Why monitor your net worth ratio?

The volume of net assets needs to be monitored due to the following circumstances:

- The volume of net assets is equal to the company's equity capital. Moreover, it is the equity capital that is an indicator of the company’s sustainability for regulatory authorities, credit institutions, as well as persons who plan to invest money in the company.

- Constant assessment of net assets allows you to reduce the risk of their size falling to a level less than the authorized capital. If this happens, the company may be forced to close. Moreover, the requirement that the value of the company’s net assets must not be lower than the amount of the authorized capital is established for companies of almost all organizational and legal forms. Even companies using a simplified taxation system are not exempt from this requirement.

Thus, for many companies, increasing net assets is a necessary operation (

Ways to increase a company's net assets

The value of net asset indicators allows you to assess the real state of affairs in the company. In accordance with Law No. 14-FZ of 02/08/1998, the company’s annual report must include information on net asset indicators. The information should contain the following:

- how the value of the indicator of interest changed over three years (the period could be shorter if the organization was registered less than three years ago);

- the reasons why there was a decrease in net assets to an amount less than the authorized capital;

- plans to correct the situation with net assets.

Important! Law 14-FZ obliges all companies to ensure that the company’s net assets are greater than the authorized capital. Otherwise, the company is obliged to increase them to the specified value. If a company neglects to do this, the company may face forced liquidation.

You can return this ratio when net assets exceed the amount of the authorized capital in one of the following ways:

- revaluation of assets (it is recommended to involve an independent valuation);

- reduction of the authorized capital (but to an amount not lower than the minimum - 10,000 rubles);

- increase in assets at the expense of the company’s founders.

How are net assets related to the company's capital?

Net assets are formed by current assets, which were purchased using own funds or using long-term loans.

With positive dynamics of this indicator over the last reporting periods:

- the company is attractive to investors;

- There is an advantage when applying for loans from banking institutions.

This indicates a high level of solvency and reliability of the enterprise’s financial system.

Low growth rates of working capital - the ratio of net assets and authorized capital with a clear predominance of the latter indicator - signals about the ineffectiveness of the financial strategy. This symptomatology is typical for enterprises in crisis. A negative net asset value means that the solvency of the company and the level of confidence in the company on the part of potential investors are critically low.

Also see “Negative Net Assets: Implications.”

When analyzing operating results, it is necessary to adhere to the rule that net assets must be greater than the authorized capital. Violation of this balance may be a consequence of attracting a large volume of short-term loans.

There are two ways to correct the situation:

- An increase in the value of assets.

- Reducing the amount of capital.

The law does not provide for penalties for violating the optimal balance between assets and the sources of their formation. But still, net assets and authorized capital must be regularly compared in order to promptly identify negative trends.

The manager is interested in quickly eliminating shortcomings in the financial sector in order to avoid undesirable consequences:

- decreased solvency;

- difficulties in attracting new investors;

- refusals of banking structures to provide loans on standard or preferential terms;

- lack of trust on the part of counterparties;

- increasing the risk of forced liquidation by regulatory government agencies.

The last option is possible if net assets are below the authorized capital over the last 2 years. The closure of a business will also be inevitable if it is impossible to revaluate assets or reduce the amount of capital.

Managers and founders must organize internal management accounting to identify negative trends in the enterprise’s economy. Significant assistance can be obtained from auditors who record in their report:

- change in the value of net assets and authorized capital, the ratio of these indicators;

- recommendations for leading a company out of crisis.

How to increase assets

To increase assets, the founders can provide their company with financial assistance, the direction of which will indicate the increase in assets. In addition, the founder can contribute additional property to the company.

Such methods will be most effective when the size of the authorized capital can no longer be reduced to the amount of net assets. That is, it is already minimal and it is no longer possible to reduce it any more.

If the founders decide to increase assets by contributing financial assistance, then they must correctly indicate the purpose for which these funds are contributed. For example, the purpose of the payment may indicate “increase in net assets by the founders.” Such an indication will allow you to judge the purpose of this operation, and will also help to avoid additional questions from regulatory authorities.

When increasing assets by adding property, the purpose of net assets is the ability to generate profit. In other words, net assets must be profitable. Despite the fact that this condition is not mandatory, the founder should evaluate all factors that influence this indicator. Of course, generating income is always accompanied by some costs, so any investment must be smart and justified. If you make mistakes in this area, this can lead to negative consequences, including losses for the company (

Analytics

| 11 September | If the guarantor refuses to pay under the bank guarantee, the beneficiary will have to prepare for court. Common reasons for refusals, arguments for the beneficiary and features of a bank guarantee issued to secure government contracts are in the article. Igor Chumachenko, Partner, Head of Real Estate Practice. Earth. Construction" Ksenia Druzhinina, Lawyer, Real Estate. Earth. Construction" |

| 11 September | Evidence is the “building material” for a legal position in a case, which must be properly prepared. Sometimes a simple copy of a document or a screenshot of a website is enough. In another case, you will have to try to provide evidence from a notary and confirm the authenticity of the copy when the opponent brought a different version of the document to court. About working with evidence - in the article. Semyon Lopatin, Lawyer, Arbitration PracticeElvira Khasanova, Junior Lawyer, Arbitration Practice |

| 11 September | When calculating procedural deadlines, weekends are not taken into account. An error in calculation, even by one day, can be fatal for a lawyer. Semyon Lopatin, Arbitration Lawyer |

| September 5 | Disputes about the procedure and conditions for registering a lease agreement for part of a property have been going on for several years, and with each new amendment and change in the current legislation in this area, disputes are renewed with renewed vigor. Igor Chumachenko, Partner, Head of Real Estate Practice. Earth. Construction" Ekaterina Ivanushkina, Senior Lawyer, Real Estate Practice. Earth. Construction" |

| September 5 | This article is devoted to certain issues of state registration of changes to a lease agreement, in relation to which the approaches of the courts have developed and changed over a fairly long period of time. Consideration of these approaches in their development will allow us to form a more accurate understanding of existing trends in judicial practice. Ekaterina Ivanushkina, Senior Lawyer, Real Estate Practice. Earth. Construction" |

| June 1st | On 25 May 2021, EU Regulation No. 2016/679 on the protection of individuals with regard to the processing of personal data and on the free circulation of such data (Regulation or GDPR) came into force as part of a major reform of EU personal data law. The regulation applies not only to EU residents, but also to foreign companies processing the data of European citizens. Violation of the provisions of the Regulation may result in a fine of up to EUR 20 million or 4% of global annual turnover for the financial year. Does the GDPR apply to your company? What are the main requirements of the GDPR? You will find answers to these questions in the diagrams* in this analytical review. Svetlana Zherdina, Lawyer, International Projects Group |

| April 19 | The commercial group VEGAS LEX has prepared an analytical infographic dedicated to determining the approximate size of a business entity’s share in the market in order to effectively manage antitrust risks. Ksenia Podguzova, Lawyer, Commercial Group |

| April 29 | As part of the judicial reform ongoing in the Russian Federation, the Code of Administrative Procedure was adopted on March 8, 2015. At the same time, the scope of regulation of the Code includes cases accepted for proceedings before the specified date. Alexander Sitnikov, Managing PartnerVictor Petrov, Head of Arbitration Practice |

| April 28 | In the current economic situation, many companies are interested in participating in both government procurement and procurement (44-FZ) carried out by individual legal entities (223-FZ), thereby ensuring a certain level of economic stability. However, the opportunities to participate in such procurements are significantly reduced if the company is included in one of the registers of unscrupulous suppliers, since most customers include in the procurement documentation a requirement that procurement participants should not be on the register. Alexander Sitnikov, Managing PartnerYulia Polyakova, Lawyer of the Commercial GroupKsenia Podguzova, Lawyer of the Commercial Group |

| April 23 | This publication is a reference book of typical commercial disputes in Russia that will be in demand on the market in 2015. This reference book on typical commercial disputes was prepared by VEGAS LEX lawyers who are directly involved in the implementation of relevant projects. Viktor Petrov, Head of Arbitration Practice |

Consequences of replenishing the authorized capital

An increase in the authorized capital for a company can be carried out by making contributions by participants . If we are talking about a joint stock company, then they issue an additional block of shares.

When replenishing the authorized capital of a subsidiary by transferring property to the co-founder organization, the consequences may be as follows:

- there is no VAT on the value of property transferred to replenish the authorized capital;

- VAT, which was accepted for deduction upon the initial purchase of property, will have to be restored;

- There is no need to issue an invoice when adding property to the authorized capital, and the invoice that was received when purchasing the transferred property is recorded in the sales book;

- restored VAT is also not taken into account;

- it is impossible to reduce the tax base of the founder due to the value of the property transferred to the authorized capital.

A legal entity that receives property as a contribution to the authorized capital must also assess the impact of this operation:

- the restored VAT on the transferred asset can be deducted in full;

- the document on the basis of which input VAT is taken into account - this is the act of acceptance and transfer of property indicated in the purchase book;

- if the company is on the simplified tax system, then it does not have the right to increase the value of property by the amount of VAT, and also to take it into account as expenses for tax accounting;

- the value of the property received will not increase the tax base, as will the restored VAT.

It should also be remembered that similar consequences may arise if other methods of increasing net assets are used.

Increase in net assets by founders: postings

Important! An increase in net assets by the founders will not in any way affect the size of the authorized capital.

The increase in assets at the expense of the founders is included in additional capital and is reflected in account 83 “Additional capital”. For this account, the source of the transfer of funds, as well as the purpose of this transfer, are taken into account. The posting when receiving funds from the founder will be as follows:

D 51 (08, 10) K 83

This posting is generated on the date the founders contribute funds.

How to calculate net assets

So, it is already clear what the net assets of an LLC are, all that remains is to understand how to calculate them. The mandatory calculation is carried out once a year, reflecting it in the annual financial statements on line 3600 of section 3 of the Statement of Changes in Capital. The presented calculation procedure is used by enterprises with such forms of ownership as:

- Joint stock companies (public, non-public).

- Limited liability companies.

- State and municipal unitary enterprises.

- Cooperatives (industrial and housing savings).

- Business partnerships.

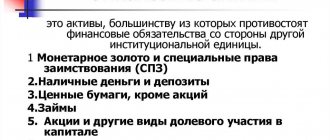

To calculate, the value of liabilities is subtracted from the value of assets:

NA = (VAO + OJSC – ZU – ZVA) – (DO + KO – DBP), where:

- NA – net assets;

- VAO – non-current assets of the company;

- OJSC – working capital of the company;

- ZU – debt of the founders to the company for filling shares in the management company;

- ZBA – debt incurred during the repurchase of own shares;

- DO – long-term liabilities;

- KO – short-term liabilities;

- DBP – future income (in the form of government assistance and gratuitous receipt of property).

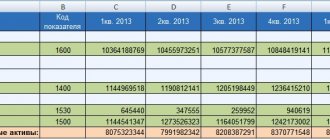

In addition, information contained in the company's balance sheet can be used. What are the company's net assets on the balance sheet? A different formula allows you to calculate the cost in this case:

NA = (line 1600 – ZU) – (line 1400 + line 1500 – DBP).

In the calculations, all the resources of the company are assessed without taking into account the receivables of the founders (participants, shareholders, owners, members) for contributions to the management company (authorized fund, mutual fund, share capital), for payment for shares.

Also, the calculations take into account all obligations, except for those future income that are recognized by the organization in connection with receiving government assistance or property free of charge. These earnings are considered the firm's equity and are therefore not included in the current liabilities section of the balance sheet.

Features of replenishing additional capital

Important! A donation between organizations cannot be formalized. The transfer of property may be recognized as a gift if there is no justification for such a transfer for the business. If organizations enter into an agreement on financial assistance, then it should clearly state what exactly the goals are pursued by both parties when making such a transaction.

All changes in the authorized capital of the company lead to the need to adjust the charter and record this in the Unified State Register of Legal Entities. And one of the advantages of replenishing additional capital is the absence of the need to make changes to the constituent documents. This method will also not affect the size of the founder’s contribution to the authorized capital. If we consider replenishing the additional capital of an LLC, then this is possible only at the expense of the founders, and for a JSC only direct financial support can be considered, and shareholders cannot contribute property.

The features of replenishing additional capital include the following:

- The amount of the contribution does not increase the taxable base for income tax if the founder who makes the contribution has a share in the authorized capital of 50% or more. Such property cannot be transferred to third parties for 1 year (251 Tax Code of the Russian Federation). If this requirement is violated, the value of the property will be recognized as income, which is subject to tax.

- In accordance with Article 251 of the Tax Code of the Russian Federation, property and funds contributed to increase net assets are not subject to taxation. If this is recorded in writing, then these assets should not be transferred to third parties for 1 year.

- The founder's contribution will be considered as a gratuitous transfer of property.