Requirements for OS accounting registers

Registration of OS accounting registers occurs in compliance with uniform requirements for the creation of these documents. Accounting registers are consolidated forms for displaying accounting data, formed on the basis of information contained in primary documents (clause 19 of Order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n). As a rule, they are formed so that each of them reflects a group of homogeneous information that falls into a certain accounting account (for example, about fixed assets, about capital investments, about inventories or about calculations). The use of this document is mandatory for all persons conducting accounting in Russia (Article 2 of the Law of the Russian Federation “On Accounting” dated December 6, 2011 No. 402-FZ).

The fundamental requirements for registers are contained in Art. 10 of the same law:

- The data included in them must be shown in accounting in a timely manner (clause 1) without any distortion (clause 2).

- Information in registers is reflected in the double entry method, unless the possibility of using a different method is established by law (clause 3).

- If there are details required for this document (clause 4), the forms of the applied registers are developed and approved by the person in which the accounting is maintained (clause 5), attaching them to its accounting policies. An exception is public sector organizations that are required to use the forms approved for them by Order of the Ministry of Finance of Russia dated March 30, 2015 No. 52n.

- Registers can exist both on paper and in electronic form (clause 6). To transfer them at the request of other persons, the electronic document is transferred to paper (clause 7). At the same time, corrections in them that are not agreed upon with the person responsible for maintaining the registers are not allowed (clause 8).

- In its meaning, the register is equivalent to an accounting document (clause 9).

The required details for the register include:

- the name of the register and the person in which this register is used;

- the period for which the register is compiled or its start/end dates;

- principle of formation: chronological or systemic;

- quantitative accounting indicators indicating the units in which they are expressed;

- signatures of responsible persons containing their transcript and indication of position.

All these rules are directly related to OS accounting registers.

For more information about existing types of accounting registers and their application for certain accounting data, read the material “Accounting registers (forms, samples)”.

Accounting registers for accounting of fixed assets

¦ Application of a special coefficient ¦ Register of information about the object of basic ¦ ¦ ¦ ¦ funds ¦ +—-+—————————————-+——————————————+ ¦ 6. ¦ Initial (residual, basic) ¦ Register of information about the main object ¦ ¦ ¦ cost of the object ¦ funds (by calculation) ¦ +—-+—————————————-+——— ———————————+ ¦ 7. ¦ Term (useful, remaining until the ¦ Register of information about the object of the main ¦ ¦ ¦ expiration of the useful life ¦ funds (by calculation) ¦ ¦ ¦ use), which is applied ¦ ¦ ¦ ¦ when calculating depreciation (in months) ¦ ¦ +—-+——————————————-+——————————————+ ¦ 8. ¦ Amount depreciation for the object ¦ By calculation based on indicators ¦ ¦ ¦ ¦ lines 4, 5, 6 of the Register ¦ +—-+—————————————-+—————————— ————+ ¦ 9. ¦ Total amount of depreciation ¦ By calculation (sum of indicators ¦ ¦ ¦ ¦ line 8 separately for fixed assets, ¦ ¦ ¦ ¦ used and unused in ¦ ¦ ¦ ¦ production of goods (works, services)) ¦ ——+—————————————-+———————————————-

Source - Recommendations of the Ministry of Taxes and Taxes of the Russian Federation dated December 30, 2001

The influence of the accounting form on OS registers

The principles outlined above for the formation of accounting registers are valid for all persons engaged in accounting, but for some of them, namely for small enterprises, non-profit organizations and participants in the Skolkovo project, the possibility of maintaining records in simplified ways is acceptable (clause 4 of article 6 of the Russian Federation law dated 06.12.2011 No. 402-FZ).

Simplification of accounting can follow the following path (clause 4.1 of the information of the Ministry of Finance of Russia No. PZ-3/2015):

- Simplifying registers and reducing their number. Recommended forms of such registers are given in Appendices 2–11 to Order of the Ministry of Finance of the Russian Federation dated December 21, 1998 No. 64n.

- Refusal to use registers. In this case, they will be replaced by one document - a book of accounting facts of economic activity, the form of which is given in Appendix 1 to the order of the Ministry of Finance of the Russian Federation dated December 21, 1998 No. 64n. Micro-enterprises are given the opportunity to maintain this book without using the double entry method (clause 2.1 of the information of the Ministry of Finance of Russia No. PZ-3/2015).

In terms of fixed assets, the simplified register provides for combining in one document information about each fixed asset and the depreciation related to it.

Register of information about a fixed asset object

The register is intended to collect information about the availability and movement of the organization’s property, recognized for tax purposes as fixed assets as part of depreciable property.

The procedure for classifying property as depreciable is established by Article 256 of the Tax Code of the Russian Federation.

The composition of fixed assets is determined by paragraph 1 of Article 257 of the Tax Code of the Russian Federation.

According to the classification of the Ministry of Taxes and Taxes of Russia, the register belongs to the registers of the status of a tax accounting unit.

The procedure for register formation

The register is called from the menu item “Tax accounting - Registers of the status of a tax accounting unit - Register of information about a fixed asset object.”

The register is formed on the basis of the details of the directory “Fixed Assets” as well as data accumulated in accounts N05.01 “Initial cost of fixed assets” and N05.02 “Amount of accrued depreciation of fixed assets” (see Fig. 1).

Rice. 1 Procedure for register formation

Composition of register indicators

Object name.

The name of the fixed asset and its inventory number are indicated based on the relevant details of the directory “Fixed Assets”.

I. General information about the fixed asset item

Date of purchase.

The date the property was recognized as depreciable. Filled in with the value of the “Date of Acquisition” attribute in the “Fixed Assets” directory.

Initial cost.

Filled in with the value of the “Initial Cost” attribute in the “Fixed Assets” directory (the “Tax Accounting” tab).

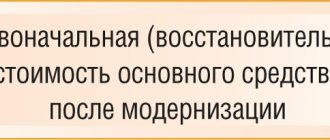

Basic cost of a fixed asset.

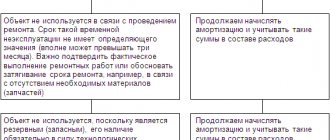

The base cost of a fixed asset is formed if the organization uses a non-linear method of calculating depreciation in the reporting month, when the residual value of the depreciable property reaches 20% of the original (replacement) cost (taking into account modernization, reconstruction, technical re-equipment, partial liquidation). The base cost is used to calculate depreciation from the next month until the end of its useful life.

The value of the indicator is the “Basic value” attribute of the “Fixed Assets” directory (the “Tax Accounting” tab).

Depreciation group.

The assignment of an object to a specific depreciation group is made in accordance with Article 258 of the Tax Code of the Russian Federation.

The value of the indicator is the “Depreciation group” detail in the “Fixed Assets” directory (the “Tax Accounting” tab).

Useful life. The value of the indicator represents the number of months of useful operation determined by the head of the organization within the time limits established for the depreciation group to which the property being put into operation belongs (clause 1 of Article 258 of the Tax Code of the Russian Federation). It is used to determine the amount of depreciation, the end date of depreciation accrual and the period for writing off the base cost of the object.

The value of the indicator is the attribute “Useful life (in months)” of the directory “Fixed Assets” (tab “Tax Accounting”).

Depreciation method.

The indicator reflects the method chosen by the organization for calculating depreciation in accordance with the standards established by Article 259 of the Tax Code. The method of calculating depreciation is established at the time the object is put into operation and is not subject to further change. Used to determine depreciation amounts.

The value of the indicator is determined by the “Method of depreciation calculation” in the reference book “Fixed assets” (tab “Tax accounting”).

The fixed asset item has been deregistered.

The date of deregistration of a fixed asset object is formed on the basis of documents confirming the loss of ownership of the fixed asset object in connection with its liquidation due to inappropriateness (impossibility) of use or sale.

The value of the indicator is the “Date of Disposal” attribute of the directory element “Fixed Assets”.

Grounds for deregistration.

The indicator is a document that reflects the disposal of a given fixed asset. This document, among other movements for tax accounting purposes, establishes the value of the “Disposal Date” attribute for this asset.

II. Belonging to fixed assets directly involved in the production of goods, works and services

The indicator is initially formed at the time of putting a fixed asset into operation (subject to other conditions for the property to be depreciable) on the basis of a document confirming the connection of its operation directly with the technological process of manufacturing and selling products (storing and selling goods, performing work, providing services) or servicing organization management apparatus.

It is used when assessing whether the amounts of depreciation accrued in the reporting month belong to direct or indirect expenses (clause 1 of Article 318 of the Tax Code).

Over time, the value of this indicator may change.

The register reflects information about changes in this indicator only for the period specified in the report dialog.

Transaction date.

The date of change in the attribute of an object’s belonging to fixed assets directly involved in the production of goods, works, and services.

Sign of affiliation (Yes / No).

It is determined depending on the account to which depreciation is calculated for tax accounting purposes (the “Fixed Assets” directory element, the “Tax Accounting” tab). “Yes” - if depreciation account N01.05 “Formation of direct costs for the production of goods (work, services) of the main production” or N01.06 “Formation of direct costs for the production of goods (work, services) of the main production subject to distribution.” In other cases, the sign of belonging is “No”.

III. Application of a special coefficient

It is formed when an object is put into operation in accordance with the provisions of paragraphs 7, 8, 9, 10 of Article 259 of the Tax Code of the Russian Federation on the basis of an order from the head of the organization on the accounting policy for tax purposes for a specific fixed asset item.

The size of the special (reducing) coefficient established in the order on accounting policy for tax purposes for the next tax period is reflected. Used to determine the amount of depreciation.

The register reflects information about changes in this indicator for the period specified in the report dialog.

Start date of application of the special coefficient. Date of installation and change of the special coefficient.

Coefficient.

In accordance with paragraph 10 of Article 259 of the Tax Code of the Russian Federation, the use of a special (reducing) coefficient is an element of accounting policy, and the organization has the right to change the decision to apply a special coefficient or change its value from the beginning of the next tax period.

The value of the indicator is the periodic detail “Special coefficient” of the directory element “Fixed assets” (tab “Tax accounting”).

OS data entering registers

Fixed assets are an accounting unit for which an incomparably greater amount of information is entered into accounting than for all other accounting units:

- method of admission;

- manufacturer data, date of issue and passport data;

- inventory number;

- the accounting group to which the product belongs;

- date of acceptance for accounting (commissioning);

- place of operation;

- financially responsible person;

- initial cost;

- depreciation group;

- depreciation calculation parameters;

- change in cost during modernization (reconstruction);

- revaluation results (ratio and resulting value);

- conservation data;

- information about movements between departments;

- information about renting or receiving;

- information on disposal indicating the residual value as of its date.

For most of this data, it may be necessary to create an appropriate accounting register. This requires broad capabilities in the formation of accounting registers related to the OS, allowing the creation of registers with an emphasis on certain parameters. To the greatest extent, these tasks are met by automated accounting, which, when entering complete information on a fixed asset and specifying it correctly, makes it possible to generate a wide variety of reports, including the required set of information for a certain period of time, thanks to the available selection function according to specified parameters.

Register for calculating depreciation

Tax accounting of depreciation expenses is not carried out in relation to fixed assets listed in clause 2 of Art.

256 of the Tax Code, as well as fixed assets not used for generating income, i.e. related to the non-banking sector. Tax accounting of depreciation is based mainly on the use of existing accounting registers with the addition of information necessary for tax accounting. Tax registers are maintained on the basis of primary documents used for accounting of fixed assets, i.e. cards for accounting of fixed assets. Data on the depreciation group (Article 258 of the Tax Code) and useful life (determined within the framework of depreciation groups), as well as the depreciation rate for tax accounting purposes, is added to the card for accounting for fixed assets. Card for accounting of fixed assets - the tax accounting register must contain the following mandatory details:

1.1 Card for accounting of fixed assets (tax register)

1 – inventory number according to accounting data; 2 – name of the object according to accounting data; 3 – book value according to accounting data; 4 – depreciation group (clause 2 of article 258) for an object is determined on the basis of Decree of the Government of the Russian Federation of January 1, 2002 No. 1 “On the Classification of fixed assets included in depreciation groups” 5 – useful life of the object (clause 1 of article 258); 6 – the service life of the previous owners is determined based on the acquired previously operated objects. The service life of the previous owners is determined by the purchasing departments based on the year of manufacture, commissioning of constructed facilities, etc. 7 – The useful life, taking into account the service life of the previous owners (clause 12 of Article 259), is determined as the difference between columns (5) and (6) or is established independently if such a life is greater than or equal to the useful life established in accordance with with NK; 8 – special coefficients are determined on the basis of clauses 7, 8 and 9 of Art. 259 Tax Code (conditions of an aggressive environment and increased shifts, leased property, cars and minibuses); 9 – the depreciation rate is determined by the formula 1/(5)*8*100% or 1/(7)*8*100% – for objects previously operated by other owners; 10 – determined on a monthly accrual basis according to depreciation rates for tax purposes (3)*(9)/12. As of 01.01.02, the amount of depreciation for tax purposes is determined taking into account the transitional provisions of Federal Law No. 110-FZ; (Tax base of the transition period) 11 – accounting data; 12 – is defined as the sum of (11) and (6) or (11) and (7) – for objects previously operated by other owners.

The main differences in the calculation of depreciation amounts for tax accounting of depreciable property from accounting of fixed assets

Tax accounting Tax Code of the Russian Federation (part two) dated 05.08. 2000 No. 117-FZ, chapter 25, article 256, clause 2

Basic OS registers

The main accounting registers of OS are:

- an inventory card that contains all information about an object or group of objects;

- turnover balance sheet.

It is these 2 documents that Order No. 52n of the Ministry of Finance of Russia dated March 30, 2015 obliges to use in public sector organizations to account for fixed assets. Also, based on the balance sheet principle, a simplified register for accounting for fixed assets and their depreciation (Form B-1) was created, given in Appendix 2 to Order No. 64n of the Ministry of Finance of the Russian Federation dated December 21, 1998.

Other persons using the usual form of accounting form balance sheets relating to fixed assets in 2 accounts: 01, which provides information about the presence and movement of fixed assets themselves, indicating their accounting value, and 02, which reflects data on accrued depreciation. As an inventory card, they, having the right to independently develop such a document, most often use those forms approved by Resolution of the State Statistics Committee of the Russian Federation dated January 21, 2003 No. 7:

- OS-6 - for one object;

- OS-6a - for a group of objects;

- OS-6b (inventory book) - for all objects of a division or the entire legal entity (IP).

Read more about these forms in the articles:

- “Unified form No. OS-6 - form and sample”;

- “Unified form No. OS-6a - form and sample”;

- “Unified form No. OS-6b - form and sample.”

Depreciation settings

The need for automatic calculation of depreciation in 1C 8.3 is specified:

- initially - in the document Acceptance for accounting of fixed assets;

- when the state of an object changes - in the document Changing the OS State .

If the acquisition of a fixed asset is documented in the document Receipt (act, invoice) type of operation Fixed assets, then depreciation will be calculated automatically in both accounting and NU, i.e. In this document, you cannot manually disable it.

Acceptance of fixed assets for accounting

The need to automatically calculate depreciation in accounting is regulated by the Calculate depreciation on the Accounting .

For NU, a similar checkbox is provided for Accrue depreciation on the Tax Accounting .

It is these checkboxes that affect the automatic calculation of depreciation at the end of the month.

Changing the OS state

There are cases when the accrual of depreciation needs to be stopped, for example, when mothballing an asset. Or, conversely, enable automatic depreciation calculation if for some reason it was not started when accepted for accounting.

For this purpose, 1C provides a document Changing the state of the OS in the section OS and intangible assets - Depreciation of OS - Parameters of depreciation of OS - button Create - Changing the state of OS.

Using the document flags, you can regulate the accrual and non-accrual of depreciation for specified fixed assets when closing the month, starting from the next month after the change in status.

In order for depreciation to begin or stop accruing at the end of the month, you must:

- select in which accounting the change occurs: in accounting;

- at NU;

- in BU and NU - if you enable both checkboxes.

- required - checkbox B affects the calculation of depreciation (wear and tear) so that the Accrue depreciation (wear and tear) ;

If the Affects the calculation of depreciation (depreciation) is not selected, then the change in depreciation calculation will not occur.

Monthly depreciation calculation

Monthly depreciation is calculated when performing the Month Closing procedure, the Depreciation and Depreciation of Fixed Assets operation in the Operations – Period Closing – Month Closing section.

This operation appears only if there is at least one fixed asset for which depreciation should be automatically calculated, starting from the next month after registration (change in the need for depreciation).

Other OS registers

In addition, a number of additional registers are convenient to use, making it possible to more clearly obtain any specific accounting information about the OS. For example, the 1C program provides for the formation of:

- a consolidated balance sheet, from which data for calculating property tax can be easily determined;

- analysis of the account, showing the turnover on it in relation to the corresponding accounts for the period;

- account cards, in which all transactions on the account are reflected in chronological order, indicating account correspondence;

- a report on transactions, which makes it possible to select transactions that have specified criteria;

- subconto analysis, which allows you to see in one report data related to one accounting unit, but accounted for in different accounting accounts;

- revolutions between subcontos, in which you can see the revolutions between the subcontos selected for its construction;

- subconto cards, formed similarly to an account card, but according to subconto;

- a calculation certificate showing the amount of accrued depreciation for each of the objects for the period;

- fixed asset depreciation sheet, which reflects all the components that affect the book value of each fixed asset.

Adjustment of depreciation of fixed assets in the program 1C: Accounting 8 rev 1.0

Not so long ago, following changes in legislation, changes occurred in 1C: Public Institution Accounting 8 rev.1.0, and several documents intended for adjusting depreciation parameters ceased to be used. What documents now need to be used instead of outdated ones?

So, the document “Changing depreciation parameters” is outdated (Fig. 1), and now the necessary information is entered in different documents, it all depends on its type. In order to change the procedure for paying off the cost, as well as the method of calculating depreciation and the useful life, the document “Changing the cost, depreciation of fixed assets and intangible assets” is used. The document contains several types of operations (Fig. 2).

Let's consider the first operation. A situation often arises when, for various reasons (an error in accepting a fixed asset for accounting, identifying errors during an inventory), it is determined that the useful life of a fixed asset is indicated incorrectly. The operation “Change depreciation (106, 109, 401.20 – 104)” allows you to adjust the useful life, as well as the amount of depreciation that changed when correcting OKOF. To correctly reflect transactions and generate primary accounting documents, it is necessary to take into account the following points (Fig. 3):

- Operation - Change of depreciation (106, 109, 401.20 – 104) specifies the details of the tabular part of the Fixed Assets tab.

- Primary document (Document type, Number, from) - data of the base document.

- KFO, NFA type - parameters for selecting objects in the tabular part of the document.

- In the Selection by hyperlink field, you can set additional conditions for selecting objects.

- Type of movement of non-financial assets - the value required to reflect the turnover of changes in the amount of depreciation in the form of regulated reporting 0503768 “Information on the movement of non-financial assets”. We recommend specifying the value Other change.

On the Fixed Assets tab, you should select fixed assets objects into the table (buttons , Selection or Fill in), the useful life of which you want to clarify.

- The object data will be indicated in substrings before the change: and after the change:.

- In the subline after the change: you should set the correct Useful Life and the Amount of Depreciation that should be accrued for the period in which the incorrect calculation was made.

In the example, the period and amount of depreciation have been changed. The transactions generated by the document are presented in Fig. 4

The new useful life, remaining useful life and residual value of the fixed asset as of the date of the document “Change in value, depreciation of fixed assets and intangible assets” are recorded in the information register “Calculation of depreciation of fixed assets” for further calculation of depreciation under the changed conditions (Fig. 5).

Changes in the useful life and calculation of depreciation of fixed assets will be reflected in the inventory card (Fig. 6), which can be printed:

- from the mode of viewing a directory element Fixed assets, intangible assets, legal acts;

- using processing Group printing of inventory cards (OS, intangible assets, legal acts - Reports on OS, intangible assets, legal acts).

Starting from the month of detection and correction of an error in accounting data, depreciation will be calculated according to the new specified parameters (Fig. 7).

The next operation “Change in value (101, 102 – 106, 401.10), depreciation (106, 109, 401.20 – 104)” (Fig. is used for additional depreciation calculation up to 100% of the book value for fixed assets (intangible assets), for which the method of calculating depreciation was changed to "100% upon commissioning". In the document, we must indicate the KFO (financial security code) on which the fixed asset is taken into account. In the tabular part, you can change the useful life, the procedure for repaying the cost, the method of calculating depreciation, the book value and the amount depreciation.

is used for additional depreciation calculation up to 100% of the book value for fixed assets (intangible assets), for which the method of calculating depreciation was changed to "100% upon commissioning". In the document, we must indicate the KFO (financial security code) on which the fixed asset is taken into account. In the tabular part, you can change the useful life, the procedure for repaying the cost, the method of calculating depreciation, the book value and the amount depreciation.

The operation “Change in value (401.10 – 101, 102), depreciation (104 – 101, 102)” (Fig. 9) is used to reflect the liquidation of part of an asset (intangible assets). We fill out the income account to which the amount from the liquidation will be allocated. We change the book value and then click the “Recalculate depreciation” button.

This document generates transactions for the debit of account 401.10 and the credit of account 101.36.

And one more operation in the document “Change in value (401.20 – 101, 102), depreciation (104 – 401.20)” (Fig. 10) is used to change the useful life of fixed assets with a linear depreciation method. In the account details we set the expense account 401.20 and indicate the new useful life. If you need to change the amount of accrued depreciation, according to the new period, then click the “Recalculate depreciation” button. To suspend and resume the calculation of depreciation, use the document “Suspending the calculation of depreciation.”

The document contains several operations: “Suspend depreciation”, “Resume depreciation”, “Preservation” and “Re-preservation” (Fig. 11). We choose the one we need.

We select the fixed asset in the tabular section and post the document. The details “OKOF code” and “Depreciation group” can be changed in the directory “Fixed assets, intangible assets, legal acts”. We go to the fixed asset card and change the details (Fig. 12).

The correctness of the operations performed can be checked by generating a standard “Depreciation Statement” report.

The article was prepared using materials from the 1C:ITS website

Results

OS accounting registers are formed according to the same rules as all other accounting registers, and have 2 main forms (inventory card and balance sheet), which exist in different versions.

For more convenient work with accounting information, other reports are also used, each of which allows you to effectively solve a specific problem. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

What is it used for?

The depreciation sheet for fixed assets is used to reduce the tax base for the reporting period, reflect the value of fixed assets for the period (month, year), as well as changes in the cost of equipment for the period.

In general, it is possible to divide the tasks regarding the OS for which the list is used into:

- disposal of fixed assets from the production process and turnover;

- modernization of means of production and costs incurred in connection with this;

- movement of the operating system during the production process;

- accrual of depreciation of funds over a period of time.

The indicators reflected in the statement must be of a cost and quantitative nature.

These parameters allow the company to have an idea of the amount of depreciation, the movement of fixed assets and allow them to adequately respond to changes.

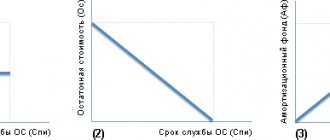

OS depreciation: calculation formula

For fixed assets, the following methods of calculating depreciation are provided (clause 18 of PBU 6/01):

- linear method;

- reducing balance method;

- method of writing off value by the sum of the numbers of years of useful life;

- method of writing off cost in proportion to the volume of products (works).

To determine the monthly amount of depreciation, let us present the calculation formulas for each of the indicated methods (clause 19 of PBU 6/01).

Linear method:

A = C / SPI / 12

where A is the amount of depreciation for the month;

C is the initial or replacement (in case of revaluation) cost of the fixed asset;

SPI – useful life of an asset in years.

Declining balance method:

A = O / SPI * K / 12

where A is the amount of depreciation for the month;

О – residual value of the fixed asset at the beginning of the year in which depreciation is calculated;

SPI – useful life of an asset in years;

K – coefficient established by the organization (not higher than 3).

Method of writing off cost by the sum of numbers of years of useful life: