Author of the article: Lina Smirnova Last modified: January 2021 30171

In case of illness, an employee working officially is entitled to payment of social benefits based on the sick leave certificate presented. Such payments are made from insurance premiums withheld from his earnings. In this article, we will find out whether insurance premiums are levied on hospital benefits, how funds for their payments are generated, what is the procedure for making payments, and what can affect the taxation of benefits with insurance premiums.

Do insurance payments for the employer decrease due to the benefits?

According to paragraph 2 of Art. 431 of the Tax Code of the Russian Federation, employers can reduce insurance payments due to compensation for temporary disability, subtracting them from the amount they contribute to the Social Insurance Fund.

This is due to the fact that the Social Insurance Fund reimburses organizations and entrepreneurs for the funds spent on disability benefits, with the exception of the period paid by the employer.

Employers can protect themselves from unnecessary payments and fines if they take into account the established maximum benefits for temporary disability, as well as the rules for processing documents and the functioning of the system of insurance and trade union dues. In addition, it is important to take into account that the legislation allows you to reduce mandatory contributions at the expense of benefits paid for each month.

Didn't find the answer to your question? Find out how to solve exactly your problem - call right now:

Any working person for whom the employer makes contributions to Social Security receives sick leave benefits by law. The basis for its accrual is a sick leave certificate issued by a doctor in case of illness of an employee or when caring for any family member. Before going on maternity leave, pregnant women also receive this document.

This law applies to all types of disability benefits provided by law. This is confirmed by judicial practice and relevant regulatory documents No. 15AP-1002/13 and No. 07AP-8508/12 of arbitration appellate instances.

You should know that sick leave is not subject to contributions to the Pension Fund and compulsory medical insurance. The obligation to provide monetary compensation due to an employee’s incapacity for work is regulated by the norm of Article No. 183 of the Labor Code of the Russian Federation. The amounts of such compensation and the rules for their provision are prescribed at the legislative level.

Expert opinion

Semenov Alexander Vladimirovich

Legal consultant with 10 years of experience. Specializes in the field of civil law. Member of the Bar Association.

The employee's management must provide certain insurance payments in the event of an insured event, also at their own expense (clause 6, clause 2, article 12 of Law No. 165-FZ of July 16, 1999).

Sick leave benefits paid at the expense of the employer are not subject to insurance contributions.

Question from Clerk.Ru reader Irina (Shakhty)

What are the contributions for 3 days of sick leave, which are paid by the employer?

In accordance with paragraphs. 1 item 2 art. 3 of the Federal Law of the Russian Federation dated December 29, 2006 No. 255-FZ “On compulsory social insurance in case of temporary disability and in connection with maternity”, temporary disability benefits for the first 3 days of temporary disability are paid at the expense of the insurer (employer), and for the rest of the period starting from the 4th day - at the expense of the budget of the Social Insurance Fund of the Russian Federation.

Based on paragraphs. 1 clause 1 art. 9 of Federal Law No. 212-FZ of July 24, 2009, benefits and other types of compulsory insurance coverage for compulsory social insurance are not subject to insurance contributions for compulsory pension, social and medical insurance.

According to paragraphs. 3 p. 1 art. 1.2 of the Federal Law of the Russian Federation dated December 29, 2006 No. 255-FZ “On compulsory social insurance in case of temporary disability and in connection with maternity”, mandatory insurance coverage for compulsory social insurance in case of temporary disability and in connection with maternity is fulfilled by the insurer ( FSS), and in certain cases established by law No. 255-FZ, the policyholder (employer) of its obligations to the insured person upon the occurrence of an insured event through the payment of benefits.

Thus, the benefit paid at the expense of the employer for the first 3 days of the employee’s incapacity for work is recognized as insurance coverage and on the basis of paragraphs. 1 clause 1 art. 9 of Law No. 212-FZ, insurance contributions to the Social Insurance Fund, Pension Fund and Compulsory Medical Insurance Fund are not subject to insurance contributions.

It’s very easy to get a personal consultation with Olga Ziborova online - you just need to fill out a special form. Several of the most interesting questions will be selected daily, the answers to which you can read on our website.

Tax audits are becoming tougher. Learn to protect yourself in the Clerk's online course - Tax Audits. Defense tactics."

Watch the story about the course from its author Ivan Kuznetsov, a tax expert who previously worked in the Department of Economic Crimes.

Come in, register and learn. Training is completely remote, we issue a certificate.

The article was written based on materials from the sites: urexpert.online, r18.fss.ru, www.klerk.ru.

Taxation

However, personal income tax must be withheld from the entire amount of sick leave benefits. Payment due to temporary disability to an employee is made with a deduction of 13%.

These requirements do not apply to maternity benefits, which are exempt from withholding all kinds of contributions and deductions (clause 1 of Article 217 of the Tax Code of the Russian Federation). Read more about what taxes are taken from sick leave in 2021 in the article https://otdelkadrov.online/7207-raschet-vzimanie-ndfl-s-bolnichnogo-lista-v-year-godu.

If the statute of limitations does not exceed six months from the onset of the illness, the employee has the right to demand payment. The management of the organization must calculate the full amount of compensation within 10 days and ensure its payment on the appropriate salary date.

Sick leave for pregnancy and childbirth: is income tax (NDFL) charged and are contributions calculated?

Another reason why sick leave is issued may be the employee’s pregnancy and, accordingly, the birth of a baby. It is prescribed by a medical institution when an employee goes on maternity leave. She, in turn, must submit it to the accounting department of the enterprise, where the appropriate allowance must be calculated. The calculation of this particular benefit, as well as the VNIM benefit, is based on data on earnings and hours worked for the last two calendar years.

Important! The employee’s length of service does not affect the amount of the B&R benefit.

In 2021, the taxation of sick leave issued on the occasion of an upcoming birth has not changed: it, as before, is somewhat different from the taxation of general sick leave. The difference is that there is no need to calculate and withhold personal income tax. The fact is that maternity benefits are directly named in the list of income not subject to this tax (clause 1 of Article 217 of the Tax Code of the Russian Federation).

Personal income tax will not be calculated and withheld from other payments related to maternity:

- for registration in the early stages of pregnancy;

- upon the birth of a child;

- benefits issued to care for a child until he reaches the age of 1.5 years.

Absolutely all benefits related to maternity are issued at the expense of the Social Insurance Fund and are not subject to taxation of insurance contributions.

Work injury

Injury, occupational disease, or rehabilitation of an employee also exempts the organization from paying insurance premiums due to their status as compensation payments. Funds in a situation of damage to health, which are related to industrial injuries, are not subject to income tax. Such payments include:

- forced leave for the period of recovery and recovery;

- necessary treatment;

- compensation for moral damage is made by the employer at his own expense if such a decision is made by the court.

The employee's insurance length is decisive when calculating the amount of compensation. The minimum amount of sick leave benefits is 60% of the average salary, the maximum allowable payment is 100%.

Sick leave due to illness

If a certificate of incapacity for work is issued to an employee due to his illness, injury or the need to care for a sick family member, then payment for it is subject to personal income tax. This tax must be calculated and withheld from the entire benefit amount. That is, before transferring benefits to the employee, personal income tax is deducted from sick pay. And the employee is paid benefits minus personal income tax. That is, for example, if the benefit is 10,000 rubles, then you need to pay out 8,700 (10,000 - 1,300). Since personal income tax is 13 percent of the sick leave amount.

The rules are:

- Calculate personal income tax on benefits at a rate of 13% on the date of actual receipt of income by the employee (clause 1, article 224, clause 3, article 226 of the Tax Code of the Russian Federation). The date of actual receipt of sick leave income is the date of payment of benefits, that is, the date of transfer of funds to the employee’s bank account or the date of issuance of cash to the employee from the cash register (clause 1, clause 1, article 223 of the Tax Code of the Russian Federation).

- Withhold personal income tax upon actual payment of the benefit, and transfer the tax to the budget no later than the last day of the month in which the benefit was paid (clauses 4, 6 of Article 226 of the Tax Code of the Russian Federation).

- If the employer is a participant in the FSS pilot project, then the FSS of the Russian Federation will withhold personal income tax from its part of the benefit independently, since it pays it itself.

The amount of sick leave is reflected in the 2-NDFL certificate with income code 2300 (clause 6.7 of the Procedure for filling out the 2-NDFL certificate).

Additional payment up to average earnings

In addition to the amount of payments determined by law, the management of the organization can assign an additional payment up to average earnings from its own reserve budget. However, it is not state compensation and, according to the law, is subject to appropriate contributions as the wages of a working person.

If management takes them into account as contributions to the Social Insurance Fund, regulatory authorities may not accept them for credit in the following situations:

- the law was violated (for example, the average salary for an employee was calculated incorrectly);

- there are no supporting documents;

- the documentation does not comply with generally accepted rules of registration (Part 4, Article 4.7 of the Law of December 29, 2006 N 255-FZ).

Thus, sick leave is not subject to insurance contributions at the expense of the employer and the Social Insurance Fund. In order to save government subsidies, a Decree was issued to limit compensation for disability.

This measure led to increased control over the correct completion of hospital documentation. In case of incorrect registration or inaccurate calculation of benefits, Social Insurance may not accept such a sheet for consideration.

In case of illness, an employee working officially is entitled to payment of social benefits based on the sick leave certificate presented. Such payments are made from insurance premiums withheld from his earnings.

In this article, we will find out whether insurance premiums are levied on hospital benefits, how funds for their payments are generated, what is the procedure for making payments, and what can affect the taxation of benefits with insurance premiums.

Procedure for paying benefits for temporary disability

The benefit paid on the basis of sick leave is intended to compensate for the earnings of an employee who has a certain insurance period. It represents an amount formed mainly from the funds of the Social Insurance Fund.

Expert opinion

Semenov Alexander Vladimirovich

Legal consultant with 10 years of experience. Specializes in the field of civil law. Member of the Bar Association.

The benefit is paid by the employee's direct employer. Responsibility for the correct accrual of state social security funds rests with the manager, as well as the chief accountant of the enterprise.

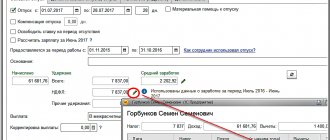

The payment is usually timed to coincide with the next salary payment. It is made together with the payment of the settlement or advance. Payment is made for the entire period of illness, starting from the first day of the employee’s illness. The costs for the first 3 days of the employee's sick leave are borne by the employer, and the remaining period is paid by the Social Insurance Fund.

Payment of sick leave benefits in connection with caring for a minor child or an adult dependent relative, as well as benefits in connection with pregnancy and childbirth, is calculated and paid entirely from the Social Insurance Fund.

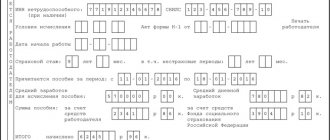

- Since January 2013, updated sick leave forms have been used, with higher requirements for their registration. This is due to the fact that previously the payment of sick leave benefits was carried out directly by the accounting department of the enterprise in which the sick employee worked, and the Social Insurance Fund compensated for the costs incurred in connection with the payment of benefits only after receiving the enterprise’s reports.

- Since 2021, legislative changes have come into force, according to which sick leave payment has become the most simplified.

- In 2021, a “pilot” project was launched in many regions, according to which benefits are paid directly from the Social Insurance Fund, bypassing the employer. With this method of making payments to the employee, the enterprise or organization pays from its own funds only the amount of benefits for the first 3 days of sick leave. In the future, the responsibility of the enterprise’s accounting department is only to transfer to the insurance fund, located geographically close to the enterprise, only the sick leave certificate itself and a certificate of the employee’s earnings for the previous two years. Based on the documents received, the Social Insurance Fund pays the benefit directly to the employee in the method chosen by him (by card, bank account or in person).

Which sick leave are subject to insurance premiums in 2021

But the obligation to accrue it concerns payments for sick leave and other similar payments. The personal income tax rate for sickness benefits is determined in accordance with the law.

Are taxes on sick leave paid by the employer? To answer the question asked, it is first important to understand how these benefits are calculated and who pays them. The legislation establishes clauses 2.6 of Art. 12 Federal Law No. 165.

When paying for sick leave in the Russian Federation, the following rule applies: the first three days of absence from work due to illness are paid by the enterprise, all the rest are paid by the Social Insurance Fund. Doubts may arise whether personal income tax is withheld from sick leave received from this Fund.

Expert opinion

Lebedev Sergey Fedorovich

Practitioner lawyer with 7 years of experience. Specialization: civil law. Extensive experience in defense in court.

It has already been said above that funds issued as part of the payment of sick leave are not included in the list of tax-free benefits.

If an employee of an organization gets sick, the employer is obliged to pay benefits that are accrued for the sick period, in accordance with Article 183 of the Labor Code of the Russian Federation. These benefits must be calculated within 10 days, starting from the day the employer provides sick leave, and accrued during the period of payment of wages.

However, we are talking exclusively about the benefit itself. The company may establish additional surcharges to the benefit. These are not reflected in Article 217. Renewal. The default value in the line is no. If the sick leave is a continuation, select the desired sick leave number from the drop-down list. Enter the information from the certificate of incapacity for work.

This is important to know: 7 years of experience, sick leave percentage

Payment for sick leave, with the exception of maternity benefits, is subject to personal income tax, regardless of the source of its payment (from the Social Insurance Fund or employer funds). Personal income tax on sick leave benefits must be withheld upon payment and transferred to the budget no later than the last day of the month in which the benefits were paid.

Benefit amount

The amount of benefits provided for payment on sick leave is determined by Article 7 of Federal Law No. 255. It depends on several factors:

- causes of disability;

- the length of time the employee was undergoing treatment;

- his insurance record.

If an employee is injured not related to work, or becomes ill and cannot perform the assigned work, he is required to pay for the entire period of being on sick leave:

- disabled people can be treated for up to 4 months;

- employees caring for disabled dependent relatives are paid monetary compensation for up to 30 days, and if the child has HIV, the duration of the payment period on the basis of sick leave is not limited.

The amount of payment is directly related to the duration of payment of insurance premiums (insurance period):

Many employers are concerned about whether sick leave is subject to insurance premiums. Most lawyers, quite rightly and in accordance with the law, answer simply - no, they are not taxed.

But, as practice shows, not everything is so simple. There are situations when sick leave is still subject to some kind of contribution.

Such situations often arise due to the peculiarities of the collective agreement between the employer and its employees, which this article will consider.

- Are insurance premiums calculated for temporary disability benefits?

- When do they still make transfers to the Social Insurance Fund?

- When are payments made?

- Calculation example

Are insurance premiums calculated for temporary disability benefits?

Before you find out whether sick leave is subject to contributions, it is worth understanding what it is and who is entitled to it. Domestic legislation clearly defines the circle of persons who are paid from the Social Insurance Fund and the recipient’s responsibilities regarding the payments received.

It must be taken into account that the state makes payments for sick leave only if the sick person has paid mandatory insurance contributions to the Social Insurance Fund. Their current rate is 2.9%.

Thus, we can say that the citizen pays for the time spent on sick leave thanks to the previously transferred insurance amounts. The amount of payments itself is calculated based on them.

Russian legal norms clearly indicate that sick leave is not subject to insurance contributions. Moreover, this applies not only to those payments that are made at the expense of the state fund, but also at the expense of the employer. Let us remind you that the Labor Code stipulates that payments from social insurance amounts begin only on the fourth day of sick leave.

The above rule applies equally to both sick leave payments in connection with pregnancy and in connection with caring for sick immediate relatives. The situation is different with personal income tax.

Insurance premiums for sick leave rules for calculation and payment

Motroy Alena Author PPT.RU May 31, 2021 For each employee who brings in , the employer pays for a period of temporary disability based on average earnings. The organization pays the amount only for the first three days of illness. The employee receives the rest from the budget of the Social Insurance Fund.

But many questions arise: are sick leave accrued, who pays it, how to calculate it correctly.

You will find the answers in our article. ConsultantPlus FREE for 3 days First, let’s figure out whether sick leave is subject to insurance premiums.

Based on this, we can conclude that payments for temporary disability cannot be considered as income from which funds should be deducted for social or pension insurance. Such payments are government benefits.

The tax law does not indicate that exemption from deductions depends on the source of payment. This means that sick leave insurance premiums are not charged at the expense of the employer (for the first three days). However, in certain cases, the employer may be required to pay social security and pension contributions.

This will happen if the employee is paid a benefit calculated from an amount that exceeds the maximum established by law.

But what is the maximum amount? According to the formula for calculating benefits, average daily earnings are calculated as the total income for the 2 previous years divided by 730 (731 if it is a leap year).

In this case, the maximum possible income is the sum of the maximum amount for paying contributions to the Social Insurance Fund, established for the two previous years.

Thus, the maximum average earnings for calculating benefits, from which you will not have to pay additionally, will be equal to: (755,000 + 718,000) : 730 = 2021.81 rubles. If to calculate temporary disability benefits in 2021.

If average earnings exceed 2,021.81 rubles, the excess amount will have to be paid in accordance with the general procedure.

Since this is already income that is not exempt from insurance fees. And you will have to pay 22% to the Pension Fund, 2.9% to the Social Insurance Fund, and 5.1% to the Compulsory Medical Insurance Fund.

Please note that if the employee’s total income exceeds 1,021,000 rubles, excluding that part of the sick leave that is exempt from insurance, then an additional 10% will have to be paid to the Pension Fund.

Consider this situation: Sidorov fell ill in 2021.

His salary has not changed since 2015 and is equal to 100,000 rubles per month. That is, for 2021 and 2021. he received 2,400,000 rubles. Despite this, the maximum amount with which temporary disability benefits exempt from contributions will be calculated in 2019 is only 1,473,000 rubles.

Therefore, the employee will either receive no more than 2,017.81 rubles for each day of illness, or the employer will calculate the amount of sick leave based on the employee’s actual earnings for 1 day, multiply this by 3 (the number of paid sick days), pay it, but withhold part of the funds during all off-budget funds.

In this case, the Social Insurance Fund will pay for the remaining period of illness based on the maximum possible average earnings in the two previous years. In our particular case, Sidorov’s average daily income is equal to: (1,200,000 + 1,200,000): 730 = 3287.67 rubles.

Compared to the maximum established by law, the average daily income of a particular employee is 1,269.86 rubles more. For three days, the amount of excess benefits, based on Sidorov’s real average salary, will be 3809.58 rubles.

This amount will have to be included in income subject to insurance premiums. Dear readers, if you see an error or typo, help us fix it! To do this, highlight the error and press the “Ctrl” and “Enter” keys simultaneously.

We will learn about the inaccuracy and correct it.

FOR AN ACCOUNTANT: ARTICLES FOR AN ACCOUNTANT: ARTICLES Subscribe to the daily newsletter Every weekday we will send you everything that was published yesterday You won’t miss anything!

Read us anywhere. Always be aware of the main thing!

Made in St. Petersburg 1997 - 2021 PPT.RU Full or partial copying of materials is prohibited; with agreed copying, a link to the resource is required. Your personal data is processed on the site for the purpose of its functioning. If you do not agree, please leave the site. Are you sure you want to remove the image you're using and replace it with your default avatar?

Are you sure you want to go out?

When do they still make transfers to the Social Insurance Fund?

When figuring out whether contributions are calculated for sick leave, it is worth considering two possible situations when you will still need to pay contributions to the state.

- about additional benefits;

- sick leave payments at the initiative of the employer in connection with the refusal of the Social Insurance Fund.

In both cases, government bodies will consider such payments as additional income, from which all due contributions and fees will have to be transferred to the budget and compulsory insurance funds.

The first situation arises when the employer, on its own initiative, increases the sick leave benefit to 100% for an employee to whom it is not yet due based on length of service.

The legislation provides that the employer is obliged to pay a sick employee a special benefit in case of illness, the amount of which depends on the length of service of the employee:

- with less than 5 years of experience - 60% of salary;

- with 5-8 years of experience - 80%;

- with more than 8 years of experience - 100%.

Starting from the 4th day of sick leave, the Social Insurance Fund reimburses him for the amounts spent on such benefits.

But there are situations when an employee of an enterprise is so valuable that his employer wants to pay up to one hundred percent of the amount, despite the length of service, for example, 6 years. The state does not compensate for the additional payment.

Moreover, from this additional 20% he is obliged to pay:

- 5.1% health insurance;

- 2.9% social insurance;

- 22% to the pension fund;

- starting from 0.2% for injuries.

Thus, when setting aside additional amounts for benefits for an employee, the employer must take into account how much he will actually have to spend.

From time to time, situations of the second type also occur - when the Social Insurance Fund denies an employee benefits for sick leave in the form of compensation to his employer. This usually happens by mistake when preparing documentation or due to some internal inconsistencies of the government agency.

The employer, wishing for a speedy recovery of the employee, can meet him halfway and still pay the amounts that he would have received as benefits. But, from the point of view of the state, this money cannot be considered a hospital benefit and is subject to all obligations regarding compulsory insurance funds.

Above you can see a list of these transfers to the state budget.

In such a situation, it is worth seeking, after the employee’s recovery, to recognize the Fund’s decision as erroneous and to transfer compensation for the entire period of illness to the employer with the return of payments.

Also, an agreement is possible between the sick person and his employer and the former will gradually return the amounts spent in the future.

When are payments made?

Expert opinion

Semenov Alexander Vladimirovich

Legal consultant with 10 years of experience. Specializes in the field of civil law. Member of the Bar Association.

Russian laws provide clear deadlines regarding mandatory insurance payments that the employer must adhere to. Otherwise, he will face an administrative penalty, which can be quite significant.

Today, payments to compulsory insurance funds, including insurance contributions for sick leave, if any are due, must be made before the 15th of the month following the issue of benefits. Of course, this day may fall on a weekend or holiday.

In this case, the payment deadline is postponed to the next working day after it. For example, if an employer added an additional 20% to the benefit in January, then he must transfer the necessary amounts to the state budget by February 15.

But the 15th day of the second winter month fell on a Sunday, which means that all debts to state funds can be paid off before February 16th.

The main document that must be filled out to pay the amounts due to the Social Insurance Fund or Pension Fund is a payment order. It will serve as proof of the debt fulfilled in the event of claims from government agencies.

Calculation example

If insurance premiums are charged on sick leave, then it all depends on the reason for this. The amount for which the calculation will be made depends entirely on whether it is an additional payment to the mandatory benefit or a complete replacement for it.

For example, consider the first situation. The employee fell ill and went on sick leave from May 11 to May 20, 2021 inclusive.

Thus, the duration of his illness according to the sick leave provided to the employer was 10 days. His insurance period, in turn, is 7 years, which is one year less than the period that the state established as a guarantee of 100% benefits.

But, the collective agreement between employees and the employer provides that the latter pays additional benefits from the company’s money up to 100%, regardless of the length of service of the employees, which also applies to our example.

The average daily earnings of a sick employee over the past year was 1,500 rubles. It is this that is taken as the basis for calculations.

But out of the additional 3,000 rubles you will have to pay:

- 660 rubles to the Pension Fund (3000 x 22%);

- 87 social insurance rubles (3000 x 2.9%);

- 153 rubles of medical insurance (3000 x 5.1%);

- 6 rubles for injuries (3000 x 0.2%).

The total amount of payments to various insurance funds was: 906 rubles.

The general rule is that sick leave is not subject to insurance contributions.

This is true. But in practice there are exceptions. For example, if the employer pays certain amounts in addition to sick leave benefits. In this case, he will still have to transfer all the necessary amounts to the Social Insurance Fund and Pension Fund.

In what cases is temporary disability benefits subject to insurance premiums? Are they accrued at any special rates and to which BCCs should they be transferred? As you can see, there are a lot of questions, although the answers to them are quite obvious.

Taxation of sickness benefits

Since funds received by an employee during a period of illness are one of the types of his income, they become subject to taxation.

What taxes are imposed on temporary disability benefits and what contributions are charged on them depends on:

- The tax regime adopted by the enterprise;

- The case in which incapacity for work occurred (due to illness, pregnancy and childbirth, caring for a sick family member, etc.).

The income of an individual is subject to personal income tax, mandatory contributions to the Pension Fund and insurance contributions. The obligation to withhold personal income tax applies to sickness benefits.

As for insurance premiums, they are not charged. The reason lies in the source of payments. If sick leave is paid at the expense of the Social Insurance Fund, then it is not rational to charge contributions for the fund, which itself paid.

Are sick leave contributions subject to contributions?

We will begin the answer to this question with the definition of the concept: SICK LEAVE. Despite the fact that this concept is currently widely used, it is absent in Russian legislation.

Instead, it talks about a certificate of incapacity for work, which is the basis for calculating temporary disability benefits. It is one of the state benefits for compulsory social services.

Expert opinion

Semenov Alexander Vladimirovich

Legal consultant with 10 years of experience. Specializes in the field of civil law. Member of the Bar Association.

insurance and therefore according to paragraphs. 1 p.

1 tbsp. 422 of the Tax Code of the Russian Federation is not subject to insurance premiums.

The same can be said about maternity benefits, called maternity benefits by many.

Errors when assessing sick leave benefits

There are frequent cases when errors in the preparation of sick leave lead to an incorrect amount of the required social payment. Errors can occur either due to human factors (arithmetic errors) or due to a computer program failure. When correcting such errors and for recalculation, the result of the error is taken into account - underpayment or excess of benefits.

If the benefit amount is less than required, a recalculation must be made and the amount for the previously unaccounted period must be paid. Moreover, if the source of the paid part of the benefit was both the employer and the Social Insurance Fund, then sick leave payment will be divided between these two organizations.

ATTENTION! Regardless of whose fault the error was made in calculating sick leave, the employer is responsible and becomes obliged to pay compensation in the amount established by the Central Bank of Russia for each day of delay.

After correcting the error and calculating the required amount of additional payment, you should expect payment on the next day you receive your salary.

If the benefit amount exceeds the required amount, it is possible to recover the excess amount only in two cases: if a calculation error occurred or if the policyholder provided incorrect (false) information that affected the amount of social benefits. In other circumstances, the excess can only be returned if the employee agrees to repay the amount or gives written permission for the excess to be withheld from the employee's next salary or benefit.

Related article: Features of zero calculation for insurance premiums and how to fill it out

After correcting the error, the corrected form should indicate:

- the reason for the error;

- correct calculation option;

- the amount of excess or underpayment;

- indicate the amount of personal income tax.

The corrected form for calculating social benefits is attached to the employer’s order. A copy of the order is sent to the Pension Fund.

To summarize from all of the above, it becomes clear that insurance premiums for sick leave in 2021 are taxable only if the employer exceeds the maximum payment limit. In addition, insurance payments are not subject to disability certificates due to pregnancy and childbirth.