Purpose of inventory of construction in progress

During the inventory, the commission must check the following:

- what is the condition of the construction projects, the construction of which has been temporarily interrupted or mothballed;

- Is there any special equipment included in the construction-in-progress that has been sent for repairs but has not yet been repaired?

For these objects, the commission must discover the reasons and grounds for conservation.

When listing the item “construction in progress”, those transactions that are recorded in the accounts are subject to verification:

- special equipment for installation (07);

- investments in non-current assets (08);

- settlements with contractors and suppliers (60).

Liability balance

Authorized capital

- this is the amount of funds initially invested by the owners to ensure the statutory activities of the organization; The authorized capital determines the minimum amount of property of a legal entity that guarantees the interests of its creditors

Extra capital

— a liability item on the balance sheet, consisting of the following elements:

- share premium

- the difference between the sale and par value of the company's shares; - exchange rate differences

- differences when paying for a share of the authorized capital in foreign currency; - the difference when revaluing fixed assets

is the difference when the value of fixed assets changes.

Reserve capital

- the size of the enterprise’s property, which is intended to place undistributed profits in it, to cover losses, repay bonds and repurchase shares of the enterprise, as well as for other purposes.

Short-term liabilities

Accounts payable

- the debt of a subject (enterprise, organization, individual) to other persons, which this subject is obliged to repay.

Reserves for future expenses

In order to evenly include upcoming expenses in production or distribution costs, the organization can create reserves for: upcoming payment of vacations to employees; payment of annual remuneration for long service; payment of remuneration based on the results of work for the year; repair of fixed assets; production costs for preparatory work due to the seasonal nature of production; upcoming costs for land reclamation and other environmental measures; upcoming costs of repairing items intended for rental under a rental agreement; warranty repairs and warranty service; covering other anticipated costs and other purposes provided for by the legislation of the Russian Federation, regulations of the Ministry of Finance of the Russian Federation.

Purpose of inventory of work in progress

The objectives of carrying out an inventory of unfinished construction are as follows:

- detection of product defects that are not taken into account in accounting;

- determining the availability of products and semi-finished products whose processing is not completed;

- checking the accounting information for the movement of semi-finished products and parts, as well as the total amount of costs for work in progress;

- checking whether costs are correctly distributed by type of goods, as well as the cost of manufactured goods;

- determining the actual completeness of the reserves and the provision of the assembly with the required parts;

- determination of work in progress balances for orders that were canceled, as well as for those orders whose execution was interrupted.

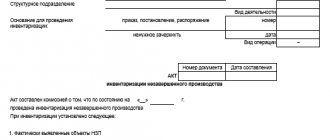

to “___” _____________ 19__

Based on order (instruction) N ____________________ dated “___” ___________ 19__, an inventory of the actual availability of valuables in safekeeping was carried out

| (job title) | (surname, name, name) |

Removing residues:

started “___” _______________ 19__,

finished “___” _______________ 19__

The following was established during the inventory:

| N p/p | Name of valuables, rub., kopecks. | Listed according to accounting data | Actual balances | Natural loss and normalized losses | Inventory results |

| surplus | shortage | ||||

| 1 | Cash | ||||

| 2 | Goods | ||||

| 3 | Tara | ||||

| 4 | Inventory | ||||

| 5 | |||||

| Total |

| Surplus | in total |

| Shortage | (in words) |

for the period from _______________ 19__ to ________________ 19__ with trade turnover in the amount

| rub. ____ kop. |

| (in words) |

| Chairman of the Commission | ||

| (job title) | (surname, name, name) | (signature) |

| Accountant | ||

| (surname, name, name) | (signature) | |

| Financially responsible person | ||

| (surname, name, name) | (signature) |

Explanation of reasons for surpluses or shortages

Financially responsible person

Decision of the head of the enterprise

| “___” _______________ 19__ |

| (signature) |

Organization of inspection

The procedure for taking inventory of work in progress must be reflected in the company's accounting policies.

First of all, the director of the organization must issue an order indicating the following information:

- the reasons for the inspection;

- types of property that fall under the inventory;

- composition of the commission that carries out the inspection;

- start and end date of the inspection;

- deadlines within which all necessary documents must be submitted to the accounting department.

We can say that this order is an assignment for the inventory commission.

The commission for inventory of unfinished construction objects may include accounting employees, administration employees and other employees. During the inspection, workers carrying the mat must be present. responsibility.

Document text:

Approved by order of the Ministry of Agriculture and Food dated June 14, 2011 N 233

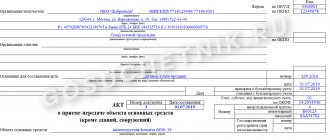

Industry form N ZPP-147 ——————- Code according to OKPO ¦ ¦ ——————- ______________________________ I approve: (organization) Manager ____________ signature “___” _________ 20__ ACT OF INVENTORY OF WORK IN PRODUCTION on “___” ___________ 20___ Compiled by a commission consisting of: Ch. engineer _________________________, head production _______________________, beginning PTL (Deputy Director for Quality) ____________________, art. shop foreman ___________________ and ch. accountant ______________________ that when removing the balances, the following presence of raw materials in work in progress was established: I. In the drying chambers - corn on the cob ———————————————————————— — ¦ N ¦N chamber¦ N control ¦ Type, variety ¦Quantity,¦ Humidity ¦ts-%¦ ¦p/p¦ ¦ cards ¦ corn ¦ kg ¦ cobs, % ¦ ¦ +—+———+— —————+————-+——-+—————+—+ ¦ 1 ¦ 2 ¦ 3 ¦ 4 ¦ 5 ¦ 6 ¦ 7 ¦ +—+———+———— ——+————-+——-+—————+—+ ¦ 1 ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+ ——-+—————+—+ ¦ 2 ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+————— +—+ ¦ 3 ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+—————+—+ ¦ 4 ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+—————+—+ ¦ 5 ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+——— +——————+————-+——-+—————+—+ ¦ 6 ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+— ———-+——-+—————+—+ ¦ 7 ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+ —————+—+ ¦ 8 ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+—————+—+ ¦ 9 ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+—————+—+ ¦10 ¦ ¦ ¦ ¦ ¦ ¦ ¦ + —+———+——————+————-+——-+—————+—+ ¦11 ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——— ———+————-+——-+—————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ —-+———+——————+————- +——-+—————+—- Reverse side of industry form N ZPP-147 ————————————————————————— ¦ N ¦N silage¦ N entry in the book ¦ Type, grade ¦Quantity,¦ Moisture ¦ts-%¦ ¦p/p¦ ¦ accounting ¦ corn ¦ kg ¦ cobs, % ¦ ¦ +—+———+———— ——+————-+——-+—————+—+ ¦ 1 ¦ 2 ¦ 3 ¦ 4 ¦ 5 ¦ 6 ¦ 7 ¦ +—+———+——————+ ————-+——-+—————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+ —————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+—————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+—————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+— ——+——————+————-+——-+—————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+—————+ ————-+——-+—————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+ —————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+—————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+—————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+— ——+——————+————-+——-+—————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+—————+ ————-+——-+—————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+———+——————+————-+——-+ —————+—+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ —-+———+——————+————-+——-+—————+—- Ch. engineer _____________________________________ (signature, transcript of signature) Head. produced by ______________________________ (signature, transcript of signature) Beginning. PTL (Deputy Director for Quality) ______________________________ (signature, transcript of signature) Art. shop foreman ________________________________ (signature, transcript of signature) Ch. accountant __________________________________ (signature, transcript of signature) “___” ______________ 20____

Tags: asset, Form, accountant, capital, loan, tax, order, expense

Inventory procedure

The chairman of the commission must put on all documents on receipts and expenses necessary for the inspection, the notes “before the inventory on a certain date.” This is necessary in order to record information about the remainder of the property before starting the inventory.

The financially responsible employee must write a receipt stating that all primary papers were transferred to the accounting department, all received property was capitalized, and disposed property was written off as expenses. Only after this can an inventory of work in progress be carried out.

The commission begins to calculate the actual availability of property. Information about its quantity is recorded in inventories and acts, drawn up in at least two copies.

The inventory document must be numbered, it must indicate the date of the inventory, the date and number of the order to conduct the inspection. After this, tables are generated for each workshop and the location of work in progress.

After the inspection report is completely completed, it must be signed by all members of the commission, as well as the persons carrying the mat. responsibility.

Inventory of work in progress and deferred expenses: regulatory documents

To properly organize and conduct an inventory of work in progress (WIP), you must be guided by:

- Order of the Ministry of Finance of the Russian Federation on the Regulations on accounting and reporting in the Russian Federation dated July 29, 1998 No. 34n. Paragraphs 26–28 of the order set out when and in what cases it is necessary to carry out an actual inspection, as well as how identified surpluses and shortages should be taken into account; paragraphs 63–65 define what applies to work in progress and deferred expenses.

- Order of the Ministry of Finance of the Russian Federation on Methodological guidelines for inventory of property and financial obligations dated June 13, 1995 No. 49. Clauses 3.27–3.35 of the order indicate the procedure for the commission to verify work in progress, deferred expenses and reflect the results in the drawn up act.