Intermediary agreements often frighten accountants because of their complexity: after all, there are 3 parties involved in the transaction. In the 1C program such operations are automated.

The article will help you understand:

- how to transfer goods to commissions in 1s 8.3;

- how to draw up a commission agent’s report if it simultaneously reflects the buyer’s advance and its offset;

- what document recognizes the intermediary’s commission as an expense;

- in which reports the principal reflects VAT on intermediary transactions;

- How the sales book and purchase book are filled out during commission trading.

Accounting with the principal in 1C 8.3 Accounting - step-by-step instructions

TEKHNOMIR LLC (hereinafter referred to as the principal) entered into an agreement with VELMART LLC (hereinafter referred to as the commission agent) for the sale of goods. According to the terms of the agreement, the agent's commission is 10% of the sales amount and is retained by the commission agent when transferring the buyer's payment at the end of the month. The principal and the commission agent work for OSNO.

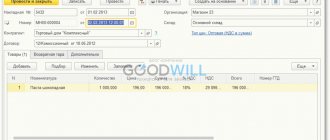

On July 7, the principal transferred goods to the commission agent in the amount of 744,000 rubles. (including VAT 20%):

Name of product Quantity, pcs. Price including VAT, rub. Cost, rub. Lenovo laptop 20 12 000 240 000 Samsung tablet 20 25 200 504 000 Total 40 744 000 On July 31, the commission agent submitted a report on advances received and goods sold to the principal, including:

- advances received - 240,000 rubles;

- offset advances - 240,000 rubles;

- sales - 246,000 rubles.

At the same time, the act and invoice for the commission were submitted.

Step-by-step instructions for creating an example. PDF

| date | Debit | Credit | Accounting amount | Amount NU | the name of the operation | Documents (reports) in 1C | |

| Dt | CT | ||||||

| Agreement with a commission agent for the sale of goods | |||||||

| July 01 | — | — | — | Commission agreement | Directory Agreements - Agreement with a commission agent (agent) for sale | ||

| Transfer of goods for commission | |||||||

| July 7 | 45.01 | 41.01 | 272 447,71 | 272 447,71 | 272 447,71 | Transfer of goods for commission | Sales (act, invoice) - Goods, services, commission |

| Registration of the commission agent's report | |||||||

| July 31 | 90.02.1 | 45.01 | 90 917,43 | 90 917,43 | 90 917,43 | Write-off of the cost of goods | Commission agent's report on sales |

| 60.01 | 76.09 | 24 600 | 24 600 | 24 600 | Deduction of commission from proceeds | ||

| 76.09 | 90.01.1 | 246 000 | 246 000 | 205 000 | Revenue from sales of goods | ||

| 44.01 | 60.01 | 20 500 | 20 500 | 20 500 | Commission accounting | ||

| 90.03 | 68.02 | 41 000 | VAT accrual on revenue | ||||

| 19.04 | 60.01 | 4 100 | 4 100 | Acceptance for VAT accounting | |||

| Registration of SF commission agent | |||||||

| July 31 | — | — | 24 600 | Registration of SF supplier | Invoice received for receipt | ||

| 68.02 | 19.04 | 4 100 | Acceptance of VAT for deduction | ||||

| — | — | 4 100 | Reflection of VAT deduction in the Purchase Book | Purchase Book report | |||

| Calculation of VAT on advances from buyers | |||||||

| payment date in July | 76.AB | 68.02 | 40 000 | Calculation of VAT on advance payment | Invoice issued for advance payment | ||

| — | — | 40 000 | Reflection of VAT in the Sales Book | Sales book report | |||

| Issuance of SF for shipment to customers | |||||||

| shipping date in July | — | — | 246 000 | Issuing SF for shipment | Invoice issued for sales | ||

| — | — | 41 000 | Reflection of VAT in the Sales Book | Sales book report | |||

| Acceptance of VAT for deduction when offsetting advance payments from buyers | |||||||

| July 31 | 68.02 | 76.AB | 40 000 | Acceptance of VAT for deduction | Commission agent's report on sales | ||

| — | — | 40 000 | Reflection of VAT deduction in the Purchase Book | Purchase Book report | |||

Commission trading in 1C: Accounting - accounting with the principal

Published 09.09.2019 11:06 Author: Administrator More and more companies have recently encountered commission trading. With the current abundance in the market, it becomes more difficult to sell your goods, and small retail companies sometimes find it difficult to purchase the required quantity of products due to a lack of working capital. Therefore, such transactions are very profitable for both the principal and the commission agent. They are formalized by commission agreements, which set out all the rights and obligations of the parties. In one of the previous articles, we looked at the accounting of commission trade transactions with a commission agent, and now we will tell you about the accounting of goods transferred to the commission agent (agent) with the consignor.

Let's start with the initial setup of the program. Go to the “Administration” section, the “Functionality” submenu and on the “Trade” tab, check the “Sale of goods or services through commission agents (agents)”. After the program is correctly configured, the document “Report of the commission agent (agent) on sales” will appear in the “Sales” section, and in contracts with counterparties a new view will appear: “With the commission agent (agent) for sale.”

Now let's move on to reflecting the fact of transfer of commission goods to the agent. Let us recall that in such a transaction the principal remains the copyright holder of the goods, therefore the transfer of goods is formalized by posting Dt 45.01 Kt 41.01.

To create it in the 1C: Accounting program, you need to create the document “Sales (goods, services, commission)” in the “Sales” section. An important detail responsible for the correct reflection of the transaction is the agreement with the commission agent.

In addition to the type of agreement, you also need to choose the method for calculating the commission, which is specified in the commission agreement.

In the program you can choose one of three types of remuneration calculation:

- percentage of the sale amount,

- percentage of the difference between sales and receipts,

- not calculated.

In our example, we will use the calculation as a percentage of the sale amount. For a more convenient calculation, let’s set the percentage equal to 10 and save the agreement.

Let's return to reflecting the transfer of goods to commission. In the tabular part of the document “Sales (goods, services, commission)”, select an item with the type “Goods”. We check the accounting accounts at the end of the line and post the document. The transfer of goods from the consignor to the commission agent is documented by a waybill TORG-12, which can be printed by clicking on the “Print” button.

After selling the goods to the buyer and receiving a report from the commission agent, enter the “Report of the commission agent (agent) on sales.” This can be done on the basis of the “Sales” document or created in the “Sales” section.

On the “Main” tab, follow the hyperlink of the accounting accounts and change 62.01 to 76.09.

The “Sales” tab displays the goods sold and also indicates the invoice date.

Attention! The “Invoice” column, highlighted in red in the figure, will be filled in automatically after posting the document.

If the agent did not sell all the goods and he wants to return some of the goods, then the “Returns” tab is filled in.

The “Cash” tab indicates the payment received by the commission agent from the buyer. On the “Advanced” tab, you can specify the Consignee and Shipper, if they are different from the Supplier and Buyer.

The completed document will generate account movements:

Dt 90.02.1 Kt 45.01 for the amount of cost of goods sold

Dt 76.09 Kt 90.01.1 for the amount of revenue

Dt 90.03 Kt 68.02 for the amount of VAT on sales of goods

Dt 60.01 Kt 76.09 for the amount of commission including VAT

Dt 44.01 Kt 60.01 for the amount of commission without VAT

Dt 19.04 Kt 60.01 VAT on commission

When issuing a certificate of completion of work for his agency services, the commission agent also issues an invoice. We register it in the footer of the document “Report of the commission agent (agent) on sales” on the “Main” tab.

Let's return to the issued invoice. The program registered it at the time of the “Commissioner's Report”. In order to print a document, you need to click on the “Go to the hierarchical list of related documents” button, or go to the “Sales” - “Invoices issued” section. This invoice will appear in the Sales Book.

The easiest way to check the commission agent’s debt is by generating a balance sheet for account 76.09, as in the figure below:

The last stage of the transaction is to receive the difference between the sale amount and the commission agent's remuneration into the bank account. In our example, it is most convenient to enter a cash receipt document based on the “Report of the commission agent (agent) on sales.”

We check the settlement account and post the document. This completes the accounting of commission trade transactions for the principal. I wish you ease in repelling such operations!

Author of the article: Alina Kalendzhan

Did you like the article? Subscribe to the newsletter for new materials

Add a comment

Comments

0 #12 Anna Fomina 02/03/2021 19:44 Good afternoon. After completing the documents, the paying organization receives the commission fee and enters the KUDiR as income. Could this be possible?

Quote

0 #11 Alina Kalendzhan 11/19/2020 02:44 I quote Natalya:

Good afternoon Tell me if we transfer the goods to a commission and the commission agent sells it at different prices (promotions and discounts) not specifically for deliveries, but arbitrarily for different goods from the supply. That is, we see real prices only in reports and there are many different products, what to do with this?

Good afternoon.

What exactly is the question? You transfer goods at one price, and he sells them at another. Reflect sales prices in the report. In the contract with the commission agent there is such a setting option as the difference between the sale and purchase prices. Quote 0 #10 Alina Kalendzhan 11/19/2020 02:42 Quote Tatyana:

Good afternoon. And if the commission agent issues another document for the services provided for the delivery and storage of goods and deducts the amount from the commission agent’s report. How to formalize it so that the total amount to be transferred matches the commission agent’s report + delivery. If all amounts include VAT, or all amounts exclude VAT, then they can be combined and called “Sales commission agent services.” And indicate the total amount in the report. Good afternoon. Where is the amount for delivery reflected in the commission agent’s report? Does it add to the commission? Thank you.

Good afternoon.

If the VAT rate is the same for everything, then it can be combined with remuneration; there is no separate line for delivery in the report. If the rates are different, then delivery must be entered in a separate act for services, but in the mutual settlement accounts indicate invoice 76.09. Then the balance at 76.09 will show the real picture. Quote 0 Natalya 11/16/2020 16:45 Good afternoon! Tell me if we transfer the goods to a commission and the commission agent sells it at different prices (promotions and discounts) not specifically for deliveries, but arbitrarily for different goods from the supply. That is, we see real prices only in reports and there are many different products, what to do with this?

Quote

0 Tatyana 06.11.2020 14:07 Good afternoon. And if the commission agent issues another document for the services provided for the delivery and storage of goods and deducts the amount from the commission agent’s report. How to formalize it so that the total amount to be transferred coincides with the commission agent’s report + up to the rate. If all amounts include VAT, or all amounts exclude VAT, then they can be combined and called “Sales commission agent services.” And indicate the total amount in the report. Good afternoon. Where is the amount for delivery reflected in the commission agent’s report? Does it add to the commission? Thank you.

Quote

+1 Galina Mikhailovna Rozhkova 10.21.2020 19:55 Thank you very much for the article!!!! It was very useful. Without you, I would have had a long and painful time getting to everything.

Quote

0 Alina Kalendzhan 10.10.2020 16:35 I quote Natalya:

Good afternoon. And if the commission agent issues another document for the services provided for the delivery and storage of goods and deducts the amount from the commission agent’s report. How to formalize it so that the total amount to be transferred matches the commission agent’s report + delivery.

Good afternoon.

If all amounts include VAT, or all amounts exclude VAT, then they can be combined and called “Sales commission agent services.” And indicate the total amount in the report. Quote 0 Natalya 10/09/2020 19:04 Good afternoon. And if the commission agent issues another document for the services provided for the delivery and storage of goods and deducts the amount from the commission agent’s report. How to formalize it so that the total amount to be transferred coincides with the commission agent’s report + up to the rate.

Quote

0 Alina Kalendzhan 09/07/2020 13:43 I quote Elena:

Good afternoon And if the goods are sold by a commission agent for export for foreign currency. In this case, the tax base for the committent must be formed according to VAT at the rate on the date of shipment, and according to profit on the date of arrival of the car, taking into account advances that are not revalued. How can this be implemented in 1C by the Principal?

Good afternoon.

The question is not a simple one, so it must be considered individually, taking into account many nuances. There will most likely be a lot of manual wiring. Quote 0 Elena 09/04/2020 16:33 Good afternoon! And if the goods are sold by a commission agent for export for foreign currency. In this case, the tax base for the committent must be formed according to VAT at the rate on the date of shipment, and according to profit on the date of arrival of the car, taking into account advances that are not revalued. How can this be implemented in 1C by the Principal?

Quote

0 Alina Kalendzhan 08.18.2020 13:22 I quote Svetlana:

Good afternoon Everything is clear about the goods. My situation is different. We sell tours through a commission agent. How to reflect in accounting the sale of travel voucher services through documents?

Good afternoon.

Why is a ticket not a product? You buy it and transfer it to the agent for further sale. If you meant that you independently provide travel services, and an agent is looking for clients for you, then such services are drawn up with a standard act of completion and are entered into the program in the section “Purchases” - “Receipts (acts, invoices). Quote 0 Svetlana 08/07/2020 13:25 Good afternoon! Everything is clear about the goods. My situation is different. We sell tours through a commission agent. How to reflect in accounting the sale of travel voucher services through documents?

Quote

Update list of comments

JComments

Regulatory regulation

A commission agreement is an intermediary agreement under which the principal instructs a commission agent-intermediary to carry out a transaction for him for a fee: for example, to purchase or sell goods (work, services).

An important feature of commission agreements: the commission agent always acts on his own behalf, but at the expense of the principal (Part 1 of Article 990 of the Civil Code of the Russian Federation).

Let's take a closer look at accounting under a commission agreement for the sale of goods (works, services).

BOO

Goods transferred by the principal to the commission agent remain the property of the principal, therefore, during the transfer, neither income nor expenses are generated (clause 12 of PBU 9/99, clause 16 of PBU 10/99).

The primary document confirming the income and expenses of the principal for the sale of goods transferred to the commission is the commission agent's sales report. The principal, if there are any objections, must notify the commission agent about them within 30 days. Otherwise, the report will be considered accepted (Article 999 of the Civil Code of the Russian Federation). Income and expenses are recognized on the date of acceptance of the commission agent's sales report (clause 12 of PBU 9/99).

Remuneration to the commission agent and expenses reimbursed to him incurred in the interests of fulfilling the contract are also recognized as expenses for ordinary activities or other expenses, depending on the nature of the intermediary transaction (clause 5, clause 11 of PBU 10/99).

WELL

When transferring goods to a commission agent, there is no transfer of ownership, therefore, proceeds from the sale of goods are not determined (Clause 1, Article 39, Article 249 of the Tax Code of the Russian Federation).

The amount of revenue is determined as of the date of sale of goods on the basis of the commission agent’s report (paragraph 5 of Article 316 of the Tax Code of the Russian Federation).

As of the date of approval of the commission agent’s report, the principal acknowledges:

- the cost of goods sold by the commission agent (clause 3, clause 1, article 268 of the Tax Code of the Russian Federation);

- commission (clause 1 of article 264 of the Tax Code of the Russian Federation);

- expenses subject to reimbursement to the commission agent (clause 1 of Article 264 of the Tax Code of the Russian Federation).

The commission agent can fulfill the principal's instructions with additional benefit: sell the goods at a higher price or buy them at a lower price than stipulated in the contract. In this case, unless otherwise provided by the agreement, the principal and the commission agent must divide such income in half (Article 992 of the Civil Code of the Russian Federation).

For the principal, additional income due to a product sold at a higher price is an increase in sales. For the commission agent - an increase in commission or a separate type of income.

VAT

When transferring goods from the principal to the commission agent, there is no object of VAT taxation (clause 1, article 39, clause 1, article 146 of the Tax Code of the Russian Federation). Therefore, VAT is not calculated and no invoice is issued.

Upon notification of the receipt of an advance payment to the account of the commission agent or the sale of goods, the principal calculates VAT and re-issues the commission agent an advance (or for sale) invoice, drawing it up in full accordance with the data of the invoice issued by the commission agent to the buyer (clause 1 of Article 167 of the Tax Code of the Russian Federation , paragraphs "i" - "l" paragraph 1, paragraphs "a" paragraph 2 of the Rules for filling out an invoice, approved by Decree of the Government of the Russian Federation of December 26, 2011 N 1137).

The principal calculates VAT on the date of advance payment or shipment of goods. The tax base is defined as (clause 1 of article 154 of the Tax Code of the Russian Federation):

- the amount of receipt of prepayment, partial payment, including VAT;

- cost of goods sold based on selling prices.

Basic concepts of commission relationships

A commission agreement is concluded between the principal, who is the owner of the goods, and the commission agent, who assumes the obligation on his own behalf, but at the expense of the principal, to carry out transactions with this product. The commission agent receives a certain remuneration for his services. This type of relationship can also be used for the sale of work or services, but most often a commission agreement is concluded specifically for the sale of goods.

Before entering into an agreement, the parties must agree on its essential terms. In accordance with Chapter 51 of the Civil Code, in an agreement of this type, such a condition is its subject matter. In other words, the contract must provide that the commission agent undertakes the obligation to carry out transactions with the principal’s goods at his expense, but on his own behalf. All other conditions are not essential, and in accordance with paragraph 2 of Article 990 of the Civil Code of the Russian Federation may be absent from the commission agreement.

Until the moment when ownership of the goods passes to the buyer, the principal is considered its owner. The commission agent undertakes to transfer to him everything received under the commission agreement, as well as to draw up a report.

Agreement with a commission agent for the sale of goods

A commission agreement can be registered in the program from the Counterparties directory (Directories - Counterparties) or the Contracts directory (Directories - Contracts). And also create it directly from the document Sales (act, invoice) (Sales - Sales (acts, invoices) - Sales button).

Install:

- Type of agreement - With a commission agent (agent) for sale .

Click on the link Commission :

- Payment method - select one of the options depending on the terms of the contract: Not calculated ;

- Percentage of the difference between sales and receipts;

- Percentage of the sale amount - in our example.

If an organization performs the functions of a paying agent, for example, in retail sales through a commission agent, then click on the Paying agent and check the box:

- The organization acts as a paying agent

and choose

- Agent attribute - one of the options: Bank payment agent ;

- Bank payment subagent;

- Payment agent;

- Payment subagent.

In our example, the commission agent is not a paying agent.

Paying agent is a legal entity (except banks) or individual entrepreneurs who accept funds from individuals in favor of the supplier for goods, works, and services sold by him (part 3 of article 2, part 1 of article 4 of Federal Law of 03.06.2009 N 103 -FZ).

Paying agents are not:

- acquiring banks (Part 3 of Article 2 of Law No. 103-FZ);

- payment aggregators (Yandex.Checkout, etc.);

- intermediaries performing other services other than accepting payments: courier services, transport companies (Part 1, Article 2 of Law No. 103-FZ).

However, within the framework of using 1C, payment agents are considered to be all intermediaries who accept money from individuals in payment for goods (work, services) of the principal for whom records are kept in the program.

Setting up accounts for settlements with counterparties

The main settlement accounts for the commission agent are configured from the counterparty card using the appropriate link. They will be automatically inserted into documents.

Set up separate accounting of settlements on the accounts:

- on commission: 60.01 “Settlements with suppliers and contractors”;

- 60.02 “Settlements for advances issued”;

- 76.09 “Other settlements with various debtors and creditors.”

Transfer of goods for commission

The transfer of goods for commission in 1C 8.3 to the commission agent is reflected in the document Sales (act, invoice) transaction type Goods, services, commission (Sales - Sales (acts, invoices) - Sales button).

Fill in:

- Counterparty is a commission agent;

- Agreement - with a view to the commission agent (agent) for sale ;

- Warehouse - the warehouse from which goods are shipped.

In the tabular part in the columns:

- Accounting account - the account in which the transferred goods were recorded, by default it is filled in 41.01 “Goods in warehouses”, adjust if necessary;

- The transfer account - 45.01 “Purchased goods shipped” - is filled in automatically, since there is no transfer of ownership during shipment.

The program automatically sets in the field:

- Invoice - Not required , since there is no VAT subject to taxation.

Transfer of goods to commission in 1C 8.3: postings

The document generates the posting:

- Dt 45.01 Kt 41.01 - transfer of goods to commission.

Registration of SF commission agent

Registration of an incoming commission invoice is carried out in the document Sales report of the commission agent (agent) on the Main .

To register an incoming invoice, indicate its number and date at the bottom of the document form and click the Register .

Invoice document is automatically filled in with data from the document Sales report of the commission agent (agent) .

- Operation type code : “Receipt of goods, works, services.”

Open the invoice received Invoices received (Purchases - Invoices received).

If the document has the Reflect VAT deduction in the purchase book by date of receipt checkbox , then when it is posted, entries will be made to accept VAT for deduction.

Postings

The document generates the posting:

- Dt 68.02 Kt 19.04 - acceptance of VAT for deduction on commission.

Sections 10 and 11

In addition to sections 8 and 9, intermediaries fill out two more new sections - 10 and 11. This applies to commission agents, agents acting on their own behalf, developers, as well as forwarders who take into account only intermediary remuneration in their income (clause 5.1 of article 174 of the Tax Code of the Russian Federation ).

Section 10 contains information about issued invoices from Part 1 of the accounting journal. And in section 11 - the indicators of received invoices, which are contained in part 2 of the accounting journal, with the exception of the names of the seller and buyer.

The data in sections 10 and 11 are essential for checking the declaration. After all, journal entries create a relationship between the supplier's sales book and the customer's purchase book. If the intermediary incorrectly fills out the invoice log, the buyer will need to prepare an explanation for the inspectors. Let's explain with an example.

Example 2. How a commission agent should fill out an invoice journal. LLC "Commissioner" entered into an agreement for the sale of goods to LLC "Committent". The commission agent sold these goods and issued an invoice. The cost of goods is 354,000 rubles, including VAT - 54,000 rubles. The invoice lists the commission agent as the seller. The commission agent registered this invoice in part 1 of the accounting journal. But VAT on the cost of shipped goods is assessed not by the commission agent, but by the principal. Therefore, the commission agent transferred data on the shipment of goods to the principal. The accountant of Komitent LLC also drew up an invoice for the shipment and registered it in the sales book as shown in the sample below. The principal then handed over this invoice to the commission agent. The principal issues an invoice for the entire cost of goods sold. Even if the commission agent transfers to the principal the proceeds from the sale of goods minus remuneration. That is, the cost indicators in the invoice of the commission agent and the principal must be identical. They do not depend on settlements between the intermediary and the principal. The accountant of LLC "Commissioner" registered the invoice received from the principal in part 2 of the accounting journal. Then the commission agent added data from the principal’s invoice to columns 10–12 of part 1 of the accounting journal. This is the name of the principal, INN/KPP and invoice details. A sample log book is shown below. Thus, LLC “Buyer” claimed a VAT deduction based on the invoice of LLC “Commissioner”. In the purchase book, the commission agent will be indicated as the seller (see example below). When checking, the program will refer to the commission agent's accounting journal and determine the supplier of goods, which is the principal. The program will then check the tax accrual in the principal's sales ledger. If the commission agent does not receive the principal's invoice and does not indicate its data in columns 10–12 of part 1 of the accounting journal, then the buyer will be asked for clarification on VAT deductions.

Since 2015, companies have not registered invoices for commission remuneration in the accounting journal (clause 3.1 of Article 169 of the Tax Code of the Russian Federation). Therefore, these invoices do not need to be reflected in section 10.

It is possible that the intermediary company applies a special regime. Then you do not need to fill out a VAT return. But the invoice log must be submitted to the inspection no later than April 20 (clause 5.2 of Article 174 of the Tax Code of the Russian Federation).

Calculation of VAT on advances from buyers

After registering advances in the document Sales report of the commission agent (agent), it is necessary to calculate VAT and register invoices for prepayment. To do this, use the processing Registration of invoices for advance payments (Bank and cash desk - Invoices for advance payments).

Set the period and click the Fill .

After filling out, check the settings using the links - these are the links to fill out the form:

- Numbering of invoices - numbering order, one of the options: single - Single numbering of all issued invoices ;

- separate with the prefix “A” - Separate numbering of invoices for advance payments with the prefix “A” ;

Next, click the Run . Invoices issued for advance payments are registered. PDF

Generated invoices will need to be adjusted. To do this, follow the link Open list of invoices for advance payment .

Enter:

- Payment document No. ... from - the number and date of the payment order for the buyer's advance according to data from the commission agent's report.

In the tabular part:

- Nomenclature - the name of the product in strict accordance with the wording in the commission agent’s SF.

Automatically installed:

- The transaction type code is “Advances received.”

Click the Print to print the invoice form for the advance payment.

VAT declaration

In the VAT return, the amount of calculated tax on advances from buyers is reflected:

- On page 070 “Amounts of payment received, partial payment...” of Section 3: the amount of prepayment received, including VAT;

- calculated VAT amount.

- invoice issued, transaction type code "". PDF

Implementation and presentation of the report in different periods

By agreement between countries, the commission agent can submit a report on each fact of implementation, and also do this with a certain frequency or after completing the entire order.

However, when choosing the frequency of submission of the report, it is worth considering that on its basis the committent calculates VAT. And there is one nuance here - the base for this tax is determined at the time of sale of the goods. This is stated in paragraph 16 of the resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated May 30, 2014 No. 33. Thus, the principal must charge VAT in the tax period when the commission agent sold his goods.

In accordance with Article 316 of the Tax Code of the Russian Federation, proceeds from sales must be determined by the principal on the basis of a notice of sale received from the commission agent. The commission agent is given three days to notify the principal of the sale of the goods.

However, in a situation where the contract provides for the submission of a report, say, after the sale of the entire volume of goods transferred to the commission, a discrepancy may arise: the sale was recorded in one period, and the report was received in another.

Since the principal has already reported VAT for the period to which the sale of his goods relates in accordance with the received report, he will have to recalculate the amount of tax and submit an updated declaration. Indeed, based on paragraph 1 of Article 54 of the Tax Code of the Russian Federation, if in the current period errors were discovered in determining the tax base for previous periods, they should be corrected. Moreover, it is necessary to adjust the tax accounting registers, the tax base and the amount of VAT for the period in which the errors were made.

Is it possible, instead of filing an updated declaration, to include income from goods previously sold by the commission agent in the VAT base for the current period? No, you shouldn’t do this, because the risk of sanctions from the Federal Tax Service is too great. During the inspection, experts will consider that in the period when the goods were actually sold by the commission agent, the principal did not reflect this sale and underestimated the amount of VAT. As a result, additional taxes, fines and penalties will follow.

Issuance of SF for shipment to customers

Registration of invoices issued for sales is carried out automatically by the program when conducting the Commission Agent (Agent) Sales Report .

In the document Invoice issued for sales, Add button to enter the number and date of the payment order for the advance according to the data from the commission agent’s report.

- Operation type code : “Sales of goods, works, services and operations equivalent to it.”

When reflected in one document, the Commission Agent's (Agent's) Report on sales of advances and sales, the chronological sequence of invoice numbering may be disrupted, especially if all issued invoices are numbered uniformly.

Violation of the sequence not a critical error and cannot entail a refusal to deduct VAT (clause 2 of Article 169 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated January 12, 2017 N 03-07-09/411).

VAT declaration

In the VAT return, the amount of calculated tax on the sale of goods to customers is reflected:

- On page 010 “Sale (transfer on the territory of the Russian Federation for one’s own needs) of goods, works (services), transfer of property rights at appropriate tax rates...” Section 3: tax base;

- calculated VAT amount;

- invoice issued, transaction type code "". PDF

Option 3. Purchase of goods. Principal - VAT payer

When purchasing goods, works or services through an intermediary, we have, in fact, a mirror sales situation. The legal side of the sales transaction is not the intermediary, but the principal, since according to the rules of civil law for transactions made by an intermediary, the rights and obligations arise with the principal. So it is he who pays for the purchase, takes it into account and receives the right to deduct. Accordingly, the most important thing here is to correctly issue the invoice. There are no problems if the intermediary works on behalf of the principal. Then all documents are immediately issued in the name of the latter. But if the intermediary acts on his own behalf, the document flow becomes more complicated.

In such a situation, the principal must receive two invoices from the intermediary. The first is for the product (it is billed taking into account the seller’s invoice; we will talk more about this in the part regarding the intermediary), the second is for the remuneration. In addition, the intermediary must provide the principal with a copy of the invoice issued by the seller of the purchased goods in the name of the intermediary. Invoices for goods and remuneration must be registered in Part 2 of the journal of received and issued invoices and the purchase book. A copy of the invoice issued by the seller to the intermediary does not need to be registered anywhere, but is supposed to be kept for four years (clause “a”, clause 15 of the Rules for maintaining a log of received and issued invoices).

Thus, the principal will be able to deduct VAT amounts based on the invoice issued to him by the intermediary reflecting the invoice figures issued by the seller. The right to deduction arises for the customer in the general manner, regardless of the date indicated in the invoice for the transfer of goods from the intermediary to the customer (see letter of the Ministry of Finance of Russia dated July 20, 2012 No. 03-07-09/80).

Acceptance of VAT for deduction when offsetting advance payments from buyers

To deduct VAT on offset advances from buyers, create a second document, Report of a commission agent (agent) on sales (Sales - Reports of commission agents on sales - Create button).

- Main tab - fill in the same way as in the first document.

- Implementation tab - do not fill out.

- Cash tab - fill in as follows:

Click the Add to enter:

- Type of payment report - Advance offset ;

- Buyer - name of the organization whose advance payment is credited towards the shipment;

- Event date - the date of shipment of the goods by the commission agent to the buyer;

- Amount including VAT (RUB) - the amount of the offset advance;

- % VAT — 20/120.

Postings according to the document

The document generates the posting:

- Dt 68.02 Kt 76.AV - acceptance of VAT for deduction on offset advance payment.

VAT declaration

The VAT return, the tax subject to deduction, reflects:

- On page 170 “The amount of tax calculated by the seller from the amounts of payment, partial payment, subject to deduction from the seller from the date of shipment...” Section 3: the amount of VAT subject to deduction.

- advance invoice issued, transaction type code "". PDF

We looked at the principal's accounting in 1C 8.3 Accounting, transfer of goods to commission in 1C 8.3 in the principal's accounting, transactions for the transfer of goods to commission in 1C.

Section 9

In section 9, you must provide sales ledger data for each invoice issued. Let's focus on the most important indicators. How to fill out the book can be seen in the sample.

Operation type code (column 2 of the sales book). In the sales book, it is worth recoding all transactions from the beginning of the first quarter that fall under the new list of codes recommended by the tax authorities (letter of the Federal Tax Service of Russia dated January 22, 2015 No. GD-4-3/794). This is necessary so that the Russian Federal Tax Service program, when checking, can compare the data for a specific invoice in the declaration of the buyer and supplier.

Seller's invoice number (column 3). The best option is to use simple invoice numbering without alphabetic symbols, dashes or other symbols. Then there will be fewer discrepancies between the reporting of the supplier and the buyer.

INN/KPP of the buyer (column 8). Companies that sell goods or services to individuals may not indicate the TIN in the invoice, and therefore in the sales book. Accordingly, this indicator will not be included in the declaration. There is no violation in this. But for correct verification, code 26 must be entered in column 2 of the sales book. It indicates the sale of goods to customers who are not VAT payers or are exempt from paying tax. This code also applies to sales to individuals. It must also be provided when the company receives advances from such buyers.

INN/KPP of the intermediary (column 10). If goods are sold through a commission agent or agent acting on his own behalf, reflect his details in the sales book. The same data will be recorded in the declaration.

Number and date of the document confirming payment (column 11). When shipping goods, payment document details do not need to be recorded in column 11 of the sales book. If the buyer made an advance payment, indicate the payment details for which the advance was received.

Cost of sales exempt from tax (column 19). This column is intended only for organizations that apply VAT exemption (Article 145 of the Tax Code of the Russian Federation). If the company sells goods that are not subject to VAT under Article 149 of the Tax Code of the Russian Federation, the sales book is not filled out. But you need to include section 7 in the declaration, intended for preferential transactions.

Let's add that the company can register corrected and adjusting invoices in the sales book and purchase book. Then you need to indicate the details of not only these documents, but also the original invoice.

Section 9 on paper return

Simplified or imputed companies that are tax agents have the right to submit a VAT return on paper. We are talking, in particular, about those companies that buy goods from a foreign organization on the territory of Russia (Clause 2 of Article 161 of the Tax Code of the Russian Federation). Or they rent state or municipal property (clause 3 of article 161 of the Tax Code of the Russian Federation).

It is safer for such companies to fill out a sales book and section 9 of the declaration. The explanation is this. From the Tax Code of the Russian Federation it follows that the sales book is kept only by VAT payers (clause 3 of Article 169 of the Tax Code of the Russian Federation). But from the rules for maintaining a sales book, we can conclude that tax agents must register invoices in the sales book (clause 3 of the Rules for maintaining a sales book, approved by Decree of the Government of the Russian Federation of December 26, 2011 No. 1137). And these rules do not contain exceptions for companies on special regimes. This was confirmed by the Federal Tax Service of Russia.

Example 1. How a simplified tax agent fills out section 9 of the declaration A simplified company leases municipal property. On March 16, 2015, the company transferred the rent under the agreement and withheld VAT from this amount. The rent is 59,000 rubles, including VAT - 9,000 rubles. The accountant wrote out an invoice for the amount of the rent and registered it in the sales ledger. And then reflected the invoice indicators in section 9 of the declaration. A sample of filling out section 9 is given below. The company does not have the right to deduct this amount of tax, since it applies a special regime. And only VAT payers can claim VAT deductions.

Note. What has changed in the old sections of the declaration

- The tax base . Amounts received from buyers and related to payment for goods must be reflected in the total sales on line 030 or 040 of section 3 of the declaration, depending on the VAT rate. For example, this applies to interest on bills received as payment for goods, the amount of which exceeds the refinancing rate (clause 1 of Article 162 of the Tax Code of the Russian Federation). Previously, these amounts were required to be shown separately on line 080.

- VAT deductions . The tax presented by contractors for capital construction work must be included in the total amount of deductions on line 120 of section 3. In the previous declaration form, such company tax deductions were indicated on line 140.

- Export of goods . Sections 4–6, which exporting companies fill out, have changed. Thus, in section 4, new codes for returning goods (1010447) and changing the price of goods (1010448) appeared.