Posting penalties according to the Writ of Execution through Bailiffs in State Institutions

For information: If, by a court decision, the state duty is transferred by the defendant institution to the budget, then the expenses should be attributed to expense type 852 “Payment of other taxes, fees” and KOSGU code 291 “Taxes, duties and fees”.

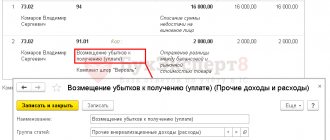

Having considered the issue, we came to the following conclusion: Expenses associated with payments under the writ of execution in terms of reimbursement of legal expenses to the plaintiffs are subject to attribution to the expense type code 831 in conjunction with subarticle 296 “Other expenses” of article 290 “Other expenses” of the KOSGU.

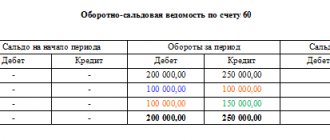

Postings for the accrual of penalties in a budgetary institution

When choosing an account for reflecting settlements for the payment of a penalty, it is necessary to proceed from the definition of the entity to which this penalty will be transferred.

In a situation where the supplier is the recipient of budget funds, the contract may provide for the transfer of the amount of the penalty to the income of the corresponding budget. In other situations, the amounts of the penalty are transferred directly to the supplier. Element of types of expenses 831 “Execution of judicial acts of the Russian Federation and settlement agreements. » is used, in particular, in the execution of court decisions and settlement agreements for the payment of penalties and fines under state (municipal) contracts for the supply of goods, performance of work, provision of services for state (municipal) needs.

It should be taken into account that the settlement agreement is also approved by the arbitration court (Part 1 of Article 141 of the Arbitration Procedure Code of the Russian Federation). That is, in the case of voluntary payment of a penalty by an institution, expense type code 831 does not apply. Each of the taxes existing for a legal entity must be paid on time. Consequently, it does not matter for what type of payment the tax penalty was accrued.

The postings are identical. Each day of delay on any of the obligatory contributions to the budget is punished equally strictly. Penalties are of sufficient size in monetary terms to hurry the debtor to pay the bills as quickly as possible.

The payment of penalties is reflected in the accounting records with the entry Dt 68 “Penies” Kt 51. Another account can also act as the credited account.

For example, “Cash” or “Settlements for short-term loans”, if the penalty was paid from funds received as a loan. As you can see, the accrual of penalties is unprofitable for the enterprise: when it is repaid, the payment obligation is reduced, but the loss is not covered by anything. For violations of fulfillment of obligations under contracts to counterparties, penalties are also applied, they are called penalties. There are two types of penalties - fines and penalties (Art.

330 of the Civil Code of the Russian Federation), which can be collected both through the court and on a voluntary basis. If penalties are accrued on contributions, accounting entries are reflected in account 69.

For the convenience of monitoring the accrual and payment of penalties for tax payments, their analytical accounting should be organized in the context of the relevant taxes. For example, when calculating penalties for VAT, transactions must be reflected in the subaccount of account 68, opened to record the accrual of this tax. If penalty payments are assessed by the company independently, then they must be reflected on the date of calculation and payment to the budget.

When accruing based on the results of an audit, they should be reflected on the date the audit decision came into force. Accounting for settlements with the budget for taxes is organized, in accordance with the chart of accounts, on account 68. Guided by the open list of expenses, the penalty should be displayed on account 91-2, along with this accruing the corresponding tax liability, which is permanent.

In accordance with another position, the penalty is close in essence to a fine, and it must be displayed on account 99. The advantage of this method is the correspondence of accounting data and financial reporting indicators.

Posting penalties according to the Writ of Execution through Bailiffs in State Institutions

The debt of accountable persons is reflected according to the article specified in the current legislation. It must be remembered that the tax sphere is constantly being reformed. If not all amounts have been spent, then the remainder is returned to the company's cash desk. If the amount was overspent, and there is evidence that it was necessary, then the overspending is returned to the employee. The necessity of the expenses incurred is checked and certified by the company management. If the employee received funds for travel expenses, then the advance report and the unspent amount should be submitted to the accounting department no later than 3 working days upon return. As a rule, a writ of execution comes by mail with a notification, which, after receiving it, must be sent back to the bailiffs. In this case, in the notification it is necessary to make a note about the receipt of the writ of execution, indicate its incoming number and date, the telephone number of the enterprise, signature and affix the seal of the organization. For bailiffs, this will be confirmation that the writ of execution has been received and the procedure for withholding the amounts specified in it has begun. Get 267 video lessons on 1C for free:

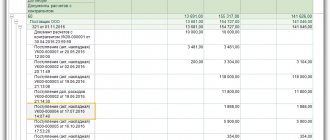

The formula for calculating deductions for claims of the same priority will be as follows: Postings on writs of execution with an example of calculating deductions In accounting, for deductions on writs of execution, account 76 is used. Let's consider an example with postings on deductions from wages on a writ of execution. Let’s say an employee receives two writs of execution for the collection of alimony. Payments under writs of execution: No. 1 – RUB 11,200.00. and No. 2 – RUB 14,200.00. Withholding according to the writ of execution of postings: Account Dt Account Ct Posting amount, rub. Description of the posting Document-basis 26 70 40 450.00 An employee of the enterprise has been paid wages Payroll statement 70 68-NDFL 5 258.50 Income tax has been withheld from the employee's wages 40,450.00 * 13% = 5,258.50 rubles.

This is interesting: PPE standards for health workers

Which entries should be used to reflect payroll transactions?

Accounting Salary entries are accounting records that reflect the facts of accrual of remuneration for the labor of employees.

How to correctly reflect the calculation and transfer of salaries in public sector institutions? We will determine payroll entries for the public sector and non-profit organizations.

September 26, 2021 Evdokimova Natalya

Let's determine the important points when calculating salaries:

- The institution must develop and approve a regulation on remuneration, which is formed taking into account the specifics of the organization’s activities and does not contradict current legislation.

- The salaries of the employees of the institution should be calculated in strict accordance with the approved regulations on remuneration and individual local orders of the head of personnel.

- Regardless of the amount of the advance, which is provided for the first half of the worked period, wages are accrued in full. And on the last day of the month.

- Personal income tax should be withheld from wages and insurance premiums calculated for the entire amount of accruals, without deducting the advance already paid for the first half of the month. The amounts that should be included in the tax base are set out in the Tax Code.

- In 2021, apply the new minimum wage for workers whose salary does not exceed the minimum wage. The minimum wage is regulated by law dated June 19, 2000 No. 82-FZ with the latest amendments.

- Provide in the wage regulations, collective agreement and labor agreements that salary transfers to the organization are carried out at least twice a month.

- Take into account the regional coefficients established in the region where the organization is located. Take into account the amounts of regional surcharges when calculating the minimum wage.

- When terminating an employment contract, make final payments on the employee’s last working day. Moreover, the amount of mandatory compensation calculation does not depend on the reason for dismissal.

- In accounting, use standard entries for budgetary institutions in 2021.

You should follow instructions No. 174n and No. 157n - for public sector institutions, and instructions No. 94n - for non-profit organizations.

Accounting for public sector employees

To reflect the amounts of accrued remuneration for the work of employees of public sector institutions, separate accounting instructions should be applied. In other words, the general Chart of Accounts (Order No. 94n) cannot be applied in this case.

General instructions for organizations are Order of the Ministry of Finance No. 157n. But this is not the only document. Additional recommendations and requirements are given in separate orders:

- Instruction No. 174n - for budgetary institutions.

- Instruction No. 183n - for autonomous organizations.

- Instruction No. 162n - for government-type government agencies.

To keep track of salaries in budgetary institutions in 2021, state employees are required to use account 0 302 10 000 “Calculations for wages and accruals for wage payments.”

To organize reliable synthetic accounting, it is necessary to detail the information. To do this, provide the appropriate analytical accounting codes:

- Code “1” or 0 302 11 000 - is intended to reflect operations for directly calculating wages. For example, on this accounting account reflect the accrued salary, incentives, and compensation payments. If a territorial (district) coefficient is applied to earnings, then reflect these amounts with code “1”. Also include in the group the amounts of accrued vacation pay and sick leave benefits at the expense of the employer.

- Code “2” or 0 302 12 000 - information on other payments in favor of employees is accumulated. For example, this group includes accruals in favor of women receiving benefits for children under three years of age. Currently, the amount of such payment is 50 rubles. If there is a regional coefficient in your region, then include it in the group with code “2”.

- Code “3” or 0 302 13 000 - this group includes all calculations for calculating benefits for illness, pregnancy and childbirth, one-time payments from the Social Insurance Fund. That is, code “3” is intended to reflect charges for wage payments.

The accrual of labor costs is reflected in the credit of account 0 302 00 000, in correspondence with the accounts:

- 0 109 00 000 - when reflecting payments in favor of employees directly involved in the implementation of municipal tasks;

- 0 401 20 000 - for calculating payments to other personnel.

Salary accounting in a budgetary institution

We collected in the table the entries for payroll in a budgetary institution in 2021.

transactionsDebitCreditNote

| Salary accrued | 4 401 20 211 | 4 302 11 730 | Remuneration - CVR 111 Other payments - 112 Benefits and sick leave and insurance contributions - 119 |

| Accrual of sick leave | 4 401 20 213 | 4 302 13 730 | |

| Accrual of other payments | 4 401 20 212 | 4 302 12 730 | |

| Wages accrued to employees of main production, posting | 4 109 61 211 (if the salary is included in the cost) 4 109 71 211 (overhead expenses) 4 109 81 211 (general business expenses) | 4 302 11 730 | |

| Personal income tax withheld | 4 302 11 830 | 4 303 01 730 | |

| Writ of execution withheld | 4 302 11 830 | 4 304 03 730 | |

| Salaries issued from the cash register, posting | 4 302 11 830 | 4 201 34 610 | |

| Transfer to bank cards | 4 302 11 830 | 4 201 11 610 | |

| Unpaid salary deposited | 4 302 11 830 | 4 304 02 730 | |

| Insurance premiums | 4 402 20 213 | 4,303,02,730 (FSS - 2.9%)4,303,06,730 (FSS, NS and PZ - 0.2%)4,303,07,730 (FFOMS - 5.1%)4,303,10,730 (OPS - 22%) |

Accounting for salaries in a government institution

We collected in a table the entries for salaries in a government institution in 2020.

transactionsDebitCreditNote

| Employees' wages accrued | 1 401 20 211 | 1 302 11 730 | For remuneration of state and municipal employees - KVR 121, for payment of benefits and insurance contributions - 129 |

| Sick leave | 1 401 20 213 | 1 302 12 730 | |

| Personal income tax | 1 302 11 830 | 1 303 01 730 | |

| Salary transferred from current account | 1 302 11 830 | 1 201 11 610 | |

| PO issued from the cash register | 1 302 11 830 | 1 201 34 610 | |

| Insurance premiums | 1 402 20 213 | 1,303,02,730 (FSS - 2.9%)1,303,06,730 (FSS, NS and PZ - 0.2%)1,303,07,730 (FFOMS - 5.1%)1,303,10,730 (OPS - 22%) |

Accounting entries for salary: salary in an autonomous institution

transactionsDebitCreditNotes

| Salary accrued | 2 401 20 211 | 2 302 11 730 | Similar for budgetary institutions |

| Personal income tax withheld | 2 302 11 830 | 2 303 01 730 | |

| Union dues withheld | 2 302 11 830 | 2 304 03 730 | |

| Issuing wages from the cash register | 2 302 11 830 | 2 201 34 610 | |

| Salary issued, posting from current account | 2 302 11 830 | 2 201 11 610 | |

| Insurance premiums | 2 402 20 213 | 2,303 02,730 (FSS - 2.9%) 2,303 06,730 (FSS NS and PZ - 0.2%) 2,303 07,730 (FFOMS - 5.1%) 2,303 10,730 (OPS - 22%) |

Accounting in non-profit organizations

Non-profit organizations are required to keep accounting records in accordance with generally accepted standards, in accordance with Order of the Ministry of Finance No. 94n. So, accumulate all accrued remunerations for labor in accounting account 70 “Settlements with personnel for remuneration”.

Regardless of the type of organization (non-profit, budgetary, commercial), keep records of accruals separately for each employee. It is not allowed to enter generalized information on the enterprise as a whole or entries by workshop, section, department, shift.

It is permissible to open corresponding sub-accounts to account 70. For example, to detail information on workshops, departments and other structural divisions of the enterprise.

To reflect the accruals, an entry is made on the credit of account 70 in correspondence with the production cost accounts. For example, to reflect the earnings of core personnel, account 20 “Main production” is used, for support personnel - account 23.

Accounting entries for wages: examples for non-profit organizations

transactionsDebitCreditNote

| Accrued wages, posting for management personnel | 26 | 70 | The salary is calculated in full, regardless of the amount of the advance payment transferred |

| Salary accrued to employees of main production, posting | 20 | 70 | |

| Personal income tax: deduction from wages, postings | 70 | 68 | |

| Salaries were paid from the current account, the posting for the advance is similar | 70 | 51 | |

| Wages have been paid from the cash register, the posting is suitable for reflecting the advance | 70 | 50 | |

| Insurance premiums | 20 (for main production) 26 (for management) | 69/1 (FSS)69/2 (OPS)69/3 (FFOMS) |

The article was prepared using materials from ConsultantPlus. Get access The article was prepared using materials from ConsultantPlus. Get access

Source: https://gosuchetnik.ru/bukhgalteriya/kakie-provodki-ispolzovat-chtoby-otrazit-operatsii-po-zarplate

Postings for deduction from wages according to the writ of execution

- Alimony for minor children;

- Alimony for elderly relatives;

- Compensation for harm caused to both physical and moral health of a person;

- Reimbursement of loans, borrowings and accrued interest;

- Compensation for damage caused to the organization.

The object of withholding is wages after taxation, that is, minus income tax. Payments under the writ of execution are transferred within 3 days from the date of payment of wages.

Reflection of penalties in the institution’s accounting

Thus, at the time the penalty is presented to the supplier or contractor and reflected in the accounting of the tax base, there is no tax base yet, and if the debtor acknowledged the penalty (signed a reconciliation report, wrote a letter of guarantee, paid part of the debt), it is necessary to charge income tax:

If the penalty was subsequently reduced or written off, the institution has the right to adjust the tax base in the general manner, that is, by amending the tax return of the tax period when the penalty was accrued.

Reflection in accounting of collection under a writ of execution

How to reflect in the accounting of a state-owned institution a writ of execution, according to which a debt is collected from a state-owned institution under an agreement with a counterparty for work performed? Those. In what account should the debt to the contractor accrued in accordance with the writ of execution be recorded?

All rights reserved. Full or partial copying of site materials is possible only with the written permission of the editors of the journal “Accounting in an Institution”. Violation of copyright entails liability in accordance with the legislation of the Russian Federation.

Legal costs of posting in accounting

The procedure for payment and the amount of state duty are established by the Law of the Russian Federation of December 9, 1991 “On State Duty” (as amended by No.

dated March 21, 2002, as amended as of December 8, 2003).

The amount of the state fee depends on the price and nature of the claim.

In accordance with paragraph 2 of Article 4 of the said Law, in cases considered in arbitration courts, the state duty is charged in the following amounts: 1) claims of a property nature with a claim price of up to 10 million rubles. 5% of the claim price, but not less than the minimum wage; over 10 million rubles.

up to 50 million rubles 500 thousand rubles. + 4% of the amount over 10 million rubles.

over 50 million rubles. up to 100 million rubles. 2 million 100 thousand rubles. + 3% of the amount over 50 million rubles.

over 100 million rubles. up to 500 million rubles 3 million 600 thousand rubles. + 2% of the amount over 100 million rubles.

over 500 million rubles. up to 1 billion rubles

11 million 600 thousand rubles. + 1% of the amount over 500 million rubles. over 1 billion rubles

Sample application for recovery from a government institution based on a writ of execution

On the pages of the Federal Treasury website you can also find out information about the list of documents submitted by the claimant, current application forms, the procedure for submitting documents, etc. The sample application for recovery from a government institution based on a writ of execution can be found on our website.

When submitting a corresponding application to the Treasury, you should remember the deadlines for payment by state and budgetary institutions of debts under writs of execution. Thus, according to the norms of the Budget Code of the Russian Federation, payment from a government institution that is a debtor must be made to the applicant’s bank account within 10 working days. Note that this condition is mandatory only if there are funds in the debtor’s personal accounts. As for budgetary institutions, the law provides for a more comfortable period for the execution of acts - up to 30 working days from the date of receipt of the executive document.

Debt collection through court (postings)

Sometimes it happens that you have to collect the debt from the debtor under a writ of execution. This is a rather complicated process, since you have to contact the bailiff service. Often, defendants do not agree with the court order and are unwilling to pay the debt voluntarily.

Now we need to deal with VAT. The fact is that it was accrued with the revenue. State duty is not subject to taxation. What about penalties and interest? The fact is that these amounts are connected directly to payments for goods or services, therefore, they should make the VAT base larger.

How to formalize and reflect in accounting deductions under executive documents

When sending the withheld amount by mail, on the back of the postal transfer coupon in the “For written message” section, indicate the details of the writ of execution, the type of deductions and their amount. For example, the entry may look like this: “According to writ of execution No. 125/1 for March 2021, alimony was collected in the amount of 1/3 of A.S.’s earnings. Kondratieva. The amount of alimony is 2160 rubles.”

As a rule, the writ of execution is sent to the bailiff within three days after the employee is dismissed. In relation to alimony, such a period is established by Article 111 of the Family Code of the Russian Federation. For other deductions, the law does not establish a specific period. However, Part 4 of Article 98 of Law No. 299-FZ of October 2, 2021 states that the writ of execution must be returned immediately after the debtor changes his place of work.

This is interesting: Problems of Qualification of Transfer of a Bribe by an Official to an Individual or Legal Entity 2021

Withholding of union dues and personal income tax

In addition, trade unions are not controlled and accountable to government agencies, employers, political parties and other public associations (Clause 1, Article 5 of Law No. 10-FZ). Unions are also independent in the conduct of their financial activities.

Republic of Uzbekistan; for children of its employees under 16 years of age (students up to 18 years of age) to children's and other health camps, as well as to sanatorium-resort and health-improving institutions specially designed for the recreation of parents with children, located on the territory of the Republic of Uzbekistan; q received from a legal entity worth up to 6 times the minimum wage during the tax period: gifts in kind to employees; gifts and other types of assistance to non-working pensioners and persons who have lost their ability to work, who were previously employees of this legal entity, and family members of a deceased employee.

We recommend reading: Young Family Program for Military Personnel

The procedure for recovery from a budgetary institution under a writ of execution

According to Resolution No. 143, you need, in addition to the writ of execution, to issue a duly certified copy of the court decision, on the basis of which this writ of execution was issued. There is some difficulty here, since Art. Article 9 of the law states that to carry out enforcement actions, one document is sufficient - a writ of execution. To get out of this situation, on a copy of the court decision, ask the judge to write not only “The copy is correct,” but also “The decision has entered into legal force.” 3 Submit documents to the executive body through which your debtor is financed. According to the Resolution, the body in which personal accounts of budgetary organizations are opened is the Federal Treasury. Send a certified copy of the court decision and a covering letter to the territorial authority at the place of registration.

- those that are executed through the Ministry of Finance of the Russian Federation, financial authorities of a constituent entity of the Russian Federation or a municipal entity;

- on the obligation of the debtor-budget recipient to perform certain actions (with such writs of execution you need to go to the bailiffs);

- in which the amount of debt is expressed in foreign currency - the Budget Code provides that the amount of debt in the writ of execution must be expressed in rubles.

Penalty under a government contract: practical recommendations

The arbitrators indicated that when deciding the proportionality of the penalty to the consequences of a violation of a monetary obligation and, for this purpose, determining the amount sufficient to compensate for the creditor’s losses, the courts can proceed from the double discount rate of the Central Bank of the Russian Federation in force during the period of such violation. The court's reduction of the penalty below the amount thus established is permitted in exceptional cases. In this case, the awarded amount of money cannot be less than that which would be accrued on the amount of debt based on the one-time discount rate of the Bank of Russia. › |

Thus, only the minimum amount of the penalty is determined by law, and the customer specifies the specific amount (not less than the minimum) at his discretion in the draft contract (Part 10, Article 9 of Law No. 94-FZ). It should be remembered that, by virtue of Article 333 of the Civil Code of the Russian Federation, if the penalty payable is clearly disproportionate to the consequences of violation of the obligation, the court has the right to reduce it.

We recommend reading: Benefits for police officers dismissed due to illness

Collection of money under a writ of execution from a municipal budgetary institution

management And about the duplicate IL and to the bailiffs - the difficulty is that the collection is carried out within the framework of the budget code, and not the law on enforcement proceedings, and the bailiffs usually write off that this is not their competence. There, in order, as I see it, the executive should be sent specifically to the treasury, and you have some kind of financial management. Check this point. A lot of interesting things have been written here.

The courts evaluate the fact of suspension of debit transactions on the debtor's personal account along with other provisions of the Budget Code of the Russian Federation. Failure to comply with a judicial act in itself does not entail automatic suspension of operations on the debtor’s account. Such rules may allow debtors to simply not execute a court decision for a long time with the reference: “no money,” which contradicts the principle of the universally binding requirements of a judicial act and the fact that the treasury cannot be empty by definition.

Writ of execution for recovery from a budgetary or government institution

An autonomous institution has the right to pay targeted expenses from other sources before the targeted subsidy is received in the account. And after the targeted subsidy arrives to the institution, restore the expenses incurred

He is liable for his obligations with all property that he has under the right of operational management (both assigned to the institution by the owner and acquired from income received from income-generating activities). The exception is: – especially valuable movable property, which is assigned to it by the owner (acquired by the institution at the expense of funds allocated by the owner); – real estate (regardless of how it came into operational management and with what funds it was acquired)

Postings in the budget for penalties under the contract

Details Category: Selections from magazines for an accountant Published: 05.28.2021 00:00 Source: Magazine “Institutions of physical culture and sports: accounting and taxation” State (municipal) contracts, as well as civil contracts, provide for conditions on the responsibility of the supplier (performer, contractor) for non-fulfillment or improper fulfillment of obligations and the payment by him of a penalty in favor of institutions. How much is the penalty charged? Do institutions have the right to use the amount of the penalty?

State (municipal) contracts, as well as civil contracts, provide for conditions on the liability of the supplier (performer, contractor) for non-fulfillment or improper fulfillment of obligations and on the payment of penalties to institutions.

Deductions under writs of execution: features of calculation and recording

When collecting funds under enforcement documents, the amount of financial assistance is not included in income. In addition, the calculation is performed based on the amount of income remaining after personal income tax withholding. Thus, the amount of income from which deduction is made according to executive documents will be 16,894 rubles. (15,000 + 4,000 – 2,106).

This is interesting: How many years of medical experience do you need to retire?

a memo for managers and accountants of organizations (enterprises) on the issues of withholding and transferring funds under executive documents. Such a memo is given in Appendix 1 to the Methodological Recommendations (hereinafter referred to as the Memo).

Accounting and legal services

The amount, calculated at 7% of the funds collected under the writ of execution, refers, in fact, to coercive measures in connection with non-compliance with the legal requirements of the state. This measure is a punitive sanction, that is, imposing on the debtor the obligation to make a certain additional payment as a measure of his public legal liability arising in connection with an offense committed by him in the process of enforcement proceedings. The enforcement fee as a penalty has the characteristics of an administrative penalty: it has a fixed monetary value established by federal law, is collected by force, formalized by a resolution of an authorized official, collected in the event of an offense, and is also credited to the state budget. The Ministry of Finance in Letter dated 04/08/2021 N 03-03-06/1/227, based on clause 2 of Art. 270 of the Tax Code of the Russian Federation (according to which, when determining the tax base for income tax, expenses in the form of penalties, penalties transferred to the budget, as well as fines and other sanctions levied by state organizations that are granted the right to impose these sanctions by law are not taken into account), reports, that the amount of the performance fee transferred to the budget is not taken into account as part of tax expenses.

Thank you for choosing Berator Online - a unique accounting publication for a writ of execution - this is a document issued by the court, which indicates the reason and amount. When paying the withheld funds to the claimant from the cash register, make an entry

Debt repayment period under writ of execution

Lawyers recommend that when submitting a document, when submitting a document, you immediately write a request to seize the property, citing the fact that there is information about its possible alienation - in any case, whether there is property or not, such an appeal will not hurt.

After reviewing the writ of execution by authorized bank employees, collection occurs according to a collection order issued by the bank service. According to current legislation, the period for fulfilling the requirements of the judicial authority should not exceed three days after registration of your appeal.

Debt collection from a budgetary institution

We received a decision to collect a debt for a very large amount from a budgetary institution (FGBU). As far as I know, there are three types of state (municipal) institutions: - budgetary - state-owned - autonomous

1) are sheets for such debtors presented to the treasury? Does the BU have accounts there? or do they have accounts in regular banks (I have often seen educational institutions have accounts in the Bank of Moscow, for example, although government agencies are also institutions and they have accounts in the treasury)?

Material damage caused to a budgetary institution

Documenting. According to Art. 247 of the Labor Code of the Russian Federation, before making a decision on compensation for damage by a specific employee, the employer is obliged to conduct an inspection to establish the amount of damage caused and the reasons for its occurrence. To conduct such an inspection, he has the right to create a commission with the participation of relevant specialists, which must establish:

The procedure for determining liability for damage caused and its compensation

Instructions for the application of the Unified Chart of Accounts for public authorities (state bodies), local governments, management bodies of state extra-budgetary funds, state academies of sciences, state (municipal) institutions, approved. By Order of the Ministry of Finance of Russia dated December 1, 2021 N 157n.

- If the amount of mandatory deductions exceeds the limit (70%), then the amount of deductions is distributed in proportion to the mandatory deductions. No other deductions are made;

- The amount of limitation on deductions initiated by the employer is 20%;

- At the request of the employee, the amount of deductions is not limited.

We recommend reading: How to choose a qualifier for the sale of building materials

Postings according to the organization’s writ of execution

The amount of alimony collected is approved in court, therefore, before withholding alimony, the accountant must check what amount is indicated in the writ of execution, because it may differ from the standard share provided for in Art. 81 IC RF. In addition, there is a maximum amount of collected deductions - no more than 70% of the employee’s income (Article 138 of the Labor Code of the Russian Federation).

Recovery is not made from the amounts of severance pay paid upon dismissal of an employee, from the amounts of payments in connection with the birth of a child, with the death of loved ones, with the registration of marriage, as well as other income listed in Art.

Writs of execution: deductions, payments, postings

In the common understanding, deduction under writs of execution is the payment of alimony. In fact, there are other situations where it is necessary to withhold part of an employee’s salary by court order. In this material we will look at what it is and look at the main entries for deductions from an employee’s salary based on a writ of execution.

This obligation covers all employee income, except those that fall under the regulations of Art. 101 of Law 212-FZ.. In addition, the amounts that the organization pays as a commission for making transfers are withheld from him.