Business

21.01.2020

5186

Return on equity is a ratio equal to the ratio of net income to the total cost of capital of an organization. This indicator is key for large investors, since it is the analysis of return on capital that allows one to assess how effectively money has been invested. The owners invest resources in the authorized capital and for this they regularly receive part of the enterprise’s profit, and return on capital allows one to calculate the income received per unit of invested funds. To calculate return on equity, information from financial statements (in particular, the balance sheet) is used.

Last news:

Remotely and free of charge. Priorbank launched new packages for business

How to invest rationally during the coronavirus crisis?

The concept of return on equity

So, in general terms, the return on equity indicator is denoted by the abbreviation ROE - Return On Equency. The coefficient clearly demonstrates what economic effect the company was able to achieve from investing its own financial resources in production.

To some, this indicator may seem identical to return on assets. This is not entirely true. The most important difference is that return on equity does not show the performance of all the assets of the enterprise, but only that part of them that is the property of the owners of the company.

Obviously, calculating the indicator makes sense only if the enterprise has its own capital. In other cases, the calculation will simply give negative values that are unsuitable for analysis.

The return on invested capital (ROIC) indicator takes into account the efficiency of using not only the organization’s own capital, but also borrowed funds.

Calculation formulas

Return on equity is determined using the firm's net income and equity data. By substituting profit values for different time intervals (month, quarter, year), you can see how efficiently equity capital worked during this period. Like any other value, return on equity is calculated as a percentage, which facilitates analysis and allows you to compare your values with those of competitors.

ROE = Net Profit / Equity * 100%

The value of net profit can be gleaned from the income statement, and equity - from the liability side of the balance sheet.

To calculate the coefficient for a period not equal to one year, but still see comparable annual figures, the formula will have to be somewhat complicated:

ROE = Net profit * (365 / Number of days in the calculation period) / ((Equity at the beginning of the period – Equity at the end of the period) / 2) * 100%

To conduct an even more thorough analysis of the ROE value, you can use the Dupont formula, where the calculated indicator is divided into three components, which allow you to more deeply understand the reasons for a particular trend:

ROE (Dupont Formula) = (Net Profit / Revenue) * (Assets / Firm's Equity) * (Revenue / Assets) = Net Profit Margin * Financial Leverage * Asset Turnover

Financial leverage is usually understood as the ratio of an organization's borrowed funds to its own.

To calculate return on debt capital, the formula should look like this:

ROIC = Net income / ( Equity + Long-term liabilities) * 100%

What is return on assets (ROA)?

In its broadest sense, ROA is the ultra-version of ROI. Return on assets tells you what percentage of each dollar invested in the business was returned to you as profit.

You take everything you use in your business to make a profit - any assets such as cash, fixtures, machinery, equipment, vehicles, inventory, etc. - and compare it to what you were doing during that period in terms of profit.

This ratio is more useful in some industries than others, in part because how much money your business invests in assets will depend on your industry:

- A manufacturing company may have a lot of capital tied up in plant and equipment.

- A service business may have expensive computer and information systems.

- Retailers need a lot of inventory.

But no matter your industry, ROA gives you insight into your overall profitability.

How to calculate return on assets?

It's a simple calculation that goes like this.

net profit / assets = return on assets

For simplicity, let's assume that your net income for the year is $248 and that your business assets are $5,193. Therefore you should calculate ROA as follows:

$248 / $5,193 = 4.8%

Naturally, you are wondering, is 4.8% good? This again depends on your industry.

For ROA, as for most financial indicators, there is no single correct value to strive for. There are ranges and expectations for different types of companies.

Banks tend to reduce ROA to around 1%. Technology companies have very few assets, so they often have high ROA. You need to compare your ratio with other companies in the same field to understand where you stand and how you could make better use of your assets.

Most profitability ratios, such as gross profit and net profit, are rarely too high, although you generally want them to be as high as possible. Return on assets, on the other hand, may be too high.

In fact, an ROA that is higher than the industry norm may indicate that the company is not updating its assets with an eye toward the future. The company may not be investing in new plant and equipment, which could be detrimental to its long-term prospects, no matter how good the ROA looks at the moment.

Another reason you might see a very high ROA is because of its balance sheet.

Take the infamous Enron. This energy company had a very high ROA. This was due to the fact that she created her own assets separately. Since its assets were thus taken off the balance sheet, the company appeared to have a higher return on assets and equity. This technique is called “denominator control.”

But "denominator management" is not always a scam. In fact, it's a smart way to think about how to run a business.

How can we reduce assets so that we can increase our ROA?

You're essentially figuring out how to do the same job at a lower cost. You may be able to restore it instead of throwing away money on new equipment. It may be a little slower or less efficient, but you will have lower assets.

Now let's look at return on equity.

Balance calculation

Like all other types of indicators, return on equity and invested capital ratios can be calculated using formulas from the balance sheet. In this case, the calculation formulas will look like this:

ROE = Line Value 2400 / Line Value 1300 * 100%,

ROIC = Row Value 2400 / Total Row Value 1300 and 1400 * 100%

Average statistical values by year for Russian enterprises

| Revenue amount | Values by year, rel. units | ||||||

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | |

| Microenterprises (revenue | -0.080 | 0.000 | -0.090 | -0.130 | 0.015 | -0.257 | -0.190 |

| Mini-enterprises (10 million rubles ≤ revenue | -0.015 | 0.031 | -0.049 | 0.028 | 0.082 | -0.005 | 0.017 |

| Small enterprises (RUB 120 million ≤ revenue | 0.049 | 0.077 | -0.013 | 0.043 | 0.098 | 0.037 | 0.063 |

| Medium-sized enterprises (RUB 800 million ≤ revenue | 0.091 | 0.068 | 0.003 | 0.060 | 0.119 | 0.081 | 0.030 |

| Large enterprises (revenue ≥ 2 billion rubles) | 0.123 | 0.091 | 0.079 | 0.110 | 0.130 | 0.095 | 0.130 |

| All organizations | 0.107 | 0.081 | 0.052 | 0.089 | 0.121 | 0.077 | 0.107 |

Table values are calculated based on Rosstat data

How to analyze indicators correctly

Analyzing return on equity values can be a major help in assessing potential income when investing in a particular business. The level of dividends and the investment attractiveness of the company as a whole largely depend on the value of the coefficient.

- If you compare the indicators of return on equity and assets, you can assess how competently the enterprise uses financial leverage, i.e. loans and credits. If the share of such borrowed funds in the volume of assets increases, the return on equity capital will also increase proportionally.

- Even if the ROE ratio shows steady growth, it is worth assessing the effectiveness of raising borrowed funds. If the effect of using the attracted capital prevails over the interest for their operation, the decision to attract borrowed capital is justified.

Undoubtedly, the higher the indicator value, the better. However, there may be pitfalls here too. Having carefully studied the DuPont formula, you can understand that a high value of the ratio may be a consequence of high financial leverage, when the share of borrowed capital significantly exceeds the share of the enterprise's own funds. In this case, a high ROE value is achieved at the expense of significant financial risks. How justified such a strategy is, each businessman must decide for himself.

So, if ROE or ROIC is declining compared to the previous period or competitors, this could mean:

- The amount of equity capital increases (for ROE).

- The total amount of debt obligations (for ROIC) is growing.

- The asset turnover rate is decreasing.

And on the contrary, if there is an increase in the indicators under consideration, this gives reason to talk about the following trends:

- Financial leverage increases.

- The organization's profits are growing.

Standard value:

Calculating the ratio for different periods helps to understand changes in profitability. Obviously, higher ratios are preferable because they demonstrate the relative increase in net profit generated for the same amount of capital. The trend of stable growth in the return on equity ratio means an increase in the company's ability to generate profit for owners. However, a decrease in equity (which could be caused, for example, by share repurchases) leads to an increase in the return on equity ratio. High debt levels also cause the ratio to increase, as it means the company is using debt capital instead of equity as a source of financing.

Example of coefficient calculation

Let's consider the procedure for calculating the ROE and ROIC coefficients for a conditional Russian enterprise. To assess efficiency and track dynamics, consider the company’s financial statements for the 4th quarter of 2021.

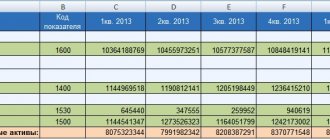

So, the values of line 1300 (total for the “Capital and Reserves” section) are:

1st quarter of 2021 - 102,345,294 rubles, 2nd quarter of 2021 - 115,035,682 rubles, 3rd quarter of 2021 - 121,729,554 rubles, 4th quarter of 2021 - 123,305,612 rubles.

The values of line 1400 (total for the “Long-term liabilities” section) are:

1st quarter of 2021 - 81,845,543 rubles, 2nd quarter of 2021 - 82,342,572 rubles, 3rd quarter of 2021 - 87,431,234 rubles, 4th quarter of 2016 - 65,309,517 rubles.

In line 2400 (Net profit / loss) we see the following indicators:

1st quarter of 2021 – -3,134,561 rubles, 2nd quarter of 2021 – 3,701,495 rubles, 3rd quarter of 2021 – 567,892 rubles, 4th quarter of 2016 – 8,823,515 rubles.

Using balance sheet calculation formulas, we determine the values of return on equity and employed capital:

ROE indicators:

ROE 2016-1 = -3,134,561 / 102,345,294 * 100% = -3.06% ROE 2016-2 = 3,701,495 / 115,035,682 * 100% = 3.22% ROE 2016-3 = 567,892 / 121,729,554 * 100% = 0.47% ROE 2016-4 = 8,823,515 / 123,305,612 * 100% = 7.15%

ROIC indicators:

ROIC 2016-1 = -3,134,561 / (102,345,294 + 81,845,543) * 100% = -1.70% ROIC 2016-2 = 3,701,495 / (115,035,682 + 82,342,572) * 100% = 1.88% ROIC 2016-3 = 567,892 / (121,729,554 + 87,431,234) * 100% = 0.27% ROIC 2016-4 = 8,823,515 / (123,305,612 + 65,309,517) * 100% = 4.68%

From the calculations made, a competent analyst will be able to glean a lot of valuable information, as well as draw a number of important conclusions:

- First of all, the negative ROE value in the first quarter is striking, which was a consequence of the lack of profit. However, further developments show that this situation turned out to be the exception rather than the rule and should not be considered as an obstacle to investment.

- Tracing the dynamics of changes in profitability parameters, one can see that the parameters take the highest values in the second and fourth quarters. Perhaps the company's main activities are seasonal. In this case, a potential investor should think about investing their funds during those periods when the potential income may be greatest. Company owners, on the contrary, should think about finding alternative sources of income during periods with the lowest (and even more so negative) profitability.

- The obtained profitability values seem to be relatively low, which suggests a rather low production efficiency. However, for the most honest comparison with its closest competitors, it is necessary to know exactly the direction of the company’s activities.

- The company is difficult to consider as an object for serious investment, since ROE and ROIC indicators for each period are less important than the average percentage for risk-free investments (for example, deposits in commercial banks).

For real enterprises, the calculation is made in a similar way. All the necessary information, as a rule, can be found on the official websites of organizations.

Normal value of efficiency of use of equity capital

Return On Equity shows owners how their invested funds work: how much net profit each unit of the insurance company brought. In this situation, the following statements can be made regarding the ROE indicator:

- The higher the coefficient, the higher the return on investment in business.

- If the calculation result turns out to be close to zero, then the feasibility of investing in enterprises is very doubtful.

Important point! Some domestic experts believe that in the Russian economy the standard ROE value is 20% (0.2). However, for analysis it is still better to compare the calculation results with industry averages.

The resulting profitability value is usually compared with the average profitability in the industry, the average interest rate in the economy, and then with the return on investments in stocks, bonds, bank deposits, etc.

Important point! An excessively high value of KRSK may indicate a decrease in the financial stability of the enterprise: the higher the return on investment, the greater the level of risk.

Comparison of indicators

To better understand the differences between the return on equity and attracted capital, their economic essence can be presented in the form of a small summary table:

| ROE | ROIC | |

| The main differences of the indicator | The company invests exclusively its own capital in production | Both own capital and attracted (borrowed) funds can be used for investment. |

| Optimal period for assessment | One year | One year |

| What industry is it used in? | At any | At any |

| What trend is favorable for the enterprise? | Indicator growth | Indicator growth |

| To whom it may be of interest | Owners of the enterprise | Owners and investors |

| Accuracy of the company's financial performance assessment | Less | More |