How to correctly register the founder's contribution to the cash desk

When a company is created, an authorized capital is formed; it can be its own or borrowed. Authorized capital (hereinafter referred to as the Criminal Code) is a reserve of a company that is created by the founders by contributing to it cash, material assets, property, and intangible rights expressed in monetary terms. It is necessary for the company to start functioning. Legislative acts of the Russian Federation regulate the amount (size) of the authorized capital. Let's look in this article at which account the authorized capital is accounted for, how to register the founder's contribution to the cash desk, and let's look at the accounting entries when registering this operation.

- Payment of wages to employees;

- Rent, for example, office or warehouse space, vehicle rental;

- Acquisition of OS objects that will be used in the future for work, for example, computer equipment, objects in a production workshop, etc.;

- Payment for purchases, transfer of funds to suppliers;

- Other.

In what cases may it be necessary to deposit cash at the cash desk?

Reasons for depositing cash, in addition to current production activities, may include:

- The need to replenish the working capital of the enterprise;

- Business expansion;

- To carry out current expenses, for example, pay wages, purchase materials, etc.;

- Pay taxes.

It is wrong to receive cash from business owners as revenue. In this case, the company will have to pay tax

. The purpose of depositing funds can be:

- Material aid. It is formalized by a gift deed or a separate agreement. The purpose of providing financial assistance may be to increase working capital, net assets, and repay losses.

- Replenishment of authorized capital. In this case, it will be necessary to make changes to the company's Articles of Association and register them accordingly.

- Applying for a loan from the founder. A loan agreement is drawn up; it can be interest-bearing or interest-free. It is more common to draw up an interest-free loan agreement; this will allow you to avoid paying taxes on the money received.

- Contribution to company property. Allowed if such a possibility is provided for in the Charter. Introduced on the basis of a written order of the founder; if there are several owners, then there must be minutes of the meeting of the founders.

- Payment for goods or work. In this case, contracts for the supply of goods, certificates of work performed or services provided must be attached.

Since 2014, a simplified procedure for maintaining cash discipline has been in effect for individual entrepreneurs. Their responsibilities include only the preparation of salary slips.

When accepting cash, you must remember that there is a restriction on making cash payments between legal entities and individual entrepreneurs. The maximum amount of payment in cash under one contract is 100 thousand rubles.

Procedure for accepting money

To deposit money into the cash register correctly, you must fill out a cash receipt order

. It consists of two parts - the document itself and the receipt. The order is filled out and signed by an accountant or other authorized person. Enter the serial number, date of operation, amount (in numbers and in words), purpose of payment. If the PKO contains a link to documents, they must be attached to the order, for example, a certificate of completion of work, a loan agreement, etc.

After accepting the money, the authorized person puts his signature on the PKO and a stamp indicating the completion of the transaction. The receipt is handed over to the depositor, the document is filed in the documents of the day, and a corresponding entry is made in the cash book.

Important! The date of the PKO and the date of receipt of money at the cash desk must coincide, otherwise the document is considered invalid.

If the actual amount of funds differs from the amount specified in the order, the cashier offers to add additional funds

(if there are not enough) or gives change (if there is a surplus). When there is not enough money, but the depositor refuses to deposit the funds, the PKO is crossed out, the documents are transferred to an authorized person to draw up a new PKO with the actual amount posted, or the money is fully returned to the depositor and the transaction is cancelled.

Accounting entries for contributions to the authorized capital

To obtain a license, you need to pay more than half of the authorized capital; 4 months are given to repay the remaining part. The exception is for joint stock companies; they are given 3 months to pay more than 50% of the authorized capital and a year to pay the rest. A joint stock company that has not paid 50% of the authorized capital does not have the right to enter into transactions not related to its establishment, and the decisions of shareholders have no legal force.

First, let’s define what a current account is intended for. It is created by legal entities for the purpose of conducting monetary transactions with other companies and individuals, allowing them to withdraw and store money obtained from cash surpluses. The company itself determines the limit of money stored at the cash register and is obliged to transfer the excess to the current account. The exceptions are paydays, non-working days and holidays.

Loan from the founder: postings

A situation may arise when the organization’s own funds are not enough to make capital investments or finance current expenses. One option for raising funds is to ask the founder for help. His assistance can be either free of charge or provided with a refund. We will tell you how to take into account a loan from the founder in our consultation.

In order to understand in which account to account for the loan from the founder, it is necessary to answer the question about the term of the loan. After all, if a loan is provided for a period of up to 12 months inclusive, then it must be taken into account in account 66 “Settlements for short-term loans and borrowings.” And if the loan term exceeds 12 months - on account 67 “Settlements for long-term loans and borrowings”.

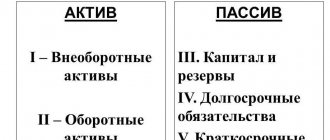

Accounting accounts 80 and 75

Authorized capital is the initial amount of funds (start-up capital) that the founders are willing to invest to ensure the activities of the enterprise. When registering an organization with the relevant authorities, constituent documents are drawn up, which include the cost of the authorized capital.

First of all, with its help, start-up capital is formed for the subsequent commercial activities of the enterprise. It consists of contributions from the founders, which can be either in the form of tangible property or in cash. Each founder has his own certain share in the capital, depending on its size, he will subsequently receive the corresponding profit from the commercial activities of the enterprise (dividends). The company is responsible for its obligations within the framework of this capital, so for creditors this is a kind of guarantee of satisfaction of their interests.

How can a founder deposit money into an LLC current account?

Info

A situation is possible when the money came from the founder. However, the founder can simultaneously be an employee of the organization. There are several options for qualifying the receipt of money from him, depending on the paperwork:

- payment of a share in the authorized capital;

- depositing money of the organization by an accountable person into its account;

- making a contribution to the company's property;

- transfer as a loan or for free use;

- loan repayment;

- payment for purchased goods, works, services;

- payment for a third party.

Due to inattention when preparing documents, a controversial situation may arise later. Thus, in one of the cases considered by the Moscow City Court, a former member of an LLC tried to return the money that he deposited into the company’s account. The claim was denied.

Formation of authorized capital in 1C 8

- Contribution of fixed assets. For example, the founder decided to repay the debt on the authorized capital in the form of equipment that can be immediately put into operation. In this case, two entries will be generated: Dt 08 – Kt 75.01 (repayment of debt on the authorized capital);

- Dt 01 – Kt 08 (commissioning of equipment).

More to read: Filling out the book of work records and inserts

Please note that if the debt on the authorized capital is repaid not in money, an assessment of this property must be carried out. The founders have the right to produce it themselves if the cost does not exceed 20,000 rubles. Otherwise, an external appraiser must be involved.

Is it possible to spend authorized capital?

The LLC manages the amount of its authorized capital at its own discretion: pays rent, utilities, buys raw materials, and so on. There are no restrictions. The minimum authorized capital of 10,000 rubles does not mean that there must always be at least 10,000 rubles in the account or cash register.

The main thing is that, starting from the second financial year, the organization has at least 10,000 rubles of assets on its balance sheet.

Example. When you deposit the authorized capital, 10,000 rubles will go into the liability side of the balance sheet in the line “Authorized capital” and 10,000 rubles will go into “Cash and cash equivalents”. You can use this money to buy raw materials, then the amount will move from cash to the “Inventories” line. At the same time, the equality of assets and liabilities is maintained.

Cash contribution to the cash desk from the founder of the transaction

Provisions of the Tax Code.

Further, according to paragraph 1 of Article 85 of the Tax Code, the SRS includes all types of income of the taxpayer. Article 96 of the Tax Code determines that the cost of any property, including work and services received by a taxpayer free of charge, is his income. The cost of property received free of charge, including works and services, is determined in accordance with IFRS and the requirements of legislation on accounting and financial reporting.

Normative base.

It may be noted that in paragraph 2 of Article 13 of the Law “On Accounting and Financial Reporting” it is defined that income is an increase in economic benefits during the reporting period in the form of an influx or increase in assets or a decrease in liabilities that lead to an increase in capital other than the increase associated with contributions from persons participating in the capital. And also, paragraph 1 of Article 13 of the Law “On Accounting and Financial Reporting” establishes that an obligation is an existing obligation of an individual entrepreneur or organization arising from past events, the settlement of which will lead to the disposal of resources containing economic benefits.

Cash funds of the founder and reflection in the financial statements

Attention

In accounting, reflect all this with the following entries: Debit 50 (51) Credit 91-1 - reflects the gratuitous receipt of money from the participant (founder, shareholder); Debit 91-1 Credit 99 – profit for the year is reflected; Debit 99 Credit 84 – reflects net profit at the end of the year; Debit 84 Credit 82 – deductions were made to the reserve fund (capital) according to the standards approved by the charter. This conclusion follows from the Instructions for the chart of accounts (accounts 84, 82). If, after increasing the reserve capital (fund), its value exceeds the restrictions established in the organization’s charter, amend the charter.

All this follows from paragraph 7 of PBU 9/99, paragraph 1 of Article 35 and Article 12 of the Law of December 26, 1995 No. 208-FZ, paragraph 1 of Article 30, paragraph 4 of Article 12 of the Law of February 8, 1998 No. 14-FZ , Instructions for the chart of accounts (accounts 84, 99) and is confirmed in the letter of the Ministry of Finance of Russia dated August 23, 2002 No. 04-02-06/3/60. Covering a loss If money is received from a participant to cover a loss generated at the end of the reporting year, do not use account 91.

As a rule, the decision of participants, including founders or shareholders, to provide financial assistance to cover losses is made after the end of the reporting year, but before the approval of the annual financial statements.

Such a decision is recognized as an event after the reporting date.

It is worth opening a subaccount for it “Funds of participants aimed at repaying losses.” The receipt of financial assistance to cover the loss generated at the end of the reporting year should be reflected in accounting entries. 1.

Settlements with founders (account 75)

The obligations and rights of individual LLC participants also apply to legal entities, but there are some restrictions. According to the law, local government bodies and state bodies have the right to be the founders of an LLC, unless this is prohibited by law of the Russian Federation.

In general, the number of LLC founders should not be more than 50 people. They can be citizens who have reached the age of majority and are legally capable; Persons with limited legal capacity also have the opportunity to engage in business, but only with the consent of the trustee. The participants of the LLC are not liable for its obligations, but bear the risk of losses that are associated with the activities of the Company and are within the value of the shares that belong to them, according to the authorized capital of the LLC.

Civil relations

As follows from Art.

27 of the Federal Law of 02/08/1998 N 14-FZ “On Limited Liability Companies” (hereinafter referred to as Law N 14-FZ), company participants are obliged, if provided for by the company’s charter, by decision of the general meeting of company participants to make contributions to the company’s property. Such an obligation of the company's participants may be provided for by its charter when the company is founded or by introducing amendments to the company's charter by decision of the general meeting of the company's participants, adopted by them unanimously. Contributions to the company's property are made in money, unless otherwise provided by the company's charter or a decision of the general meeting of company participants. Contributions to the company's property do not change the size and nominal value of the shares of company participants in the authorized capital of the company (clauses 1, 3, 4 of Article 27 of Law No. 14-FZ).