In 2020, insurance premium rates are traditionally set by the Government of the Russian Federation. Have they gone up? How did the coronavirus affect them: were they demoted? Let us explain these questions and provide a table with the new basic rates (tariffs) of insurance premiums in 2021.

Also see:

- How coronavirus affected insurance premiums: an overview of changes

- Deadlines for payment of insurance premiums in 2021: table

Change 2021

One of the main changes in insurance premiums from 2021 is the increased maximum base for the amount of payments in favor of the employee. Now the limits are set in the amount (Resolution of the Government of the Russian Federation dated November 6, 2019 No. 1407):

- RUB 1,292,000 – for contributions to compulsory pension insurance (was 1,150,000 rubles);

- 912,000 rub. – for contributions to VNiM (was 865,000 rubles).

The rates of insurance premiums calculated from salaries and other remunerations of employees and persons with whom civil contracts have been concluded have also been changed.

It should be noted that the Government of the Russian Federation increases the maximum base for contributions every year, but not for all types of contributions. And here’s what you can see in a single table in ConsultantPlus:

Data on the maximum value of the base for calculating insurance premiums for compulsory health insurance, compulsory health insurance, compulsory medical insurance from 2010 to 2021 inclusive.

Read completely.

simplified tax system with the object “income minus expenses”

Expenses can include benefits paid from employer funds.

According to the norms of Ch. 26.2 of the Tax Code of the Russian Federation, simplifiers have the right to reduce received income by the amount of temporary disability benefits paid to employees (that is, due to illness or injury) (Clause 1, Part 1, Article 5 of Law No. 255-FZ; Subclause 6, Clause 1, Article 346.16 , clause 2 of article 346.17 of the Tax Code of the Russian Federation). These benefits are covered from two sources - employer funds (for the first 3 days) and funds from the Social Insurance Fund (Part 1, clause 1, part 2, article 3 of Law No. 255-FZ). But initially, the employer pays the benefit in full himself (and then can offset it against the payment of insurance contributions to the Social Insurance Fund or ask for reimbursement from the Fund). And some simplistic people think they can expense the entire amount of sick pay paid to employees. However, it is not.

From authoritative sources Anatoly Nikolaevich Melnichenko, 1st class state councilor of the Russian Federation “In accordance with the Law on Compulsory Social Insurance in 2011, sick leave benefits are paid to employees (Part 2 of Article 3 of Law N 255-FZ): at the expense of the employer - for the first 3 days of temporary disability and at the expense of the Social Insurance Fund - starting from the fourth day of temporary disability. At the same time, the simplifier can only include in expenses the amount of benefits that he pays to employees at his own expense (that is, for 3 days of illness).”

Consequently, on the day of payment of benefits to employees (Subclause 1 of clause 2 of Article 346.17 of the Tax Code of the Russian Federation) in column 5 of the Book of Income and Expenses (Approved by Order of the Ministry of Finance of Russia dated December 31, 2008 N 154n) it is necessary to reflect only the amount of benefits for the first 3 days of illness. Benefits paid from the fourth day of illness and other social insurance benefits (for pregnancy and childbirth, child care, etc.) are not shown in the Book. After all, the source of their financing is funds from the Social Insurance Fund (Part 1, clause 1, part 2, article 3 of Law No. 255-FZ).

Contributions paid to the Social Insurance Fund are equal to the credited amount of benefits

Now let's talk about insurance contributions to the Social Insurance Fund. If such contributions were transferred to the Fund, then they would be included in expenses on the date of their payment (Subclause 7, clause 1, Article 346.16, clause 2, Article 346.17 of the Tax Code of the Russian Federation; clause 1 of the Letter of the Federal Tax Service of Russia dated May 12, 2010 N ShS- 17-3/210). In this case, contributions to the Fund are not transferred. The benefits paid will be counted towards their payment. However, in this case, you can still include insurance premiums as expenses.

From authoritative sources Melnichenko A.N., State Advisor of the Russian Federation, 1st class “There are no clarifications from the Ministry of Finance and the Federal Tax Service on this issue yet. At the same time, it should be noted that the amount of insurance contributions to be transferred by employers to the Social Insurance Fund is reduced by the amount of expenses incurred by them to pay insurance coverage to insured persons (including sick leave benefits) (Part 2 of Article 4.6 of Law No. 255-FZ; Part 2 of Article 15 of Law No. 212-FZ). That is, the indicated expenses, within the limits of the accrued amounts of contributions for the corresponding reporting (calculation) period, are essentially insurance contributions paid by employers to the Social Insurance Fund for this period. Consequently, they can be taken into account in expenses as paid contributions (Subclause 7, clause 1, Article 346.16 of the Tax Code of the Russian Federation). At the same time, it is advisable to reflect them in the Book of Income and Expenses on the last day of the reporting (tax) period (that is, on the last day of each quarter). This is explained by the fact that: - the amount of contributions paid in such a situation is determined by calculation; — calculation of contributions payable to the Social Insurance Fund and benefits offset against them is done quarterly and reflected in Form-4 of the Social Insurance Fund; — advance payments under the simplified tax system are also calculated quarterly.”

Then there are two possible options. Option 1. You owe FSS . If in some months the amount of sick leave paid does not exceed the amount of accrued contributions, then you need to transfer the difference to the Social Insurance Fund. It must be reflected in the Book of Income and Expenses as of the date of transfer of contributions. That is, in the end, you will still take into account all accrued contributions as expenses. Option 2. The FSS owes you . If the amount of sick leave paid each month is greater than the amount of accrued contributions, then nothing needs to be transferred to the Social Insurance Fund. In this case, you can ask for compensation from the Social Insurance Fund. In this case, the costs can include the entire accrued amount of insurance premiums. And it is better to reflect it in the Book of Income and Expenses on the last day of the quarter. And when you receive a refund from the Social Insurance Fund to your current account, it will not need to be included in your income. The Ministry of Finance and the tax service said that in this case the simplifier does not receive any economic benefit back in 2005 (Article 41 of the Tax Code of the Russian Federation; Letter of the Federal Tax Service of Russia dated June 15, 2005 N GI-6-22 / [email protected] ; Letters Ministry of Finance of Russia dated July 4, 2005 N 03-11-04/2/11, dated June 21, 2005 N 03-11-04/1/2). And as Anatoly Nikolaevich Melnichenko confirmed to us, this position is still relevant now.

Example. Determination of the amount of contributions to the Social Insurance Fund and benefits taken into account in expenses under the simplified tax system

Condition

The organization has 10 employees with a salary of 10,000 rubles. The amount of contributions to the Social Insurance Fund accrued for each month for all employees is 2900 rubles. (RUB 10,000 x 10 people x 2.9%). In every month of the six months, one employee in the organization was sick. All employees are entitled to 100% benefits. And every month, at the expense of the employer, 3 days of sickness were paid in the amount of 1000 rubles. The amounts of benefits to be paid from the Social Insurance Fund are shown in the table. From January to March, the amount of benefits paid to employees from the Social Insurance Fund exceeded the accrued amount of contributions. The organization decided not to ask for compensation from the Social Insurance Fund, but to count it towards the payment of insurance premiums.

Solution

We present in the table the procedure for accounting for insurance contributions to the Social Insurance Fund and paid sick leave in expenses.

Contributions for June in the amount of 2900 rubles. were listed in the Social Insurance Fund on July 14, 2011. This amount of contributions can be taken into account in expenses only in July.

Insurance premium rates for employers in 2020

Previously, the Tax Code of the Russian Federation stipulated that the aggregate tariff of 30%, at which the majority of insurers calculate contributions, would be in effect temporarily - from 2021 to 2021 (Article 426 of the Tax Code of the Russian Federation). And after the specified period, the tariff for compulsory health insurance contributions should have increased by 4% to 26%, and the total tariff, accordingly, from 30% to 34% (subclause 1, clause 2, article 425 of the Tax Code of the Russian Federation as amended before 01/01/2019). However, legislators changed their minds. And the indicated basic contribution rates have become permanent since 2021.

In this regard, in 2021, in general, the following contribution rates are applied (clause 2 of Article 425 of the Tax Code of the Russian Federation):

- for OPS - 22% within the maximum base value and 10% if it is exceeded;

- at VNiM – 2.9%;

- for compulsory medical insurance – 5.1%;

- for injuries – from 0.2% to 8.5%.

The law also establishes so-called increased insurance premium rates. They are paid by employers with harmful (difficult, dangerous) working conditions. Additional contribution rates tariffs for 2021 and what they depend on are available in ConsultantPlus:

Organizations that have jobs with the right to early retirement from clauses 1 - 18, part 1, art.

30 of Law N 400-FZ. Specific names of works are given in special lists. Read completely. Also see the table with tariffs in K+ here.

In connection with the coronavirus, from April 1, 2021, small and medium-sized businesses (SMEs) pay contributions at reduced rates for payments exceeding the minimum wage (Article 5 and Federal Law dated April 1, 2020 No. 102-FZ). Their rates are:

- for OPS – 10%;

- for compulsory medical insurance – 5%;

- at VNiM – 0%.

Accordingly, payments not exceeding 1 minimum wage per month are subject to contributions at regular rates.

KEEP IN MIND

Federal Law No. 172-FZ of 06/08/2020 for organizations and individual entrepreneurs affected by coronavirus canceled (reset to zero) insurance premiums for the 2nd quarter of 2020 - from payments to individuals accrued for April, May and June 2020. For more information, see “Features of payment of insurance premiums by organizations and individual entrepreneurs for the 2nd quarter of 2020.”

But the 2021 rate of insurance premiums for insurance against industrial accidents and occupational diseases is simply not specified in the law. The fact is that it depends on the class of professional risk according to OKVED. How to determine the contribution rate for injuries is described in ConsultantPlus:

The rate of contributions for accident insurance depends on the class of professional risk to which your main type of economic activity belongs (Article 21 of Law No. ... (see decision in full).

Contributions when combining preferential and regular activities

When simultaneously engaging in several types of work from the preferential list, the use of reduced contributions is allowed only if the total share of revenue from such work (services) is at least 70% of the annual income of the payer using the simplified tax system.

If the share of non-preferential types of production exceeds 30%, the right to preferential rates of SV is lost.

Deprivation of the right to apply a reduced rate of insurance premiums obliges entities on the simplified tax system to re-calculate contributions for the entire year in which the income threshold for activities from paragraph 8 was below 70 percent.

Example #1. Analysis of a practical situation

From January to July 2021, a company using the simplified tax system was engaged in the production of sports goods and the wholesale trade of women's clothing. The share of sporting goods production during this period was 71%. But in August, income from wholesale clothing increased sharply, which led to the fact that the share of income from sporting goods dropped to 65%.

From January to July 2021, in connection with the application of a preferential tariff on workers’ earnings, accrued in the amount of 498,012 rubles. Contributions to the pension fund were calculated in the amount of 99,602 rubles. 40 kopecks

How much and for what types of insurance should additional premiums be charged in connection with the transition to calculations at the regular rate?

In the described situation, the company will be required to recalculate accrued contributions from January to July and make additional accruals. The calculation result is summarized in the table below.

| New calculation of contributions from 01/01/2016, in rubles and kopecks | |||

| Pension Fund | health insurance | FSS | |

| amount of contributions for recalculation of total | for additional accrual | ||

| 498012 x 22%=109562.64 | 109562,64 – 99602,40 = 9960,24 | 498012 x 2.9% = 14442.35 | 498012 x 5.1% = 25398.61 |

Thus, for pension provision you will have to pay the difference amounting to 10% of the previously calculated contributions, but for the Social Insurance Fund and Compulsory Medical Insurance, recalculation contributions will need to be repaid in full.

After completing the new calculation, if you are deprived of the opportunity to use reduced contribution rates, you will need to submit adjusted RSV-1 forms for the first half of the current year.

To whom reduced rates on insurance premiums have been canceled since 2021

As you can see, the basic insurance premium rates for 2021 have not changed. But with reduced tariffs the situation is different.

From 2021, fewer companies can apply reduced contribution rates. Thus, the reduced tariffs for 3 categories :

- business entities and partnerships that practically apply or implement the results of intellectual activity, the exclusive rights to which belong to their founders or participants - budgetary or autonomous scientific institutions or budgetary or autonomous educational organizations of higher education;

- organizations and individual entrepreneurs that have entered into agreements on technology-innovation activities and make payments to employees working in technology-innovation special economic zones or industrial-production special economic zones;

- organizations and entrepreneurs who have entered into agreements on the conduct of tourism and recreational activities and who make payments to those employees who work in tourist and recreational special economic zones, united by a decision of the Government of the Russian Federation into a cluster.

Since 2021, these companies and individual entrepreneurs have been applying normal tariffs for insurance premiums (clause 2 of Article 425 of the Tax Code of the Russian Federation).

Who is allowed to apply reduced rates from 2021

Since 2021, new benefits on insurance premiums have come into force (subclause 16, clause 1 and subclause 7, clause 2, article 427 of the Tax Code of the Russian Federation).

Thus, organizations and entrepreneurs that have received the status of a participant in a special administrative region (Federal Law dated August 3, 2018 No. 291-FZ) that pay income to crew members of ships registered in the Russian Open Register can apply a 0% rate on all types of contributions until 2027 inclusive. ships by the specified payers, for the performance of labor duties of a member of the ship's crew.

In this case, zero rates can only be applied to payments to specified crew members. For the income of other employees, employers apply regular rates.

Many people believe that insurance premiums for payments to disabled people of groups 1, 2 and 3 are charged at reduced rates. Is this legal? There is a clear answer in ConsultantPlus:

From payments to disabled people of groups I – III, charge contributions to compulsory health insurance, compulsory medical insurance and VNIM according to... (read in full).

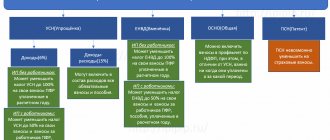

Insurance premiums for employees on the simplified tax system

Companies using the simplified tax system, as well as business entities working for OSNO, in the case of hired labor, pay insurance premiums from payments to insured persons working for them:

- for pensions and health insurance;

- for social insurance in case of illness and maternity leave, and accident insurance.

All contributions are transferred in full no later than the 15th day of the month according to the amounts accrued from payments to workers for the previous month.

In 2021, the contribution rates for pensions and health insurance correspond to the values from the table below.

| Taxable amount in 2021 in rubles | established contribution rate in % | |

| PS | health insurance | |

| up to 796,000 | 22 | 2,9 |

| over 796,000 | 10 | 0 |

For insurance of sick people and for maternity leave, the tariff will be 5.1% of the base when an individual earns up to 718,000 rubles. Social security contributions will not be assessed for earnings above this amount this year.

Some simplified payers running a business from list 8 of clause 58 of Article of Law No. 212-FZ have the right to contributions in a reduced amount. Currently, such entities pay only pension insurance in the amount of 20%, and for other insurances the rate is 0% until 2021 inclusive.

Reduced insurance premium rates in 2020: summary table (excluding coronavirus)

| Who can apply | Contribution rates, % | ||

| Pension Fund | FSS | Compulsory Medical Insurance Fund | |

| Non-profit companies on the simplified tax system with activities in the field of culture, healthcare, education, science | 20 | 0 | 0 |

| Charitable organizations on the simplified tax system | 20 | 0 | 0 |

| Businesses operating in the IT industry: software developers, testers, installers and sellers of computer programs | 8 | 2 | 4 |

| Employers of crew members of Russian ships | 0 | 0 | 0 |

| Skolkovo resident enterprises | 14 | 0 | 0 |

| Manufacturers of cartoons, video and audio products | 8 | 2 | 4 |

| Residents of the free economic zone in Crimea and Sevastopol | 6 | 1,5 | 0,1 |

| Enterprises operating in territories of rapid economic development | 6 | 1,5 | 0,1 |

| Residents of the port of Vladivostok | 6 | 1,5 | 0,1 |

| Residents of the free economic zone in the Kaliningrad region | 6 | 1,5 | 0,1 |

In 2021, many small and medium-sized businesses affected by coronavirus received the right to a reduced rate on insurance premiums. How to use it is explained in detail in ConsultantPlus:

But you need to take into account that the reduced tariffs do not apply to the entire amount of monthly payments to an individual, but only... (read the instructions in full).

Insurance premium rates for individual entrepreneurs in 2020

If an individual entrepreneur has employees, then the entrepreneur must accrue contributions from payments to them at the same rates as the organization. That is, as an insurer (subclause 1, clause 1, article 419 of the Tax Code of the Russian Federation). They are listed above.

As for contributions paid by individual entrepreneurs for themselves, interest rates are not needed to calculate fixed contributions. And if the entrepreneur’s income for the year exceeds 300,000 rubles, then, as before, he must pay additional contributions to compulsory pension insurance at the rate of 1% of the excess amount (subclause 1, clause 1, article 430 of the Tax Code of the Russian Federation).

For more information about the amounts of insurance premiums for individual entrepreneurs, read our article “Fixed insurance premiums for individual entrepreneurs “for themselves” in 2021: new amounts.”

| Payment | Amount for 2021, rub. | Payment deadline |

| Mandatory pension | 32 448 | 31.12.2020 |

| Mandatory medical | 8 426 | 31.12.2020 |

| Additional pension | 1% of income over 300,000 rubles, maximum – 259,584 rubles. | 07/01/2021 (for individuals affected by coronavirus - 11/02/2020) |

Most businessmen in Russia use a simplified taxation system. What insurance premium rates do individual entrepreneurs use on the simplified tax system? The current answer is in ConsultantPlus:

An individual entrepreneur using the simplified tax system must pay (clauses 1, 2, clause 1 of Article 419 of the Tax Code of the Russian Federation, Letters of the Ministry of Finance of Russia dated 02/06/2019 N 03-15-05/6911, dated 02/06/2018 N 03-15-05/ 6891)… (read in full).

KEEP IN MIND

Federal Law No. 172-FZ dated 06/08/2020 for individual entrepreneurs affected by coronavirus reduced the monthly fixed contributions to compulsory pension insurance (for themselves) by 1 minimum wage for the entire 2021 - from 32,448 rubles. up to 20,318 rubles. For more information, see “Features of payment of insurance premiums by organizations and individual entrepreneurs for the 2nd quarter of 2020.”

Read also

26.08.2020

Insurance premiums of the simplified tax system for individual entrepreneurs

Individual entrepreneurs without employees pay fixed insurance premiums, as well as contributions in the amount of 1% of the amount exceeding the amount of annual income of 300 thousand rubles. The simplified tax system for this category of taxpayers (individual entrepreneurs without employees) makes it possible to completely reduce the amount of the advance payment by the contributions actually transferred for themselves. For 2021, the size of the fixed part for individual entrepreneurs is 32385

rub. If in a year the total income from business activities exceeds 300,000 rubles, an additional 1% will be added to the excess amount. An entrepreneur has the right to choose when to transfer contributions to the funds. But the fixed part must be sent to the budget by December 31, and the portion exceeding the limit by April 1 of the next year (the deadline has been extended for 2021). When calculating the tax base of the simplified tax system and paying advance payments or taxes at the end of the year, he can reduce them by the entire amount of actually transferred contributions during the corresponding quarters.

Insurance premiums of the simplified tax system for individual entrepreneurs with employees are calculated and paid according to the same rules as described above. Those. For employees, the entrepreneur pays contributions monthly until the 15th, his own - until December 31 and April 1 (if the amount exceeds 300,000 rubles). As for reducing advance payments under the simplified tax system, an individual entrepreneur can deduct contributions that he paid during the quarter, both for himself and for employees, but no more than 50% of the amount to be transferred to the budget. Please note that insurance premiums paid after December 31 do not reduce the simplified tax system for the reporting period. They will be included in the next payment.

Insurance premiums of the simplified tax system are constantly changing, yes, they have been untied from the minimum wage, but they will still change - increase! This is what the law says, and this is written down for the coming years. However, there are many variables when calculating contributions; if salaries are tied to the minimum wage, then you will have to recalculate them - after all, the minimum wage has been constantly increasing recently; if a business has seasonal peaks in income, then this also needs to be taken into account correctly; you can also mention the good news of recent times - you can return paid contributions for the simplified tax system, income minus expenses for the last few years - after all, until recently, everyone paid 1% of income, without reducing for expenses. However, the courts sided with business and it is now possible to submit an application to the regulatory authorities. It is important not to get confused - contributions were paid to the Pension Fund before, and recently to the tax office. How to make sense of all this? Sitting on forums for hours? Calculate on a calculator? Usually you feel sorry for your time, and your strength, and... there is a way out! Both entrepreneurs and even accountants have been preferring to use web services for business for more than 8 years. We can say right away that there are very few quality ones! It’s probably not in vain that there are almost a million registrations - the reviews on the quality of work are very high, but it’s easier and better to try it yourself. Unlike conventional computer programs, web services can be used without installing software on a PC/laptop/tablet; you just need to create an account and use it. Fortunately, the web service gives you a month of work as a gift at the maximum rate - during this period you can try everything, measure everything and understand whether Elba’s power is enough for business or... more than enough! Of course, there are tariffs, both simple and complex, so you can choose, but what are the prices for human labor, what are the time costs, etc. for alternative ways to solve problems in business management - everyone knows very well (certainly well). Well, whether the comfort and peace of mind is worth the price of the service - everyone decides for himself, in addition to various bonuses that should be noted, the prices do not bite - from 1,500 rubles. for the quarter. Creating an account in Elba:

Try Elba 30 days free