Start of business

An individual has the right to carry out cargo transportation after registering the organizational form of an individual entrepreneur. It is necessary to follow a certain sequence of actions:

- Registration of a TIN in the absence of a previously assigned number. The TIN is provided by the registration authority of the Federal Tax Service based on the person’s application. When opening an individual entrepreneur and there is no TIN, the number is assigned unconditionally, without application.

- Opening an individual entrepreneur. Registration is carried out on the basis of an application form P21001. The application is accompanied by a copy of the passport and TIN certificate (if available), and a payment document confirming payment of the state duty.

- Choosing the optimal taxation system. To use a special regime, an application for its use is submitted when opening an individual entrepreneur. A person who has not applied for a special regime uses OSNO.

Next, the individual entrepreneur needs to register (if desired) a seal, open a bank account, receive letters with statistics codes, registration numbers in funds.

Codes used for cargo transportation

The planned type of activity of the individual entrepreneur in cargo transportation must be designated by the Federal Tax Service. If you have a registered individual entrepreneur but the registration card does not contain the corresponding OKVED, changes must be made. An application form P24001 is submitted to the registration authority with the addition of a list of OKVED codes indicating the types of commercial activities used.

The correct code is important for licensing. To determine the code, information from the OKVED 2 reference book (OK 029-2014) is used. The previously approved classifier is no longer valid. The predominant type of activity is noted as the main code. When making changes, it is allowed to change the main view.

An individual entrepreneur planning to engage in cargo transportation must declare the conduct of activities in accordance with OKVED 49.41 or 49.42 used in 2021.

| OKVED code | Characteristic | Addition |

| 49.41 | Activities of road freight transport, including cargo transportation by specialized or non-specialized vehicles and rental of freight transport with a driver | Provides for the transportation of all types of cargo, including dangerous, special purpose, containers and others |

| 49.42 | Providing cargo transportation services | Includes relocation services provided to legal entities or individuals |

Calculation of the cost of a patent for cargo transportation for individual entrepreneurs in 2021

What indicators are needed to calculate the cost of a patent for PSN

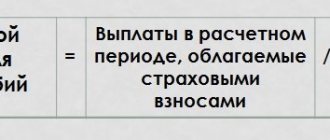

The patent taxation system involves the entrepreneur contributing a fixed amount of tax to the budget, which is determined based on:

- from the potential income of an individual entrepreneur for a particular type of activity (basic profitability);

- tax rate;

- duration of the patent.

The first indicator is always established in the regulations of the regions of the Russian Federation. In the general case, the tax rate established by the Tax Code of the Russian Federation is used. Its size is 6%. However, constituent entities of the Russian Federation have the right to reduce this rate down to zero for newly registered individual entrepreneurs (Article 346.50 of the Tax Code of the Russian Federation). The duration of a patent can range from 1 to 12 months.

If you are just planning to switch to PSN, read the terms of use of the special mode. A detailed review of the conditions for the transition to PSN and its further application was provided by ConsultantPlus experts. If you do not have access to the K+ system, get a trial online access for free.

In order to calculate the amount of tax according to PSN, you need:

- determine its annual cost using data on potential income and rate;

- divide the resulting figure by 12 and multiply the result by the number of months that corresponds to the duration of the patent.

Let's consider how the cost of a patent can be calculated if an individual entrepreneur intends to engage in cargo transportation.

Patent for cargo transportation: tax calculation

Let's agree that:

- The individual entrepreneur lives in Moscow;

- the patent is purchased for 3 months;

- The individual entrepreneur uses 4 machines, each of which has a lifting capacity of 2 tons.

ATTENTION! Tax authorities allow registration of a patent in one region, and transportation of goods in different regions of the Russian Federation. The main thing is that contracts with transportation customers be concluded in the region in which the patent was issued. Then the individual cargo carrier does not need to issue a patent in each of the regions where he transports goods. One patent is enough. See here for details.

First, we calculate the annual value of the patent. For this:

- We determine the potential income from cargo transportation.

The corresponding indicator is determined based on the standards present in line number 10 of the table in Art. 1 of the Moscow City Law “On the Patent System” dated October 31, 2012 No. 53.

The potential income of a metropolitan individual entrepreneur engaged in cargo transportation will be equal to 600,000 rubles. from 1 vehicle, if its carrying capacity is less than 3.5 tons. In total, the entrepreneur, as we agreed above, has 4 such vehicles. Therefore, his total potential income is RUB 2,400,000.

- We calculate the annual cost of a patent.

To do this, we use a rate of 6% - the one established by the Tax Code of the Russian Federation (clause 1 of Article 346.50), since Moscow legislation does not define other rates for PSN. It turns out that the annual cost of a patent for an individual entrepreneur with 4 machines with a lifting capacity of 2 tons will be 144,000 rubles.

Then we calculate the actual cost of the patent, taking into account the fact that it is purchased for 3 months. For this:

- divide 144,000 by 12, it turns out 12,000 rubles;

- multiply the result by 3, it turns out 36,000 rubles.

Contributions as part of PSN expenses

The payment burden of an individual entrepreneur on a PSN is not limited only to the costs of a patent. The entrepreneur will also need to pay fixed insurance contributions to the Pension Fund and the Federal Compulsory Compulsory Medical Insurance Fund.

In 2021, their value is 40,874 rubles if the entrepreneur works all year.

Read about fixed individual entrepreneur contributions here.

But we agreed that in our example, the individual entrepreneur is engaged in cargo transportation for 3 months. Therefore, he must pay contributions to the funds in proportion to the actual time of doing business, namely in the amount of 10,218 rubles. 50 kopecks (divide 40,874 rubles by 12, then multiply by 3).

Individual entrepreneurs have the right to deduct the amount of contributions from the amount of taxes due for payment on PSN. If an individual entrepreneur has hired employees, then he has the right to reduce the PSN, but no more than 50%. And if there are no employees, he has the right to reduce the entire amount of tax by the amount of contributions paid for himself. Therefore, the total payment burden of the capital’s individual entrepreneurs for 3 months of cargo transportation on the PSN will be 46,218 rubles. 50 kopecks

If an individual entrepreneur on the PSN, which is engaged in cargo transportation, has hired employees, then he is obliged to calculate and pay insurance premiums for the amount of the employees’ wages. Rates for individual entrepreneurs on PSN in 2021 are standard:

- 22% for pension insurance within the minimum wage and 10% for wages above;

- 5.1% for medical insurance up to RUB 12,792. and 5% on everything above;

- 2.1% for social insurance for the amount of earnings within the minimum wage;

- from 0.2% to 8% for insurance of workers against accidents at work.

The rate of “unfortunate” contributions is determined based on the class of professional risk by type of activity. Cargo transportation corresponds to the 5th risk class, the tariff in the Social Insurance Fund is set at 0.7% (order of the Ministry of Labor and Social Protection of the Russian Federation dated December 30, 2016 No. 851n, Article 1 of the Law “On Insurance Tariffs” dated December 22, 2005 No. 179-FZ).

In connection with the spread of coronavirus infection, the government has approved a number of measures to support business, including reducing the insurance premium rate to 15%. These rates remained forever. ConsultantPlus experts explained the procedure for applying rates. Get trial access to the K+ system and study the material for free.

Results

To calculate the cost of a patent for any type of individual entrepreneur’s activity, you need to know the amount of potential income established by the regional regulatory legal act for the corresponding type of activity, the size of the rate, and the validity period of the patent. In addition to the costs of paying tax under PSN, an entrepreneur must also transfer fixed contributions to extra-budgetary funds for the months during which he is engaged in business.

You can learn more about PSN and legislative regulation from the “PSN” section.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Waybill required when operating transport

Individual entrepreneur services for cargo transportation are accompanied by the issuance of documents, the main of which is a waybill. The document is issued to the driver for a period of 1 day to 1 month. Based on the data from the waybills, the consumption of fuel and other types of fuel and lubricants, and indicators of driver remuneration are calculated. The document is also required in the case of transport management by the individual entrepreneur himself. In accounting, unified forms 4-C, 4-P, PG-1 are traditionally used.

Based on the provisions of Order of the Ministry of Transport dated September 18, 2008 No. 152, the enterprise has the right to use independently developed forms of waybills. An individual entrepreneur can take a unified form as a model, modifying the form to suit the conditions of business. The main condition for using your own forms is the presence of the required details.

| Mandatory information | Data Composition | Description |

| Waybill details | Document name and number | The sheets are numbered in accordance with the accounting log |

| Validity | The start and end dates of the sheet validity period are indicated | In sheets issued for 1 day, indicate 1 date |

| Owner information | The individual entrepreneur indicates the basic details of the enterprise | The data includes full name, registration address, OGRNIP number, telephone |

| Vehicle information | Enter the type and registration number of the vehicle; when using a trailer, additional data | In addition to information about the vehicle, it is necessary to indicate the odometer readings, dates and times of departure (arrival) and, if necessary, pre-trip control |

| Driver information | Provide full name information | Indicate the time of pre-trip and post-trip medical examinations |

The waybill information can be supplemented with information about the specifics of cargo transportation and customers. The document refers to primary accounting forms and must be stored in the individual entrepreneur for 5 years.

We are an individual entrepreneur using the simplified tax system of 6% and provide dispatch services to drivers for cargo transportation, i.e.

They can be included in expenses when calculating the single tax if they are actually paid and were not previously taken into account when applying other taxation systems.

2. When determining the object of taxation, taxpayers reduce the income they receive by the following expenses:

1) expenses for the acquisition, construction and production of fixed assets, as well as for the completion, retrofitting, reconstruction, modernization and technical re-equipment of fixed assets (taking into account the provisions of paragraph 4 and paragraph six of subparagraph 2 of paragraph 5 of this article);

(as amended by Federal Laws dated March 13, 2006 N 39-FZ, dated May 17, 2007 N 85-FZ)

2) expenses for the acquisition of intangible assets, the creation of intangible assets by the taxpayer himself (taking into account the provisions of paragraph 4 and paragraph six of subparagraph 2 of paragraph 5 of this article);

(Clause 2 as amended by Federal Law dated March 13, 2006 N 39-FZ)

3) expenses for repairs of fixed assets (including leased ones);

4) rental (including leasing) payments for rented (including leased) property;

5) material costs, including costs for the purchase of seeds, seedlings, seedlings and other planting material, fertilizers, feed, medicines for veterinary use, biological products and plant protection products;

(as amended by Federal Laws dated March 13, 2006 N 39-FZ, dated November 25, 2013 N 317-FZ)

6) expenses for wages, compensation, temporary disability benefits in accordance with the legislation of the Russian Federation;

(as amended by Federal Law No. 155-FZ of July 22, 2008)

6.1) expenses for ensuring safety measures provided for by regulatory legal acts of the Russian Federation, and expenses associated with the maintenance of premises and equipment of health centers located directly on the territory of the organization;

(Clause 6.1 introduced by Federal Law dated July 22, 2008 N 155-FZ)

7) expenses for compulsory and voluntary insurance, which include insurance premiums for all types of compulsory insurance, including insurance contributions for compulsory pension insurance, compulsory social insurance in case of temporary disability and in connection with maternity, compulsory medical insurance, compulsory social insurance from accidents at work and occupational diseases, as well as the following types of voluntary insurance:

(as amended by Federal Law dated July 24, 2009 N 213-FZ)

voluntary insurance of vehicles (including rented ones);

voluntary cargo insurance;

voluntary insurance of fixed assets for production purposes (including leased), intangible assets, objects of unfinished capital construction (including leased);

voluntary insurance of risks associated with construction and installation work;

voluntary insurance of inventory;

voluntary insurance of crops and animals;

voluntary insurance of other property used by the taxpayer in carrying out activities aimed at generating income;

voluntary insurance of liability for causing harm, if such insurance is a condition for the taxpayer to carry out activities in accordance with the international obligations of the Russian Federation or generally accepted international requirements;

(Clause 7 as amended by Federal Law dated March 13, 2006 N 39-FZ)

amounts of value added tax on goods (work, services) acquired and paid for by the taxpayer, the costs of acquisition (payment) of which are subject to inclusion in expenses in accordance with this article;

amounts of value added tax on goods (work, services) acquired and paid for by the taxpayer, the costs of acquisition (payment) of which are subject to inclusion in expenses in accordance with this article;

(Clause 8 as amended by Federal Law dated March 13, 2006 N 39-FZ)

9) the amount of interest paid for the provision of funds (credits, borrowings) for use, as well as expenses associated with payment for services provided by credit institutions, including those associated with the sale of foreign currency when collecting taxes, fees, penalties and fines in accordance with the procedure provided for in Article 46 of this Code;

(as amended by Federal Law dated July 27, 2006 N 137-FZ)

10) expenses for ensuring fire safety in accordance with the legislation of the Russian Federation, expenses for services for the protection of property, maintenance of fire alarm systems, expenses for the purchase of fire protection services and other security services;

11) amounts of customs duties paid when importing (exporting) goods into the territory of the Russian Federation and other territories under its jurisdiction, and not subject to refund to taxpayers in accordance with the customs legislation of the Customs Union and the legislation of the Russian Federation on customs affairs;

(as amended by Federal Laws dated November 27, 2010 N 306-FZ, dated December 28, 2010 N 395-FZ)

12) expenses for the maintenance of official transport, as well as expenses for compensation for the use of personal cars and motorcycles for official trips within the limits established by the Government of the Russian Federation;

13) business travel expenses, in particular for:

travel of the employee to the place of business trip and back to the place of permanent work;

rental of residential premises. This item of expenses also covers the employee's expenses for additional services provided in hotels (with the exception of expenses for service in bars and restaurants, expenses for room service, expenses for the use of recreational and health facilities);

daily allowance or field allowance;

(as amended by Federal Law No. 155-FZ of July 22, 2008)

registration and issuance of visas, passports, vouchers, invitations and other similar documents;

consular, airfield fees, fees for the right of entry, passage, transit of automobile and other transport, for the use of sea canals, other similar structures and other similar payments and fees;

14) fee to the notary for notarization of documents. Moreover, such expenses are accepted within the limits of tariffs approved in accordance with the established procedure;

15) expenses for accounting, auditing and legal services;

(Clause 15 as amended by Federal Law dated March 13, 2006 N 39-FZ)

16) expenses for the publication of accounting (financial) statements, as well as for publication and other disclosure of other information, if the legislation of the Russian Federation imposes an obligation on the taxpayer to carry out such publication (disclosure);

(as amended by Federal Law dated June 25, 2012 N 94-FZ)

17) expenses for office supplies;

18) expenses for postal, telephone, telegraph and other similar services, expenses for payment for communication services;

19) expenses associated with the acquisition of the right to use computer programs and databases under agreements with the copyright holder (under license agreements). These costs also include costs for updating computer programs and databases;

20) expenses for advertising manufactured (purchased) and (or) sold goods (works, services), trademark and service mark;

21) expenses for the preparation and development of new production facilities, workshops and units;

22) expenses for food of workers engaged in agricultural work;

22.1) expenses for food rations for crews of sea and river vessels;

(Clause 22.1 introduced by Federal Law dated July 22, 2008 N 155-FZ, as amended by Federal Law dated July 23, 2013 N 248-FZ)

23) the amount of taxes and fees paid in accordance with the legislation on taxes and fees, with the exception of the amount of the unified agricultural tax paid in accordance with this chapter;

(Clause 23 as amended by Federal Law No. 94-FZ dated June 25, 2012)

24) expenses for payment of the cost of goods purchased for further sale (reduced by the amount of expenses specified in subclause 8 of this paragraph), including expenses associated with the acquisition and sale of these goods, including costs of storage, maintenance and transportation;

(as amended by Federal Law dated March 13, 2006 N 39-FZ)

25) expenses for information and advisory services;

26) expenses for training and retraining of personnel on the taxpayer’s staff, on a contractual basis in the manner prescribed by paragraph 3 of Article 264 of this Code;

(Clause 26 as amended by Federal Law dated March 13, 2006 N 39-FZ)

27) court costs and arbitration fees;

28) expenses in the form of fines, penalties and (or) other sanctions paid on the basis of a court decision that has entered into legal force for violation of contractual or debt obligations, as well as expenses for compensation for damage caused;

(Clause 28 as amended by Federal Law No. 39-FZ dated March 13, 2006)

29) expenses for training specialists for taxpayers in educational institutions of secondary vocational and higher vocational education. The specified expenses are taken into account for tax purposes, provided that training agreements (contracts) have been concluded with individuals studying in the specified educational institutions, providing for their work with the taxpayer for at least three years in their specialty after graduation from the relevant educational institution;

(Clause 29 introduced by Federal Law dated June 29, 2005 N 68-FZ)

30) became invalid on January 1, 2013. — Federal Law of June 25, 2012 N 94-FZ;

31) expenses for the acquisition of property rights to land plots, including expenses for the acquisition of the right to conclude a lease agreement for land plots, subject to the conclusion of the specified lease agreement, including:

for land plots from agricultural lands;

on land plots that are in state or municipal ownership and on which buildings, structures, structures used for agricultural production are located;

(Clause 31 as amended by Federal Law No. 155-FZ of July 22, 2008)

32) expenses for the acquisition of young livestock for the subsequent formation of the main herd, productive livestock, young poultry and fish fry;

(Clause 32 introduced by Federal Law dated March 13, 2006 N 39-FZ)

33) expenses for the maintenance of rotational and temporary camps associated with agricultural production of grazing livestock;

(Clause 33 introduced by Federal Law dated March 13, 2006 N 39-FZ)

34) expenses for payment of commissions, agency fees and fees under agency agreements;

(Clause 34 introduced by Federal Law dated March 13, 2006 N 39-FZ)

35) costs for product certification;

(Clause 35 introduced by Federal Law dated March 13, 2006 N 39-FZ)

36) periodic (current) payments for the use of rights to the results of intellectual activity and means of individualization (in particular, rights arising from patents for inventions, industrial designs and other types of intellectual property);

(Clause 36 introduced by Federal Law dated March 13, 2006 N 39-FZ)

37) expenses for carrying out (in cases established by the legislation of the Russian Federation) a mandatory assessment in order to monitor the correctness of payment of taxes in the event of a dispute regarding the calculation of the tax base, as well as expenses for conducting an assessment of property when determining its market value for the purpose of collateral;

(Clause 37 introduced by Federal Law dated March 13, 2006 N 39-FZ)

38) fee for providing information about registered rights;

(Clause 38 introduced by Federal Law dated March 13, 2006 N 39-FZ)

39) costs of paying for the services of specialized organizations for the production of documents for cadastral and technical registration (inventory) of real estate (including title documents for land plots and documents on land surveying);

(Clause 39 introduced by Federal Law dated March 13, 2006 N 39-FZ)

40) expenses for paying for the services of specialized organizations for conducting examinations, surveys, issuing opinions and providing other documents, the presence of which is mandatory for obtaining a license (permit) to carry out a specific type of activity;

(Clause 40 introduced by Federal Law dated March 13, 2006 N 39-FZ)

41) expenses associated with participation in tenders (competitions, auctions) held during the implementation of orders for the supply of products specified in paragraph 3 of Article 346.2 of this Code;

(Clause 41 as amended by Federal Law No. 155-FZ of July 22, 2008)

42) expenses in the form of losses from mortality and forced slaughter of poultry and animals within the limits of standards approved by the Government of the Russian Federation, with the exception of cases of natural disasters, fires, accidents, epizootics and other emergency situations;

(Clause 42 as amended by Federal Law dated November 25, 2009 N 275-FZ)

43) amounts of port dues, costs for pilot services and other similar expenses;

(Clause 43 introduced by Federal Law dated July 22, 2008 N 155-FZ)

44) expenses in the form of losses from natural disasters, fires, accidents, epizootics and other emergency situations, including costs associated with the prevention and liquidation of their consequences.

Other mandatory documents for cargo transportation

In addition to the waybill, the driver must have:

- Driver's license.

- Vehicle passport.

- Insurance policy on compulsory motor vehicle and other voluntary liability.

- Employment agreement for an individual entrepreneur as a delivery driver. It is acceptable to present a copy of the agreement. In the absence of an agreement, you must have a power of attorney for the right to drive transport.

- Consignment note (Bill of Lading), if goods are transported by an individual entrepreneur or a legal entity. The document reflects the details of the parties, places of dispatch and receipt of cargo, characteristics of the transported goods, weight and other additional data. Can serve as the basis for the receipt of cargo.

- Waybill (TN). Confirms the eligibility of cargo transportation, contains only the transport section. The document contains special notes from the shipper.

- Instruction to the forwarder establishing a list of services.

- Forwarding, warehouse receipt, power of attorney for cargo.

- Permission to transport cargo with special characteristics - oversized, dangerous goods.

The driver's kit includes other accompanying documents, determined by the type of cargo being transported. When transporting products, you need a sanitary passport, animals - a veterinary passport, alcohol-containing products - a certificate of technical specification and other documents.

Forms of taxation for cargo transportation

When carrying out cargo transportation, an individual entrepreneur has the right to choose one of the permitted types of taxation. Applicable:

- Generally installed system. It has the most extensive document flow and is used when it is necessary to present invoices to the customer with VAT included. The basic personal income tax rate is 13%. There are no restrictions on the number of transport units or the number of employees.

- Simplified system. Allows you to choose one of 2 tax schemes, differing in rates and the need to account for expenses. A rate of 6 or 15% applies. There are restrictions on revenue (150 million rubles) and the number of employees (100 people). The limitation on the value of property does not apply to individual entrepreneurs due to its recognition as the property of an individual.

- UTII. A convenient mode for cargo transportation that does not require maintaining a large number of primary documentation. The regime is characterized by imputed income, the amount of which depends on the number of vehicles operated. The downside of the system is the need to pay tax from the moment of registration as a UTII payer until the day of deregistration. It has restrictions on the number of vehicles (20 transport units) and employees (100 people).

- PSN. Applicable only to individual entrepreneurs through the acquisition of a patent. The payment amount at a rate of 6% depends on the estimated income established in the region. The entrepreneur independently chooses the validity period of the patent for a period of 1 to 12 months throughout the year. It has a maximum limit on revenue (60 million rubles) and number (15 people). The number of vehicles is not limited. The activities are carried out in the territory of the patent registration region.

The UTII and PSN systems are used if regimes for the selected type of activity are applied in the region. Starting from 2021, the special UTII regime will be abolished.

According to the Minister of Finance of the Russian Federation, the UTII regime turned out to be not the most effective in terms of work.

Minister of Finance of the Russian Federation A.G. Siluanov

The moment of transition to the planned taxation system is determined by the regime chosen by the individual entrepreneur. The transition to the simplified tax system is carried out when opening an individual entrepreneur or from the beginning of the calendar year; the use of UTII is allowed from any date.

OSNO is applied by default; the mode can be combined for certain types of activities with UTII, PSN.

Selecting a tax regime

There are several modes available for individual entrepreneurs. The default system is the main system, but it is very complex and in most cases unprofitable. Therefore, entrepreneurs usually choose one of the special modes. Each has its own rules for calculating the tax base and the procedure for accounting for contributions paid for insurance. Below are the features that need to be taken into account when calculating.

Free tax consultation

USN Income minus expenses

The conditions for applying the simplified tax system are as follows:

- no more than 100 employees;

- annual income - no more than 150 million rubles;

- the residual value of the property is also no more than 150 million rubles.

The tax base for such an object of taxation is equal to the difference between revenue and costs: 7,800,000 - 6,600,000 = 1,200,000 rubles. Insurance premiums are included as expenses.

USN Income

The conditions for using this mode are the same as described above. The tax base is the entire income of the individual entrepreneur; expenses are not taken into account. From the tax amount, you can deduct insurance premiums that the entrepreneur paid for himself and for the employee. However, the tax can be reduced by no more than 50%. In the example, the deduction amount will be: 40,874 + 75,000 + 120,000 = 235,874 rubles.

Patent (PSN)

The PSN tax is equal to the cost of the patent and amounts to 6% of the potential income of an individual entrepreneur for this type of activity in a specific territory. The value of this income is established by the municipal administration. To determine the amount of the fee for a patent, the Federal Tax Service has a special service.

Note!

From 2021, entrepreneurs on PSN can reduce the tax (patent cost) by the amount of insurance premiums paid for themselves and their employees. The rules are the same as for individual entrepreneurs on the simplified tax system with the object “income”.

For the individual entrepreneur from the example, for the entire 2021, a patent for cargo transportation will cost 69,240 rubles before deduction of contributions. Since the individual entrepreneur has employees, the cost of the patent can be reduced by 50% due to insurance contributions. Therefore, the payment will be 34,620 rubles.

In addition to the described regimes, there is another one - NPA, which stands for professional income tax. But it has a number of restrictions, for example, the maximum income is no more than 2.4 million rubles, a ban on hiring employees. Therefore, it is not suitable for the individual entrepreneur from our example.

Sanctions imposed for violation of transportation requirements

Articles 12.3 and 12.31.1 of the Code of Administrative Offenses provide for sanctions imposed on individual entrepreneurs in the form of an administrative fine.

Important! If violations are detected in an individual entrepreneur, subject to the sanctions of Art. 12.31.1 of the Administrative Code, the amount of the fine is the same as the amounts imposed on legal entities.

| Article of the Administrative Code | Violation | Fine amount |

| Clause 1 Art. 12.3 | The driver does not have documents to drive the vehicle | 500 rubles (warning possible) |

| Clause 2 art. 12.3 | The driver does not have a waybill or TTN documents | 500 rubles (or warning) |

| Clause 2.1 art. 12.3 | Transportation of goods without the right to carry out activities | 5,000 rubles per driver |

| Clause 2 art. 12.31.1 | Transportation of goods by motor transport without medical examinations of the driver | For citizens in the amount of 3,000 rubles, for an official - 5,000 rubles, individual entrepreneurs - 30,000 rubles |

| Clause 4 art. 12.31.1 | Transportation of goods in violation of safety conditions | For a driver - 2,500 rubles, for an official - 20,000 rubles, individual entrepreneur - 100,000 rubles |

Errors made in accounting for cargo transportation

Mistake No. 1. When accounting for individual entrepreneurs in cargo transportation, expense accounting is often required. Documented and economically justified expenses are used when calculating the tax base. It is a mistaken belief that fuel costs can be written off based on actual expenses. When writing off, it is necessary to take into account expense norms and the actual mileage of the vehicle. If fuel consumption exceeds the technical documentation norm, it is necessary to take into account the test mileage data.

Mistake No. 2. Individual entrepreneurs using a common system often do not have contracts with companies that require service provider VAT. continues to allocate VAT. Wrong position. An individual entrepreneur with a small transportation turnover can claim exemption from VAT.

Do I need an individual entrepreneur's cash register for cargo transportation: deferment until 2021

The first stage of the transition to cash register with new functionality affected the following cargo carrier entrepreneurs:

- Those who previously used cash desks with EKLZ. In this case, the taxation system does not matter.

- Those who worked with other individual entrepreneurs, enterprises and applied the general tax regime or simplified tax system. An exception was made for businessmen who accept payment for their services by bank transfer - through a bank account and electronic means of payment (except for online systems such as Yandex.Money, Qiwi).

The above business owners installed devices that transmit information to the Federal Tax Service via the Internet online even before the start of the 2nd half of 2021.

Below we will look at which individual entrepreneurs engaged in cargo transportation do not need a cash register until July 2021.

UTII

According to Article 7 of regulatory act No. 290-FZ, the period for purchasing new cash registers has been extended until the 2nd half of 2021 for businessmen who pay a single tax to the budget and provide cargo transportation services (clause 1, clause 7.1).

A mandatory deferment condition for this category of entrepreneurs is the ownership or long-term lease of no more than 20 vehicles engaged in cargo transportation.

- Rent an online cash register MTS cash desk 5

56 reviews

1 700 ₽

1700

https://online-kassa.ru/kupit/arenda-onlajn-kassy-mts-kassa-5/

OrderMore detailsIn stock

- Rent an online cash register MTS Kassa 7

43 reviews

1 700 ₽

1700

https://online-kassa.ru/kupit/arenda-onlajn-kassy-mts-kassa-7/

OrderMore detailsIn stock

PSN

Article 7 290-FZ states that cargo carriers who have chosen a patent to conduct business activities will begin working at online cash desks from July 1, 2021 (clause 3, clause 7.1).

For this category, the legislation does not provide any restrictions on the number of equipment involved.

Subscribe to our channel in Yandex Zen - Online Cashier! Be the first to receive the hottest news and life hacks!

OSNO and simplified system

Entrepreneurs under the general tax regime and a simplified system who provide cargo transportation services to the population can conduct business without cash registers with the function of online information exchange with the Federal Tax Service until the 2nd quarter of 2019. This norm is spelled out in paragraph 8 of Article 7 of the 290-FZ.

1. Ask our specialist a question at the end of the article. 2. Get detailed advice and a full description of the nuances! 3. Or find a ready-made answer in the comments of our readers.

Combination of tax regimes

If a cargo carrier combines several taxation systems, then he buys an online cash register within the time limits specified in the law for each of the modes.

For example, for OSNO, an entrepreneur installed a device in 2017, and for services that are subject to a single tax, he will begin punching checks at the cash register from July 2021. The individual entrepreneur maintains separate records for each system. But you can use one cash register for both tax regimes.

We'll tell you which cash register from our catalog is suitable for your business.

Leave a request and receive a consultation within 5 minutes.

Answers to common questions

Question No. 1. Does an individual entrepreneur need to obtain a license to provide cargo transportation services?

A license issued by the Ministry of Transport and Communications is required when transporting goods outside the country or especially dangerous goods. In other cases, transportation is carried out without additional permission.

Question No. 2. Is it necessary to indicate OKVED for freight transportation if an individual entrepreneur plans to provide freight transport for rent?

Renting a vehicle from a lessor is not considered cargo transportation.