Practice shows that the status of a tax resident or non-resident of the Russian Federation when filling out section 2 of the 6-NDFL calculation form raises many questions among accountants. In this consultation, with the help of explanations from the Federal Tax Service of Russia, we analyze 2 examples: recalculation of personal income tax due to the loss of an employee’s tax resident status and erroneous withholding of tax at a rate of 13% from the salary of a non-resident employee.

Also see:

- 6-NDFL and income certificate will be combined into one document: a draft of the new form has been published

- How to fill out 6-NDFL in 2021: official instructions

What you need to know

In a letter dated June 29, 2020 No. BS-4-11/10498, the Federal Tax Service of Russia reminded that when receiving wages, the date the taxpayer actually receives such income is the last day of the month for which he was accrued income for work duties performed in accordance with the employment agreement/contract (Clause 2 of Article 223 of the Tax Code of the Russian Federation).

When paying income in kind or receiving material benefits, the calculated amount of personal income tax is withheld from any income paid by the tax agent to an individual in cash . In this case, the withheld amount of personal income tax cannot exceed 50% of the income paid in cash.

As the Federal Tax Service notes, there are no .

How to set a 12 month period

The 12 consecutive months required to establish a person's tax status are not a calendar year from January 1 to December 31.

This period may begin in one tax period and continue in another (letters of the Ministry of Finance of Russia dated September 25, 2012 No. 03-04-06/6-289, dated May 31, 2012 No. 03-04-05/6-670 and etc.).

So, if the tax status is determined as of September 30, 2018, then the 12-month period begins on September 30, 2021, and ends on September 29, 2021, if on September 15, 2021, then the period begins on September 15, 2021 and ends on September 14 2018.

And during the calendar year, the employer must control the tax status of employees: when paying wages - on each accrual date - on the last day of the calendar month, which for this type of income is considered the moment of receipt, on the day of payment of income - for other types of income, for example, vacation pay .

Situation 1: recalculation of personal income tax due to the loss of an employee’s status as a tax resident of the Russian Federation

Let’s assume that an employee of an organization who is a tax resident of the Russian Federation received wages for January on January 31, 2019. On the same date, personal income tax is withheld and transferred. In February 2021, the employee lost his tax resident status, and when paying salaries for February, personal income tax was withheld at a rate of 30%, offset by the previously withheld tax amount.

These payments in section 2 of the calculation in form 6-NDFL for the 1st quarter of 2019 reflect:

- on line 100 - indicate 01/31/2019 (salary for January 2019);

- on line 110 – 01/31/2019;

- on line 120 – 02/01/2019;

- on lines 130 – 10,000;

- on lines 140 – 1,300.

And further:

- on line 100 – 02/28/2019 (salary for February 2019);

- on line 110 – 02/28/2019;

- on line 120 – 03/01/2019;

- on lines 130 – 10,000;

- on lines 140 – 4400 (taking into account paragraph 1 of Article 138 of the Labor Code of the Russian Federation).

According to para. 1 tbsp. 138 of the Labor Code of the Russian Federation, the total amount of all deductions for each salary payment cannot exceed 20% . And in cases provided for by federal laws - 50% of the salary due to the employee.

When deducting personal income tax from income that was previously calculated and erroneously not withheld from previously made payments, this limitation should be taken into account.

Also:

- on line 100 – 03/31/2019 (salary for March 2019);

- on line 110 – 04/01/2019;

- on line 120 – 04/02/2019;

- on lines 130 – 10,000;

- on lines 140 – 3300 (taking into account paragraph 1 of Article 138 of the Labor Code of the Russian Federation).

How to pay taxes for a foreigner on a patent

Quantity December 10, 2021

Foreigners

who work in Russia for an employer or individual often pay income tax in a special form - in the form of the cost of

a patent

. The amount of a patent for foreign citizens depends on the region where they work.

Income tax (NDFL) on the salary of a foreigner who works on the basis of a patent is calculated at the rate 13%

. The tax rate does not depend on his status - resident or non-resident.

Alien status affects deductions. Deductions are provided only to those who are residents of the Russian Federation.

As a general rule, tax residents are individuals who are actually in the Russian Federation for at least 183 calendar days over the next 12 consecutive months.

Reasons for reducing personal income tax

The employer can reduce personal income tax by fixed advance payments paid by the employee under the patent for the same year.

To do this, you need the following documents:

P/n Documents Description

| 1 | Employee's application for tax reduction and payment document for payment of a fixed payment | A sample application can be downloaded. |

| 2 | Notification from the Federal Tax Service confirming the employer’s right to reduce tax in relation to a specific migrant | It is necessary to send the form (KND 1110055) to the tax authority along with a copy of the employee’s application and a receipt for payment (from paragraph 1 of the current table) |

Notification is only available for the current year. Next year you need to apply for a new notification.

Example.

| For example, in November 2021, a foreigner got a job in the organization, whose patent was paid for six months - from October to March 2021 inclusive. The employer, based on a notice received on December 5, 2021, can reduce personal income tax on advances only for November and December 2021. To reduce tax in 2021, you need to receive a new notification from the Federal Tax Service. If in this situation the tax agent received a notification in January 2021, he has the right to reduce the amount of tax for November and December 2021 by payments paid by the migrant in 2021. |

How to reduce tax?

To reduce personal income tax you need to do the following.

- Collect

the necessary documents. - Calculate

the tax amount at a rate of 13%. At the same time, personal income tax deductions (standard, property and social) are provided only to residents. If an employee was a tax non-resident at the beginning of the year and then, for example, in June, became a resident, then deductions can be presented to him, and the tax can be recalculated from the beginning of the year. - In fact , reduce

personal income tax by fixed advance payments paid by the employee for the period of validity of the patent falling in the

current year

. The tax transferred to the budget from the beginning of the year before receiving the notification must be returned to the employee in the usual manner.

An example of calculating personal income tax when changing tax status.

| From January to May, a migrant on a patent received a salary of 20,000 rubles. per month. Personal income tax was withheld at a rate of 13%, the amount for 5 months was 13,000 rubles (20,000 rubles * 5 months * 13%) = 13,000 rubles. In June, the employee became a tax resident and claimed the standard deduction for a child - 1,400 rub. per month. Then you need to recalculate the tax from the beginning of the year, the personal income tax amount for June will be equal to 1,508 rubles (20,000 rubles - 1,400 rubles) * 6 months. * 13% – 13,000 rub. = 1,508 rub. |

If at the end of the year the amount of the fixed payment paid for this year turns out to be more than the amount of personal income tax withheld from the employee’s income for the year, then the uncredited balance of the advance payment is not carried over to the next year and is not returned to the individual.

How to fill out form 2-NDFL?

When filling out 2-NDFL

For a foreigner who works under a patent, you need to pay attention to the following.

In the field “ Payer status”

» you need to specify – 6.

In the section “ Total income and tax amounts”

» in the appropriate field you need to reflect the amount of fixed advance payments paid by the foreigner, by which the tax was reduced.

If payments under the patent exceeded the tax calculated on the foreigner’s income, in the field “ Amount of fixed advance payments”

"- enter the amount of calculated tax; in the fields "Amount of tax withheld", "Amount of tax transferred", "Amount of tax excessively withheld by the tax agent", "Amount of tax not withheld by the tax agent" - indicate zero.

Sample of filling out certificate 2-NDFL for a foreigner on a patent

How to fill out the 6-NDFL calculation?

Employers must include data on foreigners who work on the basis of a patent in the calculation using Form 6-NDFL

.

Line 040 reflects the amount of calculated tax; personal income tax from foreigners on a patent must be included in this amount.

Line 050 indicates the total amount of fixed advance payments for foreigners on a patent, which reduces personal income tax. This amount should not exceed the total amount of calculated tax.

In lines 100 and 130, fill in the date of actual receipt of income and the amount of income actually received.

In lines 110, 120 and 140, zeros are entered for such employees, since there is no tax to withhold and transfer.

An example of filling out a 6-NDFL calculation with information about a foreigner on a patent

Do foreigners with a patent have to submit Form 3-NDFL?

A foreign citizen working in Russia under an employment contract based on a patent needs to submit Form 3-NDFL if:

- he was employed by individuals

for

personal

,

household

and other similar needs and the amount of fixed advance payments paid for the year is less than the total amount of personal income tax; - patent revoked.

How to pay taxes for a foreigner on a patent

Foreigners

who work in Russia for an employer or individual often pay income tax in a special form - in the form of the cost of

a patent

. The amount of a patent for foreign citizens depends on the region where they work.

Income tax (NDFL) on the salary of a foreigner who works on the basis of a patent is calculated at the rate 13%

. The tax rate does not depend on his status - resident or non-resident.

Alien status affects deductions. Deductions are provided only to those who are residents of the Russian Federation.

As a general rule, tax residents are individuals who are actually in the Russian Federation for at least 183 calendar days over the next 12 consecutive months.

Situation 2: erroneous withholding of personal income tax at a rate of 13% from the salary of a non-resident employee

An employee of an organization who is not a tax resident of the Russian Federation was paid wages for January on January 31, 2019. On this date, personal income tax was erroneously withheld and transferred at a rate of 13%. In February 2021, having discovered an error, the accounting department recalculated the personal income tax amounts.

This payment in section 2 of form 6-NDFL for the 1st quarter of 2021 is reflected taking into account the recalculation made:

- on line 100 – 01/31/2019 (salary for January 2019);

- on line 110 – 01/31/2019;

- on line 120 – 02/01/2019;

- on lines 130 – 10,000;

- on lines 140 – 3000.

And:

- on line 100 – 02/28/2019 (salary for February 2019);

- on line 110 – 02/28/2019;

- on line 120 – 03/01/2019;

- on lines 130 – 10,000;

- on lines 140 – 3000.

Read also

31.07.2020

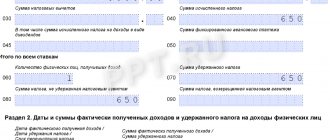

When to fill out line 090 in 6 personal income tax

Article current as of: December 2021

In line 090 of the report on form 6 personal income tax, the tax agent reflects the indicators of the mandatory income tax returned to employees. In what cases is this done and how to fill out this cell correctly.

How to fill out this line, depending on the taxation method. Cell number 090 is the last one in section 1 of the calculation in Form 6 of personal income tax. Like the entire section, it is filled in with a cumulative total from the beginning of the calendar year to the end of the reporting period. The procedure for filling out is the same as section 1.

There is no need to decipher the value indicated here based on income tax rates, so an equal indicator is included there. Unlike lines 010 - 050, it appears only once in the declaration.

The number indicated in the cell is an indicator reflecting the amount of personal income tax that the employer, represented by the tax agent, returned to the employee - the taxpayer.

- Mandatory notification to the employee of the fact of excess calculated tax. It will be an appendix to the report;

- the employee writes a written statement addressed to the employer with a request for the return of the mandatory income tax that was excessively withheld from him;

- if an individual changes status from non-resident to resident, then the refund is made not by the employer, but by the Federal Tax Service. The process occurs in the stated order.

Such explanations are described in this article.

How to correctly form an indicator for line 090

The employer, when filling out calculation 6 of personal income tax, takes into account the following nuances:

- When filling out line 090, the fee returned to employees from excessive collection for the reporting period is reflected;

- values returned in the previous reporting period are also taken into account;

- if the fee is returned by the Federal Tax Service, and not by the agent, then the latter does not reflect this indicator in the cell.

But, in a situation where the excess value is withheld by the employer, and the return is made by the Federal Tax Service, the following procedure is provided:

- The employee himself, and not the agent, must file a declaration for mandatory income tax;

- line 090 reflects information only about the tax agent, but not about the taxpayer.

On a note! If a worker wrote an application for a deduction, but the employer did not do this, then he withheld an excess amount of the fee from the employee. Then the return will be reflected in line 090 in 6 personal income tax.

For example, an employee has the right to a property deduction. I brought the relevant papers only in April. Cell 030 reflects the value of the deduction provided, but from the period in which the employer received documentary evidence.

Property deductions, as a general rule, are provided from the beginning of the year. However, the employer does not have any obligation to submit a “clarification” during the period from January to April. For the first time, the deduction will be reflected in the half-year report. There is no need to correct the calculation for the 1st quarter.

By the amount of tax returned by the tax agent to a specific employee, the employer reduces current payments to employees. But in cells 070 and 140 they indicate payroll tax.

It turns out that the withheld tax rate will be greater than the rate transferred to the budget. Control ratios will be separated. This is not considered an offense and no penalties may arise.

Example

For clarity, we give an example of filling.

Personal income tax has already been withheld from December wages on January 7th.

The calculation according to Form 6 personal income tax will look like this:

Conclusion

It is important to fill out the report correctly, including the value on line 090. Indicating incorrect indicators leads to penalties from the tax office.

Related publications

Line 90 in 6-NDFL is part of the generalizing section 1 of the reporting form.

Data should be entered into it by analogy with the indicators in other columns of this section - cumulatively for the tax period, that is, from the beginning of the year to the end of the reporting period (from January to the last day of the 1st quarter, half-year, 9-month interval, or year).

Line 090 is intended to highlight information on the amounts of income tax that were returned by the employer (tax agent) of an individual in the reporting period. The indicator is entered without kopecks, since the tax is calculated rounded to whole rubles.