What does an individual entrepreneur pay without employees? An individual entrepreneur (IP) is an individual who has passed state registration for the right to engage in business in accordance with the requirements of the law.

Can an individual entrepreneur work without employees?

The economic activities of an individual entrepreneur are carried out by him practically on the same regulatory conditions as the activities of legal entities. There are certain differences:

- Only legal entities are allowed to engage in certain types of activities;

- Several simplified taxation options are allowed for entrepreneurs.

Unlike legal entities, an individual entrepreneur can carry out its activities independently and carry out accounting without the involvement of hired employees. Typically, this form of existence is preferred by persons who receive profit from the services provided, for example, accounting operations, IT services, legal advice, training, and so on.

On the other hand, if an individual entrepreneur still attracts workers, but does not formalize them, then he bears responsibility similar to legal entities. The amount of the fine can range from 1 to 5 thousand rubles for each employee with whom an employment contract has not been concluded within 3 days. In addition, regulatory authorities may suspend activities for up to 3 months.

Who can choose the simplified tax system and who is prohibited from doing so?

To determine for yourself the most suitable tax regime, if you do not plan to attract people to your staff, you need to understand how an individual entrepreneur reports to the simplified tax system without employees. After all, according to most experts, this category is the most profitable option. However, there are a number of conditions under which it is not possible to switch to simplification:

- Number of more than 100 employees.

- Annual income is more than 150 million rubles.

- The residual value of the property is more than 150 million rubles.

In addition, in some types of activities such a regime is also unacceptable and simplified reports are not allowed. An individual entrepreneur without employees cannot apply for the simplified tax system if he is engaged in:

- Production of excise goods.

- Activities in the banking sector.

- Minerals.

- Lawyer activity.

- Insurance.

- Providing notarial services.

- Gambling.

- Activities in the field of investments and securities.

- Microloans.

- Providing recruitment services.

- Government activities.

- Foreign operations.

Taxes

If the activity is carried out directly by the entrepreneur himself, then the fees are correspondingly reduced, since there is no need to pay payroll taxes.

Interesting: How much taxes does an individual entrepreneur pay - an overview of tax regimes and rates.

What taxes do individual entrepreneurs without employees pay?

The list of taxes paid and reports submitted depends on the chosen taxation scheme.

simplified tax system

Under the simplified taxation system (STS), individual entrepreneurs without employees are required to pay income tax and insurance premiums. If there are taxable objects, the following will be additionally charged:

- property tax on property included in the regional list;

- VAT on imports.

The income tax rate depends on what exactly is chosen as the basis for calculation.

- 6 percent is charged on all income;

- if income decreases by the amount of confirmed expenses, then the rate is 15%.

When calculating, it is necessary to take into account the nuances for each option:

The 6% tax is calculated on the total amount of income, but when paid it is reduced by a fixed amount of insurance premiums. Thus:

- if the income tax is less than or equal to the insurance payment, then it is not paid;

- if the tax is higher, then the difference is transferred to the budget after subtracting a fixed amount.

15% tax is charged on the amount of income minus expenses, including insurance premiums. But this formula applies only to entrepreneurs who declare profits, i.e. excess of income over expenses. If a loss or minimal income is declared, there are two options for calculating income tax:

- in case of loss – 1% of the total income is paid;

- for profits not exceeding 1% of income, a minimum tax of 1% is paid.

Important! How is personal income tax calculated for individual entrepreneurs using the simplified tax system without employees? If an individual entrepreneur works alone under the simplified tax system, he is exempt from personal income tax, since the tax is included in a single payment from profit under a simplified system, annually transferred to the budget. At the same time, there is no exemption from mandatory contributions to compulsory medical insurance and compulsory health insurance. In addition, if the income exceeds 300 thousand rubles, the individual entrepreneur must pay an additional 1% on the excess amount. Consequently, for such individual entrepreneurs, the issue of filing a declaration in form 3-NDFL is not relevant, since the purpose of this declaration is to reflect the payment of this tax.

UTII for individual entrepreneurs without employees

Entrepreneurs can choose a single tax on imputed income if they are engaged in activities that local authorities have included in a special list. In this case, the tax is not charged on actual income, but on the estimated amount that a business representative in this area can receive. The tax rate is determined by local authorities and can range from 7.5 to 15% of the basic income. The imputed income system does not exist in all regions and is fully regulated by decisions of municipal authorities.

Interesting: Will UTII for individual entrepreneurs be canceled from 2021 to 2021 and what will happen in return?

Patent

A simplified system in the form of acquiring a patent applies to entrepreneurs engaged in activities included in the relevant list. At the level of the Russian Federation, the adopted list contains more than 60 items, mainly services provided to the population and retail trade. Municipal authorities can add types of activities that they consider relevant in the region, but do not have the right to exclude those established by the state. The acquisition of a patent exempts the entrepreneur from paying other taxes, including income tax.

An individual entrepreneur on a patent without employees must take into account that the cost of a patent depends on the region and occupation. Every year local authorities publish a list indicating the cost.

BASIC

The general tax system provides for the payment of personal income tax in the amount of 13% of the amount of income received, adjusted by the amount of confirmed expenses or by 20% of income if there is nothing to confirm expenses. Individual entrepreneurs also have the right to use other types of deductions provided for by law.

This system usually involves the payment of VAT and is used when working with legal entities.

It is important to know! To receive benefits from the state in social areas, financial assistance from federal or municipal authorities, or obtain a loan, individuals must provide a certificate of available income, since the amount of assistance directly depends on the amount of income of the applicant. In order to confirm the income received, citizens of the Russian Federation submit certificates issued and executed by employers according to the 2-NDFL form approved by law. An individual entrepreneur can also take advantage of this rule.

How much are mandatory contributions?

All entrepreneurs are required to pay annual insurance premiums for themselves and their employees. If an individual entrepreneur works alone, then he pays a mandatory fixed amount of insurance premiums. In 2019 this amount is 36,238 rubles. Those. if the amount of annual income does not exceed 603,966 rubles, then the income tax is zero and you will have to pay only to the insurance fund. For individual entrepreneurs whose annual income exceeds 300 thousand rubles, the amount increases by 1% of the excess amount.

Fixed insurance premiums are paid by individual entrepreneurs in any case, regardless of the presence of activity. An entrepreneur can receive a deferment if in the reporting year he served in the army, cared for a child under 1.5 years old, an elderly person over 80 years old, or a disabled person.

How to report to the tax authorities

The main type of reporting to the tax service is an income statement. Its form may differ for different taxation systems and is approved by the Federal Tax Service.

Deadlines for filing returns for quarterly reporting for individual entrepreneurs without employees

Individual entrepreneur reporting on the simplified tax system without employees

Individual entrepreneurs and the simplified tax system submit a declaration after the end of the tax period (calendar year), as well as when deciding to terminate official activities and before closing the individual entrepreneur.

The annual declaration must be submitted next year by April 30.

The absence of economic activity does not relieve one from the obligation to submit a declaration and from fines for its absence or late submission.

UTII

The peculiarity of reporting for individual entrepreneurs without employees for imputation (imputed tax) is a quarterly base period. Those. During the year, 4 declarations must be submitted by the 20th day in April, July, October and January.

Penalties are provided in the same amount as for other forms of reporting.

workers

Patent

If an entrepreneur pays for a patent and does not conduct other types of activities, then they do not submit a declaration. The exception is cases if income for the year exceeds the maximum threshold provided for this taxation system (60 million rubles).

Individual entrepreneur reporting on OSNO without employees

Under the general taxation system, the income declaration is submitted quarterly, but the information in it is indicated on an accrual basis, starting from the beginning of the year. When calculating tax, you can take into account expenses and losses of previous periods.

Interesting: Refund of overpaid tax for individual entrepreneurs: procedure, terms of return, offset of the amount.

Rules for conducting cash transactions for individual entrepreneurs

Conducting cash transactions for both legal entities and individual entrepreneurs is regulated by Bank of Russia Directive No. 3210-U dated March 11, 2014 (hereinafter referred to as Directive No. 3210-U). For individual entrepreneurs, this document provides simplified rules. Allowed:

- do not set a limit on the balance of money in the cash register (clause 2 of instruction No. 3210-U);

- do not draw up cash documents: cash receipts and debit orders (clause 4.1 of instruction No. 3210-U);

- do not keep a cash book (clause 4.6 of instruction No. 3210-U).

Let us note that in the mentioned instructions for the last two paragraphs the condition is specified for the entrepreneur to maintain tax records of income, income-expenses, and physical indicators. An individual entrepreneur can apply a general, simplified or patent taxation system, and be a taxpayer of the Unified Agricultural Tax or the Unified Income Tax.

ATTENTION! Starting from January 2021, UTII will lose force throughout the Russian Federation.

What should UTII residents do in connection with the abolition of the special regime, read in the Typical situation from ConsultantPlus. Study the material by getting trial access to the K+ system for free.

For OSNO, accounting is kept in the book of income and expenses and household expenses. operations (clause 4 of the Procedure for accounting for income and expenses and business transactions for individual entrepreneurs, approved by order of the Ministry of Finance and the Ministry of Taxes of the Russian Federation dated August 13, 2002 No. 86n/BG-3-04/430). For all other systems, except UTII, tax accounting is kept in the book of income or income and expenses (Article 346.24, Article 346.53, clause 8 of Article 346.5 of the Tax Code of the Russian Federation), and for UTII physical indicators are taken into account (Article 346.9 of the Tax Code of the Russian Federation ). Consequently, individual entrepreneurs on any taxation system can take advantage of the relaxations given by Directive No. 3210-U.

Read more about special regimes for calculating and paying taxes in the sections of our website:

- STS in 2020–2021 - changes, payment deadlines, reporting;

- UTII for legal entities and individual entrepreneurs (latest changes);

- Unified Agricultural Sciences;

- PSN.

Thus, individual entrepreneurs are exempt from registering a primary cash register. But if a decision is made to use PKO and RKO, then they must be drawn up taking into account all the norms of Directive No. 3210-U. In the case when an individual entrepreneur refuses to use PKO and RKO, it is advisable to use other types of documentation, for example, recording income and expenses in an Excel file or in a regular notebook in order to monitor the availability of funds.

In addition, individual entrepreneurs often keep records in common accounting programs applicable to organizations. The movement of cash in these programs is documented by expenditure and receipt cash orders. Therefore, for such entrepreneurs, it is easier to properly register receipts and consumables - this way, confirmation of cash withdrawals and their contributions will be preserved, which will facilitate the accounting of the entrepreneur and help avoid disagreements with employees. The cash book may not be maintained, despite the presence or absence of PKO and RKO.

Online cash register for individual entrepreneurs without employees

In recent years, there has been a gradual introduction of online cash registers for various types of businesses (cash register equipment (CCT)). Deferments were granted several times to certain categories. According to changes to the legislation dated 06.06.19 (No. 129-FZ), the next deferment until 07.01.21 was received by individual entrepreneurs who do not have employees who:

- personally provide services;

- sell products they produce directly.

Remember: Bill No. 682709-7, which was adopted by the Federation Council and signed by the President - Federal Law 129-FZ dated 06/06/2019 states that for individual entrepreneurs without employees, cash registers are not needed until 07/01/2021.

Entrepreneurs who sell low-cost goods (ice cream, newspapers, soft drinks by the glass) or provide inexpensive services to the population (shoe repair, key making), as well as a number of other business transactions, are completely exempt from the obligation to use online cash registers.

Step-by-step instruction

So, you must understand that there is absolutely no need to keep full accounting records for an entrepreneur. There is no need to submit financial statements in the full sense of the word.

We offer you seven steps to a successful business.

Step 1. Calculate expected expenses and income.

Step 2. Select the appropriate tax regime.

Step 3. Find out what reporting forms need to be submitted to the Federal Tax Service under your tax payment system.

Step 4. If you are going to keep a record book. individual entrepreneur reporting on the simplified tax system without employees, then there is no need for this step. If you decide that you need hired workers, know that you need to submit reports on personnel composition to the Pension Fund, Social Insurance Fund, Federal Tax Service, and territorial statistics office.

Step 5: Take the time to study the tax calendar, as missing filing deadlines can result in hefty penalties.

Step 6. Decide whether you can do simplified accounting yourself or whether you should invite someone from the outside.

Be sure to save all documentation related to the business, such as contracts, bank statements, source documents.

How is the pension calculated?

Payment of annual insurance premiums is the basis for calculating pensions for entrepreneurs (individual entrepreneurs without employees) on a general basis, i.e. upon reaching retirement age and having insurance coverage. Currently, age and length of service increase annually until they reach the maximum values provided for by law.

Since individual entrepreneurs annually pay a minimum fixed contribution, they are usually accrued a pension at the subsistence level.

Expense of funds for personal needs of the entrepreneur

An individual entrepreneur can take money from the cash register for business needs, or maybe for his personal needs. Let's figure out whether this will be issued for reporting and how such operations are formalized.

Since all the money in the cash register belongs to the entrepreneur, there is no point in filing a report on the use of the taken amount to himself, since such a report will not have any control function. Therefore, if an individual entrepreneur takes money from the cash register, then it is advisable to draw up an expense order. In the future, if a purchase of goods or payment for services is made, the expense will be recorded in the book of income and expenses based on primary documents (sales receipts, invoices, etc.). If an individual entrepreneur decides to use the money for personal needs, then there will be no expense for business purposes. When registering a consumable of money for the personal needs of an individual entrepreneur, you can indicate in the description: “for personal needs.”

We note that clause 2 of the Bank of Russia directive “On making cash payments” dated October 7, 2013 No. 3073-U allows individual entrepreneurs to use cash from the cash register received from customers as payment for personal needs, not for doing business.

How to apply for sick leave for an individual entrepreneur without employees

Despite the fact that individual entrepreneurs pay fixed insurance premiums, they do not entitle them to sick pay. To obtain this opportunity, you need to voluntarily register, enter into an agreement and pay insurance premiums.

The amount of payments depends on the minimum wage. In 2021, the tariff is 2.9% of wages. Taking into account the fact that this year the minimum wage is 11,280 rubles (and next year it will be 12,130 rubles), i.e. for the year is 135,360 rubles, then 2.9% of it is 3,925.44 rubles.

Since sick pay is calculated taking into account the length of service, paying such an amount becomes profitable only if you have a work experience of more than 8 years, when sick leave is accrued at 100%.

What does the status of an individual entrepreneur give?

First of all, it allows you to legally conduct business, which is important for obtaining a stable income. After all, punishment for violations can have irreversible consequences, starting with huge fines that will negate all previous efforts to earn money, and ending with the loss of freedom for any kind of fraud.

Secondly, sleeping peacefully and knowing that in a number of issues you are protected by your newfound status is important for preserving life and health.

In order to obtain state registration as an individual entrepreneur, a resident of the Russian Federation must have:

- Original and copy of passport.

- A copy of your birth certificate.

- Application with a notarized signature of the future entrepreneur.

- A document confirming the place of registration.

- A receipt for payment of the state fee, which in 2019 is 800 rubles.

The prepared package of documents must be submitted to the tax office. You can visit the Federal Tax Service office in person, or you can send the collected papers electronically or by mail, after having them certified by a notary. This completes your steps to register an individual entrepreneur. After reviewing the documents, and according to the law, after 5 working days, you become an individual entrepreneur. What's next?

Decree for individual entrepreneurs without employees

Sick leave is accrued under similar conditions in connection with pregnancy and childbirth. But since the minimum amount of such sick leave is 51,918.9 rubles, it is more profitable to pay about 4 thousand rubles than to completely lose benefits.

The peculiarity is that when going on maternity leave in 2021, contributions for 2021 must be paid.

Also, to receive child care benefits, you need to pay a voluntary contribution to the Social Insurance Fund for the previous year. Considering that the monthly benefit amount is 4,512 rubles or 6,284.65 rubles, respectively, for the first and second child, the payment of contributions is fully justified.

Deadlines for submitting declarations and making payments

Tax reporting of individual entrepreneurs on the simplified tax system without employees is ensured as follows:

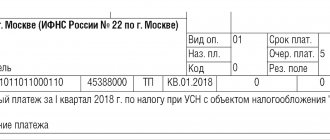

- By April 30 of the year following the reporting year, you must submit a tax return for the simplified tax system for the previous year and pay the remaining amount of the tax, minus advance payments made last year.

- By the 25th day of the first month of the new quarter, it is necessary to make a quarterly advance tax payment to the Federal Tax Service.

- By the first day of the month following the reporting quarter, amounts must be paid for pension and health insurance.

It is important to know that late advance payments entail the accrual of penalties. They are determined by calculation. A figure equal to 1/300 of the current rate for each day of delay from the total amount of arrears is applied.

It should be noted that such a simple system of payments and submission of declarations is valid only in the case of entrepreneurial activity on the simplified tax system without employees. Quarterly reporting of individual entrepreneurs under such taxation is not submitted.

An entrepreneur must take into account that failure to pay the final amount for the year on time can lead not only to penalties, but also to a fine.

How to draw up a staffing schedule and whether it is necessary to submit HR reports

If an individual entrepreneur works without employees, then he is exempt from drawing up a staffing table and maintaining personnel documents. Also, he does not need to submit reports in form 4-FSS to the Social Insurance Fund and SZV-M to the Pension Fund of the Russian Federation.

Is it necessary to take RSV-1 for an individual entrepreneur without employees? In this case, insurance premiums are not calculated. RSV is a report submitted by companies that pay remuneration only to hired employees.

Do individual entrepreneurs pass SZV-M if they work without employees? For IP, a zero SZV-M is formed. There is no need to hand it in. If you have hired personnel (even 1 person), you will already need to take the SZV-M. The very definition of a document carries the answer. SZV-M is a monthly personalized report to the Pension Fund about employees and other individuals.

Which simplified tax system should you prefer?

With the “STS Income” option, the tax is calculated at 6% of all financial income, including non-operating income. The amount of the advance payment, obligatory for payment after receiving the first revenue, is reflected in the declaration and in the financial report of the individual entrepreneur on the simplified tax system 6. An entrepreneur carries out his activities without employees or having full-time employees, he still has several advantages. If you have hired personnel, you can reduce your tax payment by the amount of transferred insurance premiums, payments for temporary disability and voluntary insurance. If there are no personnel, then contributions for oneself to the Pension Fund and the Federal Compulsory Medical Insurance Fund can reduce the tax.

Among the disadvantages of this option, it is worth noting that large expenses can result in losses.

When choosing “STS Income minus expenses”, the tax rate is 15% and is calculated based on the difference between revenue and expenses. It should be noted here that not all expenses can be included when determining the basis. They must be designated in Article 346.16 of the Tax Code and are necessary for the activities of the entrepreneur. The costs of such expenses should be confirmed by primary documents, they must take place in real activities, that is, the individual entrepreneur can present invoices, certificates of work performed and services provided. With such a system, there is no risk of going into the red.

A special feature is the mandatory control of the total amount of tax paid for the year. If it is less than 0.01 part of the total income, then you should pay additional tax up to 1%.

The disadvantage in this case is the fact that not all costs can be confirmed by two types of documents, some of which state payment, and others indicate receipt of goods or services. In this situation, these amounts cannot be included in expenses.

Tax and accounting reporting for individual entrepreneurs in 2021

Since the list of activities for PSN is limited, and it is impossible to hire more than 10 people, many businessmen combine a patent with other modes. In this case, the corresponding reports must also be submitted.

Unified agricultural tax

PSN is the simplest possible taxation system, designed only for entrepreneurs. Organizations cannot buy a patent, the cost of which immediately replaces all types of taxes and exempts them from filing reports.

Unused accountable funds returned to the cash desk do not have to be deposited into the current account. Therefore, they can be issued again for reporting or used for other needs (except for those for which it is necessary to specifically withdraw money from the account, for example, to pay for rent of real estate and

3.6. If the advance report is submitted for own funds spent in accordance with clause 1.7, then the employee simultaneously submits an application (see Appendix No. 5) addressed to the manager with a request to approve the advance report and reimburse the overexpenditure in the appropriate amount.

Submission of expense report

If an organization uses a corporate card for accountable needs, then in the instructions for accountables or in another internal document all related nuances should be additionally specified (for example, about the procedure for transferring the card and its return, about the employee’s obligation to keep the PIN code secret, about the absence restrictions on payments over 100 thousand rubles, etc.). Also remember that when using corporate cards, money is considered issued on account not at the moment of transfer of the card, but at the moment when the employee withdraws money from it or pays with it.

We recommend reading: Labor Protection Agreement Canceled

Important! It must be remembered that, according to regulatory documents, a person cannot be given a report if he has not fully accounted for the previous advance. Some tax inspectorates impose a fine for this during an audit.

If, after submitting a report, an employee has identified amounts of money that need to be returned to him, or vice versa, he needs to be compensated for what he spent excessively, then the details of the cash document are entered below.

Advance report 2021-2021: forms and samples of filling out the AO-1 form for free download in Excel, Word, PDF | CUBE

The accountant, after checking the correctness of the data and the validity of the expenses, fills out columns 7 and 8, where he enters the amount actually accepted for accounting, and in column 9 indicates the corresponding account. Subsequently, the generalized data from these columns is transferred to the front side of the document.

The employee is given money according to an outgoing cash order, and unspent amounts are accepted into the cash register according to an incoming cash order. They can be compiled on paper according to general rules. If the company has implemented an electronic document management system, cash orders can be prepared electronically. Then:

How to correctly fill out a zero calculation for insurance premiums

Calculation of insurance premiums is classified as a quarterly type of document. Usually we are talking about the following periods of time:

- Year.

- 9 months.

- Half year.

- 1st quarter. In this case, it is always necessary to transfer documents.

Until the 30th day of the month following the reporting period is the maximum period for which regulatory authorities must receive information. If the delivery day falls on a holiday or weekend, you can postpone the date until the next working day. It is acceptable to use paper and electronic media equally.

Reference! Information is provided during a personal visit or via email. Both options are acceptable. The responsible employee may suffer if at least part of the information is lost.

Previously, such calculations were based only on information regarding profits. Now we are talking about the income received. The main thing is not to confuse the concepts with each other. The following types of income can be classified as income, depending on the chosen tax regimes:

- The amount of profit based on the relevant document when the patent system is applied. All receipts are based on existing documentation.

- With UTII, the income previously imputed for the year is summed up. Indicators from lines 100 are added up for the last several reporting periods.

- Under the simplified tax system, the amount also includes the so-called non-operating profit. For example, when payments for rent of premises are received. Such indicators are prohibited from being reduced by the amount of costs. This also applies to cases where the appropriate regime is used. This scheme does not apply only in the case of social payments.

- For OSNO, everything that is included in standard documents is taken into account.

If there is a single founder, then he is also considered the general director. It is he who receives the salary along with other forms of remuneration. And in this case, he is listed in the compulsory insurance system. Data is still transmitted to Federal Tax Service employees, albeit in a minimal form.

Important! All lines in the document are filled in, but only one person will be the recipient of the payment.

When completing zero calculations, the following components must be filled out:

- Title page.

- The first section, where the company that pays the insurance premiums describes its data.

- Second application.

- Third section.

All lines indicate the number 0 when there are no numerical indicators.

After receiving the documents, the tax service will organize a desk audit. Explanations are requested if any errors or inaccuracies are identified. The response must be sent within a maximum of 5 working days.

If there is no response, a fine of up to 5 thousand rubles may be imposed. Repeated violations result in the fine increasing to 20 thousand rubles.

- report on your income by submitting a 3-NDFL declaration at the end of the year, and in a new form (). 3-NDFL for 2021, an individual entrepreneur must submit for OSN no later than 04/30/2020 ();

- submit a quarterly VAT return ().

In 2021, the VAT return must be submitted within the following deadlines:

Companies and entrepreneurs who have at least one individual with whom an employment contract or a civil employment agreement has been concluded are required to submit a calculation of insurance premiums for 2021 (zero), even if they did not accrue remuneration.

- during temporary suspension of activities;

- the already completed activities of the employer subject to further liquidation.

- seasonally occurring workload;

- the work of the recently registered future contribution payer has not yet actually begun;

Try it for free: Payers of mandatory insurance premiums, that is, policyholders, are companies and their separate divisions, individual entrepreneurs, heads of peasant farms:

The general tax system provides for the payment of personal income tax in the amount of 13% of the amount of income received, adjusted by the amount of confirmed expenses or by 20% of income if there is nothing to confirm expenses. Individual entrepreneurs also have the right to use other types of deductions provided for by law.

Fixed insurance premiums are paid by individual entrepreneurs in any case, regardless of the presence of activity. An entrepreneur can receive a deferment if in the reporting year he served in the army, cared for a child under 1.5 years old, an elderly person over 80 years old, or a disabled person.

If during the year the individual entrepreneur alternately hired workers, that is, after terminating the contract with one of the employees, the individual entrepreneur entered into an agreement with a new one, then in the SZV-Experience report the entrepreneur is obliged to reflect data on all employees with whom the individual entrepreneur had labor (civil) relations during a year.

Upon conclusion of the contract, Shumov acquired the obligation to maintain individual personalized records of the insured person, in connection with which Shumov submitted monthly SZV-M reports to the Pension Fund for the reporting periods of August and September in the following form: