Options for errors requiring a refund and their consequences

In relations between counterparties, errors in the transfer of funds are possible, associated with:

- with the wrong choice of counterparty when generating a payment order;

- indicating an incorrect payment amount;

- reflection in the purpose of payment of the details of a document that does not exist in the relationship.

Such errors can be identified by any of the parties, but will require a mandatory written expression of the initiative of the payer of funds to take actions carried out in connection with their correction.

In a number of situations, the error can be corrected by adjusting the purpose of the payment if, for example, there is a supplier-buyer relationship between the counterparties, against which an erroneously transferred amount (or a payment with an incorrectly specified purpose) may be taken into account.

You will find a sample letter to the counterparty to clarify or change the purpose of payment in ConsultantPlus. If you do not already have access to this legal system, a full access trial is available for free.

Correction via payment adjustment cannot be applied if there are no current engagement agreements with the payee.

Regardless of the reason for which the payment was considered to have been made without reason, it is recorded by both the payer and the recipient using the same algorithms, taking into account the fact that for these two parties the transactions when returning the erroneously transferred funds will be mirror images.

Since erroneous transfers subject to refund have no connection with the calculations performed between suppliers and buyers, VAT on them is not allocated either for payment or as deductions. However, if calculations are carried out in foreign currency, then exchange differences attributable to income/expenses may arise. The recipient of the funds, when returning them, in the purpose of payment in the payment document should reflect information that this payment is used to return the funds erroneously transferred to him, and provide a link to the details of the document in which the payer expressed a request to return the money to him.

If the error is corrected by taking into account the transferred amount as payment under another supply agreement, then it will be taken into account in the usual manner for the supplier-buyer relationship with the implementation of the necessary VAT transactions.

If you need to return money to the buyer from the cash register, first look at what ConsultantPlus experts say about returns:

If you don't have legal access, a full access trial is available for free.

How to reflect a refund from a supplier in 1C 8.3?

Yulia79, yes. I chose a return. I re-posted it. That's it too. When I pay a supplier, I first make a receipt of goods (Dt26 Kt60.01), and then write off funds from the current account using the “receipt” document. In this case, do we need to receive services? It turns out that we sent the money, then it came back and we still have it. So there was no receipt?

Lidochka Dugarova, everything is fine. I checked.

there can be no advance payment.

Yulia79, invoice from the supplier.

Lidochka Dugarova, should this amount be reflected in the SALT? I wrote it off and returned it and it was completely closed at SALT.

Mahosha, should be reflected in the SALT. After all, there were debits from the current account and refunds.

There's something wrong with the analytics. Can you once again generate an invoice of 60 for subaccounts with selection only for your supplier?

In the report settings (Groups), please check the boxes next to the Contract and Calculation Document analytics

1) Based on the invoice, you paid the supplier the amount of 4250 - D 60.1 K 51 2) They returned this money back to you, in the bank statement you select “return from supplier” D 51 K 60.1, as a result, everything is closed perfectly.

3) An invoice is a document of intent and never serves as the basis for posting to the accounting office, as Yulia wrote to you:

Lidochka Dugarova only made payment to the supplier. When I make a refund, the amount disappears from the SALT. I am attaching screenshots with payment to the supplier. Maybe there is something wrong there..

The holding, for some reason, when I pay the bill, Dt is not 60.01, but 60.02 Kt 51.

Kamushek, we paid in August, the money was returned to the account in October.

Lidochka Dugarova, this is how I write off. Then this amount disappears in SALT and that’s it. Nothing is reflected.

Makhosha, I wrote an incorrect answer yesterday. I'll rewrite it now))))

Mahosha, we pay the supplier in August: Document Write-off from the current account, transaction type Payment to the supplier. because there is no debt, there will be posting Dt 60.02 Kt 51

the amount at 60.02 will remain until the money is returned from the supplier. there will be a document Receipt to the current account, transaction type Return from supplier, posting will be generated Dt 51 Kt 60.02

after that, account 60.02 for this supplier will be closed and there will be no balance as of 31.10. in the balance sheet there will be only turnovers.

In this case, a quality or low-quality product is returned, does not affect the design.

The return of goods to the supplier is reflected according to Dt 76.02 “Calculations for claims” (chart of accounts 1C). If the returned goods have not previously been paid for, then when returning to the supplier in 1C 8.3, an additional entry Dt 60.01 Kt 76.02 is created, which automatically reduces the debt to the supplier by the cost of the returned goods.

If a defective product is taken into custody or only part of it is returned, then the low-quality product is first registered and then returned to the supplier.

Purchasing goods

Document the receipt of goods at the warehouse with the document Receipt (act, invoice) transaction type Goods (invoice) in the section Purchases - Purchases - Receipt (acts, invoices).

If you are returning only part of the goods, then issue 2 documents Receipt (act, invoice) : one - for the receipt of goods accepted for registration, the second - for the receipt of goods not accepted for registration.

Receipt of registered goods

Registration of SF supplier

For the return of goods not accepted for registration to the supplier, document the return of goods to the supplier transaction type Purchase, commission based on the document Receipt (act, invoice) transaction type Goods (invoice) or in the section Purchases - Purchases - Returns to suppliers.

An invoice for the return of goods not accepted for accounting is not issued. An adjustment invoice from the supplier issued for a partial return of goods is not registered in the purchase book (Letter of the Ministry of Finance of the Russian Federation dated February 10, 2012 N 03-07-09/05).

On January 10, the Organization purchased the “Imperial” Table (100 pcs.) from the supplier “CLERMONT” LLC for the amount of RUB 1,416,000. (including VAT 18%). On the same day, the goods arrived at the warehouse and were accepted for accounting.

On February 6, part of the goods (38 pieces) was returned due to a defect.

Fill out the return of goods accepted for registration with the document Return of goods to supplier transaction type Purchase, commission based on the document Receipt (act, invoice) transaction type Goods (invoice) or in the section Purchases - Purchases - Returns to suppliers.

Issuance of invoices for return to the supplier

If goods already accepted for registration are returned to the supplier, then issue an invoice for their return at the bottom of the document form Return of goods to supplier .

Reflect the purchase of goods in the document Receipt (act, invoice) transaction type Goods in the section Purchases - Purchases - Receipts (acts, invoices) - Receipt button.

Invoice document will be automatically filled in.

After subscribing, you will have access to all materials on 1C Accounting, recordings of supporting broadcasts, and you will be able to ask any questions about 1C.

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Related publications

Incorrectly addressed money arrived in the current account: postings

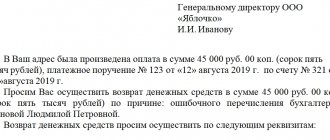

For the recipient of funds to whose current account money was mistakenly received, a posting reflecting the receipt of unidentifiable funds will be made at the time the payment document is linked to the accounting accounts.

A similar amount is debited to account 76, and this is done by posting Dt 76 Kt 51 (52).

Accordingly, if the erroneous payment is returned to the counterparty's current account, the posting will be reversed: Dt 51 (52) Kt 76. The exchange rate difference when returning currency will be reflected by the posting Dt 91 Kt 76 or Dt 76 Kt 91.

If, in relation to a payment reflected as an error, a decision arises to take it into account as payment for a future or already completed sale of goods (performance of work, provision of services), then on the basis of written information received from the payer, an entry will be made Dt 62 Kt 76 with the ensuing hence the VAT implications.

Refund transactions

For organizations and individual entrepreneurs working on the simplified tax system, the return of an advance from a supplier does not entail tax consequences. Despite the use of the cash method, when transferring the prepayment, no expenses arise, since materials, goods, services have not yet been received, etc. Therefore, the returned advance is not recorded in KUDiR, but should be recorded in the accounting (in the bank statement) a note clarifying the meaning of the transfer of money received. Each gift voucher and discount coupon has a unique number.

Gift vouchers and vouchers cannot be redeemed for cash or give rise to cash claims. Products purchased with a gift certificate or coupon are subject to a general exchange or refund of the coupon if the product is returned. They can be used during their stated validity period. Gift vouchers and coupons are not associated with other coupons or promotions. This item does not apply to affiliate products.

An advance or prepayment is a payment that is received by the supplier (seller) before the date of actual shipment of products or before the provision of services (clause 1 of Article 487 of the Civil Code). If the supplier (performer) has not fulfilled its obligations within the period established by the contract, then it must return the funds received from the buyer (customer). How to reflect such a refund of advance payment from the supplier in the buyer’s accounting and tax records?

- A report on identified discrepancies, drawn up in the TORG-2 form (for imported goods - TORG-3 form)

. This document is drawn up if, upon shipment of the goods and after payment, the customer identifies deviations in the quality or quantity of products, as well as if inconsistencies are detected in the shipping documents. - Invoice (form TORG-12)

, which is used to issue a return if a defective product is detected, or the product does not comply with the approved state or contractual standard.

Postings when returning an erroneously transferred payment from a counterparty

For the payer, the amount transferred to the wrong counterparty or transferred in a larger volume also goes to account 76: Dt 76 Kt 51 (52) or Dt 76 Kt 60 (if it is no longer possible to correct the posting made on the payment order).

The return of incorrectly transferred funds from the counterparty in the postings will be expressed as Dt 51 (52) Kt 76. For currency payments, here you will also need to take into account the exchange rate difference, the amount of which will be charged either to the debit or credit of account 91 (Dt 91 Kt 76 or Dt 76 Kt 91).

If, in relation to an erroneous payment, a decision is made to offset it against payment for a delivery within the framework of an existing relationship with the counterparty, then the payment recorded on account 60 will simply change the analytics due to internal posting. In this case, it will be possible to take into account VAT in deductions for both advance payment and delivery.

Example of a return to the cash register

Let’s say the caretaker of the State Budgetary Educational Institution DoD DYUSSHOR “ALLUR” received a report of 10,000 rubles for the purchase of household chemicals. The funds were transferred to the employee’s bank card. The caretaker spent 9,500 rubles. The remaining 500 rubles were returned to the institution's cash desk. The cashier deposited the balance into the bank account at the end of the working day.

An advance payment for the purchase of household chemicals was transferred to the caretaker on a bank card

Accepted expenses for the purchase of household chemicals based on the approved advance report

The funds were returned to the institution’s cash desk, a cash receipt order was generated

The money was issued to the cashier for depositing into the company's current account, a cash receipt order was generated and an announcement for cash deposits was created.

Funds have been deposited into the current account

Results

All actions with a payment transferred to a counterparty by mistake are carried out with a written indication of their nature on the part of the payer.

In this case, the funds can be offset against settlements on existing relationships. In the accounting of both the recipient and the payer, the amount of the erroneous payment is reflected in account 76. In correspondence with this account, both parties will show the cash flow for the return: Dt 76 Kt 51 (52) - for the returning party, Dt 51 (52) Kt 76 - at the recipient of the refunded funds. Returning an erroneous payment has no tax consequences. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How to issue a refund via an online cash register: sample receipt, document flow, rules

Constituent documents, "Cash receipt order" (KO-1), 50 76-3 Receipt of cash: - from equity participation in other organizations. - on account of profits received from joint activities, Decision of participants, shareholders' meetings, "Cash receipt order order" (KO-1) 50 76-2 Receipt of the amount of claims to the organization's cash desk. »

Receipt cash order" (KO-1) 50 79 Receipt of cash from a separate division of the enterprise.

“Cash receipt order” (KO-1) 50 91-1 Sale for cash of fixed assets and other assets. “Cash receipt order” (KO-1) KKM check. 50 91-1 Reflection of positive exchange rate differences (based on changes in the ruble exchange rate against foreign currency held at the organization’s cash desk).

Accounting certificate-calculation 70 50 Issuance of wages from the cash register.

“Cash expenditure order” (KO-2), “Payroll” (T-53).

Forgiveness of an interest-free loan: we charge personal income tax According to the rules in force from 01/01/2016, when issuing an interest-free loan to an employee, personal income tax must be calculated on a monthly basis from the individual’s benefit from saving on interest.

The question arises: what to do with the already accrued tax amounts in the case when the lender forgives the borrower the entire amount of the loan issued. Return of cash to the buyer using a posting check Mikhail Obukhov | Labor Law | 03/08/2018 00:20 0 Comments