The concept of local taxes and fees

Local authorities are also given limited powers by domestic legislation to establish local taxes and fees in the territory under their control.

The granting of such powers is due to the inability to fully ensure the interests of the basic municipal districts at the expense of the republican and regional budgets, which is why local taxation and the formation of the local budget are designed to ensure the local interests of the population and the territorial unit as a whole and to promote its development.

Local taxes and fees are mandatory payments that are established by the local authorities of the basic administrative-territorial unit within the limits of the rights and powers granted to such authorities by federal tax legislation and the Tax Code of the Russian Federation.

Like federal and regional, local taxes and fees are included in the taxation system of the Russian Federation.

The nature of such taxes and fees does not differ from other obligatory payments payable to the budgets of higher levels; they have a pronounced fiscal nature and are designed to provide financial expenses for the municipal budget.

Enrollment in the budget

We have studied what taxes the local Russian Federation collects, as well as how they are established and calculated. Let us consider the aspect related to the practical use by the municipality of the corresponding financial source. In accordance with Article 61.1 of the Budget Code of the Russian Federation, 100% of the amounts received as taxes on land and property of individuals must be credited to local budgets. In turn, the treasury of the settlements that are part of the district can be replenished based on the decisions of the municipal authorities.

System of local taxes and fees

The system of local taxes and fees is also provided for by the Tax Code of the Russian Federation and is represented by an exhaustive list of both taxes and fees. State power represented by local government cannot go beyond this list and establish additional fees or local taxes.

Local taxes are presented in the form of taxes:

- federal;

- regional;

- local, put into effect by the self-government body within the municipality.

Local fees include:

- Federal level;

- local level.

Within the region, the introduction of fees is not provided for by the Tax Code of the Russian Federation, and accordingly is unacceptable, which is why the system of fees throughout the country is represented by two levels.

We will recalculate and minimize tax deductions

Sign up for a consultation with a specialist

+7

Criticism

The Russian tax system is regularly criticized by both business and the opposition. But recently, with the worsening of the crisis, structure-forming organizations have also expressed dissatisfaction with the existing system of taxes and fees. So on December 20, 2015, through the Rossiyskaya Gazeta, the President of the RF Chamber of Commerce and Industry, Sergey Katyrin, made proposals to change the existing tax order[13]. His initiative boils down to changing the procedure for adopting new taxes and structuring and accounting for old ones to avoid double and sometimes triple taxation.

Types of local taxes and fees

Local taxes include the following:

1. Land tax. The Russian tax system provided for the introduction of this tax in order to stimulate the rational use of land with all the ensuing consequences, as well as for the development of local infrastructure. The regulatory framework consists of two levels:

- federal laws;

- acts issued by local representative bodies.

Cities of federal significance, which include Moscow and St. Petersburg, have their own characteristics, but they relate more to the procedure for introducing the specified tax.

When establishing a land tax, the authority by whose decision it is introduced also determines:

- tax rates;

- payment procedure;

- payment terms.

If necessary, they may also provide for in the same laws:

- tax benefits;

- grounds for providing benefits;

- procedure for providing benefits;

- the amount of money that is not subject to taxation for certain categories of taxpayers.

Taxpayers of land tax are:

- legal entities - organizations;

- individuals.

An important criterion for classifying them as taxpayers is the presence of a land plot that they own with one of the following rights:

- property;

- use on an ongoing basis;

- lifelong ownership, transferred by inheritance.

Individuals and legal entities using plots of land in accordance with a lease agreement or under the right of free-term use are excluded from the number of taxpayers of such tax.

The object of payment of land tax is a piece of land that is territorially related to the municipality where the local government authorities have introduced such a tax. An exception to this rule are plots of land that:

- according to the legislation of the Russian Federation were withdrawn from circulation;

- According to the legislation of the Russian Federation, circulation was limited.

2. Tax on property of individuals.

The subjects of property tax payment are citizens (not only Russian ones) who are the owners of property that is subject to tax in accordance with federal law. Such property includes:

- residential building, apartment or room;

- country house;

- garage;

- other buildings, structures and premises, as well as shares in the ownership of the above property.

The calculation of the tax amount depends on the tax base, which is annually as of 01.01. calculated in accordance with the total investment cost.

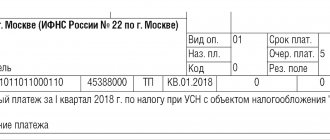

Local taxes include only trade fees. However, the effect of the right to establish local self-government is territorially limited. Such a fee can be introduced only on the territory of several administrative-territorial units, namely:

- Moscow;

- Saint Petersburg;

- Sevastopol.

Full list and characteristics

Local taxes are divided into the following subtypes :

- For the property of individuals . The object is legally owned real estate, as well as an aircraft, motor boat, or other vehicle, excluding cars, motorcycles and other self-propelled machines and mechanisms with pneumatic propulsion. The tax is paid by the owner. To make the calculation, you need to know the cadastral value of the property and the inventory value. The difference between them, multiplied by a special reduction factor, which depends on the year of payment, is the full amount.

- For land (land tax) . Owner pays. Land that is in possession or in perpetual use is taxed. The interest rate ranges from 0.3 to 3% of the land value. In addition, a decreasing or increasing coefficient may be taken into account, which is applied depending on the availability of benefits or other factors.

- Collection (registration) from persons engaged in individual entrepreneurial activities . The object of taxation in this case is the activity of an individual that he will engage in or is engaged in to make a profit. The amount is determined by the level of the minimum wage, taking into account benefits, if any.

- For industrial construction in an area recognized as a resort . Thus, the object of taxation is the right to such construction, and specific rates are set by the local government. Paid by the initiator and organizer of the construction.

- Resort . This fee is paid by vacationers, tourists who come to relax, but it does not have a fixed amount, since it is set for each specific area separately.

- For trade (trading fee) . The object is the right to trade in a certain place (places), and the payer is the entrepreneur (trader) himself. It is paid every quarter and is a fixed amount, which depends on the nature of the trade and the trading area. It can range from 50 rubles per square meter. If the area allocated for a store (retail outlet) is more than 50 meters, the figure can be more than 40,000 rubles, and in the absence of a sales area (with the exception of gas stations) - more than 80,000 for each object.

- Target fees . For example, for the maintenance of the police or landscaping. They are determined “locally” and paid for by citizens living in the given territory, as well as organizations. Limit: no more than 3% of the annual minimum wage for individuals or no more than 3% of the annual wage fund for legal entities.

- For advertising . Both individuals and legal entities who want to advertise their products pay. The rate should not exceed 5% of the cost of this advertising, the right to which is subject to taxation in this case.

- For resale of cars, computer and computing equipment . The tax amount should not exceed 10% of the amount of transactions carried out.

- For dogs (collection from citizens who own dogs, except for service dogs) . An amount established at the local level is paid per year, not exceeding one-seventh of the minimum monthly salary.

- For the right to trade in alcoholic beverages . Payment is made by purchasing a license by a person carrying out such activities. Organizations (legal entities) are charged 50 times the minimum wage for one year, 25 from individuals. If we are talking about trading at temporary points, the fee will be half the minimum monthly wage for each day.

- For the right to hold lotteries and auctions at the local level . This is a license fee and is paid by the organizer of these events. Paid in an amount not exceeding 10% of lots or tickets issued.

- For a warrant for an apartment . Individuals pay this fee when moving into a new apartment; it is no more than three-quarters of the minimum monthly wage, however, it depends on the area of the housing.

- For parking vehicles . This fee is paid by drivers who leave their cars (vehicles) in specially equipped parking lots. The amount of the fee should be set by local authorities at no more than 5% of the non-taxable minimum income.

- For the use of state symbols . Paid by manufacturers who wish to place the specified symbols on their products in the amount of no more than 25% of its value.

- For the participation of horses in races at the hippodrome . Applies to any persons who enter horses into competitions. The maximum bet size cannot be more than 5% of each winning.

- To win . Paid by persons who place bets at the racetrack and win. The rate is the same as in the previous case.

- For betting participants at the hippodrome . Included in the price of the ticket purchased when placing a bet and is no more than 5% of the cost of the bet itself.

- From a transaction on the stock exchange . Participants in such a transaction pay no more than one tenth of one percent of the amount to the local treasury.

- For the right to film (video or film) . It is contributed by the organizers of such filming (commercial television and film organizations) on the condition that they require the authorities to cordon off the filming site with law enforcement agencies. The size is determined on a case-by-case basis when organizing and planning such events.

- For cleaning the area . The taxpayers in this case are the owners of buildings and structures around which utility services carry out cleaning. Local authorities set the rate of this fee at their discretion.

- To maintain social and cultural facilities in working order, if these facilities are on the balance sheet of an enterprise or organization . The owners of the latter pay this tax, and its amount cannot exceed 12.5% of turnover (volume of products, services).

Principles of local taxes and fees

Local taxes and fees exist and operate according to the general principles of the entire tax system of the country. These include the following principles:

1. The principle of justice. When introducing a particular tax, the existence of an objective opportunity for the target group of taxpayers to pay the tax (fee) must be taken into account;

2. The principle of universality and equality of taxation. The obligation to make payments to the budget, if there are legal grounds, lies with an indefinite circle of persons who are equal in their rights and responsibilities. It is not permissible to unjustifiably exempt some payers from paying a tax (fee) and simultaneously collect it from others under the same conditions.

3. The principle of economic feasibility. The establishment of taxes cannot be spontaneous and arbitrary, but must be justified from an economic point of view. Their introduction should not infringe on the rights and freedoms of citizens provided for by the Constitution of the Russian Federation.

4. The principle of unity of the economic space of the Russian Federation. Taxes (fees) that in any way encroach on the integrity of the country’s economic space are unacceptable. Mandatory payments to the budget cannot directly or indirectly affect the freedom of movement within the country, both goods (works, services) and financial resources. Any obstacle to legally permitted business activities by introducing mandatory payments is prohibited.

5. The principle of compliance with the procedure for establishing a tax (fee). Taxes (fees) that are not provided for in the Tax Code of the Russian Federation or are introduced in violation of the procedure are not subject to payment.

6. Certainty of tax liability. By regulation, when the obligation to pay to the budget is introduced, all elements of taxation must be fixed. The wording of tax legal norms must be clear so that the taxpayer clearly knows for what, how much, and when the corresponding tax is required to be paid to the budget.

7. Presumption of interpretation of tax doubts in favor of the taxpayer. If there are vague formulations and doubts about tax rules, their interpretation is carried out in favor of the taxpayer.

Second category: regional taxes

The list of them is small, but according to the table, they will continue in 2021. Regional taxes are a payment that is established on the territory of certain subjects. They are also based on the Tax Code of the Russian Federation. But there are several situations when the inspection itself can determine how certain points will be carried out. For example, this list includes the dates when they need to be repaid and what the procedure is for this; it is also supplemented by the same rates for the transport tax at the place of residence, a list of benefits along with the basis and procedure for citizens. As in the case of federal taxes, the table of regional and local taxes applies to different categories of citizens.

Transport tax is one of the types. It must be repaid by everyone who has cars, buses, motorcycles, boats, boats, airplanes and other vehicles registered in their name. Depending on local regulations, a regional rate is set for each city. The number of horsepower or kilowatts is also taken into account. Particular attention should be paid to those who own a vehicle for up to 1 year or up to 3 years. In this case, a special formula is used to calculate the tax. Another criterion is the luxury factor. It ranges from 1.1 to 3 and depends on the cost of the car or other transport. Everything that starts from the threshold of 3 million rubles and is included in the list of the Ministry of Industry and Trade will include this luxury factor when calculating the transport tax.

The second type of taxes, which is established by regional authorities, is property taxes. It will affect any organization to which an apartment, a plot in a village or other real estate registered in the Tax Code of the Russian Federation is registered. In the event that the right to land remains with the federal source of power, then it will also set the tax.

Regional taxes apply to persons who own a gambling business. Tables, machines, cash registers, bookmaker bets, etc. are taxable entities. Each of these types has its own interest charges, which can be found out either at the inspection office at the place of registration or in the Tax Code of the Russian Federation.

Features of local taxes and fees

Despite the similarity of local taxes and fees with the general characteristics of the entire Russian tax system, local taxes and fees have their own distinctive features:

- funds received by the relevant local budget are subject to spending exclusively on the needs of the municipality itself;

- local withholding taxes are accumulated in the local budget; higher budgets at the regional or federation level are distributed in certain proportions between all three levels, including the local one.

- the decision to introduce and collect appropriate fees lies solely with local authorities;

- control over the use of local budget funds is also carried out locally by self-government bodies.

- a wide range of powers for the legal regulation of local taxation, which includes the ability to reduce tax rates and establish benefits and privileges for certain categories of tax payers.

Tax calculation

The corresponding payments to the local treasury are calculated in accordance with the recommendations set out in the letters of the Federal Tax Service and the Ministry of Finance. As for land tax, you can be guided by the wording of the letters of the Ministry of Finance dated April 9, 2007 No. 03-05-05-02/21 and dated June 6, 2006 No. 03-06-02-02/75.

If you need to calculate property tax, you can use Letter of the Ministry of Finance dated April 21, 2008 No. 03-05-04-01/19. In the case of real estate taxation, you can pay attention to the Letter of the Federal Tax Service of the Russian Federation dated July 24, 2007, No. 04-3-02/001613.

The procedure for establishing local taxes and fees

The enactment and cancellation of a particular local tax (fee) is carried out according to the rules prescribed by the domestic tax code, on the basis of legislative decisions of bodies performing representative functions at the basic level. This competence of local authorities is enshrined in Article 39 of the federal law “On the General Principles of the Organization of Local Self-Government.” According to this norm, local authorities have the right to establish (cancel):

- local taxes (fees);

- preferential conditions for local taxation for certain categories of payers.

In addition, one-time contributions of funds to the local budget by citizens living in a certain territory on a voluntary basis may be provided.

Voluntariness consists of citizens expressing their will at a local referendum, meeting, etc.

Collection of land and property taxes is also carried out after the relevant decision is made at the local level. Moreover, such a decision should not contradict the federal tax code.

Author of the article

Property tax for individuals

In relation to this type of mandatory payments, two categories of property are distinguished:

- real estate: houses and apartments, country houses, garages and other structures;

- movable: all vehicles, except cars and motorcycles.

Payers of this type of tax are persons who own the specified objects. Moreover, these can be both residents of the Russian Federation and foreign citizens. The basis for taxation is the estimated inventory value, which is multiplied by the appropriate coefficient determined by municipal authorities and tax services.

A number of categories of persons are exempt from paying property tax. These include:

- people assigned to state awards of various degrees;

- participants in the Great Patriotic War and other military operations;

- persons who participated in the measures to eliminate the consequences of the accident at the Chernobyl nuclear power plant;

- active military personnel, as well as those who retired with over 20 years of service;

- families of military personnel who died in the line of duty, as a result of illness or accident;

- pensioners;

- cultural and artistic figures, as well as persons whose property is used as museums, galleries, amateur theaters, and so on;

- from owners of buildings with an area of less than 50 square meters. m, located on the territory of gardening farms or cooperatives.

The tax payment period is 365 days. Moreover, if the owner of the property changes during a calendar year, the obligations for this type of payment are assigned to the previous owner.

Taxes are diverse

Thus, we record the fact that local fees are a fairly multifactorial phenomenon, which, according to some experts, can be recorded in two main mechanisms operating in the tax system of the Russian Federation. Firstly, these are payments classified at the level of federal legislation - land tax and property tax for individuals. Secondly, these are regional and federal taxes, through which the local budget receives funding in one way or another.