Funds turnover indicators

Turnover ratios are indicators of the business activity of an enterprise and allow one to assess the effectiveness of asset and capital management of the enterprise.

The basis for their calculation is revenue from sales of products or services, its ratio to the average annual size of assets, receivables and payables.

The turnover ratio is a financial ratio showing the intensity of use (turnover rate) of certain assets or liabilities.

Asset turnover

Asset turnover is a financial indicator of the degree of intensity of use by an organization of the entire set of available assets.

Asset turnover formula:

Asset turnover = Revenue / Average annual value of assets

Data on revenue can be obtained from the “Income Statement”, data on the value of assets can be obtained from the Balance Sheet (balance sheet).

To calculate the average annual value of assets, find their amount at the beginning and end of the year and divide by 2.

Based on the line numbers of the balance sheet and the Income Statement, the formula for the asset turnover ratio in Form 1 and Form 2 can be displayed as follows:

Asset turnover on balance sheet:

Asset turnover = (line 2110) /((line 1600 at the beginning of the year to + line 1600 at the end of the year) / 2)

Where:

Page 2110 - revenue from form 2;

Page 1600 - assets from Form 1.

There is no specific standard for turnover indicators, since they depend on the industry characteristics of the organization of production.

If the asset turnover ratio is 1.5, this means that for every ruble of assets there are 1.5 rubles. revenue.

When the indicator is less than 1, asset turnover is low, and the income received does not cover the costs of acquiring assets.

What is Return on Equity

Return on equity (ROE)

(also known as Return on Shareholders' Equity) is a financial ratio that shows the return on shareholders' investment in terms of accounting profit.

This accounting measurement method is similar to return on investment (ROI). This relative indicator of operational efficiency is expressed in the formula: Divide the net profit received for the period by the organization’s own capital.

The amount of net profit is taken for the financial year, excluding dividends paid on ordinary shares, but taking into account dividends paid on preferred shares (if any). Share capital is taken without taking into account preference shares.

The benefits of ROE ratio

The financial return indicator ROE is important for investors or business owners, since it can be used to understand how effectively the capital invested in the business was used, how effectively the company uses its assets to generate profit. This indicator characterizes the efficiency of using not the entire capital (or assets) of the organization, but only that part of it that belongs to the owners of the enterprise. However, Return on Equity is an unreliable measure for determining the value of a company, as it is believed that this indicator overestimates economic value. There are at least five factors: 1. Project duration. The longer it takes, the more inflated the indicators are. 2. Capitalization policy. The smaller the share of capitalized total investments, the greater the overstatement. 3. Depreciation rate. Uneven depreciation results in higher ROE. 4. The lag between investment costs and the return from them through cash inflows. The greater the time gap, the higher the degree of overestimation. 5. Growth rate of new investments. Fast-growing companies have lower Return on Equity.

Indicators of ROE values

The return on equity rate is approximately 10-12% for advanced economies. For inflationary economies the figure should be higher. Essentially, ROE is the rate at which shareholders' funds work for the company. Therefore, if ROE = 20%, this means that for every ruble invested by shareholders, the company generated 20 kopecks. net profit. Return on equity analysis is the main comparative criterion in relation to the alternative return that a shareholder could receive by investing his money in another business. For example, if securities bring a profit of 10% per annum, and the profitability of the business is only 5%, then the question of the advisability of further running such a business should be decided. Moreover, the standard value of ROE is usually assessed in the long term: the return on capital should not be lower than investments in financial instruments with a low degree of risk. It must be taken into account that the risks of doing business are much higher than investing in securities or a bank deposit. Thus, the prospects of a business are assessed taking into account rates on low-risk investments plus a risk premium (corporate, market, economic, political, etc.). We can conclude that the higher the return on equity, the better. But a high value of the indicator can also be associated with a high share of debt capital and a small share of equity capital, which negatively affects the financial stability of the organization. In total, calculating ROE makes sense only if the organization has equity capital (positive net assets). Otherwise, the calculation is of little use for analysis.

Turnover of working capital (assets)

Turnover of working capital (assets) shows how many times during the analyzed period the organization used the average available balance of working capital.

According to the balance sheet, current assets include: inventories, cash, short-term financial investments and short-term receivables, including VAT on purchased assets.

The indicator characterizes the share of working capital in the total assets of the organization and the efficiency of their management.

Working capital turnover formula:

Working capital turnover = Revenue / Average annual cost of current assets

In this case, current assets are taken as the average annual balance (i.e. the value at the beginning of the year plus the end of the year is divided by 2).

Working capital turnover on the balance sheet:

Working capital turnover = line 2110/(line 1200 at the beginning of the year + line 1200 at the end of the year)*0.5

Where:

Page 2110 — revenue from form No. 2;

Page 1200 - current assets from form No. 1.

The standard value of the coefficient has not been established.

The value of the indicator varies depending on the field of activity of the company.

The maximum values of the coefficient are for trading enterprises, and the minimum are for capital-intensive scientific enterprises. That is why it is customary to compare enterprises by industry, and not all together.

A higher value compared to competitors indicates intensive use of current assets.

Return on equity ratio. Calculation example for KAMAZ OJSC

| ROE for KAMAZ OJSC | We will calculate the return on equity ratio for the automobile corporation KAMAZ OJSC, which produces trucks, special equipment and buses. |

To assess return on equity, it is necessary to obtain the financial statements of the company under study. On the official website of the KAMAZ OJSC enterprise you can get financial data for the last 4 years. An alternative option is to use the InvestFunds service, which allows you to obtain data for several quarters and years. The figure below shows an example of importing balance data.

Calculation of the return on equity ratio for KAMAZ OJSC. Income Statement

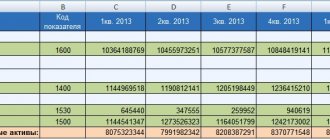

Calculation of the return on equity ratio for KAMAZ OJSC. Balance sheet

Let's calculate the coefficients for 4 years:

Return on equity ratio 2010 = -763/70069 = -0.01 (-1%) Return on equity ratio 2011 = 1788/78477 = 0.02 (2%) Return on equity ratio 2012 = 5761/77091 = 0.07 (7%) Return on equity ratio 2013 = 4456/80716 = 0.05 (5%)

There is an increase in the indicator from -1% to 5% over 4 years. However, investing in shares of this company is not advisable, because the profitability ratio is less than investing in alternative projects. For example, in 2013, the bank deposit rate was about 10%. It was more effective to invest available funds in a deposit than in KAMAZ OJSC (5%<10%).

Equity turnover

The equity capital turnover ratio is an indicator characterizing the speed of use of equity capital and reflects the efficiency of enterprise resource management.

The equity capital turnover indicator is used to assess various aspects of the functioning of an enterprise:

- The commercial aspect is the effectiveness of the sales system;

- Financial aspect - dependence on borrowed funds of the enterprise;

- The economic aspect is the intensity of use of equity capital.

The coefficient under consideration may be important for current and potential investors, partners, creditors, and also play an important role in terms of procedures for internal corporate assessment of management quality and business model analysis.

Equity turnover formula:

Working capital turnover = Revenue / Average annual cost of capital

Equity turnover on the balance sheet:

Equity turnover = line 2110 / 0.5 × (line 1300 at the beginning of the year + line 1300 at the end of the year)).

Where:

Page 2110 — revenue from form No. 2;

Page 1300 – line of the balance sheet (total line of section III “Capital and reserves”).

This indicator belongs to the group of business activity coefficients and there is no clearly accepted standard value for it.

A capital turnover ratio of 10 or higher indicates that the company's equity capital is being used effectively and that the company is generally doing well.

Low values of the indicator (less than 10) reflect that the enterprise's own capital is not used effectively, and there are possible problems in the business.