Kontur.Accounting - 14 days free!

Personnel records and employee reports, salaries, benefits, travel allowances and deductions in a convenient accounting web service

Try it

When a company employee goes on a business trip, he receives compensation for travel expenses - accommodation and travel costs, communications, visas and other expenses. At the same time, during a business trip, he continues to receive a salary: it is calculated based on average earnings. Also, even before the trip, the employee receives a daily allowance (Part 1 of Article 168 of the Labor Code of the Russian Federation) for each day of the business trip.

Determination of daily allowance

The official interpretation of the concept of “daily allowance” is in the ruling of the Supreme Court of the Russian Federation dated April 26, 2005 No. CAS 05-151. Per diem - funds necessary for the performance of work and accommodation of an employee at the place where the official assignment is carried out.

According to the Supreme Court, an employee is entitled to daily allowance when performing a task not at his permanent place of work and when he is forced to live outside his permanent place of residence.

In practice, an employee often receives a daily allowance only if the business trip lasted more than a day and he spent the night away from home. However, the Supreme Court decision No. 4357/12 dated September 11, 2012 states that the amount of time on a business trip is not related to the calculation of daily allowances. The court allowed enterprises to pay funds to an employee if he went on a business trip for less than a day, since this is reimbursement of his expenses, and not a benefit. In addition, according to Regulation No. 749, daily allowances do not depend on the expenses of a posted employee for housing and travel.

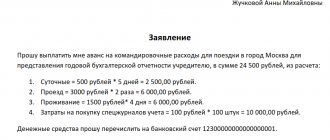

To confirm your daily allowance expenses, prepare your daily allowance calculation using an accounting certificate.

Per diem in a new way

Keep records in Kontur.Accounting - a convenient online service for calculating salaries, travel allowances, benefits and sending reports to the Federal Tax Service, Pension Fund and Social Insurance Fund. Get free access for 14 days

There is no limit on daily allowance; companies can set any amount, stipulating it in internal documents. Small businesses often limit their daily allowance to 700 rubles, because this amount is not subject to personal income tax (clause 3 of Article 217 of the Tax Code of the Russian Federation). If the daily allowance is more, then personal income tax will have to be withheld from the excess amount. For foreign business trips, the tax-free daily allowance limit is 2,500 rubles.

From 2021, daily allowances above the limits are subject to insurance contributions. But there is no need to pay “injury” contributions from the daily allowance.

Example. The employee was on a business trip for 3 days and received a daily allowance of 1,000 rubles. During the days of his business trip he received 3,000 rubles. Only 3 * 700 = 2,100 rubles are not subject to contributions and personal income tax, and from the difference 3,000 - 2,100 = 900 rubles, you need to withhold personal income tax and pay insurance premiums.

What is a business trip

A business trip, according to the Labor Code, is a trip by an employee on behalf of the head of an organization to another city or country to perform various official tasks.

An employee’s trip will not be considered a business trip if his work takes place on the road (driver, driver, etc.), as well as if his work activity is of a traveling nature.

The exact list of positions and specialties that fall into these 2 lists is approved by each employer independently using an order or other local regulation.

When traveling on a business trip, an employee incurs various types of additional expenses (food in catering, housing, transportation, etc.), all of which must be compensated.

During the trip, he retains his place of work in the organization, and is also required to be paid an average salary.

Comment. To eliminate controversial issues regarding the issue of compensation for expenses associated with a business trip, the employer must approve the procedure for its payment in the relevant local regulation.

Typically, the worker is given an advance for the trip, and then he reports on expenses and hands over the remaining funds.

But there are other situations, especially when it comes to business trips of executives.

Russian legislation well protects the rights of workers, including when on business trips.

It establishes the obligation for the employer to pay compensation for additional expenses of the employee himself associated with the trip.

For example, food in canteens/cafes will cost much more than at home, etc.

What is the limit

The legislation does not establish limits for organizations or entrepreneurs regarding reimbursable expenses; similarly, there are no strict limits on the amount of daily allowance.

In fact, each organization (IE) must independently adopt the appropriate local regulatory act and set the maximum amount of compensation paid.

They should be communicated to employees against signature to avoid questions and disputes.

While the worker is required to report for most travel expenses, there is no such rule for per diem. This is simply compensation to him for increased expenses for himself.

This payment, like others, is taken into account by the employer as an expense and reduces income tax.

But releasing any amount as daily allowance could lead to an abuse of power.

Only compensation for additional expenses associated with living in another city (country) within established limits are exempt from taxation.

We provide detailed information on this issue in the following table:

| Type of trip | Across Russia | Outside the country |

| Tax-exempt daily allowance limit | 700 rub./day | 2500 rub./day |

Important! Other expenses (transport, housing) are not included in the daily allowance. Daily allowances are paid for all days of a business trip.

Existing travel expenses

When traveling on business, company employees face various types of expenses.

But we can distinguish 4 main categories of such expenses:

| Travel expenses | They are confirmed by tickets, boarding pass, itinerary receipt, waybill and receipt for gasoline, etc. |

| Rental expenses | When staying at a hotel, they are confirmed by an invoice and a check or BSO. If an employee rented an apartment on a business trip, he will need an agreement and payment documents (BSO, check, account statement) |

| Additional expenses associated with living in another location or country | This is the daily allowance. They don't require any confirmation |

| Other expenses | An employer can compensate an employee on a business trip for other types of expenses, for example, pay for communications. These expenses are reimbursed only if they are made with his permission. |

How much to pay

The legislation does not contain direct instructions on restrictions on the amount of daily allowance. They can be either more than the non-taxable personal income tax limit or less than it.

The specific amount of payments must be fixed in a collective or employment agreement, or approved by local regulations.

This will allow the organization to accept these amounts as expenses even without supporting documents.

Important! Excessively large amounts written off as daily allowances may lead to questions from the tax service.

It is possible that because of this, an additional inspection will be launched, especially if the company’s activities are already suspicious.

During foreign voyages

When traveling to other countries, an employee's expenses are usually higher than when traveling within Russia.

The employer will also have to compensate for living expenses, transportation, etc., as well as pay per diem. The personal income tax-free limit for foreign trips will be higher – 2,500 rubles.

But this does not mean that the organization will not be able to pay a larger daily allowance for its employee.

If the daily allowance is established in the LNA or contract in the amount of 3000 rubles. per day, then from the amount of 500 rubles. (RUR 3,000 – RUR 2,500) will need to withhold and pay personal income tax in the prescribed manner.

If, when traveling around Russia, business trip dates are confirmed using tickets or waybills, then on foreign voyages this is done by stamps from customs authorities in the international passport.

Moreover, if an employee is sent to Belarus or Kazakhstan, then they will not be marked.

In this case, you can also rely on travel documents or waybills.

Across Russia

The most common business trips are within the country. In this case, the employer must compensate for expenses associated with accommodation, payment for transport services and also pay daily allowance.

Only amounts up to 700 rubles are not subject to personal income tax. in a day. But this does not mean that the employer cannot set daily allowances for employees only within this limit and not a penny more.

It is quite acceptable that the company will establish in the regulations on business trips, labor or collective agreements a larger daily allowance, for example, 1000 rubles.

In 1 day

An employee may not necessarily travel for several days to carry out an assignment from the employer.

Often issues can be resolved in 1 day. In this case, the employer still arranges the trip in accordance with the general procedure.

He will have to issue an order, issue the required advance, etc. upon returning from the trip, the employee will have to submit the appropriate reports to the accounting department and management.

According to the general rule, when traveling for 1 day within the territory of the Russian Federation, the employer does not pay daily allowances.

But this does not mean that he cannot compensate for other employee expenses, for example, food.

They must be confirmed with documents, and the compensation rules must be specified in the company’s local regulations.

If the amount spent does not exceed 700 rubles, then, according to the Ministry of Finance, there will be no need to withhold personal income tax. Likewise, insurance premiums are not paid from these expenses.

Of course, it’s rare, but there are still short-term business trips outside of Russia. In this case, the rule applies regarding the payment of daily allowance in the amount of 50% of the established norm in the organization.

In this case, the amount up to 2500 rubles will not be taxed. At least the Ministry of Finance gives such instructions in its letters.

Withholding personal income tax and paying contributions from daily allowances

According to paragraph 4 of Art. 226 of the Tax Code of the Russian Federation, personal income tax must be calculated and withheld on the nearest date of payment of cash income to the employee. Before this, management must approve the advance report (according to the letter of the Ministry of Finance of Russia dated January 14, 2013 No. 03-04-06/4-5). This is due to the fact that the employee, even before the advance report, may underuse the funds allocated to him on a business trip: the employee is obliged to return the excess. The opposite situation: the employee exceeded the allocated amount (for example, due to delays in work matters or simply overspent).

Money that is allocated to a posted employee for reporting purposes is not considered an economic benefit until the employee returns from a business trip and the subsequent approval of the expense report. Before payment, the employee must provide documents about the time of the business trip and attach receipts explaining the expenses.

Contributions from excess amounts must be paid before the 15th day of the next month (Federal Law of July 3, 2021 No. 243-FZ).

KVR

One of the essential requirements of the approved structure of types of expenses, enshrined in clause 46.5 of Procedure No. 85n, is the reflection of travel expenses * (4), as follows:

- issuance of cash to seconded workers (employees) (or transfer to a bank card) on account of the guaranteed expenses listed above - according to CVR 112 “Other payments to personnel of institutions, with the exception of the wage fund”, 122 “Other payments to personnel of state (municipal) authorities, with the exception of the wage fund", 134 "Other payments to military personnel and employees with special ranks" and 142 "Other payments to personnel, with the exception of the wage fund" (see also clause 48.1.1.2, clause 48.1.2.2, clause 48.1.4.2 clause 48 of Order No. 85n);

- payment for the purchase of tickets for travel to and from the place of business trip and (or) rental of residential premises for seconded workers under agreements (contracts) - according to KVR 244 “Other procurement of goods, works and services”.

Thus, Procedure No. 85n clearly establishes the use of various CVRs when reimbursing an employee’s expenses and when an institution purchases services for him under a contract.

More on the topic: Consultation line “Accounting in 1C: BSU”. Issue No. 41/20

Note! According to clause 46.5 of Procedure No. 85n, the list of other expenses incurred by a posted employee with the permission or knowledge of the employer, attributable to CVR 112, 122, 134 or 142, is determined by the employer in a collective agreement or local regulation (due to the specifics of the activities of individual main managers of budget funds - in a normative legal act). That is, if the relevant act does not indicate certain expenses incurred by an employee on a business trip with the knowledge of the employer, they cannot be attributed to CVR 112, 122, 134 or 142. In this case, the expenses will be attributed to CVR 244 * (5) .

As we can see, the attribution of travel expenses can be carried out according to various CVR and KOSGU, depending on whether funds are issued (compensated) to the employee or whether the institution purchases services for him. And the procedure for attributing other expenses incurred by an employee on a business trip depends on the availability of a list of such expenses, enshrined in the relevant act, and the presence of specific expenses in such an act.

Along with the above, it is interesting that if the purpose of the business trip is the purchase of material supplies, for example, fuels and lubricants, then the purchase costs should be reflected according to KVR 244 and subarticle 343 of KOSGU (letter of the Ministry of Finance of Russia dated March 15, 2019 No. 02-05-10/17872 ).

Let us remind you that the CWR and KOSGU expenditure subitems are used in mutual coordination. In this regard, we advise you to always check the CVR for coordination with the articles (sub-articles) of the KOSGU according to what is posted by the Ministry of Finance of Russia on its official website (www.minfin.ru). Please note: the table of correspondence between the CWR and the articles (subarticles) of the KOSGU related to expenses often undergoes changes. At the time of preparation of the material, the correspondence table posted on the website of the Ministry of Finance of Russia on 04/09/2020 is valid (Budget - Budget classification of the Russian Federation - Methodological office).

Proof of business purpose of travel

Keep records in Kontur.Accounting - a convenient online service for calculating salaries, travel allowances, benefits and sending reports to the Federal Tax Service, Pension Fund and Social Insurance Fund. Get free access for 14 days

In 2015, the list of documents confirming the business nature of a business trip changed. Now you don't need:

- Travel certificate;

- Service assignment;

- Report on the completion of a job assignment;

The company has the right to independently determine the document that describes the business part of the trip. The main purpose of an employee on a business trip can be stated in the business trip order, which is drawn up in form No. T-9; it is also not prohibited to create your own forms in accordance with the internal standards of the company.

You can request a written report from the employee on the results of the trip, if such a right is specified in the company’s internal documentation. In this case, familiarize employees with this local act.

To confirm the period of stay on a business trip, the employee is required to provide documents with travel dates (train ticket, plane boarding passes, etc.). If an employee went on a business trip in his own or official transport, he needs a service note (clause 7 of the Decree of the Government of the Russian Federation of October 13, 2008 No. 749).

Payment for hotel accommodation

The legislation establishes the employer's obligation to pay losses incurred in connection with paying for a hotel on a business trip. But, in addition to this provision, the company can independently develop and adopt internal legal acts regulating the procedure for reimbursement of expenses.

The main provisions that make it possible to pay for accommodation on a business trip are:

- The dispatch of an employee on official business must be accompanied by the issuance of a work trip order. Such a document certifies the employee’s actions in the interests of the organization.

- Payment of expenses is carried out on the basis of documentation confirming accommodation. This is a prerequisite for compensation of such expenses.

- Legal entities have the right to set limits on the amounts possible for reimbursement. This rule is most typical for government agencies and is aimed at preserving budget funds. They set a minimum limit for their employees.

IMPORTANT! Budgetary organizations do not have the right to refuse to reimburse an employee for expenses incurred on a business trip. The existence of an order to go on a work trip and provide proof of residence, institutions are required to compensate for the costs.

How to confirm expenses on a business trip

Keep records in Kontur.Accounting - a convenient online service for calculating salaries, travel allowances, benefits and sending reports to the Federal Tax Service, Pension Fund and Social Insurance Fund. Get free access for 14 days

According to Decree of the Government of the Russian Federation dated July 29, 2015 No. 771, the actual time that an employee was on a business trip is determined based on the travel documents provided by the employee.

If the travel document is lost, the accounting department has the right to refuse compensation for its cost.

Example: A company employee lost his boarding pass for an airplane. He flew on a business trip for two days, paid for the ticket from his own money in hopes of compensation. The accounting department initially refused to pay him, since he did not have a document in his hands confirming that the flight had taken place. As a result, the employee had to go to the airport to request documents. confirming his flight.

Employees who go on a business trip using transport (personal, work or rented) are also entitled to compensation. For them, travel documents will be waybills, payment receipts, invoices, checks, etc.

Refund of compensation in case of trip cancellation and force majeure

Keep records in Kontur.Accounting - a convenient online service for calculating salaries, travel allowances, benefits and sending reports to the Federal Tax Service, Pension Fund and Social Insurance Fund. Get free access for 14 days

If a planned business trip is cancelled, the employee can receive money for unused tickets. You can also get a refund of the amount spent on obtaining a visa except for the fee paid.

It is worth considering that when returning tickets, the airline in most cases returns only part of their cost (especially on cheap fares). In this case, the difference in the amount paid and the amount returned is usually justified as a fine for violation of transportation rights.

If force majeure occurs during the business trip itself (bad weather, flood, plane breakdown, etc.) and the employee cannot return home on time, then the company must provide him with daily allowance and pay for the necessary accommodation. In this case, the employee must put a stamp/mark on the travel document (certificate) with the actual date of departure. If a travel document is not provided for by the organization’s accounting policy, then a document confirming the fact that the employee was delayed through no fault of his own can be a certificate from the airport about the cancellation or delay of the flight.