Hi all!

Today the topic of our conversation will be of a slightly accounting nature: we will talk about the property structure of the enterprise. Surely many people know that assets are premises, factories, ships and everything that a company has. However, not everyone is aware of how they are reflected in the balance sheet. How can they be assessed?

How do they differ from liabilities and how do they relate to each other? What is the difference between current and non-current? And this is only a small part of the current issues, which I will try to analyze and explain simply and clearly, as they often say, “for dummies.”

What are assets and liabilities

Assets are property owned by a company at the reporting date. Using this property, the company carries out its activities and tries to make a profit (the left side of the balance sheet).

Liabilities are the economic means through which the company's assets are formed (the right side of the balance sheet).

Difference between liabilities and assets

To explain the difference and establish the correct cause-and-effect relationship, I will give a small example.

A company buys a machine for its activities for 100 rubles. Now the machine is the property of the company and is reflected on the left side of the balance sheet with a valuation of 100 rubles. At the same time, in order to buy equipment, the company took out a loan of 100 rubles. This is a liability and is reflected in the corresponding place on the right side of the balance sheet.

Are own shares an asset or a liability?

To answer this question, you should use the following accounting logic.

The issue of shares or other securities is the raising of funds with which it is possible to purchase property involved in the activities of the organization. This means that this is a source of funds; accordingly, own shares are a liability and are reflected as the company’s capital on the right side of the balance sheet.

Interaction of assets and liabilities

Liabilities are the sources from which the company’s property is formed. Therefore, in accounting there is an absolute rule that states that “LIABILITIES = ASSETS.”

Let me give you a couple more easy examples.

The company has funds contributed by its founders, i.e. capital (this is a liability) in the amount of 100 rubles. She buys a building (asset) worth 50 rubles with them. In this case, the balance will look like this: Liabilities = 100 rubles. Assets = 50 rub. Building and 50 rubles. - These are available funds.

Next, the company decided to purchase goods worth 100 rubles, but it did not have enough money, so it took out a loan of 50 rubles. The balance has changed: now the organization’s liabilities include 100 rubles. equity and 50 borrowed funds.

On the left side of the company’s balance sheet, a building purchased for 50 rubles remained, and goods worth 100 rubles appeared. The company has no free cash left. But the balance has not changed: 150 rubles. = 150 rub.

Assets and liabilities in financial statements

All information about the structure of the company is contained in such a type of reporting as the balance sheet. It is not filled out in free form, but has certain rules and structure.

Assets include two forms:

- non-current;

- negotiable.

Liabilities are divided into:

- equity;

- Short-term liabilities;

- long term duties.

Assets and liabilities according to Kiyosaki

Robert Kiyosaki is the bestselling author of Rich Dad Poor Dad. He offers his own system of grading property elements. His books have sold millions of copies, and his lectures attract (or have attracted) huge numbers of listeners.

Therefore, people often come across this information and begin to think that in accounting and when reading reports they can use the method he proposed. However, it is not.

Its definition rules do not apply to accounting; their meaning is as follows:

- an asset is anything that generates income;

- a liability is something that requires investment.

And the main idea is to increase the number of the former and reduce the number of the latter.

Structure of bank liabilities

The bank's liabilities include 2 groups - equity capital (authorized, additional, reserve) and attracted funds (loans, liabilities, deposits of individuals). Moreover, the first group usually makes up about 10%. This means that banks carry out their activities using borrowed funds.

Liabilities are formed as a result of passive operations, i.e. attracting borrowed or own funds. Such operations include:

- issue of securities;

- attracting deposits;

- loans;

- deductions from profits;

Bank liabilities include own funds, because they are also used to form the active part of the balance sheet.

Kinds

The organization's resources are divided into two large groups: non-current and current. The main factors when assigning property to a certain group are the following:

- Duration of use or sale. For non-current assets, the useful life generally exceeds 12 months. For negotiables the situation is the opposite and is limited to a circulation period of 12 months.

- Liquidity. This is a measure of how quickly a property can be converted into cash. The industrial building has low liquidity and is classified as a non-current asset. Money has the highest liquidity and is strictly classified as current assets.

Liabilities are divided into three large groups:

- Equity. For example, own funds invested by the founders or money raised from the issue of shares, etc.

- Long term duties. The repayment period is more than 1 year.

- Short term. Repayment period is less than 1 year.

Types of assets

When compiling an official or household balance sheet, assets should include such areas that are directly related to the liabilities of the balance sheet :

- bank deposit;

- income from online projects;

- rent received for the use of real estate, or, for example, a car;

- stock;

- mutual funds;

- bonds;

- lending money;

- acquisition of assets, the liquidity of which only increases every year.

Among the latter are investments in rarities, stamps, collections, metals (gold), platinum. By the way, for the first time in 16 years, the price of platinum exceeded that of gold.

I highly recommend using multiple sources of assets, a rule I detail in my investing tips for beginners.

Asset classification

Considering what assets and liabilities are in the accounting literature, one can find several approaches to the main classifications. I offer the most popular of them , taking into account the size of liquidity :

- the most liquid (deposits);

- quickly sold (selling goods at a premium);

- slowly realized (dividends from shares);

- difficult to sell (antiques).

In the article on trust management, I spoke in detail about how specialists will help form and distribute categories of expenses and investments among themselves. The nuances are in the finished material. Taking into account the period of circulation, assets can be current or non-current. This is important when considering the assets and liabilities of different organizations. The first include money, materials, products, goods. The second includes patents, certificates, know-how, and developments. I would also like to point out that there are tangible, intangible and financial assets. And if we take into account the nature of ownership, then assets can be leased, owned or free of charge. The latter, of course, are not very common.

What are the net assets of an enterprise

In simple terms, NAV (from English netassets) is the difference between the total assets and liabilities of the company. Otherwise, it is property that is covered within the company's equity.

Alarm bell if this value is in the negative zone. Then the value of debts exceeds the sum of all assets.

CA and legislation

By law, if this indicator falls below a certain level, the company does not have the right to pay dividends for the reporting period.

The minimum acceptable threshold is determined as the size of the authorized capital and reserve fund. Preferred shares are also accounted for as the difference between their par value and liquidation value.

Calculation formula

The formula for calculating the NA is as follows:

Types of assets and what they include

It's time to look a little deeper at the structure of the balance sheet.

Non-current include the following subsections on the balance sheet:

- intangible assets;

- Finnish investments (more than a year);

- fixed assets;

- deferred tax liabilities.

The negotiables form the following sections:

- stocks;

- receivable;

- Finnish investments (less than a year);

- cash and equivalents.

This is an incomplete list; it may still be supplemented by some articles depending on the specifics of the activity, etc.

How are the assets and liabilities of the balance sheet formed?

Here I will briefly outline the main relationships when forming a balance:

- Assets = Liabilities = (equity + liabilities).

- Assets – liabilities = equity.

These accounting rules must always be followed.

What are active and passive accounting accounts?

1 min

Accounting should be used in every small firm or large company. The quality of work of the entire organization depends on the effectiveness of the accountant’s actions. The accounting characteristic involves the use of multiple accounts and entries during budgeting activities. It is quite important to know the main accounts and which of them should belong to and be included in the active and passive accounts of accounting. The layout, structure and list of accounts can be easily understood, however, they are difficult to remember. It will take a good specialist some time to identify and remember the most used types.

What is an active view?

Active accounts are those types that count the company's assets. They have a closing and opening balance in the form of a mandatory debit. According to debit (Dt), an increase in the asset is indicated, and according to credit (Kt), a decrease is indicated. The presented rule must be a prerequisite for correctness, otherwise the accounting contains an error.

Examples of division

The main programs for keeping records in electronic form have a limitation that will not allow you to write off more than what was received in total terms.

In addition to the assets of the enterprise, this type displays available property and external debts.

Company assets are divided by type:

- monetary;

- expensive;

- material (property, inventory, etc.);

- settlement;

- distribution

The income of active accounts is constantly recorded according to Dt, and the decrease or disposal - according to Kt. In the most accessible way, you can consider the accounting account called “Cashier”, number 50. The California Hotel received revenue for rental services for a golf course and car parking in the amount of 38 thousand rubles. During the specified day, the staying guest received a refund for the overpayment of room rent in the guest house. This is due to the fact that the visitor left a day earlier. The refund amount is 4 thousand rubles. At the end of the day, the remaining funds were transferred from the cash register to the current account. All that remains is the approved balance limit for the cash register.

Sample

The calculation is made as follows:

- debit 50, credit 76, transaction description - revenue received for field and parking services, amount - 38,000. Document - receipt;

- debit 76, credit 50, transaction description - partial refund, amount - 4000. Document - consumable;

- debit 51, credit 50, description of the transaction - cash transfer to an account, amount - 34000. Document - expenses.

The executed transactions are displayed in the table.

What is passive type?

Unlike the first example, they display the liability of the institution. The presented accounts have an initial credit balance, the increase in turnover is carried out on a loan, and the final balance can only be in the form of a credit balance. They indicate the state of passivity, which is the source of financial resources for the company, and also indicate changes in them.

Description

The chart of such accounts can be reflected according to existing types:

- stock;

- on accounting for borrowed funds;

- on depreciation of assets.

A simple example of a movement of this type using the example of “Authorized Capital”, number 80. The owner contributed funds that are displayed according to Kt. The corresponding account can be in the form of cash (number 50) or non-cash (number 51), depending on the type of receipt of funds.

The posting will look like this: debit 51, credit 80, description of the transaction - transfer of funds to the authorized capital, amount - 10,000. Document - payment order.

What are active-passive types?

An alternative option, in which there are signs of active and passive types at the same time, is called active-passive. The type shown may have a credit or debit balance at the end of the period. Indicate operations:

- for settlements with counterparties, for example, buyers or suppliers, persons who are accountable);

- budget (taxes and fees;

- other transfers and operations.

It is necessary to consider an example of posting, according to invoice number 60. I completed an order from the trading company “First” for a batch of machines and tools for a total amount of 118,000 rubles. (VAT included). According to the contract, the conditions are stipulated for delivery only after a fifty percent advance payment. After “Leader” transferred the advance payment, the products were shipped in full.

The wiring is done like this:

- debit 60.2, credit 51, transaction description - transfer of advance payment for the supplier, amount - 59000. Document - payment order;

- debit 10, credit 60.1, description of the transaction - capitalization of inventory items, amount - 50000. Document - delivery note;

- debit 10, credit 19, description of the transaction—acceptance of input value added tax, amount—9000. Document—invoice;

- debit 60.1, credit 60.2, description of the transaction - partial offset of the advance, amount - 59000. Document - financial statements.

Based on the results of the transaction received, after submitting the consignment note, on Dt 60.1 there remained a balance of debt to the seller, which amounted to 59 thousand rubles. In this particular case, the synthetic account has a credit balance, which indicates a debt to the seller.

Diagram and structure

The balance sheet in accounting creates the state of the property and the sources that form it for a specified period (for example, the first day of the month). Owners and directors of the company who supervise and manage business operations should have indicators of the movement of property and sources of income. These indicators can be obtained using an accounting system.

Accounts are a local system that is formed as a result of the influence of business transactions. The system performs accounting and control of the movement and availability of accounting objects. Each accounting object must have its own account, which is a store of data about the business processes carried out in the company.

Economic influences on the accounting object differ only in two directions - decrease or increase, which are visible in the balance sheet summary of data.

The account itself is divided into two informative sections, called Dt and Kt. Each direction, depending on the indicated object, is used to take into account changes that are directed towards decreasing or increasing the primary indicator of the state of the accounting object.

Any account, both active and passive, requires the following data:

- initial balance or balance (Сн);

- standards that lead to a decrease or increase in the primary balance, the final indicators of which for each side (Dt and Kt) are called turnover (V) (debit and credit turnover, respectively);

- the final balance (balance - Sk), indicating the state of the object of accounting supervision at the end of the reporting period.

Main types

The most commonly used active species are:

- 01 “Fixed assets”;

- 03 “Profitable investments in material assets”;

- 04 “Intangible assets”;

- 08 “Investments in non-current assets;

- 09 “Deferred tax assets”;

- 10 "Materials"

- 19 “VAT on acquired values”;

- 20 “Main production”;

- 23 “Auxiliary production”;

- 25 “Overhead expenses;

- 26 “General business expenses”;

- 29 “Service industries and farms”;

- 41 "Products";

- 43 “Finished products”;

- 45 “Shipped goods”;

- 50 "Cashier";

- 51 “Current accounts”;

- 52 “Currency accounts”;

- 58 “Financial investments”;

- 97 “Deferred expenses”.

- 02 “Depreciation of fixed assets”;

- 05 “Amortization of intangible assets”;

- 42 “Trade margin”;

- 66 “Settlements for short-term loans and borrowings”;

- 67 “Settlements for long-term loans and borrowings”;

- 70 “Settlements with personnel for wages”;

- 80 “Authorized capital”;

- 82 “Reserve capital”;

- 83 “Additional capital”;

- 98 “Deferred income.

Scroll

Active-passive accounts are shown in the figure.

How to distinguish

Experienced specialists know by heart which category this or that type of account belongs to. A less experienced accountant will need to know how to distinguish active from passive. As an example, we can take 62 “Settlements with customers”. It will be necessary to perform an analysis to understand what type it can be classified as.

Chart of accounts in 1C program

The 62nd account reflects relationships with customers. For example, sale or purchase of goods, services, shipment. By selling products, the person purchasing the goods becomes a debtor to the company, which is indicated according to debit 62. Accounts receivable is an asset of the company, which means that an increase in the asset is indicated according to Debit.

After paying for the products, the debt decreases, so the decrease in the asset is reflected in Kt 62. It turns out that 62 represents an active account. But, there are cases when the buyer transfers an advance payment, then the company’s accounts payable to him or a liability turns out. It will pass according to Kt 62. After the products are shipped to the customer against the prepayment, accounts payable are reduced, the decrease in liabilities is indicated in accordance with Kt 62. In this situation, account 62 is classified as passive.

The considered example shows that count 62 has two types of signs, so it is classified in the third category, active-passive. In a similar way, you can analyze any other account and understand which class it belongs to. Electronic programs have built-in symbols and indicate opposite each value its type, according to the classification.

In accounting, there are three types of accounts. They have their own scheme and structure. You should know all existing species according to classification and be able to distinguish one from another.

Net assets of an enterprise: calculation and interpretation

Essentially, netassets shows how much the property used by the enterprise can realistically be valued at. First of all, this is necessary to analyze and identify the risks of bankruptcy of the company.

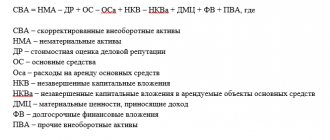

Formula for calculation

NA are calculated based on balance sheet data and include the following indicators:

Calculation example

I will give the calculation of the NAV using the example of a real company. For this I chose the Kuzbass Fuel Company. The organization is engaged in the extraction and sale of thermal coal. The reporting is based on Russian standards (RAS) for 2021 and does not include consolidated data for the entire group.

The company has no deferred income and no debt from the founders. Therefore the calculation looks like this:

40,029,277 thousand rubles. (total assets) – 16,679,715 thousand rubles. (long-term liabilities) – 7,506,614 thousand rubles. (short-term liabilities) = 15,842,948 thousand rubles.

Balance sheet codes and lines

The calculation of the NAV according to the balance sheet lines looks like this:

(Assets, line 1600) – (liabilities, lines 1400 and 1500) + (DBP, line 1530) – (debt of the founders, as part of line 1170).

Diagnostics of business efficiency using the net asset method

The main thing you need to pay attention to when analyzing the NA is that their value is not in the negative zone. This situation indicates the following trends in the enterprise:

- the activity systematically brings losses;

- the company is unable to pay its obligations.

In this case, the organization may face bankruptcy. Firm managers should monitor netassets performance and try to take actions to improve them.

Valuation of assets on the balance sheet

For evaluation, various analytical ratios or multipliers are used, which are useful in their own way and can clearly present the financial characteristics of the company’s balance sheet. Next I will talk about some of them.

Cost and average value of total assets

The aggregate indicator combines the cost of non-current and current assets as of a certain date. It is listed under line 1600.

Average value is an amount calculated as an average between data within one period. Typically this is one year.

Those. (amount at the beginning of the period + amount at the end) / 2.

Real assets ratio

Assets that are involved in the production cycle are subject to such analysis. This could be fixed assets, products, etc.

The coefficient shows how many real assets (core) there are in the overall structure. Therefore, it is generally accepted that the normal indicator should be above 0.5 points. This would mean that more than half of them are directly involved in the business activities of the company.

If the coefficient is lower, this means that most of them are non-core for the organization and some problems may be associated with this.

Asset immobilization ratio

The ratio shows the degree of efficiency in using the company's property resources. It is considered quite simple. To do this, non-current assets must be divided into current assets.

It is believed that the lower this ratio, the better the financial condition of the enterprise.

Permanent Balance Index Ratio

This multiplier shows how much non-current assets are covered by equity capital. It is generally accepted that the indicator should be below one, then the financial condition of the organization can be called stable.

If this limit is seriously exceeded, the company is considered to be overly indebted and experiencing financial difficulties.