Concept and organization of accounting in the Russian Federation

Organization of accounting is a set of system-forming elements and conditions of the accounting process necessary for the formation of complete and reliable information about the economic activities of an enterprise.

In order to comply with the law when carrying out business transactions, accounting must be organized at each enterprise. The head of the organization is responsible for this.

Depending on the volume of work, the manager can choose one or another form of accounting work:

- Approve the “Accounting” division in the organizational structure, headed by the chief accountant;

- Introduce into the staffing table the position of a single person accountant;

- Transfer, on contractual terms, the maintenance of accounting to a centralized accounting department, a consulting firm or a specialist accountant;

- Maintain accounting records in person.

The basic principles of accounting are determined by the legislation of the Russian Federation on accounting. The regulation of accounting on a national scale consists of the development and approval of regulatory documents for all enterprises on the territory of the Russian Federation:

- Federal Law on Accounting;

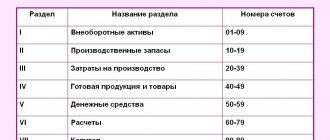

- Charts of accounts and instructions for use;

- Accounting Regulations (Standards);

- Other regulations and guidelines on accounting issues.

Why is accounting regulation necessary?

Legal regulation of accounting allows the state to establish a number of norms and rules, compliance with which is mandatory for all persons engaged in economic activities.

The general methodological regulatory regulation of accounting in the Russian Federation is carried out by the Russian government, which develops and approves rules for documenting and recording various business transactions.

In accordance with paragraph “r” of Art. 71 of the Russian Constitution, accounting is the responsibility of the state. Methodological regulation of accounting is entrusted by the Russian government to the Ministry of Finance. The regulation of certain aspects of accounting by a number of federal laws is entrusted to such regulators as the Central Bank, the Federal Financial Markets Service, etc., within the limits established by the Ministry of Finance. Accounting is regulated through the adoption of various laws, regulations and various regulations.

Documents regulating the organization of accounting

- Federal Law “On Accounting” No. 402-FZ dated December 6, 2011;

- Regulations on accounting and financial reporting in the Russian Federation, approved. by order No. 34n dated July 29, 1998. (as amended on March 29, 2017);

- Chart of accounts for accounting of financial and economic activities of organizations and Instructions for its application, approved. by order No. 94n dated October 31, 2000. (as amended on November 8, 2010);

- “Regulations on accounting of long-term investments” (approved by letter of the Ministry of Finance of the Russian Federation dated December 30, 1993 No. 160);

- Civil Code of the Russian Federation;

- Accounting policy of the organization.

The Ministry of Finance of the Russian Federation forms a special group of normative documents regulating the accounting procedure for individual areas: standards:

- Accounting Regulations (PBU). They are developed taking into account the main provisions of international accounting standards.

List of current PBUs adopted by the Ministry of Finance of the Russian Federation

- PBU 1/2008 Accounting policy of the organization, approved. by order of the Ministry of Finance of Russia dated October 6, 2008 N 106n;

- PBU 2/2008 Accounting for construction contracts, approved. by order of the Ministry of Finance of Russia dated October 24, 2008 N 116n;

- PBU 3/2006 Accounting for assets and liabilities in foreign currency, approved. by order of the Ministry of Finance of Russia dated November 27, 2006 N 154n;

- PBU 4/99 Financial statements of the organization, approved. by order of the Ministry of Finance of Russia dated July 6, 1999 N 43n;

- PBU 5/01 Accounting for inventories, approved. by order of the Ministry of Finance of Russia dated 06/09/2001 N 44n;

- PBU 6/01 Accounting for fixed assets, approved. by order of the Ministry of Finance of Russia dated March 30, 2001 N 26n;

- PBU 7/98 Events after the reporting date, approved. by order of the Ministry of Finance of Russia dated November 25, 1998 N 56n;

- PBU 8/2010 Estimated liabilities, contingent liabilities and assets, approved. by order of the Ministry of Finance of Russia dated December 13, 2010 N 167n;

- PBU 9/99 Income of the organization, approved. by order of the Ministry of Finance of Russia dated 05/06/1999 N 32n;

- PBU 10/99 Organizational expenses, approved. by order of the Ministry of Finance of Russia dated May 6, 1999 N 33n;

- PBU 11/2008 Information on related parties, approved. by order of the Ministry of Finance of Russia dated April 29, 2008 N 48n;

- PBU 12/2010 Information on segments, approved. by order of the Ministry of Finance of Russia dated November 8, 2010 N 143n;

- PBU 13/2000 Accounting for state aid, approved. by order of the Ministry of Finance of Russia dated October 16, 2000 N 92n;

- PBU 14/2007 Accounting for intangible assets, approved. by order of the Ministry of Finance of Russia dated December 27, 2007 N 153n;

- PBU 15/2008 Accounting for expenses on loans and credits, approved. by order of the Ministry of Finance of Russia dated October 6, 2008 N 107n;

- PBU 16/02 Information on discontinued activities, approved. by order of the Ministry of Finance of Russia dated July 2, 2002 N 66n;

- PBU 17/02 Accounting for expenses on R&D and technological work, approved. by order of the Ministry of Finance of Russia dated November 19, 2002 N 115n;

- PBU 18/02 Accounting for corporate income tax calculations, approved. by order of the Ministry of Finance of Russia dated November 19, 2002 N 114n;

- PBU 19/02 Accounting for financial investments, approved. by order of the Ministry of Finance of Russia dated December 10, 2002 N 126n;

- PBU 20/03 Information on participation in joint activities, approved. by order of the Ministry of Finance of Russia dated November 24, 2003 N 105n;

- PBU 21/2008 Change in estimated values, approved. by order of the Ministry of Finance of Russia dated October 6, 2008 N 106n;

- PBU 22/2010 Correction of errors in accounting. accounting and reporting, approved. by order of the Ministry of Finance of Russia dated June 28, 2010 N 63n;

- PBU 23/2011 Cash flow statement, approved. by order of the Ministry of Finance of Russia dated 02.02.2011 N 11n;

- PBU 24/2011 Accounting for costs for the development of natural resources, approved. by order of the Ministry of Finance of Russia dated October 6, 2011 N 125n;

Concept and features of the regulatory system

There are 4 levels of legislative acts, divided by level of importance and priority:

- Federal Law “On Accounting”.

- Regulations on the implementation of accounting.

- Chart of Accounts, Regulations on Document Flow.

- Instructions and guidelines regarding the use of accounting provisions.

What is the status and application of accounting regulations and industry standards ?

General management of accounting is the responsibility of the Government of the Russian Federation. Each company, based on existing standards, must independently determine its accounting policies. Its various provisions may differ depending on the needs of the company or specific industry. However, the points that the organization itself introduces should not contradict adopted laws. At the moment, an accounting reform is being carried out in the Russian Federation. The basics of accounting are brought into line with international standards. The reform concerns such areas as:

- Improved regulations that enable effective detection of violations and enforcement of the law.

- Foundation of adequate standards.

- Formation of methodological instructions: instructions, comments, etc.

- Creation of an educational system (for example, advanced training).

- Bringing laws into line with regulations.

One of the objectives of the reform is to maintain the stability of the regulatory system.

How is an organization’s accounting policy formed if keeping records of objects according to accounting standards leads to unreliable presentation of information in reporting ?

Federal Law of the Russian Federation on Accounting

The main legislative act regulating accounting is the federal law “On Accounting”, N 402-FZ dated December 6, 2011 . The Accounting Law regulates the following issues:

- Defines objects and basic requirements for accounting;

- Reveals the basic concepts used in the legislative regulation of accounting;

- Establishes the rights and obligations of officials of the enterprise, as well as liability for violation of the requirements of the legislation on accounting;

- Determines the main tasks of accounting, requirements for the preparation and maintenance of primary accounting documents and accounting registers;

- Establishes deadlines and general requirements for conducting an inventory of the property and liabilities of the enterprise;

- Establishes deadlines, general requirements and procedures for submitting financial statements;

The legislative framework

The Federal Law of the Russian Federation on Accounting is the necessary milestone on which the entire accounting system of the country is built. It provides not only the necessary legislative framework for effective financial accounting of varying degrees of significance in our country, but also helps resolve disputes that may arise.

It describes in detail and discusses clear definitions of accounting, how it should be maintained, within what framework of the law it is allowed to be, and also spells out the basic requirements for documentation and reporting. It also directly regulates the accounting system itself as a process.

Regulations on accounting and reporting of the Russian Federation

Regulations on accounting and financial reporting in the Russian Federation, approved. by order No. 34n dated July 29, 1998. establishes the procedure for organizing and maintaining accounting, drawing up and submitting financial statements by legal entities. It was developed on the basis of the Law “On Accounting” and clarifies the application of certain requirements of the law. The provision is secondary in relation to the Law “On Accounting” and is the basis for all regulatory documents developed by the Ministry of Finance of the Russian Federation. The regulation establishes the possibility of choosing from two or more options for reflecting individual business transactions. For example, an enterprise can choose the method and form of accounting, the method of assessing materials, methods of calculating depreciation of fixed assets and intangible assets, etc. In order for the accounting of an enterprise to comply with the requirements of the regulations, it is necessary to ensure constant monitoring of the state of the legislative and regulatory framework.

How is the accounting regulatory system structured in Russia?

The system of regulatory regulation of accounting has its own hierarchy (guiding documents are listed in descending order of importance):

- Law No. 402-FZ.

- Regulations on accounting and reporting, approved by order of the Ministry of Finance of Russia dated July 29, 1998 No. 34n.

- Chart of accounts and FSB/PBU, as well as regulations on documents and document flow in accounting, approved by the Ministry of Finance of the USSR on July 29, 1983 No. 105. To date, two FSBs have been adopted.

From 2021, FAS 5/2019 “Inventories” will begin to be applied (it will replace PBU 5/01), and from 2022, FAS 25/2018 for lease accounting will become mandatory. The procedure for accounting for inventories under the new FSBU 5/2019 differs significantly from the current one. Analytical material from ConsultantPlus will help you rebuild your accounting starting in 2021. You can get trial access to the system for free. - Instructions and methods, as well as local regulatory documents.

With the help of clearly defined rules, fiscal authorities can monitor the degree of compliance and hold violators accountable.

In developing the rules for maintaining and organizing accounting in Russia, information from the Accounting Reform Program in accordance with international financial reporting standards, approved by government decree No. 283 dated March 6, 1998, is taken as a basis.

System of legal acts regulating accounting

First, let's look at what regulations need to be followed when organizing and maintaining records and reporting (Articles 3, 5 of the Law of November 21, 1996 N 129-FZ). For clarity, we built a pyramid out of them, arranging legal acts according to their legal force from the top of the pyramid (greater legal force) to the base (less legal force).

The chart of accounts and financial reporting forms recommended by the Ministry of Finance contain only technical issues of accounting and reporting (Clause 2 of Article 5 of the Law of November 21, 1996 N 129-FZ). There are no accounting rules in them.

But the explanations (letters) of the Ministry of Finance on issues of accounting regulation are not normative legal acts (Clause 2 of the Rules, approved by Decree of the Government of the Russian Federation of August 13, 1997 N 1009). Therefore, decide for yourself whether to take into account the position of the supervisory authority expressed in them or not. By the way, if you have doubts about how to carry out a particular operation, you can try to make an official request to the Russian Ministry of Finance. But, as a rule, from there comes a reply like “the competence of the Ministry of Finance does not include advising commercial organizations on accounting issues” or “applications from organizations to assess specific economic situations are not considered by the Ministry of Finance.” On the other hand, if you come across a letter from the Ministry of Finance, although not addressed to you, but with one hundred percent your situation and with an answer beneficial to you, then use it. For example, according to the Russian Ministry of Finance, the selling organization, during the period of registration of the transfer of ownership of real estate transferred to the buyer, must reflect the disposal of the object from the OS. To do this, the object can be accounted for on account 45 “Goods shipped”, a separate sub-account “Transferred real estate objects” (Letter of the Ministry of Finance of Russia dated March 22, 2011 N 07-02-10/20). This means that property tax on this property will not be paid during the registration period. By the way, the Supreme Arbitration Court of the Russian Federation also agrees with this (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated March 29, 2011 N 16400/10). As for international reporting standards (IFRS), today they have already been included in the current regulatory system of Russian accounting. The Ministry of Finance of Russia gave them official status by issuing an Order on the implementation of IFRS and clarifications of IFRS (Order of the Ministry of Finance of Russia dated November 25, 2011 N 160n; paragraphs 7, 23 of the Decree of the Government of the Russian Federation dated February 25, 2011 N 107). But not everyone is required to prepare reports according to international standards - for now these are only credit and insurance companies, and from 2015 they will be joined by companies whose securities are traded on the stock markets of other countries. And ordinary organizations apply the rules of international standards if Russian PBUs do not establish the method of accounting for any transaction (Clause 7 of PBU 1/2008).

What documents represent the second level?

As for the official regulatory documentation of the Russian Federation concerning accounting, its next level consists of a system of regulatory provisions for accounting. accounting. What does this mean?

This part of the documents is called normative, because it is in it that the basic norms for the functioning of accounting as such are spelled out. They contain very important information as follows:

- rules for maintaining direct accounting;

- rules for submitting accounting information on various accounting objects;

- a mandatory list of necessary information that must be shown in the financial statements is submitted;

- established international accounting standards.

We can say that documents at this level are intended to explain in a more accessible way the legal basis of the federal law on accounting. accounting in the Russian Federation, which is accepted at the highest level and may not always be understandable to beginners in the field of accounting.

Documents of the fourth level of regulation

Documentation belonging to this category is not so significant in the scale of its effect, but this does not make it any less important for the general accounting system of the Russian Federation. It directly represents the working documents of organizations that deal with accounting.

They spell out the basic working provisions and rules for working with accounting and reporting in any of the ways that are currently offered by the Ministry of Finance of the Russian Federation.

Naturally, they are intended exclusively for internal use at enterprises, because they are approved by the immediate manager of a particular organization.