The expenditure of money given to an employee in advance is confirmed by a primary accounting document - an advance report. The completed sample expense report is a unified form No. AO-1, in one part of which the employee enters information, and in the second - the accountant.

Attached to the expense report are checks and receipts confirming expenses. As of July 1, 2019, amendments regarding the mandatory details of checks came into force if goods (services) are purchased by a legal entity or individual entrepreneur or an employee on behalf of the company. To ensure that tax authorities have no complaints about checks, they must contain:

- name and tax identification number of the buyer;

- excise tax amount;

- Number of customs declaration;

- country of origin of the goods;

- breakdown by product item.

Remember also that BSOs are now practically not issued on paper; all sellers, with the exception of individual entrepreneurs on the simplified tax system and PSN, are obliged to issue full checks to buyers.

Another important point: in order to process the return of accountable amounts on an advance report, the employee has the right to bring a printed receipt received by e-mail or SMS, including with a QR code. Electronic and paper cash receipts are equivalent, so there will be no problems during checks. The exception continues to be e-tickets. To accept them as expenses for income tax purposes, boarding passes are printed and presented for inspection. Otherwise, it will not be possible to prove the cost of transport services. Or you will have to make a request to the carrier company so that it confirms the provision of the service to a specific passenger.

Return of accountable amounts

The law establishes specific deadlines for submitting an advance report by the accountable person, within which the employee is obliged to report on the funds spent. This is three working days after the expiration date for which the funds were issued, or from the date of going back to work (clause 6.3 of Directive No. 3210-U).

If the employee has not fully spent the funds, an advance report is drawn up for the used portion, and the remaining amount is indicated in it. This is subject to the return of imputed amounts on the advance report, and this should be done simultaneously with the submission of the report.

There are often situations when an employee spends his own money, then brings documents and asks for reimbursement of accountable amounts according to the advance report. In this case, he applies to the accounting department with an application for reimbursement of expenses incurred, and the accountant also makes such calculations using an advance report.

If the employee has not spent anything, he returns the entire accountable amount received to the cashier, and does not prepare an advance report. In this case, the deadline for submitting the advance report by the accountable person is not taken into account, but the money must be returned no later than three days after the expiration of the period for which it was issued.

REPORT FORM FOR COST CONTROL IN EXCEL

Creating a budget won't seem like a complicated process if you use a template to work with.

The main thing is to choose from a huge number of templates the one that suits your purposes: create a budget for an investment project, track the current expenses of an enterprise, plan the upcoming financial year, etc. In this article we will present the most informative and accessible report formats for controlling expenses in Excel. Let's do this using an example (the name is conditional). Every day, the head of the company needs to make a decision on how to distribute funds and prioritize payments. A Cash Flow Budget ( CFB can help him with this - a document that collects all received requests for payment and information about the available funds in the company.

This document is generated in Excel. As information material, they take accounting data on cash balances in accounts at the beginning of the period for which they plan to compile a cash balance sheet, cash balances (if there is a cash accounting), all outstanding obligations both according to accounting data (accounts payable at the beginning of the period), and and in accordance with concluded payment agreements.

When preparing the BDDS, you need to remember that all payments must correspond to the approved planned budget of income and expenses of the company. As soon as an unscheduled payment appears, a message should appear that this is not included in the plan.

If, as a result of planning, negative cash balances , the budget is adjusted by reducing the payment plan. Therefore, to understand the situation, it is better to immediately add information to the BDDS about the current debt to suppliers, planned costs for the coming month and forecast debt at the end of the month, taking into account the amounts of payments included in the budget.

Table 1 shows the cash flow budget of Vasilek LLC for November 2021.

As can be seen from table. 1, the net flow for the month is predicted to be negative (–2270 rubles), however, due to the initial balances of 6500 rubles. the company is able to fulfill the stated budget for a given month . At the same time, it increases receivables from its customers from 18,500 to 29,000 rubles. and reduces accounts payable to suppliers of goods from 45,000 to 30,000 rubles. In general, the picture for the month is optimistic.

Of course, there are mandatory payments that cannot be postponed until the second half of the month (rent, utility bills, wages). Therefore, a weekly or daily payment plan is needed , which the company must strictly adhere to. Let's consider daily payment planning for Vasilek LLC for November 2021 (Table 2).

Please note that the presented daily payment plan is formed as an Excel summary table. Of course, you can use a developed report transferred to Excel, but experience shows that it is better to work with an information array or database . Currently, in Excel, using ready-made layouts, you can not only create a very convenient report, but also install a multi-level analysis system.

In the report for calculating the amount of expenses, you can immediately see income and expenses, and grouping by day is possible (Table 3).

From Table 2 you can see how much you need to spend in a period for a certain cost item, from Table. 3 - what amount should be in your accounts on a specific date.

The form for forecasting and recording expenses by day does not have to be conservative. There may be small deviations in it, for example, a more detailed name of costs (sometimes a standard grouping is not enough, you need to have a more detailed idea of the expense).

To account for expenses, you can use the form presented in table. 4.

To create this table, you need to process a huge amount of data.

Filling procedure

Since a unified form has been developed, the rules for how an advance report on the accountable amounts spent in the current year are drawn up also apply.

First, it is filled out by the employee who received the money and reports on it, then by the accountant. When the document is completely ready, it is given to the manager for control.

Let's look at a specific example of filling out an advance report on business expenses and at the same time tell you about all the nuances.

What does the employee fill out?

Front side.

On the front side of form No. AO-1, the employee must:

1. Indicate the company name and OKPO code.

2. Enter the date the document was compiled and assign a number.

3. In the “Report in amount” column we enter the amount that the employee spent on the business needs of the enterprise. For example, he was given 12,000 rubles, and he spent 10,000. Therefore, in this column he indicates 10,000.

4. We indicate the name and code of the structural unit.

5. After this, indicate your full name. the accountable person, his personnel number and profession (position).

6. Enter the purpose of the advance.

7. On the left side of the table located on the front side of the form, indicate the amount of the amount received from the company’s cash desk (or to a bank card). If necessary, indicate the amount of money issued in foreign currency.

8. We indicate the total amount of funds received.

9. Enter the amount spent on the business needs of the enterprise.

10. Indicate the amount of the balance.

Reverse side.

There is information that must be indicated on the back of the employee's advance report document. The reporting person in columns 1-6 lists all documents (sales receipts, cash receipts, etc.) confirming the expenses incurred, indicating the amounts spent. Documents are numbered in the order they are listed in the expense report.

The presented completed sample advance report clearly demonstrates what information the employee should enter in the appropriate columns:

- 1 — payment number assigned to the document confirming expenses;

- 2 - date of check;

- 3 — check number;

- 4 - name of the document confirming expenses;

- 5 - the amount of expenses incurred in rubles;

- 6 - filled in if necessary if there were expenses in foreign currency.

After listing the details for all attached documents, fill out the “Total” line, where they indicate the total amount of expenses.

After the employee has filled out the required fields, he puts his signature on the form with a transcript. Then the document is sent to the accounting department, where the accountant checks the correctness of completion.

What does an accountant fill out?

Front side.

After receiving the form, the accountant must ensure that it is filled out correctly. If there are no errors, the accountant makes a note about this in the “Report verified” column and signs it.

The accountant provides information about the deposited balance or overspending.

After this, he proceeds to further filling out the form.

The detachable part of the form is filled out, signed and given to the employee.

Reverse side.

The accountant records information in columns 7 and 8. The amounts of expenses accepted for accounting are indicated here. Column 9 indicates the numbers of accounting accounts that are debited for the amount of expenses. The amounts indicated by the employee and the accountant must match.

After this, the accountant fills out the front side of the form.

Front side.

On the front side in the right table, the accountant checks the following information:

- balance or overspending of the previous advance;

- the amount of the advance received from the enterprise's cash desk;

- amount of money spent;

- balance or overexpenditure of advance amounts.

In the table on the left - the accounting entry - information is entered from the data in column 9, which is on the reverse side.

The accountant sends the document to the chief accountant (if there is one), who also checks it. After checking the expense report, the chief accountant signs it and sends it to the head of the enterprise for approval.

The director approves the document and returns it to the accounting department.

This is what a sample of filling out an advance report in 2021 for business expenses looks like. A similar registration procedure applies in any other situations - when you need to report on travel or entertainment expenses.

The completed expense report is kept in the company's accounting department for 5 years. After this period, the document is destroyed.

The legislation does not contain a direct prohibition on compensation of employee expenses in the interests of the organization. And at the same time, it does not provide specific recommendations for the execution of this operation. Moreover, this type of operation occurred at least once in every organization.

If for a specific issue of accounting (AC) the federal standards do not establish methods for maintaining accounting, then the organization itself develops an appropriate method (clause 7.1 of PBU 1/2008). Thus, the Organization needs to prescribe in its Accounting Policy the method and procedure for compensating employees for expenses incurred for the needs of the organization, including approval of the document on the basis of which compensation for expenses will be made to the employee.

In our opinion, the use of account 71 “Settlements with accountable persons” is not appropriate, since the account is intended for settlements with employees for amounts issued to him on account (Instructions for the use of the Chart of Accounts, approved by Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 N 94n ). And in this situation, the employee was not given accountable amounts.

To reflect settlements with an employee, in our opinion, it would be more correct to use account 73.03 “Settlements for other transactions”.

Since when purchasing goods at his own expense, the employee acted with the permission and in the interests of the organization, it is necessary to document that the organization approved such a transaction (Clause 1 of Article 183 of the Civil Code of the Russian Federation). Such documents may be:

- An employee’s application for reimbursement of expenses, approved by the manager (the resolution on the application is “pay”).

- An approved report on the funds spent with documents for purchase and payment attached to it (sales receipt, delivery note, invoice, etc.), including in the form based on AO-1.

- An order on behalf of the manager to reimburse expenses to an employee.

Funds spent by an employee on the purchase of goods or services for the needs of the organization and reimbursed to the employee by the organization on the basis of supporting documents (checks, receipts) are not recognized as the employee’s income and, accordingly, are not subject to personal income tax (Letter of the Ministry of Finance of the Russian Federation dated 04/08/2010 N 03- 04-06/3-65). Also, this compensation is not subject to insurance premiums (clause 2, clause 1, article 422 of the Tax Code of the Russian Federation).

In 1C, the operation is best documented with the following documents:

- Receipt (act, invoice)

; - VAT write-off

; - Cash withdrawal

or

debit from current account

.

Type of transaction – Other expense

, debit account – 73.03 “Settlements for other transactions”.

Structure and content of the report

For a person without special education, the document may seem quite complicated. It consists of three sections in which monetary transactions are reflected in code values according to three main indicators of the organization’s performance:

- current,

- financial

- and investment.

It should be borne in mind that not all cash movements need to be included in this document. Exceptions include

:

- currency exchange transactions,

- receipt and delivery of cash to a bank account,

- exchanging cash equivalents for each other,

- transfer from one organization account to another, etc.

A complete list of actions can be found in clause 6 of PBU 23/2011.

Important Feature

: The report includes any financial transactions of the company. falling under its qualification requirements, regardless of the monetary units of which country they were produced in, but all data in the document is entered only in Russian rubles, and strictly in the unit of measurement (thousands, millions) that was used in drawing up the balance sheet .

Receipt of material assets

Receipt of goods, materials, services is documented with the document Receipt (act, invoice)

from the section Purchases - Receipts (acts, invoices).

- Account for settlements with counterparties – 73.03 “Settlements for other transactions”;

- The invoice is not registered.

Postings according to the document

Automatic analytics for account 73.03 “Settlements for other transactions” in the document Receipt (act, invoice)

not substituted. It is necessary, using manual adjustment, to substitute the name of the employee who incurred the costs.

Checking settlements with an employee

To check mutual settlements with an employee, you need to create a balance sheet

for account 73.03 “Settlements for other transactions” section Reports - Standard reports - Account balance sheet.

- the acquisition may be considered by the tax authorities as expenses incurred in favor of employees with additional personal income tax (clause 2 of Article 226 of the Tax Code of the Russian Federation and subclause 2 of clause 1 of Article 228 of the Tax Code of the Russian Federation);

- in the absence of a purchase and sale agreement between the employee and the organization, the tax authority may not recognize expenses on documents issued to the employee for tax purposes.

By Gretchen im Westen nichts Neues

asked a question in the section

Other household matters

And again about “school” money - do you require a report from the parent committee? I'm thinking about demanding... and I got the best answer

Answer from Nyusha K[guru] So today I was indignant - we donate to the class fund, to the school fund, and next week they demanded that we bring work gloves from home so that the children could clean the area. We're already sick of these extortions... I don’t feel sorry for the money, I just feel bad that they make idiots out of us.

Answer from Arseny Bakaev Bakaev

[newbie] Of course ask! You have every right to do this!

Answer from Pioneer Komsomol member)))

[guru] At the end of the year, they print it out and bring it to the last meeting. Whoever needs it takes it and reads and counts. Claims are only based on the amount of money spent on gifts, etc.

Reply from Angel

[guru] Ask. I'm kind. Committee. I keep all the receipts, I can account for every penny. But no one has yet been interested in where the money goes.

Answer from a bright corner...)))

[guru] I should ask... Ours report to the penny...)))))))))

Answer from Oriy Kulikov

[guru] was at the parent meeting?

Reply from Orlicka

[guru] Our committee always reports without reminders, at the next meeting. What, you didn’t have any gifts for the New Year or for March 8th? I don’t think that your family stuffed your money into their pockets...

Reply from *~*Green-Eyed Beauty10000*~*

[guru] At our meetings they always reported themselves and without demands)))

Answer from Olga S

[guru] I don’t require it yet. The parent committee reports itself. No reminders.

Answer from Aksinya Nikalavna™

[guru] ahh... I was late for the meeting (I was visiting a graduate) and forgot to report. and forgot that the meeting was the last one!! ! ok, at the beginning of the year I’ll tell you where the money goes))) otherwise my parents really don’t know. we fed the children at 8 and 23, and how much money was spent on gifts for the teachers... Moreover, I was ordered to buy gifts. and for New Year's too.

Reply from Yinsha

[guru] We have no monetary taxes, no parent committee.)) And we don’t have a housing and communal services system either.

Answer from Velkhatnaya

[guru] We collected money only for gifts. Coolers, various accessories, repairs were done at the expense of the school. We had an adequate parent committee, before graduation they called everyone and asked what to give to the teachers, whether it was worth ordering a limousine or, more simply, a bus, all the amounts were outlined step by step... . Ask if you have any doubts.

Reply from Laura Petrarkina :)

[guru] I am the parent committee. I keep records in Excel - income, expenses, balance. I bring printouts to every meeting. Last year, one mother was indignant at why they didn’t call her and tell her how much she needed to donate and for what needs. This mother’s eldest child graduated from the same gymnasium, she knows very well that every meeting is a collection of money for the holiday (with a small reserve, which constitutes the so-called class fund, spent on all sorts of needs). I expressed all this and offered to hand over the affairs to the dissatisfied mother on the same day. I also have a family, work, household chores. Those who do not consider it necessary to come to parent meetings and make collective decisions about fees and expenses should not be offended. YOU are handing over YOUR money, so you have the right to politely demand that you be provided with a report on your expenses. P.S. I certainly thank the parents by name who donated the money on time, and read out the list of basic purchases (although some parents frown nervously, not wanting to waste precious time listening to these lists).

Reply from 3 replies

[guru]

Hello! Here is a selection of topics with answers to your question: And again about “school” money - do you demand a report from the parent committee? I'm thinking of requesting...

Legislative reform of accounting provisions regarding budgetary institutions began in 2021. According to Order of the Ministry of Finance dated July 1, 2013 No. 65n, a number of amendments were made to the instructions on budget classification, changing some codes for the classification of operations of the general government sector (). Thus, analytical accounts have been updated in the budget accounting registers, reflecting the movement of accountable amounts. At the same time, amendments were included in the Tax Code of the Russian Federation.

In 2021, the Central Bank made changes to the report,

having adopted the regulatory legal act No. 4416-U dated June 19, 2017, which introduced significant amendments to the instructions of the Central Bank of the Russian Federation dated March 11, 2014 No. 3210-U. The main modifications affected clause 6.3, and from August 19 it became easier to issue accountable amounts.

New reporting rules:

- It is allowed to issue money on account only to an employee with whom the employer has signed an employment contract (Article 15 of the Labor Code of the Russian Federation), or to an individual working under a civil law contract (Letter of the Central Bank of the Russian Federation dated October 2, 2014 No. 29-R-R-6/7859) ;

- Employees do not have to provide an application to issue money. The basis for payment of the advance amount is an order, instruction or decision signed by the manager;

- the issuance of the required amounts is carried out even if there is a debt on accountable money issued earlier.

What has changed in the algorithm for issuing funds?

The new reporting rules represent the following sequence of actions:

- The employee submits it to the accounting department in any form signed by the head of the institution.

- Accountable persons, the changes of 2021 approved this innovation, are now allowed to have debt on previously issued advances. But before issuing, make a complete reconciliation of mutual settlements with him.

- The employee provides an advance report no later than 3 working days after the date established in the order. All available documents confirming expenses must be attached to the advance report. Unspent money (accountant).

- An accountant or cashier checks the received expense report and primary documents to ensure they are filled out correctly. The inspection period is set independently by each institution through local regulations.

If the management of a budget organization wants to protect itself from non-repayment, approve a ban on issuing funds if the employee has an existing debt. For this purpose, the Regulations on settlements with accountable persons are approved.

No changes in accountable amounts have been recorded in 2021. The employee has the right to receive any amount of money in advance without restrictions. If an employee pays with suppliers, contractors or performers as a representative of a budget organization, the amount of cash given to him is limited to 100,000 rubles per contract.

Is it possible to transfer accountable amounts to a card?

Legal regulation does not establish any prohibitions on the transfer of funds to a corporate or debit plastic card to an employee. The Ministry of Finance also speaks about the possibility of transferring advance money to a salary card (Letter dated July 21, 2017 No. 09-01-07/46781). For the legitimacy of carrying out such actions, a budget organization must prescribe and approve the feasibility of non-cash payments in its accounting policies, in the Regulations on settlements with accountable persons, and in the order on the development of standard advance reporting forms, noting non-cash transfers as an additional item.

If the employee spent personal money

If an employee has raised his own funds to meet the needs of the organization, he draws up a reporting statement. The employee writes an application for reimbursement of the money spent by him, the manager accepts, reviews and approves it. An order is then issued to reimburse the money spent.

If the employee spent his own money, this is not reporting!

The reimbursement algorithm must be prescribed in the organization’s regulatory framework by drawing up a local act with an appendix in the form of a sample report on the employees’ own money spent on the needs of the institution.

The accounting department must carefully check the provided primary documents for reimbursement. If possible, the employee must register them directly with the organization in order to avoid additional personal income tax accrual to him. Letter from the Ministry of Finance dated 04/08/2010 No. 03-04-06/3-65 explains such situations as follows: the employee’s actions exclude economic benefit, and, accordingly, the taxable base.

Guardian report 2017-2018 - the sample for filling

it out has changed compared to the forms relevant for earlier periods. It must be submitted no later than February 1 of the year following the reporting year. When compiling it, you must adhere to the approved form and filling rules, which will be discussed in this article.

Report on the expenditure of funds from customs. Who came across it?

The results of such reconciliation are drawn up in an act in the form approved by order of the Federal Customs Service of Russia dated December 22, 2010 No. 2521. The reconciliation act is drawn up in two copies, signed by the customs authority and the person who made the advance payments. One copy of the act after its signing is handed over to the specified person.

Thus, without joint reconciliation by the customs authority and the person who made the advance payments, a customs payments reconciliation report cannot be provided.

Please note that the basis for conducting a joint reconciliation is the disagreement of the person who made the advance payments with the results of the customs authority’s report on the expenditure of funds made as advance payments.

Thus, in order for your organization to compare customs information with available information, you must perform the following steps:

1) send a written application to the customs office to provide a report on the expenditure of funds contributed as advance payments;

2) having received a report on the expenditure of funds, the organization may agree with this report or not;

3) if the organization that made the advance payments does not agree with the results of the customs authority’s report, a joint reconciliation of the expenditure of this person’s funds is carried out, based on the results of which a reconciliation act for the advance payments is compiled.

Appendix No. 1

to the Order of the Federal Customs Service of Russia

dated December 23, 2010

Guardian's report 2017–2018 (form, basic rules for drawing up)

The Law “On Guardianship and Trusteeship” dated April 24, 2008 No. 48-FZ provides for the annual submission of a report on the ward’s property, his income and expenditure of funds. The guardian must report for the past year by February 1 (inclusive) of the next year. The report is placed in the personal file of the ward, which is stored in the guardianship authority.

In 2014, major changes occurred in the reporting form for persons guarding minors. The authorities simplified reporting, since the need to account for even minor expenses was a serious problem for guardians. Therefore, when compiling a report for 2017-2018, guardians and trustees of children will no longer have to account for the purchase of food, shoes, clothing, hygiene products, medicines and other similar expenses.

However, when preparing a report on the property of minors, certain rules must be followed:

- the report is not compiled arbitrarily, but according to the form approved by Decree of the Government of the Russian Federation dated May 18, 2009 No. 423 (as amended on September 10, 2015);

- the information reflected in the report must be confirmed by attached documents (copies of receipts, checks, etc.);

- it is possible to fill out the form either by hand (legibly) or using a computer;

- mandatory details - the signature of the compiler with the transcript and date of submission of the report;

- corrections and crossing-outs are unacceptable;

- You should not leave fields blank - if there is no information, write the words “no”, “does not have”;

- it is necessary to take into account that monetary amounts are indicated in thousands of rubles;

- information about income must be reflected in total for the year;

- if the child received income in foreign currency (for example, as a gift), then the report indicates the equivalent of this amount in rubles at the Central Bank exchange rate as of December 31 (or December 30, if the 31st is a day off) of the reporting year.

Report on the intended use of funds: how to fill out

The report is structured according to the usual scheme: balance at the beginning + receipts – expenses = balance at the end. They begin to fill out the form with the line under code 6100, which reflects the incoming balance of funds corresponding to their size at the end of the previous period.

Next is a block of positions reflecting all types of income, distinguished by individual flows. For example, in line 6210 the amount of entrance fees is indicated, in line 6215 - membership fees, and in line 6220 - target fees. Property contributions and donations on a voluntary basis are coded with code 6230; for amounts of profit, if the enterprise is engaged in income-generating activities, there is line 6240, and income that does not fall into the listed flows is considered other (for example, additional fees to cover the losses of a gardening partnership) and is accumulated in line 6250. The final position under code 6200 records the amount of lines filled in the “receipt” section.

The use of funds in the form of a report on the intended use of funds is also distributed among individual items in the corresponding block with codes from 6310 to 6320. In turn, expenses in this section are grouped by expenses:

• for carrying out targeted activities - period 6310 with breakdown by lines:

- 6311 (charity and social projects);

- 6312 and 6313 (conferences and other events);

• for the maintenance of the administrative apparatus – line 6320, broken down by cost structure by codes:

- 6321 (wages and accruals);

- 6322 (payments not related to work duties);

- 6323 (business trips and business trips);

- 6324 (maintenance of buildings, structures, premises, vehicles);

- 6325 (repair);

- 6326 (other expenses);

• for the purchase of inventory, fixed assets – line 6330;

• other (for example, expenses for auditor consultations, repayment of bank loans - line 6350).

Line 6300 combines all the listed costs for the year.

The final position under code 6400 represents the amount of unused funds at the end of the year, calculated using the formula:

page 6400 = page 6100 + page 6200 – page 6300.

If, according to the results, the share of costs exceeds income, then the negative result is recorded in parentheses.

An example of a report on the targeted use of funds for 2021

The gardening partnership SNT "Bely Klyuch" operates with a staff of employees, which consists of a chairman, an accountant, and an electrician. Seasonal maintenance work on the water supply system is carried out by hired workers - a welder and a mechanic. The activities of the partnership are carried out in accordance with the approved estimates of income and expenses. The performance indicators of SNT "White Key" for 2018 and 2021 are presented in the table:

| Indicators in rub. | 2019 | 2018 |

| Balance of funds at the beginning of the year | 22 000 | 52 000 |

| Income, including: | 1 430 000 | 1 900 000 |

| Entry fees | 10 000 | 100 000 |

| Membership fee | 900 000 | 990 000 |

| Target fees: | ||

| - for the construction of the central road | 280 000 | 500 000 |

| - for the construction of light poles | 80 000 | 260 000 |

| Income from renting out premises to Leo LLC | 160 000 | 50 000 |

| Use of funds received in the activities of SNT "White Key" | 1 446 000 | 1 930 000 |

| — remuneration of full-time and hired workers, taking into account insurance contributions | 380 000 | 320 000 |

| — payment for the chairman’s trip to the seminar | 36 000 | |

| — road repair | 280 000 | 260 000 |

| — holding the event “Harvest Festival” | 70 000 | 80 000 |

| — acquisition of equipment for reconstruction of the power supply system and its installation | 120 000 | 140 000 |

| — renovation of the SNT board building | 100 000 | |

| — payment for rental of electrical equipment | 100 000 | 200 000 |

| — construction of a waste collection area | 150 000 | |

| - garbage removal | 110 000 | 120 000 |

| - water pipeline repair | 80 000 | 200 000 |

| - Payment of utility services | 270 000 | 360 000 |

| Balance at the end of the year | 6000 | 22 000 |

In the report on the intended use of funds, the balance at the beginning of 2019 in line 6100 must correspond to the balance at the end of 2021. (p.6400).

All receipts are recorded in the lines of the first block of positions, expenses - with line-by-line differentiation according to the target attribute. In practice it looks like this:

Filling out a report from a guardian of a minor child

The header indicates the period for which the guardian is reporting. Sections 1–3 of the report contain information about its compiler and the ward. Section 4 reflects information about the child’s property. Table 4.1 contains information about real estate owned by a minor (type, method of acquisition, location, etc.). The following table (4.2) is intended to indicate the vehicles owned by the ward. Table 4.3 indicates the amounts of funds in bank accounts as of December 31 of the reporting year.

Subsection 4.4 of the report reflects information about the ward’s shares in the authorized capital of commercial organizations and the availability of shares or other securities in his possession. Section 5 contains information about the guardian’s withdrawal of funds from the ward’s account (including details of the act of the guardianship authority authorizing such withdrawal). In the same section, the child’s things that have become unusable are indicated.

Section 6 deals with the ward's income. For each type of income (alimony, benefits, etc.) there is a separate line indicating the amount of this income for the year. Next, the total (total) annual income is reflected. Section 6 does not indicate income from the use of property, since a separate table is provided for this - 7, which reflects the benefits from leasing or selling real estate, interest on bank deposits, income from securities, etc. It is necessary to indicate documents guardianship authorities authorizing real estate transactions.

Section 8 contains information about the child’s spending:

- for his treatment in medical institutions;

- purchase of durable goods (costing more than 2 subsistence minimums);

- repair of the person's home.

There is no need to report small household expenses for 2017-2018.

Section 9 reflects information on the payment of taxes on the property of a minor.

— an invoice, if the purchased assets are subject to VAT.

Please note: to write off expenses for fuel and lubricants, travel documents are also required.

Read more about this in the articles “Business trip abroad” and “Taking into account expenses for business trips abroad” // Salary, 2010, NN 1 and 2. - Note. ed.

In addition to paying for transport services for delivery to the point of assignment, the employee has the right to pay for taxi services or local passenger transport. These expenses are taken into account if appropriate supporting documents are available. These can be cash register receipts, tickets.

— its name, six-digit number and series;

- name and legal form - for an organization or last name, first name, patronymic - for an individual entrepreneur;

— location of the hotel;

— cost of the service in monetary terms;

— date of calculation and preparation of the document;

- position, surname, name and patronymic of the person responsible for the transaction and the correctness of its execution, his personal signature, seal of the organization (individual entrepreneur);

— period of residence of the employee;

— a list of additional services included in the cost of living. After all, some of them do not reduce the taxable base for income tax, for example, service in bars and restaurants, room service, use of recreational and health facilities and other services that are not economically justified (clause 1 of Article 252 of the Tax Code of the Russian Federation).

— date of preparation of the document;

— measuring business transactions in physical and monetary terms;

— names of positions of persons responsible for carrying out a business transaction and the correctness of its execution;

- for an official reception;

— transport support for delivery to the event venue and back;

— buffet service during negotiations;

— payment for the services of translators who are not on staff to provide translation during the event.

Example of preparing a cash flow statement

Filling out the header

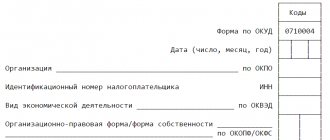

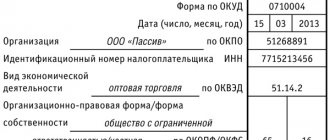

Since the document is extremely important, you must be very careful when drafting it and fill out all the necessary cells.

- First, the report indicates the year for which it was compiled.

- Next, enter the full name of the organization (with the abbreviation of the organizational and legal status) and the following data:

- Date of preparation,

- OKPO code (All-Russian Classifier of Enterprises and Organizations),

- TIN,

- type of economic activity (required in the form of an OKVED code and decoding).

- Below, again, the organizational and legal form and form of ownership are entered, and next to them are the OKOPF (All-Russian Classifier of Organizational and Legal Forms) and OKFS (All-Russian Classifier of Forms of Ownership) codes.

- The last line of the document header indicates OKEI (All-Russian Classifier of Units of Measurement) codes: i.e. thousands or millions used in the report.

Filling out section 1

The first section of the document contains information about current cash flows .

- First of all, information about “receipt” : data on the total amount of funds received is entered in line 4110, which is then scattered across the underlying thematic lines - from 4111 to 4119 - in accordance with the accounting registers. This takes into account transactions from the sale of services and inventory, rental payments, interest, royalties and other “incoming” finances.

- Line 4120 indicates the total amount for payments made during the reporting period : payment of taxes and contributions to pension funds, wages, transfers to contractors and suppliers, etc. Then this amount is also posted to lines 4121 to 4129.

- the balance from current operations is entered in line 4100 (i.e., the amount of “incoming” finances minus expenses incurred).

This section also contains information about cash transfers and receipts that cannot be unambiguously classified.

An important nuance: expenses in the table must be indicated in parentheses, and excise taxes paid to suppliers and contractors, just like VAT, do not need to be included here.

Filling out section 2

The section entitled “ Cash flows from investment operations ” is completed in a similar manner. First of all, “ total receipts ” are entered in line 4210, including from the sale of shares, returns on loans, dividends, sales of non-current assets, etc., which is then posted in the required values on the corresponding lines (from 4211 to 4219).

Payments ” for investment transactions are also filled in below total is entered into line 4220 , which is then, in full accordance with the accounting registers, signed on the lines below (from 4221 to 4219), including the acquisition and other costly transactions with non-current assets, payment of interest, acquisition of debt securities, etc. .d.

Then enter the value of the balance of cash flows from all investment activities (receipts minus expenses).

Filling out section 3

The last section of the document is devoted to cash flows from various types of financial transactions . Everything is similar here:

- first, line 4310 indicates the value of “total” receipts , which is then distributed along the lower lines (from 4311 to 4319), including income from the issue of shares and bonds, loans, borrowings, etc.

- “total” indicators for financial payments are entered in line 4320, followed by their distribution in lines from 4321 to 4329.

- Then the difference between the “incoming” and “outgoing” cash flows for the reporting period for financial transactions is indicated.

- Finally, the document includes the total balance of all three cash flows for the reporting period (can be either with a plus or a minus sign), financial balances at the beginning and end of the period, as well as the difference in the exchange rate between the currencies of other countries and the Russian ruble, which is calculated using a special formula (filled in only when the organization made settlement transactions in foreign currency).

After drawing up the report, the document is submitted for approval to the head of the organization, who, with his signature, certifies the authenticity of the information included in it.