Deferment of tax payment and reporting due to COVID-19

A 6-month deferment has been introduced for the payment of tax under the simplified tax system.

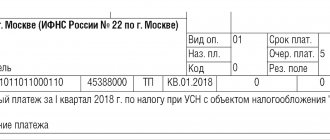

LLCs must pay tax for 2021 by September 30, 2021, and individual entrepreneurs by October 30. The advance payment for the first quarter of 2021 must be made by October 26, for the first half of 2021 by November 25. The above tax payment deadlines apply only to LLCs and individual entrepreneurs included in the list of the most affected industries. Businesses that the state has not recognized as affected must pay taxes by May 12. Those companies that were recognized as a going concern and continued to operate on non-working days were required to pay taxes within the standard deadlines.

Tax payments (except VAT) and insurance premiums for the second quarter will not be allowed to be paid at all. The President of the Russian Federation announced this in his last address on May 11. The benefit is intended for individual entrepreneurs and organizations that are included in the SME register and operate in the most affected industries. There is no regulation on this issue yet, so the exact conditions are unknown.

Deferment of payment of insurance premiums for employees and reduction of rates

From April 1, 2021, insurance premium rates for employees can be reduced to 15%. This applies not only to the affected industries, but to all small and medium-sized businesses (Federal Law No. 102-FZ dated April 1, 2020).

If an employee’s salary exceeds the federal minimum wage (12,130 rubles) at the end of the month, then reduced rates are applied to part of the excess. It looks like this:

| Insurance premiums | Salary up to 12,130 rubles | Salary over 12,130 rubles |

| Pension Fund | 22 % | 10 % |

| Compulsory Medical Insurance Fund | 5,1 % | 5 % |

| FSS | 2,9 % | 0 % |

Example. AfroPineapple LLC is included in the SME register. For April 2020, she paid her employee 45,000 rubles. For part of the earnings within the minimum wage, contributions are calculated at the standard rate:

- 12,130 rubles × 22% = 2,668.6 rubles

- 12,130 rubles × 5.1% = 618.63 rubles

- 12,130 rubles × 2.9% = 351.77 rubles

The payment exceeding the minimum wage amounted to 32,870 rubles. Contributions to it are calculated at reduced rates:

- 32,870 × 10% = 3,287 rubles

- 32,870 × 5% = 1,643.5 rubles

Total for April, AfroPineapple LLC will pay 8,569.5 rubles instead of 13,500 (45,000 × 30%).

In his last address dated May 11, the President of the Russian Federation announced that individual entrepreneurs from the most affected industries will receive a tax deduction for insurance premiums within one minimum wage, that is, 12,130 rubles of salary will not be subject to insurance premiums. There is no regulatory act on this benefit yet, so the detailed conditions are unknown.

In addition, businesses from affected industries may pay insurance premiums for workers later:

- for May 2021 - December 15;

- for June 2021 - November 16;

- for July 2021 - December 15.

Installment payment of taxes and contributions

Also, SMEs from the affected industries were given an installment plan to pay taxes, advance payments and insurance premiums, for which a deferment is provided. The installment payment period begins in the month following the month in which the extended payment due date occurs. You must pay in equal installments in the amount of 1/12 of the specified amount monthly, but no later than the last date.

For example, the extended deadline for paying income tax for 2021 is September 28. You will have to pay 1/12 of the tax amount monthly, starting in October.

For the payment of VAT and agency personal income tax, the government did not postpone the payment deadline and did not provide for an installment plan.

New simplified tax system limits and tax rates

In April 2021, the simplified basic rates will remain the same: simplified tax system “income” - 6%, simplified tax system “income minus expenses” - 15%. Entrepreneurs lose the right to apply the simplified tax system if the number of their employees exceeds 100 people and their annual income exceeds 150 million rubles.

In connection with the coronavirus, 49 regions of Russia have reduced rates for organizations and individual entrepreneurs on the simplified tax system. Let us remind you that the maximum reduction is possible up to 1% on the “income” basis and up to 5% on the “income minus expenses” basis. Some have reduced taxes for everyone, while others have reduced taxes only for affected industries - check local government regulations for details.

Bill No. 875580-7 provides for the opportunity to remain on the simplified tax system until the end of the year if the established limits are exceeded to an insignificant extent. But from the quarter in which excesses were made, you will have to pay taxes at an increased rate - 8% for the simplified tax system “income” and 20% for the simplified tax system “income minus expenses”.

If intermediate limits are exceeded, the right to simplification will be lost and taxes will have to be paid within the framework of OSNO.

You can clearly see the changes in the tax regime in the table.

| Criteria for applying the simplified tax system for individual entrepreneurs and legal entities | Tax rates of the simplified tax system “income”/“income minus expenses” | Loss of the right to the simplified tax system and transfer to OSNO | |

| 6 % / 15 % | 8% / 20% (draft bill) | ||

| Amount of workers | Less than 100 people | From 101 to 130 people | More than 130 people |

| Annual income | Less than 150 million rubles | From 150 to 200 million rubles | More than 200 million rubles |

If in the next tax period the income for the year does not exceed 150 million rubles, and the number of employees is 100 people, the taxpayer has the right to apply the standard rate - 6% or 15%.

If the limit on revenue or number of employees is exceeded at the end of the year, then advance payments will have to be paid at an increased rate for the entire next year.

New income limits

The income limit of 150 million rubles has not been indexed since 2021, and finally, for 2021, a deflator coefficient of 1.032 was established (Order of the Ministry of Economic Development of Russia No. 720 of October 30, 2020).

This means that in 2021, in order to retain the right to apply the simplified tax system, the simplified person’s income should be no more than 150 × 1.032 = 154.8 million rubles. The income limit for 9 months for switching to the simplified tax system is also subject to indexation by the same coefficient. If previously it was 112.5 million rubles, then from 2021 it will be 116.1 million rubles. That is, in order to switch to the simplified tax system from 2022, the organization’s income for 9 months of 2021 should be no more than 116.1 million rubles.

To switch to the simplified tax system from 2021, the income limit for 9 months of 2020 remained the same - 112.5 million rubles.

Let us remind you that individual entrepreneurs, before switching to the simplified tax system, are not required to meet the income limit for 9 months; this rule is only for organizations. But already being on the simplified tax system, they are also required to adhere to limits for annual income.

Additional expenses to reduce the tax base

For taxpayers using the simplified tax system, “income minus expenses” has increased the list of expenses by which the tax base can be reduced. Now these include costs (clauses 7, 8 of article 1 of the Federal Law of April 22, 2020 No. 121-FZ):

- for disinfection of premises;

- purchase of devices, equipment, masks, gloves, antiseptics and other means of personal and collective protection.

But only if these costs are incurred to fulfill the requirements of state authorities, local governments and their officials in connection with the spread of coronavirus.

Amount of the simplified tax system in 2021

Exceeding the income limit and (or) the average number of personnel automatically increases the single tax rate:

- “Income” - 8% (instead of 6%)

- “Income minus expenses” - 20% (instead of 15%)

In both cases, the tax burden will increase by a third, however, the transition to the simplified tax system in 2021 will become more profitable for businessmen on OSNO with incomes up to 200,000,000 rubles. If the taxpayer does not exceed the old limits in force in 2019, he will pay tax at classic rates - 6% or 15%.

Simplified tax system online and cancellation of declarations

Bill No. 875583-7 provides for the abolition of annual declarations for those individual entrepreneurs who use the simplified tax system for “income” and work with an online cash register. They will also not need to keep KUDiR - a book of income and expenses. The Federal Tax Service officially called this mode “STS-online”.

Under the new regime, the tax office will receive data on an entrepreneur’s income through an online cash register. Based on them, she herself will generate receipts for advance payments and taxes at the end of the year. They can be seen in the taxpayer’s personal account.

The Federal Tax Service will also take into account and deduct the amounts of insurance premiums paid for yourself and your employees. Entrepreneurs will only have to pay taxes on time.

Refusal to independently submit an annual declaration is a right, not an obligation, of an entrepreneur. If he decides to transfer the function of calculating taxes to the Federal Tax Service, he must notify the tax authority about this through the taxpayer’s personal account, indicating the date of transition.

Now the Tax Code of the Russian Federation obliges all simplifiers to annually submit an income declaration. Until March 31 of the next year - for organizations, until April 30 - for individual entrepreneurs (Article 346.23 of the Tax Code of the Russian Federation).

Increase in insurance premiums for individual entrepreneurs

For 2021, individual entrepreneurs will pay increased amounts of insurance premiums for themselves. Their size is fixed in part 1 of Art. 430 Tax Code of the Russian Federation. More details in the table.

| Purpose of payment | Contribution amount for 2021 | Payment deadline |

| For pension insurance in the Federal Tax Service | 32,448 rubles | Until 12/31/2020 |

| For health insurance in the Federal Tax Service | 8,426 rubles | Until 12/31/2020 |

| For pension insurance in the Pension Fund of the Russian Federation, if the annual income from business activities exceeds 300,000 rubles | 1% of income over 300,000 rubles | Until 07/01/2021 |

Contributions for 2021, which individual entrepreneurs were required to pay before July 1, 2020, were deferred for 4 months. But only for affected industries.

An individual entrepreneur is required to pay insurance premiums to the Pension Fund and the Compulsory Medical Insurance Fund even when he does not conduct business and does not receive income. Exceptions are provided in Part 7 of Art. 430 Tax Code of the Russian Federation.

Limit bases of insurance premiums for employees

To pay insurance premiums for an employee, the employer takes into account all his income on an accrual basis from the beginning of the year. If they do not exceed the maximum base established by the Government of the Russian Federation, then the standard tariff rate is applied.

When the amount of annual payments to an employee reaches a certain limit, the employer pays insurance premiums for him at a preferential rate.

The maximum bases of insurance premiums for 2021 are established by Decree of the Government of the Russian Federation dated November 6, 2019 No. 1407. Maximum bases for compulsory medical insurance and injuries are not established.

| Insurance fee | Limit base | Standard rate | Rate when income base is exceeded |

| Pension insurance | 1,292,000 rubles | 22 % | 10 % |

| Social insurance in case of temporary disability and maternity | 912,000 rubles | 2,9 % | 0 % |

| Compulsory health insurance | — | 5,1 % | |

| Accident insurance in connection with occupational diseases and work-related injuries | — | From 0.2% to 8.5% depending on the class of professional risk of activity | |

In Art. 427 of the Tax Code of the Russian Federation contains a list of taxpayers who have the right to apply a preferential tariff rate. For example, participants in the free economic zone of Crimea and Sevastopol, organizations participating in the Skolkovo project.

Simplified taxation system limits for 2021

From January 1, 2021, entrepreneurs and organizations will be able to exceed the limits on income and number of employees, while maintaining the right to the simplified tax system. The innovation is enshrined in bill No. 90556.

| Income limits | Limits on the average number of employees | |

| Limit | 150 000 000 ₽ | 100 people |

| Overlimit | + 50 000 000 ₽ (200 000 000 ₽) | + 30 people (130 people) |

| If the individual entrepreneur/LLC is between the limit and the excess limit | Tax at an increased rate (+2…+5%) | |

| If the individual entrepreneur/LLC has crossed the upper limit of the excess limit | Forced transfer to OSNO and additional tax assessment | |

Thus, the basic limits of the simplified tax system for 2021 remain at the level of previous years. The transition to the category of “medium business” - from the simplified tax system to the OSNO - becomes smoother and painless from the point of view of the tax burden.

Filing personal income tax reports

From January 1, 2021, reporting in form 2-NDFL with any indication and 6-NDFL at the end of the year must be submitted no later than March 1. The deadline has been pushed back by a month. From 2021, information on the income of individuals must be submitted as part of a single 6-NDFL report.

Due to the coronavirus, the deadline for submitting the 6-NDFL report for the first quarter was postponed to July 30.

Now companies with ten or more employees must submit 2-NDFL, 6-NDFL and ERSV (unified calculation of insurance premiums) electronically. If the reports are submitted in paper form, they will be fined in the amount of 200 rubles (Article 119.1 of the Tax Code of the Russian Federation).

If the number of employees is less than ten people, it is allowed to submit reports on paper.

Reporting related to employee availability

The employer is required to submit many reports related to the calculation of personal income tax of employees, as well as contributions. From 2021 the number of reports will decrease. See what employee reports will be new in 2021 for an accountant:

- the form “Information on the average number of employees” will cease to exist as a separate unit and will become part of the calculation of contributions starting from the reporting for 2021;

- forms 6-NDFL and 2-NDFL will be combined into one.

The SZV-TD form cannot be called new, since it has been used since 2020. But a situation could arise where an organization or individual entrepreneur never submitted this report if there was not a single personnel change in 2021. In this case, the SZV-TD in 2021 will in any case have to be submitted by February 15.

Starting from 2021, a fine for untimely or inaccurate submission of SZV-TD will be introduced for officials in the amount of 300 to 500 rubles.

Tax holidays for individual entrepreneurs

2020 is the last year when tax holidays with a 0% rate are in effect at the federal level. In some regions of Russia, tax holidays have already ended.

In 2021, they can be used by individual entrepreneurs who meet several criteria:

- registered for the first time;

- apply the simplified taxation system or patent taxation system;

- conduct activities in the social, industrial, scientific spheres, as well as in the sphere of providing consumer services and services for providing places for temporary residence of the population;

- revenue from activities that are subject to a zero rate is at least 70% of total income.

Individual entrepreneurs using the simplified tax system “income minus expenses” do not even pay the minimum tax if they are subject to tax holidays.

The holidays are valid for two years from the date of registration of an individual entrepreneur and do not exempt entrepreneurs from paying insurance premiums for themselves and their employees. But if you registered an individual entrepreneur in 2021, you will be able to take advantage of tax holidays only until January 1, 2021.

Changes to the simplified tax system that came into force at the end of September 2019

The sensational Law of September 29, 2019 No. 325-FZ “On Amendments to Parts One and Two of the Tax Code of the Russian Federation” introduced a number of innovations to the simplified tax system, and they are already in effect:

- Simplified people at the “income minus expenses” facility can take into account expenses associated with the purchase of fixed assets (including real estate) without waiting for the moment of submitting documents for state registration (clause 3 of Article 346.16 of the Tax Code of the Russian Federation).

- Individual entrepreneurs providing services for the provision of places for temporary residence will be able to apply tax holidays under the simplified tax system in 2021 (clause 4 of article 346.20 of the Tax Code of the Russian Federation).

Please note that from 01/01/2021 tax holidays under the simplified tax system are cancelled. Individual entrepreneurs will no longer have the opportunity to apply a zero rate.

- Simplified people include in income the amounts of subsidies received for business development (clause 1 of Article 346.17 of the Tax Code of the Russian Federation): when expenses are actually incurred from the amounts of such subsidies;

- when using subsidy amounts to compensate for expenses already incurred.

Previously, it was envisaged to include in income only those amounts of subsidies from which expenses were actually incurred.