An essential element of the contractual policy of many organizations is the replacement of supply contracts with intermediary transactions (commission, commission, agency agreement). Many good articles have been written on this topic, but the number of questions practitioners have and the number of mistakes made does not decrease. These types of contracts have a number of features determined by the Civil Code of the Russian Federation. The specifics of such agreements affect the accounting and taxation procedures for the transactions that comprise them. The proposed article by M.L. is devoted to the consideration of the specifics of accounting for these contracts. Pyatova, Doctor of Economics, St. Petersburg State University.

The current civil legislation distinguishes three types of intermediary transactions - commission agreements, assignments and agency agreements.

The listed transactions formalize the representation by one person of the interests of another through the conclusion of agreements with third parties and other legal actions.

Article 990 of the Civil Code of the Russian Federation defines the commission agreement

as an agreement under which “one party (the commission agent) undertakes, on behalf of the other party (the principal), for a fee, to carry out one or more transactions on its own behalf, but at the expense of the principal.”

As follows from this definition, when executing a contract, transactions are made on behalf of the commission agent. This is the main distinguishing feature of a commission agreement. When performing an assigned transaction, the commission agent acts as a completely independent person.

According to Article 990 of the Civil Code of the Russian Federation, in transactions made by a commission agent with third parties, it is the commission agent who acquires rights and becomes obligated, although the principal was named in the transaction or entered into direct relations with the third party for its execution. On the other hand, third parties have obligations towards the commission agent and acquire rights in relation to him.

Article 971 of the Civil Code of the Russian Federation defines the contract of agency

as an agreement under which one party (the attorney) undertakes to perform certain legal actions on behalf and at the expense of the other party (the principal).

Here, as in the commission agreement, the attorney is entrusted with performing certain legal actions of interest to the principal. However, in contrast to the commission agent, the attorney, fulfilling the obligations under the agency agreement, performs legal actions on behalf of the principal. According to Article 971 of the Civil Code of the Russian Federation, “the rights and obligations under a transaction completed by an attorney arise directly from the principal.” On the other hand, third parties in transactions carried out by the attorney at the expense of the principal are obligated in relation to the latter and acquire rights in relation to him.

According to Article 1005 of the Civil Code of the Russian Federation, under an agency agreement

one party (agent) undertakes, for a fee, to perform legal and other actions on behalf of the other party (principal) on its own behalf, but at the expense of the principal or on behalf and at the expense of the principal.

The design of an agency agreement in Russian civil law pursues the goal of legal formalization of relations in which the intermediary (representative) carries out both transactions and other legal actions, as well as actual actions that do not entail legal consequences. For example, an organization acting as an agent may take on the task of selling other people's goods, which will imply not only concluding sales and purchase agreements, but also conducting an advertising campaign and other activities to study and develop the market. In such situations, it is impossible for the parties to the contract to make do with one of the traditional structures of an order, commission or contract. It is necessary to conclude either several different but closely interrelated agreements between the same entities, or a complex mixed (complex) agreement. Concluding an agency agreement can significantly simplify this situation.

According to paragraph 1 of Article 1005 of the Civil Code of the Russian Federation, in a transaction concluded by an agent with a third party on his own behalf and at the expense of the principal, the agent acquires rights and becomes obligated, even if the principal was named in the transaction or entered into direct relations with the third party for the execution of the transaction. In a transaction concluded by an agent with a third party on behalf and at the expense of the principal, the rights and obligations arise directly from the principal.

Although an agency agreement is an independent business agreement that synthesizes commission and mandate agreements, specific transactions, specific business transactions performed by the agent for the principal fit within the framework of commission and mandate agreements. According to Article 1011 of the Civil Code of the Russian Federation, the rules provided for in Chapter 49 “Assignment” or Chapter 51 “Commission” of the Civil Code of the Russian Federation are applied to relations arising from an agency agreement, depending on whether the agent acts under the terms of this agreement on behalf of the principal or on his own behalf , if these rules do not contradict the essence of the agency agreement or special regulations of the Civil Code of the Russian Federation on agency.

Thus, we can highlight the following feature of commission agreements, commissions and agency agreements, which determines both the taxation scheme for transactions under them and the accounting procedure for business transactions carried out within the framework of these agreements: the property with which transactions are carried out (in relation to which purchase transactions are concluded - sale, contract, etc.) does not belong to the intermediary (commission agent, attorney, agent) by right of ownership.

Is an agency agreement without remuneration possible?

The essential terms of an agency agreement are its subject matter (legal and actual actions performed by the agent on its own behalf or on behalf of the principal, who in any case finances their execution) and other conditions, the need for approval of which is stated by at least one of the counterparties. The transaction price is not significant and may not be specified in the document (Article 1006 of the Civil Code). However, this does not mean that the law allows no remuneration to be paid to the agent at all.

The courts have repeatedly indicated that the rule on compensation for an agency agreement is imperative and cannot be changed by agreement of the parties (for example, the FAS of the Volga District in its resolution of May 24, 2013 in case No. A55-6675/2012).

Several more conclusions can be drawn from judicial practice:

- The principal is not released from the obligation to pay remuneration under an agency agreement even if he:

- independently carried out the actions that are the subject of the transaction, while the agent did not refuse to perform them (resolution of the Federal Antimonopoly Service of the West Siberian District (WSO) dated June 22, 2010 in case No. A45-20150/2009);

- did not issue a power of attorney to the contractor in violation of the terms of the agreement, but the agent still carried out the actions that are the subject of the transaction (resolution of the Federal Antimonopoly Service ZSO dated August 19, 2010 in case No. A03-14308/2009);

Accounting for the purchase of goods for the principal, principal or principal

A commission agent, attorney or agent can not only sell the goods of the principal, principal, or principal, but also acquire any valuables for the latter.

In this case, the process of actual receipt of goods to the consignor, principal or principal can be organized in one of the two most commonly used ways:

- the goods arrive at the warehouse of the commission agent, attorney or agent and are subsequently transferred by him to the principal or principal;

- the recipient of the goods is directly the consignor, principal or principal.

In the first case, the receipt of goods and its subsequent transfer to the consignor, principal or principal are reflected in account 004 “Goods accepted for commission” or 002 “Inventory assets accepted for safekeeping.”

According to paragraph 6 of PBU 5/01 “Accounting for inventories”, approved by order of the Ministry of Finance of Russia dated 06/09/2001 No. 44n, fees paid to the intermediary organization through which inventories were acquired are included in the actual costs of acquiring inventories. Consequently, in the accounting of the principal, principal or principal, the amount of remuneration paid to the commission agent, attorney or agent is included in the cost of the purchased goods.

How is the agent's remuneration determined under an agency agreement, and what influences its value?

In accordance with Art. 1006 of the Civil Code, the amount of remuneration under an agency agreement is established by agreement of the parties, and if they have not specified a condition on the price, by the general rule for determining it. In accordance with paragraph 4 of Art. 424 of the Civil Code, the price determined by the compensation agreement is considered equal to that charged in similar circumstances for similar goods, work or services.

The parties are advised not to ignore the condition of the transaction price, since failure to resolve this issue may lead, for example, to the following:

- The transaction price, determined after the agent has performed the actions assigned to him, may differ significantly from the amount that each party expected.

- The contract may be recognized as not concluded. For example, when an agent, guided by paragraph 54 of the resolution of the Plenum of the Supreme Court No. 6, Supreme Arbitration Court No. 8 of July 1, 1996, cannot prove that there were similar circumstances that could be taken as a basis for determining the price. Or when, on the basis of an agency agreement concluded according to the instruction model, legal services are provided (Part 4 of Article 25 of the Law “On Advocacy ..." dated May 31, 2002 No. 63-FZ).

In any case, the parties should take into account that:

- The size of the fee may depend on:

- from the amount of expenses incurred by the agent (Resolution of the Presidium of the Supreme Arbitration Court dated May 18, 2010 No. 17795/09);

- from the effect following the actions taken (resolution of the Federal Antimonopoly Service of the North-Western District dated April 12, 2010 in case No. A42-1861/2009);

Payment of remuneration in cash or non-cash funds

When agreeing on the terms of the agent's remuneration, issues of not only its magnitude, but also its form are raised. Typically, cash is used. Cash payments can be made in cash or non-cash form.

- Cash payments

The use of cash payments between persons engaged in business activities is an exception to the general rule. Clause 6 of Directive No. 3073-U dated October 7, 2013 sets the maximum permissible limit for such calculations. For one transaction, it is equal to 100 thousand rubles, and if the transaction price is determined in foreign currency, then the equivalent of this amount is taken into account, calculated at the official exchange rate on the day of payment.

IMPORTANT! Exceeding the established limit for cash payments entails a fine in accordance with Part 1 of Art. 15.1 Code of Administrative Offences. In this regard, it is not recommended to agree on a condition for payment of remuneration in cash if the principal is obliged to pay an amount exceeding 100 thousand rubles.

- Cashless payments

Taking into account Art. 862 of the Civil Code, the agent and the principal have the right to choose any of the forms of non-cash payments: checks, letters of credit, collection, payment orders, etc.

In addition to indicating the chosen form of transfer of funds, the contract must stipulate payment details (or the condition that they will be communicated separately in written notice, by issuing an invoice or otherwise), as well as the form of payment documents. The list of details and contents of settlement documents are established by the Bank of Russia (see Regulations on the rules for making money transfers, approved by the Central Bank on June 19, 2012 No. 383-P).

Accounting with a commission agent, attorney or agent

The lack of ownership rights of the commission agent, attorney or agent to the property involved in the transactions is also important for the purposes of accounting for transactions under the agreements in question. According to paragraph 2 of Article 8 of the Federal Law “On Accounting”, the organization’s own property and property that does not belong to it by right of ownership are subject to separate reflection in accounting. In the Chart of Accounts for accounting the financial and economic activities of organizations, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n, special off-balance sheet accounts are allocated to account for property actually owned by the organization, but not owned by it by right of ownership.

From the system of off-balance sheet accounts, only one account - 004 “Goods accepted on commission” is specifically intended for accounting for intermediary transactions. According to the Instructions for using the chart of accounts, account 004 “Goods accepted on commission” is intended to summarize information on the availability and movement of goods accepted on commission in accordance with the contract. There are no special accounts for accounting for goods received into possession under mandate agreements and agency agreements, respectively, by an attorney and an agent in the system of off-balance sheet accounts of the chart of accounts. For these purposes, in the organization’s working chart of accounts, you can use either account 004 or account 002 “Inventory assets accepted for safekeeping.”

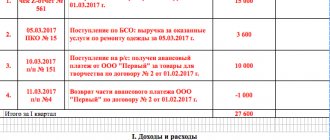

Example

Wholesale trade organization A enters into an agreement with organization B for the sale of a consignment of goods, in which A acts as a commission agent. In accordance with the terms of the contract, the goods must be sold for 354,000 rubles (including VAT - 18%). The amount of remuneration A is 10% of the selling price of goods.

Let us reflect the receipt and sale of goods in the accounting records of organization A.

Debit 004 “Goods accepted for commission” - reflects the receipt of a consignment of goods from organization B - 354,000 rubles Debit 62 “Settlements with buyers and customers” Credit 90 “Sales” subaccount “Revenue” - 35,400 rubles Debit 62 “Settlements with buyers and customers » Credit 76 “Settlements with various debtors and creditors” - 318,600 rubles - the sale of goods to customers is reflected; Credit 004 “Goods accepted for commission” - sold goods are written off - 354,000 rubles Debit 90 “Sales” sub-account “Value Added Tax” Credit 68 “Calculations for taxes and fees” sub-account “Value Added Tax” - debt to the budget for VAT is accrued from turnover for the sale of services for the sale of goods - 5,400 rubles Debit 51 “Settlements” Credit 62 “Settlements with buyers and customers” - goods paid for by buyers - 354,000 rubles Debit 76 “Settlements with various debtors and creditors” Credit 51 “Settlements” - funds are transferred to the principal - 318,600 rubles.

Payment in kind

Guided by Art. 421 of the Civil Code on freedom of contract, the parties may establish another form of payment - a non-monetary representation, which can be expressed, for example:

- in the issuance of a bill of exchange by the principal (see, for example, resolution of the Federal Antimonopoly Service of the Moscow District dated May 6, 2011 No. KA-A41/3588-11);

- in the counter provision of goods, performance of work or provision of services.

In this case, the counterparties need to expand the agreement by including rules related to the supply agreement, contract or paid provision of services, depending on the type of consideration. Thus, when transferring goods, delivery standards will be used.

The agency agreement will ultimately become mixed, and its subject matter will be:

| № | The subject of a mixed agreement, if the counter-provision is... | ||

| Product | Job | Service | |

| 1 | Transfer by the principal of goods as compensation (indicating its name and quantity) | Execution by the principal, within a specified period or terms, of work of a certain content and volume, which should lead to an agreed result | Provision of services by the principal in accordance with the list and scope of actions agreed upon by the parties |

| 2 | Legal and other actions performed by the agent on his own behalf or on behalf of the customer, but always at his expense | ||

Agent expenses

The agent's remuneration is a value that, as a general rule, does not include the agent's expenses for the performance of his duties under the contract concluded with the principal (we must not forget that he acts at the expense of the other party). Activities to execute an order, like any other, may be accompanied by payment for goods, works, and services of third parties. But we must distinguish:

— the agent’s costs for ensuring his current activities (staff salaries, office equipment, rental of premises and transport);

— expenses aimed only at the execution of the agency agreement (payment for the production of advertising materials, advertising time in the media, services and work of third parties, etc.).

From the above examples it is clear that the classification of costs is not strict. From the principal’s point of view, there is a risk that the agent will charge an inflated amount of expenses. It should be noted that even with the commission type of agency agreement, Art. 1001 of the Civil Code of the Russian Federation is not applied subsidiarily, since direct regulation is provided for in clause 2 of Art. 1008 of the Civil Code of the Russian Federation. Evidence is attached to the report, and proven expenses must be compensated.

There are ways to avoid disagreements about the appropriateness of expenses:

- provide for preliminary approval by the principal of the estimate (plan) of the agent's expenses and payment by the principal of expenses strictly according to the estimate, without exceeding it or with an agreed percentage of excess (no more than 5%, for example);

- indicate in the contract that expenses are compensated only for the agent’s reports accepted by the principal without comments (in this case, the dispute is postponed to the time of acceptance of the report).

In order to correctly reflect the transactions performed, it is necessary to indicate in the contract that the evidence of expenses attached to the report (Article 1008 of the Civil Code of the Russian Federation) must comply with the agreed forms of primary accounting documents.

If a claim is made for the recovery of costs, it should be taken into account that the court will consider it as separate and independent from the claim for the recovery of remuneration.

How is payment made under an agency agreement, and what are the consequences of non-payment?

The procedure for transferring remuneration under an agency agreement is established similarly to the price condition - by agreement of the counterparties, and in the absence of a special clause about this - under Art. 1006 Civil Code. In accordance with it, the principal pays for the agent’s services within 7 calendar days from the moment the contractor submits a report on the actions performed.

NOTE: the clause on the submission of a report by the agent is not significant in determining whether the obligation to pay has arisen. The Federal Antimonopoly Service of the North-Western District, in a resolution dated November 9, 2010 in case No. A56-30147/2008, indicated that remuneration can be recovered when the agent performs assigned actions, even if he has not submitted a report.

Violation by the principal of the obligation to pay remuneration to the counterparty may entail the imposition of such liability measures on him as compensation for losses and (or) penalties (depending on the specific terms of the contract), as well as payment of interest for the use of other people's funds.

The parties have the right to provide for a condition on full or partial payment of remuneration before the agent performs actions under the transaction. When agreeing on rules for prepayment or advance payment, counterparties are advised to determine the amount of such payments, the timing and procedure for making them. If the prepayment is partial, then it is additionally required to determine the payment procedure and the amount of the remaining remuneration.

If the parties agree on a prepayment condition and the principal does not fulfill his obligation to make it, then the agent, guided by Art. 328 of the Civil Code, has the right to suspend the implementation of legal and other actions entrusted to him.