An agency agreement under the simplified taxation system (abbreviated as STS) is an agreement between the principal and the agent, in which the difference between income and expenses allows the agent to transfer part of the functional responsibilities associated with the purchase and sale of various goods.

Despite the simplicity of the procedure (which is only possible with a simplified system), mediation operations are possible with special knowledge. Let's take a closer look at contracts of this type.

Agency agreement under simplified tax system 6% Income

Agency agreements are not only convenient documentation that allows you to consolidate the agreement between the principal and the agent. In most cases, especially recently, agency agreements are a convincing document in various proceedings (including litigation). That is why you should remember the importance of understanding the rules and regulations for drawing up such agreements. One of the most common contracts involved in proceedings are contracts with a simplified tax system of 6%.

The subject of such agency agreements (as well as other types of agreements) is the relationship between the agent and third parties, and the interests that the agent represents completely coincide with the interests of the principal. That is why, in the income and expense books, when signing an agency agreement with a simplified tax system of 6%, you should reflect only the amount of remuneration (agent's fee). This amount should be the difference between the amount that is paid by the buyer and the amount that should be transferred to the principal.

Requirements regarding these procedures are specified in detail in letter of the Ministry of Finance of Russia (dated April 18, 2013) No. 03-1111. According to paragraph 1 of Article 346 of the Tax Code of Russia, income that arises as a result of the transaction must be reflected in tax accounting on the following date:

- actual receipt of funds (as shown in the bank account);

- transfer of property into ownership (in addition to property, there may be work, services, property rights, etc.).

- repaying the debt to the taxpayer in any other way.

This is the case if the agent receives payment in advance, before the report is approved by the principal.

- If the agreement states that funds must be transferred after the agreement is concluded, and it is virtually impossible to determine the amount of remuneration, then according to the letter from the Ministry of Finance of Russia, all funds must be included in income, which will be taken into account when determining the tax base for simplified tax 6%.

- If orders for intermediary services continue, the agent, like the agency as a whole, can make changes to the amount of income that will be transferred to the principal (except for the deducted amount of fees). Such a right is regulated by a letter from the Ministry of Finance dated September 30 (letter No. 03-1106).

Such rules make it possible to avoid situations in which the customer pays the agent for intermediary services before the amount of his fee can be determined accurately.

Filling out KUDIR under the simplified tax system

Provision of motor transport services under an agency agreement, agent customer on the basis of executor usn

When determining the profit of an individual entrepreneur on a “simplified basis”, he must rely on the provisions of articles two hundred and forty-nine and two hundred and fiftieth of the Tax Code. In turn, this means that the entire amount received during the provision of services by the agent will not be included in the single tax base.

For example, the agency agreement states that the agent himself pays for an advertising campaign with personal money, after which this amount is billed to reimburse the principals. These funds will also serve as income.

It should be noted that the agents themselves do not have the right to recognize the costs of advertising the product of their principals as part of the costs that are taken into account when actually calculating the amount of the single tax.

In the accounting of agents, revenue that is directly related to intermediary services is usually considered profit from ordinary operations (clause 5 of the Accounting Regulations PBU 9/99 - Order of the Ministry of Finance of the Russian Federation dated May 6, 1999 No. 32n)

Accounting requirements are the same for all organizations and individual entrepreneurs. These rules are established by law and are mandatory when conducting any transactions related to the sale of a product or service.

This also applies to transactions carried out through intermediaries (agents), but the methods of conducting tax or accounting when selling services or goods with the signing of agency agreements have some peculiarities.

The remuneration transferred to the agent by the principal must be posted to one of the following accounts:

- 90 “Sales” (applies to ordinary forms of activity);

- 91 “Other income and expenses.”

The amount received from the customer to the agent for services cannot be included in expenses, therefore, they are not taken into account. It is possible to take into account only money transferred by the principal to the agent’s account as remuneration for services received.

What is the procedure for document flow between the parties in this situation?

What is the procedure for accounting and tax accounting of cash receipts from customers for the principal and the agent? Everything received by the Agent under the agency agreement is the property of the Principal (Article 974 and paragraph 1 of Article 996 of the Civil Code of the Russian Federation, Art.

Civil legal aspects Since in the situation under consideration, under the terms of the contract, the agent acts on his own behalf, the rules provided for in Chapter 51 of the Civil Code of the Russian Federation for a commission agreement are also applicable to such intermediary relations (Art.

1011 of the Civil Code of the Russian Federation). When implementing intermediary services on the territory of the Russian Federation, subject to VAT, by organizations that are VAT payers, the VAT tax base is determined as the amount of income received by them in the form of intermediary remuneration (clause

Accounting and taxation with an agent-firm using the simplified tax system

The money that the principal transferred to pay for the goods or services is not your income. Therefore, tax must be paid only on agency fees.

To determine the date of receipt of income, carefully read the clause of the contract that establishes the agency fee and the procedure for its payment.

Go How to get a disabled person's sign for a car if your grandmother is disabled

The amount of remuneration is fixed in the contract.

The principal can transfer the remuneration in a separate amount or you yourself will withhold it from the money received for the purchase. Take the remuneration into account in the simplified tax system on the day you receive money from the principal.

For example, you place an advertisement for a principal on Yandex.Direct. He transfers you 15,000 rubles, of which you keep your reward - 5,000 rubles - yourself, and spend 10,000 rubles to pay Yandex. Take into account 5,000 rubles in the income of the simplified tax system on the day you receive money from the principal.

You do not know the amount of the remuneration in advance and withhold it from the money received from the principal.

In such a situation, on the day you receive money from the principal, take into account the entire amount in the income of the simplified tax system. When you agree on the amount of the fee and approve it with the agent's report, you can reduce your income.

For example, you are buying furniture for the principal's office. He transfers you 200,000 rubles. According to the terms of the deal, your reward is what remains after the purchase. Therefore, on the day you receive money from the principal, you do not yet know the exact amount of the remuneration and take into account all 200,000 rubles in your income.

After purchasing the furniture, 20,000 rubles remain - this is your reward. You approve it with the agent’s report and on the same day make an adjusting entry in KUDiR: income of 180,000 rubles with a minus sign.

What to do if the agent is on the simplified tax system, and the principal is on the OSNO

Are you an agent or use their services? How are transactions carried out, how are invoices issued and is VAT allocated? Let's consider the features of interaction between an agent on the simplified tax system and a principal on the general taxation system.

No matter how well you understand the legislation regarding your tax regime, you will not be able to insure yourself against the occurrence of questions and difficulties. Often, ambiguities arise during the execution of an agency agreement.

Let’s define what is meant by the expression “agent” and “principal”, what rules should be followed when concluding an agency agreement, and what legal documents should be followed.

If the principal works with VAT, issue an invoice

You will be faced with VAT and invoicing if three conditions are met at the same time:

- you buy on your own behalf;

- the principal works with VAT;

- The seller issued an invoice.

You need to re-issue the invoice received from the seller with the same details. Only in the buyer's data indicate the principal's details and change the invoice number according to your numbering. Provide the principal with the reissued invoice and a copy of the seller's invoice.

Register both invoices - received from the seller and re-issued to the principal - in the invoice journal. This journal must be sent via the Internet to the tax office by the 20th day of the month following the quarter in which the invoices were issued.

In Elbe, issue an invoice with the transaction type “Purchased on my own behalf as an agent for clients (principals) on OSNO goods or services with VAT.” At the end of the quarter, a task on VAT reporting will appear in the “Current tasks” section.

If you are not buying on your own behalf, you won’t have to do all this. The seller will immediately indicate the principal’s details on the invoice, and you will just hand it over.

Providing transport services through agents

Under the contract, the freight forwarder undertakes to perform or organize the performance of certain services related to the transportation of goods.

The forms and procedure for preparing these documents are approved by the Russian Ministry of Transport.

5 Rules of transport and forwarding activities, approved.

Source: https://imdbmedia.info/byt-esli-agent-printsipal-osno/

Agency agreement under simplified tax system 15% Income minus expenses

In order for a principal who pays taxes under a simplified scheme to be able to sell and purchase goods through an agent (using an “income minus expenses” agreement), he must take into account two types of requirements:

- requirements regarding the execution of an agency agreement under the simplified tax system;

- must recognize income and expenses that directly arise from the agency agreement.

In order to fulfill the requirements associated with the execution of an “income minus expenses” agreement, the principal must examine the content of the subject of the agency agreement, the agent’s rights and obligations, his own rights and obligations, etc. To do this, you need to adopt the norms of the Civil Code of Russia.

For example, when drawing up an agency agreement, you should pay special attention to:

- terms of the agency agreement;

- form of principal-agent relationship;

- specifying the degree of authority of the agent;

- restrictions details.

Let's take a closer look. When studying the terms of the contract, you should understand that the conditions are basic (their essence is disclosed in the subject of the contract) and indirect, complementary. The indirect ones include the cost of the agent’s services in accordance with the provisions of the agency agreement and the speed (timing) of execution. An important condition that the principal must pay attention to is the price and terms on which the agent's fee is paid.

When clarifying the form of the “principal-agent” relationship, it is important to understand which specific orders the agent will perform on his own behalf, and which on behalf of the customer. Specification of the level of authority is necessary in order to understand and provide for that part of the transactions that the agent will perform on his own behalf.

Detailing the restrictions is an important stage, since it is here that the principal has the opportunity to outline the powers of the agent and specify the subtleties with the possibilities or prohibitions regarding the conclusion of subagency agreements (delegation by the agent of part of the task to another agent).

Also, in the agency agreement it would not be superfluous to specify the details of cooperation and points that should appear in the agent’s report (a document drawn up after completing all instructions).

If the payment of funds and delivery of goods to buyers occurs thanks to the work of an agent (through him, for example, through his bank account or the agency’s internal cash desk), then the agency agreement must detail the period during which the agent must notify the principal about the receipt of funds in his account (or to the cashier). Such seemingly trifles may ultimately determine the period during which the profit will be included in income. The result is timely tax payments.

Also, as we have already noted, the principal must recognize income and expenses directly arising from the agency agreement. These requirements are provided for in Chapter 26.2 of the Tax Code of the Russian Federation.

Agent on OSNO, principal on simplified tax system

Intermediary services are generally considered to be the performance by an intermediary company of certain actions for the company ordering these services. In this case, an agreement called an agency agreement (assignments/commissions) must be concluded.

In it, the customer (Principal) instructs the contractor (Agent) to perform certain services for a fee.

In the future, the agent, fulfilling his obligations, has the right to act on behalf of the customer or his own, but always at the expense of the principal (Article 1005 of the Civil Code of the Russian Federation).

Such an agreement stipulates (but not necessarily) the deadlines for fulfilling the terms of the agreement and submitting a report on expenses incurred with the attached documents.

In the absence of such requirements in the contract, reports are submitted by the agent upon fulfillment of obligations (Article 1008 of the Civil Code of the Russian Federation).

In addition, the agreement specifies the amount of remuneration for the agent, which can be a fixed amount or a percentage of sales.

The services of an intermediary are subject to VAT at a rate of 18% if he is a tax payer. This rule also applies to the sale of VAT-free goods (Article 149 of the Tax Code of the Russian Federation), with the exception of medical goods, funeral services and rental of premises to foreign companies (Article 156 of the Tax Code of the Russian Federation).

The mechanism for applying an intermediary agreement is simple, but taking into account the difference in the taxation systems of counterparties, we will understand the features that accompany the relationship between agents and principals in the field of recognition of income and expenses and taxation.

Principal on the simplified tax system – agent on the simplified tax system

All types of agency agreements have the same accounting principle for the purposes of calculating tax on the simplified tax system: the remuneration received by the agent increases the tax base of the intermediary company.

The date of recognition of income will be the day the funds are credited to the account. It depends on the terms of the agreement. If an agent, participating in settlements, withholds remuneration from the amount transferred by the customer during the transaction, then the date of income is the day the funds are received.

The agent must allocate the amount of remuneration and reflect it in the KUDiR. If it is transferred separately, then the agent will record the income at the time of receipt of the remuneration, and not the amount received to fulfill the contract.

The agent's income does not include amounts allocated for the execution of the contract, and expenses do not include expenses incurred for their implementation.

Income from sales through an agent is recognized as income of the principal depending on the specifics of the agreement:

- if the agent participates in settlements on behalf of the customer - the day the money from the implementation of the agreement is received into the principal’s account (clause 1 of Article 346. 17 of the Tax Code of the Russian Federation);

- when an agent conducts sales on his own behalf - the day the money is received into the intermediary's account.

The amount of recognized income is considered to be the sales value of the goods indicated in the agent’s report.

Since companies using the simplified tax system (income minus expenses) can take into account expenses only upon payment, the amounts transferred by the principal-customer will be recognized as expenses after the agent fulfills his obligations (clause 2 of article 346.17 of the Tax Code of the Russian Federation). Those. when the agent submits documents confirming the expense.

In practice, the relationship between agent and principal is as follows:

- with the participation of an agent in transactions, amounts received from the customer for the implementation of the specified operations are credited to the agent’s account, then transferred to counterparties upon fulfillment of the terms of the agency agreement. The agent reflects the purchase of property for the principal in off-balance sheet account 002, since he is not the owner of the goods. When goods are transferred to the principal, the purchase amounts are debited from the account. 002. Since simplifiers are not VAT payers, they do not allocate tax in the amount of remuneration, and accordingly do not draw up invoices;

- without the participation of an agent in settlements: in this case, no amounts are received from the customer into the intermediary’s account; he only submits a report upon completion of the transaction and receives the agreed amount of remuneration.

An example of accounting support for intermediary operations using the simplified tax system:

| Operation | D/t | K/t |

| Receipt of funds from the principal | 51 | 76 |

| Transfer to supplier | 60 | 51 |

| Receipt of goods from the supplier | 76 | 60 |

| Reflection of inventory items on the balance sheet | 002 | |

| Write-off of commissions for inventory items | 002 | |

| The reward received is reflected | 76 | 90/1 |

Agent on the simplified tax system – principal on the OSNO

If the principal company uses OSNO, then its agent (even a simplifier), regardless of whose name he acts, is obliged to issue invoices with VAT included in them.

In accordance with the Civil Code of the Russian Federation, the principal, transferring the goods to the agent for sale, remains its owner until the moment of sale.

The sale is carried out by the principal with the involvement of an intermediary, so the proceeds are taken into account by him when calculating income tax and VAT.

An agent on the simplified tax system is remunerated from the principal’s income, and his remuneration will be an expense without VAT, i.e. in this case the agent does not issue an invoice for the remuneration.

Invoices issued by the agent to the purchasers are recorded in the invoice journal, and are not recorded by him in his sales book, but are subsequently transferred to the principal as attachments to the report. The agent using OSNO fills out an invoice for the amount of his remuneration.

Accounting for transactions according to the scheme “Agent on the simplified tax system – principal on the OSNO ” in accounting will be reflected as follows:

| Operation | D/t | K/t |

| At the agent's | ||

| Sales of services under an agency agreement | 62 | 76/settlements with the principal (RP) |

| Receipt of funds from acquirers | 51 | 62 |

| Transfer of funds to the principal minus remuneration | 76/RP | 51 |

| Revenue from agency fees | 62 | 90/1 |

| Agent's remuneration credited | 76/RP | 62 |

| At the principal's | ||

| Based on the agent's report, the sale of services is reflected | 62 | 90/1 |

| Agency fee accrued | 20 (44) | 76 |

| Costs for intermediary services written off | 90/2 | 20 (44) |

| Purchasers of services are charged VAT | 90/3 | 68 |

| Revenue taken into account minus intermediary fees | 51 | 62 |

| Agent's remuneration taken into account | 76/PDK | 62 |

A type of mediation agreement is a commission agreement.

The peculiarity of the status of this agreement in comparison with its agency counterpart is that the commission agent (intermediary) can act in it, carrying out the instructions of the principal (customer of services), only on his own behalf, but at the expense of the principal. Accounting according to the scheme “commission agent on the simplified tax system – principal on the OSNO ” will be identical to that presented above.

Agent on OSNO – principal on simplified tax system

Art. 346.11 of the Tax Code of the Russian Federation exempts simplifiers from the obligation to pay VAT, therefore the principal’s agent on the simplified tax system does not calculate tax on transactions relating to the principal.

But at the end of the transaction, the agent issues an invoice for the amount of the remuneration, without registering it in the accounting journal (clause 3.1 of Article 169 of the Tax Code).

The VAT presented by the agent is subsequently taken into account by the simplified principal in the costs of the simplified tax system in the usual manner.

A peculiarity of the recognition of income by the principal using the simplified tax system is that, according to tax legislation, the simplified person’s revenue is the entire amount of receipts into the account. Therefore, when the agent deducts remuneration from funds received from transactions, the amount of income will be considered all proceeds from sales received to the agent’s account.

Source: https://spmag.ru/articles/agent-na-osno-principal-na-usn

Taxation

As you know, working through an agent is sometimes not only convenient, but also very profitable. One of the immediate advantages of agency agreements under a simplified system is a clear reduction in the tax burden on the simplified system.

According to agency agreements, income is only remuneration, and not the entire circulating amount that passes through the current account. Let's give an example: a taxpayer (for example, an individual entrepreneur) places advertising material as part of his business. The client, as a result of the success of the material, pays the entrepreneur money for the product or service. The businessman sends part of these funds to a service (for example, Yandex). Paying taxes on the full amount is not profitable, and not particularly advisable. The solution is simple: we enter into an agency agreement and take into account only the percentage of net profit in tax deductions.

When calculating taxes under the simplified system, only agency profits need to be taken into account. If a businessman sells, for example, equipment, receiving 5% of sales, then there is no need to pay tax on 500 thousand rubles received from buyers for selling 10 units for 50 thousand. You only need to pay for your 25 thousand profit. This is precisely the advantage of agency agreements under the simplified tax system in small and medium-sized businesses. Similar thoughts apply to excise duties, VAT, etc.

Agency agreements: how an agent pays taxes when purchasing goods or services for a principal

When placing customer advertisements on Yandex.Direct, not all the money that passes through the account is real income. Most of them go to pay for Yandex services. We tell you what amount to take into account in income when calculating the simplified tax system and how to arrange everything so that the tax office does not have any questions.

Your client - the principal - can hire you to buy anything: an apartment, advertising or phones from China.

When you agree on the terms of the transaction, he will transfer you money to pay for goods or services.

In some situations, the principal pays for the purchase directly, and your task is only to find the seller and negotiate a deal with him. For the work you will receive an agency fee from the principal.

Try Elba for free for 30 days. The service will calculate taxes and prepare reports for individual entrepreneurs, LLCs and employees. You can do it even if you don’t know anything about accounting.

Pay the simplified tax system only from your remuneration

The money that the principal transferred to pay for the goods or services is not your income. Therefore, tax must be paid only on agency fees.

To determine the date of receipt of income, carefully read the clause of the contract that establishes the agency fee and the procedure for its payment.

The amount of remuneration is fixed in the contract.

The principal can transfer the remuneration in a separate amount or you yourself will withhold it from the money received for the purchase. Take the remuneration into account in the simplified tax system on the day you receive money from the principal.

For example, you place an advertisement for a principal on Yandex.Direct. He transfers you 15,000 rubles, of which you keep your reward - 5,000 rubles - yourself, and spend 10,000 rubles to pay Yandex. Take into account 5,000 rubles in the income of the simplified tax system on the day you receive money from the principal.

You do not know the amount of the remuneration in advance and withhold it from the money received from the principal.

In such a situation, on the day you receive money from the principal, take into account the entire amount in the income of the simplified tax system. When you agree on the amount of the fee and approve it with the agent's report, you can reduce your income.

For example, you are buying furniture for the principal's office. He transfers you 200,000 rubles. According to the terms of the deal, your reward is what remains after the purchase.

Therefore, on the day you receive money from the principal, you do not yet know the exact amount of the remuneration and take into account all 200,000 rubles in your income. After purchasing the furniture, 20,000 rubles remain - this is your reward.

You approve it with the agent’s report and on the same day make an adjusting entry in KUDiR: income of 180,000 rubles with a minus sign.

If the principal works with VAT, issue an invoice

You will be faced with VAT and invoicing if three conditions are met at the same time:

- you buy on your own behalf;

- the principal works with VAT;

- The seller issued an invoice.

You need to re-issue the invoice received from the seller with the same details. Only in the buyer's data indicate the principal's details and change the invoice number according to your numbering. Provide the principal with the reissued invoice and a copy of the seller's invoice.

Register both invoices - received from the seller and re-issued to the principal - in the invoice journal. This journal must be sent via the Internet to the tax office by the 20th day of the month following the quarter in which the invoices were issued.

In Elbe, issue an invoice with the transaction type “Purchased on my own behalf as an agent for clients (principals) on OSNO goods or services with VAT.” At the end of the quarter, a task on VAT reporting will appear in the “Current tasks” section.

If you are not buying on your own behalf, you won’t have to do all this. The seller will immediately indicate the principal’s details on the invoice, and you will just hand it over.

Give the agent's report to the principal

Do not forget to report to the principal on the work done. To do this, draw up an agent report within the deadlines established by the contract - every week, monthly, or only based on the results of work.

In the report, indicate what you bought for the principal and how much money you spent on it. Attach to the report documents confirming the purchase - acts, invoices, checks, etc. Also write down the amount of your remuneration in the report. If this is not done, you will have to draw up a separate act for the agency fee.

Agent report form

Document flow between the parties

The main document in the “agent-principal” relationship is (besides, of course, the agency agreement itself) a report on the implementation of the agency agreement. All agents are required to provide such a document, regardless of the type of activity and the specifics of the relationship. Moreover, Article 1008 of the Civil Code of Russia requires agents to provide reports on completed assignments even when the principal allows them not to be provided,

This document must contain not only formal explanations, but also all evidence of expenses that the agent had to make during the execution of the agency agreement. A more complete package of documents (receipts for payment of duties, subagency agreements and agreements with partners or lessors) is stipulated in the agency agreement itself. Thus, in addition to the documents provided for by the Civil Code, the rest of the document flow is regulated exclusively by the principal and agent in the manner of drawing up an agency agreement.

The agent's report on blood pressure under the simplified tax system can be found here.

Sample report of an agent on blood pressure under the simplified tax system

At the agent's

Clause 1 of Art. 1005 of the Civil Code of the Russian Federation provides that under an agency agreement, one party (agent) undertakes, for a fee, to perform legal and other actions on behalf of the other party (principal) on its own behalf, but at the expense of the principal or on behalf and at the expense of the principal.

The principal is obliged to pay the agent remuneration in the amount and in the manner established in the agency agreement (Article 1006 of the Civil Code of the Russian Federation).

According to clause 1.1 of Art. 346.15 of the Tax Code of the Russian Federation, when determining the object of taxation, income provided for in Art. 251 Tax Code of the Russian Federation.

In particular, income in the form of property (including cash) received by a commission agent, agent and (or) other attorney in connection with the fulfillment of obligations under a commission agreement, agency agreement or other similar agreement, as well as for reimbursement of expenses incurred by the commission agent, is not taken into account. , agent and (or) other attorney for the principal, principal and (or) other principal, if such costs are not subject to inclusion in the expenses of the commission agent, agent and (or) other attorney in accordance with the terms of the concluded agreements. The exception is commission, agency or other similar remuneration (clause 9, clause 1, article 251 of the Tax Code of the Russian Federation).

Thus, the agent’s income is recognized only in the amount of agency remuneration, additional remuneration if its receipt is provided for in the agency agreement, as well as the amount of additional benefit remaining at the disposal of the agent. These conclusions are confirmed in Letters of the Ministry of Finance of Russia dated 02/10/2009 N 03-11-06/2/24, 01/26/2009 NN 03-11-09/18, 03-11-09/19, dated 11/26/2007 N 03-11 -05/274, in the Letter of the Federal Tax Service of Russia for Moscow dated September 7, 2009 N 16-15/093049, in the Resolution of the Federal Arbitration Court of the Ural District dated November 26, 2007 N F09-9602/07-C3.

Moreover, if the agent does not participate in the calculations, then the date of recognition of revenue will be the day of receipt of the agent’s remuneration (additional benefit, additional remuneration) from the principal to his current account or to the cash desk (clause 1 of Article 346.17 of the Tax Code of the Russian Federation).

Opinion. Andrey Brusnitsyn, 3rd class adviser to the State Civil Service of the Russian Federation:

It should be noted that when conducting tax audits of individual entrepreneurs who use agency agreements in their activities, the tax authorities carefully check the reality of the transactions concluded by the entrepreneur, including their actual execution. For this purpose, data on cash flows across accounts, information about counterparties, and analysis of primary documents are used. Therefore, individual entrepreneurs should especially carefully keep records of documents in this area of activity.

At the same time, collecting evidence about the fictitiousness of transactions concluded by an entrepreneur is a rather complex process. Therefore, in the event of legal disputes, entrepreneurs have sufficient chances to defend their position in court.

As an example, we can cite the Resolution of the Federal Antimonopoly Service of the North Caucasus District dated May 12, 2009 in case No. A53-11082/2008-C5-44, which reflects the position that the courts lawfully satisfied the entrepreneur’s demands to recognize the tax authority’s decision regarding additional assessment as illegal the single tax paid when applying the simplified tax system, the corresponding penalties and fines, since when determining the tax base, income in the form of funds or other property that is received, in particular, under agency agreements is not taken into account. At the same time, the corresponding opinion is confirmed by the Ruling of the Supreme Arbitration Court of the Russian Federation dated September 18, 2009 N VAS-11344/09 in the same case, which refused to transfer the case for review in the manner of supervision of judicial acts, since the tax authority unlawfully included in the income of the entrepreneur funds received to his current account in connection with the fulfillment of obligations under agency agreements and commission agreements.

If the agent participates in the calculations and withholds remuneration from the money received from buyers, then it becomes income precisely on the day the money is received in the agent’s current account or cash register. Note that the commission agent takes into account the remuneration as part of the income, regardless of whether at that moment the order is considered completed or not, since with the cash method of determining income and expenses, advances also include advances (clause 1 of Article 346.17 of the Tax Code of the Russian Federation; Decision Supreme Arbitration Court of the Russian Federation dated January 20, 2006 N 4294/05).

In column 4 section. I “Income and Expenses” The Book of Income and Expenses does not reflect income received in the form of property (including cash) received by the agent in connection with the fulfillment of obligations under an agency agreement (clause 2.4 of the Procedure for filling out the Book of Accounting of Income and Expenses of Organizations and individual entrepreneurs using the simplified taxation system approved by Order of the Ministry of Finance of Russia dated December 31, 2008 N 154n).

These incomes are not taken into account when determining the maximum amount of income that limits the right to use the simplified tax system (clause 2 of article 346.12, article 248 of the Tax Code of the Russian Federation).

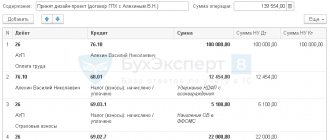

Example 1. IP Ivankov I.A. is an agent under an agency agreement with Beta LLC (principal) and applies a simplified system with the object of taxation “income”.

March 1, 2010 IP Ivankov I.A. received from the principal goods for sale in the amount of 590,000 rubles. (including VAT - 90,000 rubles). The agency fee under the contract is 10% - 59,000 rubles.

Payments are made through an agent. April 15, 2010 IP Ivankov I.A. received 590,000 rubles into my bank account for goods sold. (including VAT - 90,000 rubles). On the same day, having withheld the amount of remuneration, he transferred 531,000 rubles to the principal. (590,000 - 59,000).

Based on the provisions of paragraphs. 9 clause 1 art. 251 Tax Code of the Russian Federation IP Ivankov I.A. must reflect in taxable income only the amount of his remuneration, i.e. 59,000 rub.

Example 2. IP Novikov A.A. (agent) applies a simplified system with the object of taxation “income”. On February 1, 2010, he received goods for sale from the principal in the amount of RUB 177,000. (including VAT 18% - 27,000 rubles). The cost of delivery of goods amounted to 23,600 rubles. (including VAT - 3600 rubles). The agency fee, in accordance with the terms of the contract, is withheld from the proceeds and amounts to 25,000 rubles. IP Novikov A.A. participates in calculations.

He received the proceeds from the sale of goods to his bank account on February 15, 2010. On the same day, the money was transferred to the principal’s bank account in the amount of 128,400 rubles 0 - 23,600).

Thus, on February 15, 2010, individual entrepreneur Novikov A.A. will include in income only the amount of its agency fee, i.e. 25,000 rub.

With regard to the additional benefit from the sale of goods belonging to the principal, it should be taken into account that the amount received by the agent in the part that is not subject to transfer to the principal under the terms of the agreement is also income for the agent and, accordingly, is subject to a single tax (Letter of the Federal Tax Service of Russia for the city of No. Moscow dated April 17, 2007 N 20-12/035144).

Example 3. IP Tsvetkova I.A. (agent) applies a simplified system with the object of taxation “income”. On March 1, 2010, she received the goods for sale. According to the terms of the agency agreement, the minimum selling price of the goods is 177,000 rubles. (including VAT - 27,000 rubles). The agency fee is provided in the amount of 25,000 rubles. and is retained by the agent from the proceeds received from buyers for goods sold.

As part of the execution of this contract, the agent sold the goods for 200,600 rubles. (including VAT - 30,600 rubles). The procedure for distributing additional benefits is not specified in the agreement. The costs associated with the provision of intermediary services (not reimbursed by the principal) amounted to 15,000 rubles. In the case under consideration, the agent sold the goods on more favorable terms for the principal, and the agency agreement does not define the procedure for distributing additional benefits. Consequently, in addition to the remuneration (clause 1 of Article 991 of the Civil Code of the Russian Federation), the agent is entitled to half of the additional benefit (parts 1, 2 of Article 992 of the Civil Code of the Russian Federation).

Thus, the total amount of remuneration due to the entrepreneur, on which a single tax is paid, is 38,600 rubles. (15,000 rub. + (200,600 - 177,000) rub. x 50%).

Yu.Suslova

Auditor

LLC "Audit Consult Law"

Remuneration for blood pressure under the simplified tax system

According to agency agreements, the agent is obliged to carry out instructions from the principals solely for a fee (fee). According to Article 1005 of the Civil Code of the Russian Federation, even if the principal, after fulfilling the agency agreement, entered into personal cooperation with a third party (the entity with whom the agent must work, representing the interests of the principal) and claims that he independently fulfilled his own instructions, the agent should receive a reward.

Moreover, if an agent carries out orders for free (under a pre-agreed agency agreement with zero payment), then the Civil Code requires payment for services in accordance with internal government tariffs.

Also, it should be remembered that according to Article 974 of the Civil Code, everything that an agent receives in the process of executing an assignment under an agency agreement is the property of the principal. Withholding remuneration from the total amount of funds received under the contract is the full right of the principal. In addition, the Civil Code allows agents to deduct their fees from amounts received from third parties under the contract. This right is spelled out in paragraph 2, article 1 and paragraph 4, article 421 of the Civil Code.

At the principal's

The rules provided for in Chapter 1 apply to relations arising from an agency agreement. 51 “Commission” of the Civil Code of the Russian Federation, if these rules do not contradict the provisions of Chapter. 52 “Agency” or the essence of the agency agreement (Article 1011 of the Civil Code of the Russian Federation).

According to paragraph 1 of Art. 996 of the Civil Code of the Russian Federation, things received by the commission agent from the principal or acquired by the commission agent at the expense of the principal are the property of the latter.

Consequently, the receipt of funds to the settlement account or to the agent’s cash desk from buyers in payment for goods sold on behalf of the principal, which are his property, should be taken into account as revenue from the sale of these goods from the principal (Letter of the Ministry of Finance of Russia dated August 20, 2007 N 03-11- 04/2/204).

The Letter of the Ministry of Finance of Russia dated 05/07/2007 N 03-11-05/95 explains that the date of receipt of income for the principal will be the day of receipt of funds transferred by the intermediary to bank accounts and (or) to the cash desk of the principal.

The principal's income is the entire amount of proceeds from the sale of goods received to the agent's account. Article 251 of the Tax Code of the Russian Federation does not provide for a reduction in the income of principals by the amount of remuneration paid by them to agents. Therefore, the income of principals applying the simplified taxation system should not be reduced by the amount of agency fees withheld by the agent from the proceeds from sales received in his current account when it is transferred to the principal. In this case, it does not matter which object of taxation is used by the commission agent applying the simplified tax system - “income” or “income reduced by the amount of expenses”.

Based on this, the income of the individual entrepreneur - the principal is not reduced by the amount of remuneration withheld independently by the agent from the amounts received by him on the basis of the agency agreement. The same position is reflected in Letters of the Ministry of Finance of Russia dated June 25, 2009 N 03-11-06/2/107, dated June 5, 2007 N 03-11-04/2/160, Federal Tax Service of Russia for Moscow dated March 5, 2007 N 18 -11/3/ [email protected]

In this case, the agency fee, paid by the principal to the agent or withheld by the agent independently from the amounts received by him on the basis of the agency agreement, relates to the expenses of the principal on the basis of paragraphs. 24 clause 1 art. 346.16 Tax Code of the Russian Federation.

Consequently, an individual entrepreneur who is a principal and uses the “income minus expenses” taxation system has the right to reduce the income received by the amount of remuneration paid to agents (Letters of the Ministry of Finance of Russia dated April 22, 2009 N 03-11-09/145, dated November 29, 2007 N 03- 11-04/2/290, Letter of the Federal Tax Service of Russia for Moscow dated 03/05/2007 N 18-11/3/ [email protected] ).

Accounting and postings

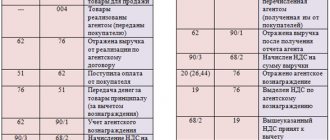

It is customary to keep accounting records of agency agreements on account 76 “Settlements with various debtors and creditors.” You can assign various subaccounts to this account, including agents.

- Since the goods that the agent purchases under the agency agreement are not his property, they are reflected in the balance of account 002 “Inventory assets accepted for safekeeping.”

- If the principal transferred goods to the agent for the purpose of their further sale, then such goods are included in the balances of account 004 “Goods accepted on commission.”

- Agents' fees and their remunerations are displayed in accounts 62 “Settlements with buyers and customers”. This account is the base account for VAT deductions.

Intermediary transactions on the simplified tax system - the topic of this video:

AD for utilities with simplification

For landlords who pay taxes under a simplified scheme, taxes and utility payments are often too high. There are only two options for reduction, and only one of them is absolutely legal. The first is not to pay taxes, the second is to reduce tax deductions by concluding an agency agreement and paying utility bills within the framework of a “principal-agent” relationship.

The Ministry of Finance considers this work scheme to be quite possible and legal. In order to work according to this principle, two agreements must be signed between the landlord and the tenant:

- a lease agreement, which clearly states all rental amounts;

- agency contract.

The first agreement implies that the tenant must pay utilities. The second agreement specifies that at the expense of the tenant and with his full consent and instructions, the landlord purchases services from utility companies.

Sample AD for utilities