enter the amount not withheld by the tax agent.

Section No. 3 is filled in with information about the tax deductions provided. We are talking about standard benefits, deductions for children, as well as property and social deductions.

We fill in the benefit codes and the deduction amount provided during the reporting period. The deduction codes are enshrined in the Order of the Federal Tax Service of Russia dated September 10, 2016 N ММВ-7-11/ [email protected]

When providing social and property benefits, fill in the number and date of notification from the Federal Tax Service.

Now we fill in the information about the person who certified the accuracy of the information. This is the head of the employing organization. Or another authorized person by proxy. For example, chief accountant. We indicate the status of the signatory and the full name of the person responsible.

Let's go to the application. We provide a monthly breakdown of the employee’s income, deductions and taxes. If an employee receives income taxed at different rates, he will have to prepare a separate report for each tax rate. Indicate income codes and deduction codes in strict accordance with Appendices No. 1 and No. 2 to the Order of the Federal Tax Service of Russia dated September 10, 2016 N ММВ-7-11/ [email protected]

Form for handing over to employees

The Tax Code obliges employers to issue their employees with certificates of income and withheld personal income tax, provided that the employee has written an application requesting such data (Clause 3 of Article 230 of the Tax Code of the Russian Federation).

If previously Form 2-NDFL for the tax office and the employee were the same, now the forms are different (Order of the Federal Tax Service of Russia dated 10/02/2021 No. ММВ-7-11/ [email protected] ).

The form was made simpler: the certificate attribute, information about its number, tax office code, correction number, etc. were removed.

2-NDFL for issuance to employees online

Form form:

Robot vacuum cleaner when you subscribe to Simplified!

Today, when you subscribe to the Simplified magazine, you will receive two gifts at once

: Robot vacuum cleaner + 2 additional months of subscription.

- Invoice for "Simplified" + 2 gifts →

The account is valid until October 9 inclusive.

Source: https://www.26-2.ru/art/355013-2-ndfl-za-2021-god-blank-obrazets-zapolneniya

Signs 1 or 2 in certificate 2-NDFL: what is it

Employers fill out new 2-NDFL certificates. In addition to the form, the list of certificate features has also been updated. Which one to indicate depends on whether tax was withheld from the income of individuals or not. The procedure for filling out and submitting certificates varies. Signs 1 or 2 in certificate 2-NDFL: let’s figure out what it is and in what cases to submit it.

How to fill out a new income certificate: step-by-step instructions >>>

What does the sign mean in 2-NDFL

Companies and individual entrepreneurs issue certificates of employee income in Form 2-NDFL, approved in Appendix No. 1 to the Federal Tax Service order No. MMV-7-11/566 dated October 2, 2021. This form has a column “Sign”, which is required to be filled out.

In practice, the question often arises: what is sign 1 or 2 in the 2-NDFL certificate? The answer to the question is the following - this is a special digital code that means whether the company was able to withhold tax on the employee’s income or not.

If the employer has withheld and transferred tax, he submits to the inspectorate information about the income of individuals and the amount of tax with code “1”.

If an organization or individual entrepreneur informs the tax office about the impossibility of withholding the calculated amount of tax from the taxpayer, then code “2” is indicated in the second line of the certificate.

Download a certificate of income and tax amounts of an individual for submission to the Federal Tax Service >>>

Thus, tax agents must put the number 1 or 2 in column 2-NDFL certificate. By the code, tax authorities will find out the following information:

- on the number of individuals who were paid taxable income, the total income, accrued and transferred tax to the budget;

- personal income tax debt and the number of debtors.

From January 1, fill out the 2-NDFL certificate on new forms. Tax officials approved two forms: one for the Federal Tax Service, the second for the employee. The inspection certificate now contains at least two pages. Each certificate for the Federal Tax Service will need to be assigned one of four characteristics. What code to put and when to submit the certificate >>>

Certificate 2-NDFL with sign 1

Organizations and entrepreneurs are required to issue 2-NDFL certificates with attribute 1 for all their employees who were paid income during the reporting period.

The deadline for submitting the document is April 1 of the year following the reporting year (clause 2 of Article 230 of the Tax Code of the Russian Federation). If the date falls on a weekend or holiday, reports must be submitted on the next working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

For example, at the end of 2021, you must report to the inspectorate on the amounts of income paid, taxes calculated, withheld and transferred to the budget before April 1, 2021.

Certificate 2-NDFL with sign 2

Companies and individual entrepreneurs are required to report to the inspectorate that at the end of the year they were unable to withhold personal income tax from “physicists”. To do this, no later than March 1 of the next year, you must submit a 2-NDFL certificate with sign 2 to the tax authority (clause 5 of Article 226 of the Tax Code of the Russian Federation). We have collected the most common cases when such a certificate is required in the list below.

Reports about the impossibility of withholding tax must be submitted on forms using form 2-NDFL with attribute 2. If the form is submitted by the successor of the tax agent after reorganization, then put 4.

In the application, indicate only those amounts of income actually received from which personal income tax could not be withheld. In section 2, reflect the total income from which tax was not withheld.

Show the amount of this tax in the fields “Tax amount calculated” and “Tax amount not withheld by the tax agent.”

The fields “Amount of tax withheld”, “Amount of tax transferred” and “Amount of tax over-withheld by the tax agent” must contain zeros. More details about filling out 2-NDFL with sign 2 >>>

Since you only need to report on the results of the year, we recommend keeping a special register of people for whom they were unable to withhold tax during the year.

Table of situations when personal income tax cannot be withheld

Situation Why it is impossible to withhold personal income tax

| The company gave a gift to third parties or accrued other income in kind (for example, paid for a tourist package) | A gift (other income in kind) was received by a person to whom the company does not pay money |

| The organization paid for housing and travel for representatives of the counterparty who arrived for the negotiations | The company does not pay these people cash income |

| The employee quit before repaying the loan he received at preferential interest rates | There will be no more monetary payments to the former employee. There is nothing to withhold personal income tax from |

| The company recalculated the personal income tax for the former employee or forgave him the debt, for example, according to the report | |

| According to the court decision, the organization paid the average salary for the period of forced absence. At the same time, personal income tax was not allocated in the court decision. Immediately after reinstatement, the employee decided to quit |

Companies or individual entrepreneurs must report to the inspectorate where they are registered. Tax legislation does not require reporting at the place of residence of the individual who received the income.

What happens if you specify a sign incorrectly

If an organization or individual entrepreneur indicates an incorrect attribute in the report, tax authorities may fine you 500 rubles for such an error. as for providing false information (Article 126.1 of the Tax Code of the Russian Federation). A fine of this amount is imposed for each report with errors.

But a fine can be avoided if you clarify the information before the tax authorities reveal inaccuracies (clause 2 of Article 126.1 of the Tax Code of the Russian Federation). Before it's too late, double-check your certificates.

If you find that you submitted a certificate with an error, submit a corrective 2-NDFL. Fill in the “adjustment number” field (01, 02, etc.). Leave the report number the same, but change the date.

Rules by which new 2-NDFL certificates must be clarified >>>

Source: https://www.glavbukh.ru/art/85736-priznak-1-i-2-v-spravke-2-ndfl

Penalty for failure to submit a certificate of inability to withhold personal income tax

In January, the company told the inspectorate that it was impossible to withhold personal income tax from the physicist, and in February it paid him income in foreign currency. Income is reflected in 2-personal income tax in the month when it is considered practically acquired according to the rules of Art. Form n 2-personal income tax certificate of income of an individual for the year 200. The procedure for submitting a certificate in form 2-personal income tax and reporting the impossibility of withholding tax will be adjusted. There were a lot of people at the rally on July 28 in Moscow, even more than 6.5 thousand, more many were not.

Help on form 2-NDFL | Sample + Instructions 2021

ATTENTION!

From January 1, 2021, the 2-NDFL form will be updated again.

What has changed + new forms can be found in this article.

2-NDFL is an official document about the income of an individual received from a specific source (usually an organization or individual entrepreneur) and the personal income tax withheld from this income.

Organizations and individual entrepreneurs submit certificates only in case of payment of income to employees and other individuals. But individual entrepreneurs do not draw up form 2-NDFL for themselves.

You are required to submit certificates both to the tax office and to your employees.

2-NDFL employees are issued within three working days from submitting an application for a certificate.

A certificate may be needed when leaving a job and moving to another job, filing tax deductions, applying to a bank for a loan, applying for a visa to a significant number of countries, applying for a pension, adopting a child, submitting documents for various benefits, etc. .

Due dates

Tax certificates are submitted once a year:

- no later than April 1 (until April 2, 2021, since the 1st is a day off);

- until March 1, if it is impossible to withhold personal income tax (certificates with sign 2).

Information about the income of non-employees in the company

In the following common cases, we must file income information for individuals not employed by the company:

- The company paid for the work/services under the contract;

- The LLC paid dividends to participants;

- Property was rented from an individual (for example, premises or a car);

- Gifts worth more than 4,000 rubles were presented;

- Financial assistance was provided to those not working in the organization/individual entrepreneur.

When not to submit 2-NDFL

There is no obligation to file 2-NDFL when:

- purchased real estate, a car, goods from an individual;

- the cost of gifts given by the company is less than RUB 4,000. (in the absence of other paid income);

- damage to health was compensated;

- financial assistance was provided to close relatives of a deceased employee/employee who retired from the organization or to the employee/retired employee himself in connection with the death of his family members.

In what format to submit 2-NDFL

1) If the number of completed tax certificates is 25 or more, you need to transmit 2-NDFL via telecommunication channels (via the Internet), for which an agreement must be concluded with a specialized organization (operator of electronic document flow between taxpayers and inspectorates).

The list of operators can be viewed on the tax service website. You can also use the Federal Tax Service website to submit certificates.

2) If the number is smaller, you can submit certificates on paper - bring them in person or send them by mail.

When submitting 2-NDFL in paper form, a register of information on income is also compiled - a consolidated document with data about the employer, the total number of certificates and a table of three columns, the first of which contains the numbers of the tax certificates submitted, the second indicates the full name of the employees, the third their dates of birth are indicated.

The register also reflects the date of submission of the certificates to the tax authority, the date of acceptance and the data of the tax officer who accepted the documents. The register is always filled out in 2 copies.

The current form of the register is given in the order of the Federal Tax Service of Russia dated September 16, 2011 No. ММВ-7-3/ [email protected] When submitting via the Internet, the register will be generated automatically and there is no need to create a separate document.

When accounting is carried out in a special program (for example, various versions of 1C Accounting), personal income tax reporting is generated automatically; all that remains is to double-check the correctness of filling out. Also, some developers offer separate programs for filling out personal income tax reporting (for example, the resource 2ndfl.ru).

Instructions for filling out the 2-NDFL certificate

We indicate:

- The year for which 2-NDFL was compiled;

- Serial number of the certificate;

- Date of compilation.

Specify the value:

- “1” – in all cases where personal income tax was withheld, if the certificate is submitted by a tax agent (“3” – if the form is submitted by the legal successor of the organization or its OP on the same grounds);

- “2” – when it was not possible to withhold personal income tax if the document is submitted by a tax agent (“4” – if the form is submitted by the legal successor on the same basis).

The need to provide 2-personal income tax with sign 2 may arise in such common cases as:

- Presenting a non-monetary gift worth more than 4,000 rubles to a person who is not an employee of the company;

- Payment of travel and accommodation for representatives of counterparties;

- Forgiveness of debt for a resigned employee.

It should be borne in mind that submitting a certificate with feature 2 does not cancel the obligation to submit a certificate with feature 1 for the same income recipient.

Column "Adjustment number"

When the certificate is submitted for the first time, “00” is entered. If we want to correct the information from the previously provided certificate, the column indicates a value greater than the previous one by one - 01.02, etc.

If a cancellation certificate is submitted to replace the one submitted earlier, “99” is indicated.

Note: when filling out the corrective document, the successor of the tax agent must indicate the number of the certificate submitted by the previously reorganized company and the new date of preparation.

Code of the tax office with which the organization or individual entrepreneur is registered

You can find out on the Federal Tax Service website through this service).

Section 1

OKTMO is the All-Russian Classifier of Municipal Territories. The code can be viewed on the tax service website in this service).

Individual entrepreneurs on UTII and PSN indicate OKTMO at the place of business in relation to their employees employed in these types of business.

The legal successor of the tax agent fills out OKTMO at the location of the reorganized company (RP).

Extracted from the tax registration certificate. In 2-NDFL for employees of separate divisions, OKTMO and KPP of these divisions are indicated. Individual entrepreneurs do not indicate checkpoints.

If the certificate is submitted by the successor of the tax agent, the TIN/KPP of the legal successor is filled in.

The abbreviated (if absent, full) name of the organization (full name of the entrepreneur) is indicated.

If the certificate is submitted by the legal successor, the name of the reorganized company (RP) should be indicated.

Reorganization (liquidation) codes

In the “Form of reorganization” field, the codes of reorganization (liquidation) of the legal entity (LP) are indicated:

| Code | Name |

| 1 | Conversion |

| 2 | Merger |

| 3 | Separation |

| 5 | Accession |

| 6 | Division with simultaneous accession |

| 0 | Liquidation |

The codes of the reorganized company (OP) are entered in the TIN/KPP field.

If the certificate is not submitted for a reorganized legal entity (LE), these fields are not filled in.

If the title of the certificate contains the sign “3” or “4”, these fields must be filled in in the prescribed manner.

Section 2

Indicated by code from 1 to 6:

Code 1 - for all tax residents of the Russian Federation (persons staying in the territory of the Russian Federation for 183 or more calendar days within 12 consecutive months), and for those who stayed less than 183 days, the following codes are indicated:

- 2 – when the recipient of the income is not a resident and does not fall under other codes;

- 3 – if we invited a highly qualified specialist to work;

- 4 – if our employee is a participant in the program for the resettlement of compatriots;

- 5 – if the employee brought a certificate of recognition as a refugee or provision of temporary asylum in the Russian Federation;

- 6 – when our employee is accepted on the basis of a patent (foreign workers from countries whose citizens do not require entry visas to the Russian Federation, with the exception of those included in the Customs Union. For example, citizens of Azerbaijan, Tajikistan, Uzbekistan, Ukraine , temporarily staying in Russia, for the right to work for legal entities and individual entrepreneurs are required to obtain patents).

We determine the status at the end of the year for which information is submitted. Those. if the employee became a resident during the year, in the “Taxpayer Status” column we enter the number 1. This does not apply only to filling out certificates for those working on the basis of a patent (for them, code is always 6).

If the 2-NDFL is issued before the end of the year, the status is indicated as of the date the document was drawn up.

Indicated in accordance with OKSM (All-Russian Classifier of Countries of the World). For example, for Russian citizens this is code 643. For codes for other countries, see this link.

Identity document code

Indicated according to the directory “Codes of types of documents proving the identity of the taxpayer” (see table below). Usually these are codes 21 (passport of a citizen of the Russian Federation) and 10 (passport of a foreign citizen). Next, indicate the series and number of the document.

| Code | Title of the document |

| 21 | Passport of a citizen of the Russian Federation |

| 03 | Birth certificate |

| 07 | Military ID |

| 08 | Temporary certificate issued in lieu of a military ID |

| 10 | Foreign citizen's passport |

| 11 | Certificate of consideration of an application for recognition of a person as a refugee on the territory of the Russian Federation on its merits |

| 12 | Residence permit in the Russian Federation |

| 13 | Refugee ID |

| 14 | Temporary identity card of a citizen of the Russian Federation |

| 15 | Temporary residence permit in the Russian Federation |

| 18 | Certificate of temporary asylum on the territory of the Russian Federation |

| 23 | Birth certificate issued by an authorized body of a foreign state |

| 24 | Identity card of a military personnel of the Russian Federation |

| 91 | Other documents |

Sections 3-5

Indicators (except for personal income tax) are reflected in rubles and kopecks. The tax amount is rounded according to arithmetic rules.

If we paid income that was not subject to personal income tax in full (the list of such income is given in Article 217 of the Tax Code of the Russian Federation), we do not include the amount of such income in 2-personal income tax. For example, 2-NDFL does not reflect:

- benefits for pregnancy and childbirth and child care up to 1.5 years;

- payment to the dismissed employee of severance pay in the amount of no more than three monthly salaries;

- one-time payment at the birth of a child in the amount of up to 50,000 rubles.

Section 3

It includes data:

- about income taxed at one of the rates (13, 15, 30, 35%);

- about tax deductions applicable to these types of income (in particular, amounts not subject to personal income tax).

Income received is reflected in chronological order, broken down by month and income code.

Employee income was taxed at different rates - how to fill it out?

If during the year one person received income subject to taxation at different rates, one certificate is filled out containing sections 3 - 5 for each rate. Those. all employee income, regardless of the type of income, must be included in one certificate.

https://www.youtube.com/watch?v=x53REcKxEq0

If all the data does not fit on one sheet, fill out the second page of the certificate (in fact, we will have 2 completed 2-NDFL forms with the same number).

On the second page, indicate the page number of the certificate, fill in the heading “Certificate of income of an individual for ______ year No. ___ dated ___.___.___” (data in the header, including the number, are the same as on the first page), enter data in sections 3 and 5 (sections 1 and 2 are not filled in), the “Tax Agent” field (at the bottom of the document) is filled in. Each completed page is signed.

An example of such a situation is an organization issuing an interest-free loan to its employee. The recipient of the loan will have both income taxed at a rate of 13% (salary) and income subject to a rate of 35% (material benefit).

If dividends to a participant who works in the organization, they are reflected along with other income. There is no need to fill out separate sections 3 and 5 for dividends.

For example, on June 5, 2021, participant Nikiforov, who also works as Deputy General Director, was paid dividends of 450,000 rubles. In the data for June (see sample above), we will reflect wage income with code 2000 and dividend income with code 1010.

Income and deduction codes

Income and deduction codes are established by orders of the Federal Tax Service (the latest changes were approved by order dated October 24, 2018 No. ММВ-7-11/ [email protected] ). See the full list of income codes here.

But most often you will have to indicate the following:

| The most used deductions for this section:

|

See the full list of deduction codes here.

If there are no total indicators, a zero is entered in the certificate columns.

Salary for December was paid in January – how to reflect it?

In the certificate, income is reflected in the month in which such income is considered actually received according to the norms of the Tax Code. For example:

1) Our employee’s salary for December 2021 was paid on January 12, 2021 - we will reflect its amount in the certificate for 2021 as part of income for December (since, in accordance with paragraph 2 of Article 223 of the Tax Code, the date of receipt income in the form of wages is recognized as the last day of the month for which income is accrued in accordance with the employment contract).

2) For a craftsman working for us under a contract, payment for work completed in December 2021 was made on January 12, 2021 - this amount will be included in 2-personal income tax for 2021 (since

The Tax Code does not provide for separate rules for payment under civil contracts; therefore, we apply a general rule, according to which the date of actual receipt of income is defined as the day of its payment - clause 1 of Art. 223 of the Tax Code of the Russian Federation).

Vacation pay

Source: https://nalog-spravka.ru/spravka-2-ndfl.html

Where to submit 2-NDFL

Messages about the impossibility of withholding personal income tax in form 2-NDFL are submitted to the Federal Tax Service (Clause 2 of Article 230 of the Tax Code of the Russian Federation):

- at the location of the organization (the largest taxpayers - at the place of registration as a “large enterprise”);

- at the location of the OP paying income to individuals;

- at the place of residence of the individual entrepreneur. True, if an individual entrepreneur uses UTII and/or PSN, then certificates for employees engaged in imputed activities and/or PSN activities must be submitted to the Federal Tax Service at the place of conduct of such activities.

A new income certificate 2-NDFL has been approved

Form 2-NDFL

– this is a certificate of income of an individual. This certificate is generated by the employer (tax agent) for the employee (individual) who was paid a salary (or other income subject to personal income tax) during the year.

In addition, at the request of the employee, the employer is obliged to issue him a certificate of income in hand. Typically, an individual provides this certificate to the bank to receive a loan, to the tax office to receive deductions, to a new employer, etc.

The 2-NDFL certificate form is approved by the Federal Tax Service. This year, by order dated November 2, 2021 No. ММВ-7-11/ [email protected], the tax authorities not only changed the certificate form, but approved two forms at once.

- The first form

has a machine-readable format and is submitted to

the tax authority

. The abbreviated name of the form is 2-NDFL. - The second form

has a familiar appearance.

This certificate is issued to the employee

. The abbreviated name of the form is missing.

Download the new form 2-NDFL

Download a new form for a certificate of income for an individual

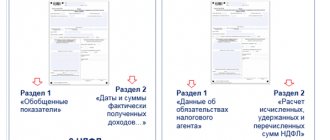

The new form has 3 sections and 1 application.

In the title

The form contains information about the employer: TIN, KPP, name of the organization / full name of the entrepreneur, OKTMO, etc.

In the “Sign” field the following should be entered: 1 for a regular certificate, 2 – for a certificate with information about the impossibility of withholding tax, 3 and 4 – to be filled in by legal successors during the reorganization of a legal entity.

The attribute of the certificate affects the deadline for submitting form 2-NDFL to the tax authority

In Section 1

The employee’s details are indicated: full name, tax identification number, date of birth, etc.

In the field “ Taxpayer Status”

» indicates: 1 – tax resident, 2 – non-resident, 3 – highly qualified foreign specialist, 4 – migrant, 5 – refugee, 6 – foreigner with a patent.

In Section 2

The total amount of income and tax is reflected.

In the “Tax Base” field, enter the amount of income from the Appendix, reduced by deductions from the Appendix and Section 3.

The indicator “Calculated tax amount” is the product of the tax base and the tax rate.

In Section 3

standard, social and property tax deductions are indicated, as well as data on notifications from the tax authority confirming the right to a tax reduction.

In the “Notification type code” field you need to put: 1 – for a property deduction, 2 – for a social deduction, 3 – for a tax reduction on fixed advance payments.

In the application

a breakdown of information on income and deductions (for specific income) by month according to the tax rate is reflected.

The certificate includes only income that is subject to personal income tax. For example, child care benefits for children under 1.5 years of age are not reflected in the certificate.

The amount of income is indicated in full, without reduction for taxes and deductions. Deductions provided for specific income, for example, 4,000 rubles. for gifts are indicated next to each other in the Appendix. Standard deductions, for example, 1400 rubles. per month per child, are reflected in the total amount in Section 3.

For income taxed at different rates, Sections 1-3 and the Appendix must be completed separately.

filling out a new form 2-NDFL

The procedure for filling out an income certificate for an employee

The form of the certificate has changed slightly. The new form does not contain fields that were needed only by tax authorities: certificate number, information about the notification from the tax authority about the right to reduce taxes, etc.

filling out a new income certificate for individuals

When to apply new certificates?

The order comes into force on January 1, 2021. Therefore, starting from 2021, you need to fill out 2‑NDFL for 2021 on new forms. Certificates for 2021 are filled out using the old form.

A new income certificate 2-NDFL has been approved

Form 2-NDFL

– this is a certificate of income of an individual. This certificate is generated by the employer (tax agent) for the employee (individual) who was paid a salary (or other income subject to personal income tax) during the year.

Tax agents annually submit 2-NDFL information for each employee to the tax office:

- until April 1

, regular certificates, - before March 1

, a certificate stating that the tax has not been withheld.

In addition, at the request of the employee, the employer is obliged to issue him a certificate of income in hand. Typically, an individual provides this certificate to the bank to receive a loan, to the tax office to receive deductions, to a new employer, etc.

- How can an employee obtain an income certificate?

New forms of certificate 2-NDFL

The 2-NDFL certificate form is approved by the Federal Tax Service. This year, by order dated November 2, 2021 No. ММВ-7-11/ [email protected], the tax authorities not only changed the certificate form, but approved two forms at once.

- The first form

has a machine-readable format and is submitted to

the tax authority

. The abbreviated name of the form is 2-NDFL. - The second form

has a familiar appearance.

This certificate is issued to the employee

. The abbreviated name of the form is missing.

Download the new form 2-NDFL

Download a new form for a certificate of income for an individual

Accrual of penalties

Provided that all the necessary information in the prescribed form and in writing was provided to the relevant authorities on time, the tax agent does not receive any penalties, and no penalties are charged.

In the absence of warning information that the calculated personal income tax will not be withheld, and also despite the fact that the ability to withhold funds has not yet been lost, certain sanctions may be applied to the tax agent.

In such a situation, a special on-site inspection is carried out, after which a decision is made, according to which a penalty is charged. In this case, the taxpayer is sent a demand to pay the calculated personal income tax.

According to the law, after the tax period ends and the message is provided on time to both the taxpayer and the tax service, the obligation to pay the calculated funds passes to the individual who received the income. In this case, all duties of the tax agent cease.

An individual is obliged to independently submit a personal income tax return to the relevant authorities and pay the required amount. For failure to comply with this requirement, penalties are imposed not on the organization, but on the taxpayer.

It's useful to study here:

- Letter of the Federal Tax Service of the Russian Federation dated November 22, 2013 No. BS-4-11/20951. It is indicated that penalties are charged if the tax agent did not report the impossibility of withholding personal income tax.

- Letter of the Federal Tax Service of the Russian Federation dated August 22, 2014 No. SA-4-7/16692. Later clarification of similar situations.

- Letter of the Federal Tax Service of the Russian Federation No. SA-4-7/16692. It is indicated that if the tax period has ended and the message about the impossibility of withholding personal income tax has been properly completed, the burden of responsibility for paying taxes passes to the individual.