Is a day trip a business trip?

A business trip is a trip by an employee in accordance with the order of the employer for any period of time for the purpose of performing an official assignment outside the permanent place of work (166 Labor Code of the Russian Federation). Business trips of employees are also regulated by the Regulation on Business Travel No. 749, hereinafter referred to as the Regulation. Both the Labor Code and the Regulations do not contain a minimum period for which an employer must send an employee on a business trip. From this we can conclude that if an employee goes on a trip in accordance with the order of the manager, carries out his instructions while on the trip, and this happens outside the place of work, then such a trip can be considered a business trip. It does not matter how many days it lasts, one or several (

One day business trip

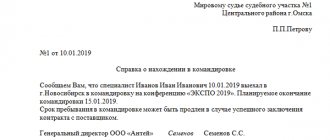

E. PETROV, Travzagot LLC It happens that the duration of a business trip is only one day. Registration appears

The norms of the Labor Code of the Russian Federation on business trips apply to all employers. To the extent that does not contradict the Labor Code of the Russian Federation, the Instruction of the Ministry of Finance of the USSR, the State Committee for Labor of the USSR, the All-Union Central Council of Trade Unions dated 04/07/88 No. 62 “On official business trips within the USSR” continues to apply. It establishes the maximum time an employee can spend on a business trip. 40 days, not counting travel time, and also provides for the possibility of sending employees on a business trip for one day (clauses 2 and 4 of the Instructions). The procedure for arranging a one-day business trip largely coincides with arranging a longer business trip. So, when sending an employee on a business trip, including a one-day trip, the employer issues an order. In this case, the unified form No. T-9 is used if one employee is sent on a business trip, or form No. T-9a if several employees are sent on a business trip (these forms were approved by Resolution of the State Statistics Committee of Russia dated January 5, 2004 No. 1). An official assignment for sending on a business trip and a report on its implementation are also drawn up (form No. 10a).

Let us remind you that the official assignment is signed by the head of the structural unit in which the seconded employee works. It is approved by the head of the organization or a person authorized by him and submitted to the personnel service for issuing an order (instruction) on sending him on a business trip. Upon returning from a business trip, the employee draws up a brief report on the work performed on the business trip. The report is agreed upon with the head of the structural unit in which the traveler is registered, and is submitted to the accounting department along with an advance report (form No. AO-14 approved by Resolution of the State Statistics Committee of Russia dated 01.08.01 No. 55).

It is important to note that, unlike a regular business trip, during a one-day travel certificate (unified form No. T-10), the employee may not be issued (clause 2 of the Instructions). In the logbook of employees going on business trips, a record is made of the employee being sent on a business trip. Compensation payments

During a one-day business trip, the organization must compensate the employee for travel expenses to and from the place of business travel, as well as the cost of transporting luggage if the employee requires special equipment to perform a job assignment.

The above-mentioned Instruction prescribes that when traveling on business to an area from where the business traveler has the opportunity to return daily to his place of permanent residence, daily allowances (allowances in lieu of daily allowances) are not paid (clause 15 of the Instructions). Moreover, the developers of the instructions apply this standard not only to one-day business trips. The question of whether an employee can return daily from a business trip to his place of permanent residence is decided in each specific case by the head of the organization. This takes into account the distance, transport conditions, the nature of the task being performed, as well as the need to create conditions for the employee to rest.

At first glance, this provision of the Instruction contradicts the norms of the Labor Code of the Russian Federation. The Labor Code of the Russian Federation does not provide for exceptions for compensation payments. However, if we turn to the definition of the concept of “daily allowance” given in the Labor Code of the Russian Federation - “additional expenses associated with living outside the place of permanent residence” - then everything falls into place. During a one-day business trip, the employee does not have living expenses, and even more so there will be no additional expenses associated with living.

However, as mentioned above, the procedure and amount of reimbursement of expenses associated with business trips are determined by a collective agreement or local regulations of the organization. Therefore, the collective agreement of the organization may provide for the payment of daily allowances for a one-day business trip.

The Ministry of Finance of Russia, referring to the mentioned paragraph 15 of the Instructions, believes that for a one-day business trip, daily allowances should not be paid (letters of the Ministry of Finance of Russia dated 03/29/99 No. 04-02-05/6, dated 01/12/2000 No. 04-04-06). If the organization nevertheless makes a daily allowance payment, then the Ministry of Finance proposes to take this amount into account in the employee’s total income when calculating personal income tax, and not include it in expenses that reduce income received when calculating income tax.

In this case, UST should not be accrued, since payments that are not attributable to expenses that reduce the tax base for corporate income tax in the current reporting (tax) period are not recognized as an object of UST taxation (clause 3 of Article 236 of the Tax Code of the Russian Federation).

The latter allows you not to charge insurance premiums for compulsory pension insurance, since the object of taxation of insurance premiums and the base for their calculation are the object of taxation and the tax base under the Unified Social Tax (Clause 2 of Article 10 of the Federal Law of December 15, 2001 No. 167-FZ “On compulsory pension insurance in the Russian Federation").

Employees of the territorial bodies of the Social Insurance Fund of the Russian Federation will most likely require payment of insurance premiums for compulsory social insurance against industrial accidents and occupational diseases.

Vladimir Fedorovich, I somehow didn’t understand this proposal...

In the List of payments for which insurance contributions are not accrued to the Social Insurance Fund of the Russian Federation (approved by Decree of the Government of the Russian Federation dated July 7, 1999 No. 765), namely, the payments given in this list do not accrue insurance contributions in accordance with the Accrual Rules, accounting and expenditure of funds for the implementation of compulsory social insurance against industrial accidents and occupational diseases (approved by Decree of the Government of the Russian Federation dated 02.03.2000 No. 184) mentions the amounts paid to employees to reimburse expenses, and other compensation (including allowances for compensation in return daily allowance) within the limits established by the legislation of the Russian Federation in connection with business trips (clause 10 of the List).

As mentioned above, officials believe that Russian legislation does not establish an employer’s obligation to compensate an employee’s expenses in the form of daily allowances for a one-day business trip.

Contributions for compulsory social insurance against industrial accidents and occupational diseases, made in accordance with the legislation of the Russian Federation, are included in other expenses associated with production and (or) sales (clause 45 of Article 264 of the Tax Code of the Russian Federation). However, in this case, the tax authorities will not allow them to be taken into account in expenses when calculating income tax. The argument is still the same: the payment of daily allowances for a one-day business trip is not provided for by the legislation of the Russian Federation.

In accounting, the amounts of daily and insurance contributions for compulsory social insurance against accidents will be taken into account when generating accounting profit. In tax accounting, these amounts are not included in expenses, which reduce income received when calculating income tax. However, they are not taken into account either in the reporting period or in subsequent ones. The resulting difference in expenses is recognized as constant (clause 4 of PBU 18/02 “Accounting for income tax calculations”; approved by order of the Ministry of Finance of Russia dated November 19, 2002 No. 114n). It must be reflected separately in analytical accounting. The product of the permanent difference that arose in the reporting period by the profit tax rate established by the legislation of the Russian Federation on taxes and fees and in force on the reporting date is recognized as a permanent tax liability (clause 7 of PBU 18/02). To reflect it in the accounting records, the following entry is made: Debit 99 subaccount “Permanent tax liability” Credit 68 subaccount “Calculations for income tax” . a permanent tax liability has been accrued.

Example

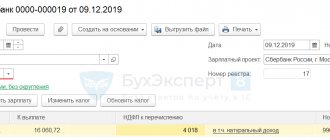

An organization registered in Moscow has separate divisions, including in Tula. A special section of the accounting policy on the procedure for document flow provides for the submission of the necessary documents for drawing up a report to the head office by the 18th day of the month following the end of the reporting period. Therefore, the accountant of the separate division in Tula was sent on July 18, 2005 on a one-day business trip to Moscow. The collective agreement provides for the payment of daily allowances for business trips in the amount of 300 rubles. However, there are no exceptions for one-day business trips.When sent on a business trip, an employee is given 600 rubles on account. Upon return, the employee draws up a business trip report, which is submitted to the accounting department with an advance report. Advance report in the amount of 600 rubles. (round trip fare - 300 rubles, daily allowance - 300 rubles) approved by the head of the branch. Tariff of insurance contributions for compulsory social insurance against accidents at work. 0.4%.

In accounting, business trip expenses, if all the requirements of tax authorities and FSS specialists of Russia are met, will be reflected as follows:

Debit 71 Credit 50 - 600 rub. . funds were issued for a business trip; Debit 26 Credit 71 - 600 rub. . business trip expenses are taken into account.

When making calculations for July 2005, there will be additionally:

- 39 rubles were withheld from the accountant's salary. (300 rubles x 13%) in the form of personal income tax;

- increased by 300 rubles. base for calculating insurance premiums for compulsory social insurance against accidents;

- a permanent tax liability was accrued in the amount of 72.29 rubles. ((300 rub. + 300 rub. x 0.4%) x 24%):

Debit 99 subaccount “Permanent tax liability” Credit 68 subaccount “Calculations for income tax” - 72.29 rubles. — a permanent tax liability has been accrued.

If, at the end of the working day, an employee decides to stay at the place of business trip to complete the work assignment, then he must also be paid for the cost of renting housing. But in this case, the business trip will not be considered one-day. And a travel certificate becomes a mandatory attribute. In this case, the employee is paid daily allowance. Therefore, if there is doubt that the employee will be able to complete the official task in one day, then it is better to issue a travel certificate.

Daily allowance for a business trip for one day

When an employee is sent on a business trip for two days or longer, he must pay not only for travel to and from his destination, but also for accommodation. In addition, the employee is paid a daily allowance, depending on the number of days of travel (168 Labor Code of the Russian Federation). As for daily allowances for one-day business trips, everything will depend on where exactly the employer sent the employee. There are business trips in Russia and abroad.

If an employee is sent across Russia on a business trip for one day, then the payment of daily allowances is not provided (Regulation). At the same time, the company itself has the right to decide whether to pay compensation to the employee instead of daily allowance or not (168 Labor Code of the Russian Federation). In this case, the employer should provide for such compensation in the organization’s local document. Such a document can be an employment or collective agreement. You can also arrange it in another way. For example, issue an order to pay the employee compensation for travel expenses instead of daily allowance. Both in the order and in the employment or collective agreement, the employer must specify the amount of such payments.

Payment of daily allowance for one day of business trip

What is a daily allowance?

Per diem is reimbursement of an employee’s expenses for housing outside their place of permanent residence. Such expenses are borne by everyone who travels on official business to an area located far from the main place of work.

As for business trips for one day, the legislation of the Russian Federation does not provide for daily allowances.

The concept of daily allowance during a business trip for 1 day does not exist. This is due to what the very concept of “daily allowance” implies. If a person leaves on a business trip in the evening of one day and returns in the evening of another day, this is considered a two-day business trip, for which the employer can assign the employee daily allowance in the amount established by law.

This amount will not be subject to income tax, and it can be given to your employee to reimburse his expenses during a business trip.

Maximum and minimum payout limits

The maximum amount is determined by the employer.

As for daily allowances, their amount is strictly regulated by law. The maximum amount of daily allowance that is not subject to personal income tax within the Russian Federation is 700 rubles; if a person travels abroad, then the maximum amount that is not taxed is 2,500 rubles.

If a person returns from a business trip on the same day on which he left, but he was abroad, then the maximum tax-free daily allowance is 50% of the usual amount - 1250 rubles.

Procedure for paying for a business trip for one day

When traveling for one day, the employee is entitled to the same types of payment as for multi-day trips. With the exception of daily allowances, as we have already discussed above, they are only valid for one-day trips abroad. When traveling for one day in Russia, daily allowances are not paid.

For one-day business trips, the employee is reimbursed for the following expenses:

- For travel;

- Other expenses that the employee incurred with the permission of the employer.

Such payments, as well as their amount and procedure for compensation, are determined in the collective agreement or local regulations of the company. Moreover, the amount of payments can be differentiated depending on what position the employee occupies. In other words, a one-day trip for an employee with a higher position may be paid higher than the same trip for an ordinary employee.

Important! In addition to these payments, the employee is paid the average salary for this day of travel (167 Labor Code of the Russian Federation).

Business trip 1 day: daily allowance

Based on clause 11 of the Regulations on Business Travel (Government Decree No. 749 of October 13, 2008), daily allowances are not paid for one-day trips around Russia. At the same time, the law does not prohibit giving employees certain amounts to reimburse some expenses in another area. Based on judicial practice, such payments should be considered as compensation necessary to cover expenses associated with the performance of official duties (see Determination of the RF Armed Forces dated 04/07/2017 No. 310 KG17-3888). In this case, they will not be included in wages, which means that insurance premiums and taxes will not be collected from them (see Letter of the Ministry of Finance dated October 2, 2017 No. 03-15-06/63950).

If an employee is sent to another state, then he must be given half (50%) of the required daily allowance (clause 20 of the Business Travel Regulations). Please note: if we are talking about state and municipal employees, then the standards are established in Government Decree No. 812 of December 26, 2005 or in regulations at the regional level. Private companies set their own daily allowance. But within the limits of 2,500 rubles, neither personal income tax nor insurance premiums may be withheld. Anything more is subject to taxation in accordance with the general procedure.

Does an employee need to return home from a business trip every day?

Whether or not to return home every day from a business trip, even if there is such an opportunity, is decided by the manager. Each specific case is considered separately, taking into account:

- Travel range;

- What are the transport conditions?

- Nature of the job assignment;

- Does the employee need rest?

If an employee, after completing a working day on a trip, decides to remain in the place of business trip, he must agree with the employer. If the manager agrees, then the employee will need to reimburse the costs of renting housing within the amounts determined by the collective agreement. However, such a business trip will no longer be considered a one-day trip.

Payments for business trips abroad

The employee will be reimbursed for all expenses.

Local acts on business trips indicate the amounts paid when traveling abroad. They may be more or less than the maximum amounts established by law.

When an employee is sent on a business trip, according to the law, he retains his job, his average salary, and also under the terms of internal regulations, the business traveler can be awarded a bonus for work during a business trip, in the evening or on weekends.

The employer is obliged in accordance with Article 168 of the Labor Code of the Russian Federation:

- reimburse all necessary expenses spent on travel;

- reimburse all expenses related to rental housing;

- reimburse those expenses that are associated with expenses not at the place of residence;

- not provided for by the parties, but those that were made with the permission of the employer.

These are the basic requirements of the law, and the amounts, time, duration and tasks can be established by an internal act of the employer.

In order to send a person on a business trip, it is necessary to issue an appropriate order or instruction, familiarize the employee with the duration of the business trip, the time of departure, as well as the purpose and tasks, which will also indicate the amounts for future costs associated with travel, business purchases, and rental housing. and daily payments.

Arranging a business trip for one day

The registration procedure for one-day tickets is the same as for multi-day tickets. Before the employee leaves, he must complete a work assignment. After this, an order is issued. If the company’s internal documents provide for the issuance of a travel certificate, the employee must issue it.

Important! For one-day business trips, a travel certificate is not required.

In the time sheet, the employer records the fact of the employee’s trip. Upon return, the employee provides a report on the work he has done in the official assignment, and also fills out an advance report. Documents confirming expenses are attached to the advance report. These can be checks, receipts, contracts, transport documents, etc.

Personal income tax and insurance premiums on daily allowances

If an employee sent on a one-day business trip confirms all his expenses, then personal income tax does not need to be withheld from the funds that were paid to him. If the employee is unable to confirm his expenses, then the payment is exempt from taxation only up to 700 rubles for business trips in Russia and 2,500 rubles for business trips abroad (Letter of the Ministry of Finance of Russia No. 03-04-07/6189 dated March 26, 2013).

As the Ministry of Finance explains, those funds that are paid for a one-day business trip are not per diem. They represent other expenses associated with business travel. They are also included in expenses subject to exemption from personal income tax, due to the fact that these payments are directly related to the employee’s performance of his official duties.

However, if the employee cannot provide documentary evidence of the costs of such payments, then they are recognized as income. In this case, personal income tax is assessed only on the amount paid in excess of 700 rubles when traveling within the Russian Federation and in excess of 2,500 rubles when traveling abroad. As for insurance premiums, the logic is the same. Those payments that the employee can confirm are not subject to contributions, since they represent compensation for expenses incurred by the employee.