Where are short-term loans and borrowings reflected on the balance sheet?

The form of the balance sheet was approved by Order of the Ministry of Finance dated July 2, 2010 No. 66n. In this form, 2 lines in the liability are intended to reflect debt on loans and borrowings:

- 1410 “Borrowed funds”;

- 1510 “Borrowed funds”.

Naturally, we are talking about loans and borrowings received. After all, issued loans that meet the criteria for financial investments specified in paragraph 2 of PBU 19/02 are part of the organization’s assets. We talked about accounting for financial investments and their reflection in the balance sheet in this material.

The above lines 1410 and 1510 of the balance sheet are included in long-term and short-term liabilities, respectively.

Short-term loans and borrowings in accordance with the Chart of Accounts and the Instructions for its application are reflected in account 66 “Settlements for short-term loans and borrowings” (Order of the Ministry of Finance dated October 31, 2000 No. 94n). Therefore, we can say that the balance of short-term loans and borrowings, i.e. the credit balance of account 66 as of the reporting date, should be reflected on line 1410.

But here it is necessary to take into account that the balance of account 67 “Long-term loans and borrowings” can be transferred in whole or in part to line 1410. This is possible if, as of the reporting date, account 67 contains liabilities whose maturity as of that date does not exceed 12 months. After all, the Chart of Accounts and the Instructions for its application do not provide for the transfer of short-term credits and borrowings from account 67 to account 66 (Order of the Ministry of Finance dated October 31, 2000 No. 94n). And the remaining balance of account 67 (in terms of long-term loans and borrowings) should be transferred to line 1410 (Order of the Ministry of Finance dated July 2, 2010 No. 66n).

You can read about filling out other balance sheet lines here.

Short-term liabilities on the balance sheet: varieties

Debts with a short repayment period can be divided into 3 groups:

| Type of short-term liabilities | Details |

| Debts that must be paid within 1 year | The 12 month count starts from the date of reporting. |

| Operating | This may include: – tax payments, – advances received, – current payments to the budget, - rental payments, – advances paid, – debts for materials received for production activities, – accrued wages to staff (not yet paid). |

| Money to pay off debts with a repayment period of up to 1 year | This group includes: – staff vacation payments, – bonuses to salaries, – other short-term debts. |

What is the difference between a loan and a loan?

A loan represents funds transferred by a credit institution to a borrower. In this case, the latter pays interest for the use of such borrowed funds.

An important difference between a loan and a credit is that a loan is borrowed funds from organizations and individuals, expressed in money or their equivalent in kind.

Taking into account these definitions, we can highlight how a loan differs from a loan:

- a loan is issued only by a bank, and a loan can be provided by individuals, organizations and individual entrepreneurs;

- a loan implies payment of interest to the lender for using the amount issued; the issuance of loans does not contain such a mandatory condition: they can be interest-free;

- a loan is issued exclusively in cash, a loan - both in money and in the form of an equivalent in kind (in goods, for example).

What entries does the accounting of loans and borrowings received contain?

In accounting there are no special differences between a loan and a loan. Thus, the rules for accounting for loans and borrowings in accounting are described in PBU 15/2008 “Accounting for expenses on loans and credits.”

The costs should include:

- interest on loans and borrowings;

- other associated costs: payment for consulting and information services, expert assessment of the loan agreement, etc.

Interest, according to clause 8 of PBU 15/2008, is taken into account in one of the following ways:

- evenly throughout the entire term of the contract,

- in the manner prescribed by the terms of the contract, if this does not violate the uniformity of their accounting.

Other costs associated with loans and borrowings should be taken into account evenly throughout the entire term of the contract.

Accounting for borrowed assets is carried out using the following accounts:

- 66 - under contracts valid for 12 months or less;

- 67 — under contracts valid for more than 12 months.

We will consider the accounting procedure for received loans and borrowings using examples.

Composition of obligations

The obligations can be divided as follows:

- Related to current operations. This includes tax payments, advances and wages to employees, rent payments, payments for materials and goods supplied under the contract.

- Liabilities that are subject to liquidation within a year after the financial statements are prepared. These may be long-term obligations that must be repaid in the near future.

- Liabilities that must be settled within one year of the balance sheet. This includes payment of compensation for unused vacation, bonuses, etc.

The most common types include the following:

- Accounts payable is the amount that the debtor is obliged to pay as payment for goods delivered or services received that are necessary for the functioning of the enterprise. Its size is stipulated by the terms of the contract.

- Short-term bills are invoices for goods and services supplied that were not purchased for the main activities of the organization.

- The share of long-term debt that must be repaid in the next reporting period.

- Accrued payments. They include loan payments to the bank and employee salaries.

- Cash payments that an organization makes at the request of a creditor.

- An advance payment towards a future transaction. This also includes deposits.

- An advance payment received for a future supply of goods or for the provision of a service.

- Tax deductions to federal and local budgets.

- Debt for employee vacations (so-called estimated liabilities). Its occurrence is a consequence of the reluctance of employees to go on vacation during the reporting period.

- Dividends that must be calculated for all owners of shares and bonds of the enterprise.

Current liabilities include debts that must be repaid in the near future

An example of accounting for a loan received

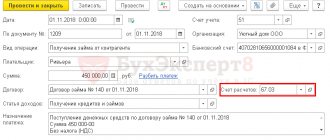

The organization received a loan on February 2 in the amount of RUB 1,500,000. Interest rate - 10%. The term of the loan agreement is 24 months. The monthly payment amount is RUB 62,500. The agreement with the bank provides for payment of interest and repayment of the loan amount monthly on the last day of each month. Interest accrues from the next day after receiving the loan.

In February, the organization will make the following transactions:

Dt 51 Kt 67.1 - a loan was received to the organization’s current account in the amount of RUB 1,500,000.

Dt 91.2 Kt 67.2 - interest accrued on the loan: 1,500,000 / 365 × 26 × 10% = 10,684.93 rubles.

Dt 67.2 Kt 51 - payment of interest - 10,684.93 rubles.

Dt 67.1 Kt 51 - partial repayment of the loan - 62,500 rubles.

Postings in March:

Dt 91.2 Kt 67.2 - interest accrued on the loan: (1,500,000 – 62,500) / 365 × 31 × 10% = 12,208.90 rubles.

Dt 67.2 Kt 51 - payment of interest - 12,208.90 rubles.

Dt 67.1 Kt 51 - partial repayment of the loan - 62,500 rubles.

This loan, being long-term, will be reflected on line 1410 “Borrowed funds” of the balance sheet in the amount recorded in the credit balance of account 67.

If the loan were short-term, it should be reflected in line 1510 “Borrowed funds” of the balance sheet.

Commercial loans and commercial bills are shown by lines:

- 1450 “Other liabilities” (for long-term debt);

- 1520 “Accounts payable” (for short-term debt).

It should be noted that if funds were received for the purpose of acquiring, constructing or manufacturing an investment asset, interest must be reflected using account 08 “Investments in non-current assets” (Dt 08 Kt 66.2/67.2). An exception to this rule is made for business entities that keep records in a simplified way, which have the right to use account 91.2 for these purposes (clause 7 of PBU 15/2008).

Displaying the company's borrowed funds in the balance sheet

The amount of an interest-bearing loan provided in kind should be determined based on the value of assets transferred or to be transferred by the organization. Such value is established based on the price at which, in comparable circumstances, the organization usually determines the value of similar assets. Own working capital 2. Short-term bank loans and borrowings (line balance 611 + 612) 3. Settlements with creditors for commodity transactions (line balance 612 + 622 + 627) 4.

Organizations have the right to independently determine the detail of indicators for reporting items. Therefore, in principle, an organization can add decoding lines to drill down the indicator by page.

In this case, the entry that is created at the time the borrowed funds are received into the organization's current account is valid: In addition to the main body of the loan, interest on the use of the loan, which is the income of the lender, is taken into account in separate sub-accounts 66 and 67 of the account.

The interest that the recipient must pay on the loan is usually specified in the agreement. If there is no such condition in it, then they are calculated based on the refinancing rate in effect at the time of loan repayment. The company has the right to issue an interest-free loan.

To do this, the balance sheet is supplemented with the appropriate lines (for example, 1521 “Debt to suppliers and contractors”, 1522 “Debt on taxes and fees”, etc.).

In this case, the amount of interest due for payment is automatically reflected as part of short-term liabilities on line 1510 “Borrowed funds”, regardless of which account (66 or 67) this interest is recorded.

After all, the Instructions for the chart of accounts establish only uniform approaches to reflecting transactions in accounting accounts.

How to reflect issued loans and borrowings in accounting?

To reflect loans in accounting, the lender uses account 58 “Financial investments”.

The organization issued a loan on March 1 for a period of 1 year. Loan amount - RUB 3,000,000. The interest rate on the loan is 15% per annum. In accordance with the terms of the agreement, the borrower pays interest for each day of use of the loan at the end of each month. Interest begins to accrue from the day following the day the loan is issued. The Agreement does not provide for partial repayment of the loan amount on a monthly basis.

In October the lender reflected:

Dt 58 Kt 51 - loan issuance - 3,000,000 rubles.

Dt 76 Kt 91.1 - interest accrued: 3,000,000 / 365 × 30 × 15% = 36,986.30 rubles.

Dt 51 Kt 76 - interest received from the borrower - RUB 36,986.30.

Postings in April:

Dt 76 Kt 91.1 - interest accrued for April: 3,000,000 / 365 × 30 × 15% = 36,986.30 rubles.

Dt 51 Kt 76 - interest received - RUB 36,986.30.

Dt 76 Kt 91.1 - interest accrued: 3,000,000 /365 × 31 × 15% = 38,219.18 rubles.

Dt 51 Kt 76 - interest was credited to the current account - RUB 38,219.18.

...and so on until February 28 of the next year.

The lender will reflect the loan amount in the balance sheet on line 1170 “Financial investments” in the amount of RUB 3,000,000.

Accounting for interest-free loans issued

Let's consider the conditions from example 2, and assume that the agreement provided for the issuance of an interest-free loan.

Then the lender’s postings will look like this:

Dt 76 Kt 51 - issuance of an interest-free loan of 3,000,000 rubles.

The next and last entry in the lender's accounting will be entry Dt 51 Kt 76 (it will appear on the day the loan is repaid).

IMPORTANT! Loans issued on interest-free terms are not financial investments for the lending company (clause 2 of PBU 19/02), since the essential condition for recognizing assets as such is not met: their ability to generate income. At the same time, a loan issued that includes interest will be considered as such (clause 3 of PBU 19/02).

In the lender's reporting, the loan issued will be reflected in line 1230 “Receivables”. In this case, the organization can detail the type of receivables in the balance sheet: short-term debt with a maturity of 12 months or less and long-term debt with a maturity of more than 12 months.

Read how to account for an interest-free loan issued to an employee here.

What are the features of tax accounting for loans and borrowings?

Received credit or borrowed funds are not income for the purpose of calculating income tax for their recipient due to the provisions of sub. 10 p. 1 art. 251 Tax Code of the Russian Federation. Also, the funds issued are not an expense, taking into account the provisions of clause 12 of Art. 270 Tax Code of the Russian Federation. Likewise, funds received and paid to repay a loan or loan are not considered income or expenses.

In this case, the amounts of accrued and paid interest are fully recognized as non-operating expenses in accordance with subparagraph. 2 p. 1 art. 265 Tax Code of the Russian Federation. The moment of reflection of interest amounts in expenses is determined in accordance with clause 8 of Art. 272 Tax Code of the Russian Federation:

- at the end of each month,

- on the date of repayment of the loan or loan (if they are fully repaid).

The amount of interest in the presence of controlled debt is included in non-operating expenses in the amount provided for in Art. 269 of the Tax Code of the Russian Federation.

Interest received under agreements on the issuance of loans and borrowings relates to non-operating income (clause 6 of Article 250 of the Tax Code of the Russian Federation).

It should be noted that differences in accounting and tax recognition of accrued interest expenses for an investment loan or in the presence of controlled debt give rise to temporary differences accounted for in accordance with PBU 18/02 “Accounting for corporate income tax calculations.”

Features of calculating net debt

In order to perform such calculations and assess the financial condition of the company, you need to take into account many nuances. First of all, this concerns the availability of a package of receivables, which include such types of agreements as:

- Loans received from lenders and investors.

- Papers about the sale and purchase of real estate or property. Only objects are taken into account, which are then exchanged for specific financial resources.

- Financial checks and papers demonstrating settlements for various transactions. Documents confirming certain indicators.

Other nuances include the fact that long-term and medium-term indicators need to be compared with the average values for a specific area. If a firm's debt levels are higher than what is generally accepted in the industry, then there is cause for concern.

This is due to the fact that companies will be a source of concern for directors, investors, and creditors. They will refuse to provide loans or invest money, since the data obtained will indicate that management does not know how to develop a flexible plan for maneuvering in the market.

In turn, this causes distrust among shareholders and a desire to withdraw their money from the company’s turnover. Net debt can be calculated taking into account a special analytical indicator, which is equal to the amount of profit received before deducting expenses for paying taxes, interest on loans and depreciation (already accrued) .

It is used to compare company data with similar indicators in the region. As a result, the efficiency of the enterprise is assessed without taking into account its debt to creditor banks and the state.

The depreciation method is also not taken into account. This analytical indicator helps the company see the size of its net debt in order to know how much available funds can be used to pay it off.

It is also worth considering that there is a type of debt - guarantees to third parties, which affects the net debt indicator. This type of financial documentation can provide the company with security, because The guarantor bears some degree of responsibility for a particular debtor.