Regular bonuses

Regular bonuses are incentive payments upon achievement of predetermined results. They are permanent and are included in the wage system. If the bonus conditions are met, the employee receives a pre-agreed remuneration. If the conditions are not met, the premium is not paid.

Regular bonuses, in turn, are divided into:

- Monthly.

They are paid every month along with the salary and are included in the average salary of the employee.

- Quarterly.

Paid based on the employee's performance for the quarter. Typically, such bonuses are issued for the 1st, 2nd and 3rd quarters.

- Annual.

The calculation period for calculating this bonus is from January 1 to December 31. It is paid once a year, subject to the fulfillment of a production task.

Data on regular bonuses are not entered into the employee’s work book or personal card.

One-time bonuses

These payments are one-time in nature and are not included in the wage system. In most cases, a one-time bonus is paid not when certain indicators are achieved, but based on the results of an overall assessment of the employee’s work.

Bonuses that are not part of the remuneration system are not taken into account when calculating the employee’s average earnings. They also cannot be the subject of a labor dispute, since their payment is at the discretion of the employer. But this type of incentive must be entered into the employee’s work book and personal card (clause 4 of article 66 of the Labor Code of the Russian Federation, clause 24 of the Rules for maintaining and storing work books, approved by Decree of the Government of the Russian Federation of April 16, 2003 No. 225).

A one-time bonus is given to an employee on the basis of an incentive order signed by the director of the organization. You can familiarize yourself with the procedure for drawing up and a sample of this document in the article “One-time bonus: sample order”.

An incentive order is drawn up on the basis of a submission (petition or memo) to reward an employee. In this document, the employee’s immediate supervisor evaluates his work and argues for the need to assign him a bonus. The head of the organization, on the basis of this document, issues an order for incentives.

You can find out more about how to write a memo for employee bonuses in this article.

One-time bonuses can be divided into two types:

- Production.

Expert opinion

Gusev Pavel Petrovich

Lawyer with 8 years of experience. Specialization: family law. Has experience in defense in court.

The basis for paying such a bonus may be the achievement of certain work results, conscientious and high-quality performance of one’s duties, or the completion of an important or urgent task.

- Non-productive.

Their payment is not tied to work results, but to specific events: public holidays, anniversaries, the employee’s retirement or the birth of a child.

Conditions for payment of bonuses

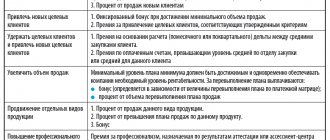

The indicators at which an employee is paid a bonus are:

- High quality.

They are determined not by the number of actions performed, but by their result (quality). These indicators include: a high level of customer service, the absence of comments and errors in work, the introduction of new innovative ideas into production.

Qualitative bonus indicators are suitable for assessing the work of employees not involved in the production process.

- Quantitative.

Such indicators have a clear numerical expression. These include: concluding a certain number of transactions, fulfilling a plan for the production of goods, selling a large number of goods. Quantitative assessment of labor is more suitable for workers involved in the production process.

Bonus conditions are prescribed in the Regulations on Bonuses, an employment contract or other local regulatory act (LNA). You can learn how to draw up a Regulation on bonuses for employees from this article.

If the bonus is not included in the remuneration system (one-time bonus), the conditions for its payment do not need to be specified separately. More information about the reasons for rewarding employees can be found here.

What if the company has losses?

If the company’s business is not going well this year, is it worth spending money on paying a bonus based on its results? It's up to the employer to decide.

According to the law, the payment of bonuses must depend on the indicators that were included in the Regulations on Bonuses when formulating the conditions. If the indicators are exclusively production, then losses will deprive the opportunity to bonus employees. But if other factors are included in the conditions, and the funds make it possible to find funds to pay incentives, then even in the event of losses, employees can receive their 13th salary, which should encourage them to work more efficiently next year.

Let's sum it up

- Bonuses are divided into two types: regular, paid on an ongoing basis, and one-time, transferred at a time.

- Data in the employee’s work book and personal card is entered only about one-time bonuses.

- The conditions for permanent bonuses must be specified in the LNA; for one-time bonuses, this need not be done.

The types of bonuses to employees are determined by the employer or by the provisions of local acts, collective agreements, and agreements. In the article we will analyze the issues of bonuses for employees, highlight the main types of bonuses, and talk about the procedure for securing incentive payments.

What types of bonuses are there for employees - the main classifications of types of bonuses and their differences

The current legislation does not establish types of bonuses. In Art. 191 of the Labor Code of the Russian Federation states that bonuses are incentive payments for conscientious performance of duties. In practice, organizations pay various types of bonuses, which can be classified:

By the number of employees awarded:

- Individual awards. Paid to a specific employee.

- Collective awards. Paid to a group of employees. They can work in the same department or division. As a rule, bonuses are paid when joint results are achieved in work activities, for example, the fulfillment of certain indicators.

In order to determine the amount of payments:

- In a fixed amount of money.

- As a percentage of salary.

- In shares of salary.

- As a percentage or fraction of the total salary (for example, from salary + bonus for length of service, etc.).

According to the frequency of accrual.

- One-time.

- Systematic. They can be paid once a month, once a quarter, semi-annually or annually.

Based on the basis for calculation.

- For good work.

- For fulfilling the plan.

- For any other employee achievements.

According to the method of consolidation in the organization:

- Enshrined in employment contracts.

- Collective agreements.

- Local acts.

- Agreements.

- Not fixed in internal documents, paid at the initiative of the manager (these bonuses are not provided for in the remuneration system).

Next, let's talk about the main types of employee bonuses that are most often found in organizations.

Annual bonus

This type of bonus is calculated at the end of the year, usually in February of the year following the reporting year. The annual bonus is not a mandatory payment for the employer. Its payments are not required by law. Therefore, there are no specific recommendations on charges and payments. Employers independently develop these points and methods.

Important! The calculation of annual bonuses is necessarily preceded by the inclusion of the main issues of its calculation and payment in local documents. If there is no reference to annual incentive payments in any document, then their accrual is fraught with claims from the tax office. The fact is that such expenses cannot be taken into account in the tax base for income tax.

Local acts should not only mention the bonus, but also specify the size, procedure, conditions and terms of accrual.

Main documents setting out the terms of the bonus:

- employment contract;

- collective agreement;

- wage regulations;

- order on awarding bonuses to special employees.

Responsible persons

The main person responsible for bonuses to employees is the head of the enterprise. He has the right to independently determine not only the amount of bonuses, but also the criteria according to which remuneration is calculated (Article 144 of the Labor Code of the Russian Federation).

But, despite this, there are cases when not only the manager, but also a representative of the workforce participates in the development of bonus regulations.

In the process of work, the responsible person for submitting reports for bonuses is the head of the structural department. It is he who analyzes the work, in the form of monitoring his subordinates, and has the right to apply for a monetary reward in connection with a job well done.

All other work on accrual and registration is performed by the personnel department and accounting department of the enterprise.

Rules and payment procedure

After submitting a report to the head of the structural unit, the head considers this request. The decision to award an employee a bonus is made by the manager after an analysis of the work performed.

Then the manager’s order is processed in the accounting department, where the bonus calculation itself is carried out (you can find out more about why an order to reward an employee is needed, and also see a sample document here).

Rewarding an employee of an enterprise with a monetary payment and a sample order for bonuses for an employee.

If the bonus amount is determined as a percentage, then the accountant multiplies the salary by the corresponding percentage specified in the bonus order. And then, according to paragraph 6 of Art. 164 of the Tax Code, already deducts income tax from the amount received, which is 13%.

In the case where the bonus is a fixed amount, then 13% is immediately calculated from it, that is, income tax (we talked about the peculiarities of taxation of funds allocated for bonuses to employees here). The remaining amount will be paid to the employee.

- Example: An employee worked for a full month, and his monthly salary is 10,000 rubles. The employee receives a bonus of 30% of his salary.

The bonus is 30% of the salary.

From the amount received you will need to subtract contributions to the funds. These calculations are carried out in the same way as when calculating regular wages.

In the case where the bonus is a fixed amount, it is summed up with accrued wages for the time actually worked, and 13% is calculated from the resulting amount. Example: The monthly salary of an employee who has worked for a whole month is 20,000 rubles. He receives a bonus of 5,000 rubles.

- 25,000×13%= 3250 – income tax;

From the amount received, it will be necessary to make an accrual to the funds, which is carried out as for regular wages.

Read more about how to register and record the payment of one-time bonuses here.

How to calculate the bonus for the year

An annual bonus can be a mandatory form of incentives for employees at an enterprise or optional - that is, awarded at the request of the employer and, if possible, the company’s budget for special merits in work.

Labor legislation determines the circle of employees who are not entitled to receive quarterly bonuses and year-end bonuses. Such employees include:

- subordinates who violated labor discipline and received disciplinary action;

- employees who have been temporarily suspended from performing their official duties;

- employees on parental leave to care for children under 3 years of age.

To determine the size of the bonus at the end of the year, you need to sum up all the employee’s income (without taking into account various types of increasing factors, if any are applied), and then multiply the result by a pre-agreed percentage of the bonus. The calculation formula is as follows:

RGP = (UZP x 12 months x PP) – (UZP x 12 months x PP) x 13%,

where RGP is the amount of the annual bonus;

EZP – monthly salary (without taking into account increasing factors);

PP – bonus percentage;

13% – personal income tax withholding.

How the bonus is calculated: general step-by-step instructions

Awards can vary not only in size, but also in nature. The most common of them are:

- incentive bonuses;

- incentive bonuses.

Incentive payments

Incentive bonuses are most often paid to employees for good work during the year, length of service, or dedicated to holidays and special occasions (you can find out what a sample order for a bonus for a professional holiday looks like here, and in this article we told you what the procedure is accrual of incentives for the anniversary). Incentive bonuses have a slightly simplified calculation method.

Let's look at the step-by-step instructions, using the example of bonuses for a special date:

- The head of the company issues an order for bonuses to his employees.

- The HR department or accounting department processes the manager’s order.

- Rewarded employees familiarize themselves with the manager’s order and put their signatures.

order to issue an incentive bonus

- The document is sent to the accounting department for accrual and calculation of bonuses to the employee.

- Payment of bonuses.

- Entry in the work book.

- The head of a structural unit writes a memorandum indicating the fact that a certain employee has exceeded the plan.

- The head reviews the note and issues an order.

- The order is signed by the manager, the employee being awarded and stamped.

Incentive bonuses most often have a fixed amount of monetary remuneration and are paid to employees regardless of their position.

Incentive rewards

Incentive bonuses are most often awarded for excellent work done, production above the norm, or delivery of work within a certain time frame. Let's look at step-by-step instructions for calculating an incentive bonus, using the example of bonuses for exceeding the plan:

order to issue an incentive bonus

An example of how to calculate a bonus for a year

Programmer R.A. Knopkin a salary of 56 thousand rubles per month is paid. This salary was accrued to him for all 12 months of the past year. The employer instructed an accountant to calculate the annual bonus. The company's collective agreement contains information about the bonus percentage at the end of the year - it is 12%.

Over the past year, the programmer earned: 56,000 rubles. x 12 months = 672,000 rub .

The bonus at the end of the year will be: 672,000 rubles. x 12% = 80,640 rubles .

The accountant is obliged to withhold personal income tax from bonus payments in the amount of: 80,640 rubles. x 13% = 10,483 rub. 20 kop .

The employer will transfer insurance contributions from his own funds in the amount of: RUB 80,640. x 22% = 17,740 rub. 80 kop .

Total, Knopkin R.A. received in hand: 80,640 rubles. – 10,483.2 rub. = 70,156 rubles 80 kopecks .

Documentation of the procedure

Expert opinion

Gusev Pavel Petrovich

Lawyer with 8 years of experience. Specialization: family law. Has experience in defense in court.

Documentation of bonuses begins with a memorandum or template documents, which are called submissions for bonuses. The main information reflected in this note is:

- personal data of the head of the organization;

- document's name;

- personal data of the employee applying for bonuses;

- information about the employee’s work performed and his merits is recorded;

- a request for a bonus is made;

- the amount of incentive is indicated only if this information is not determined by the boss himself;

- personal data of the head of the structural unit who submits the report;

- signature;

- date of.

Today, the remuneration system increasingly includes bonuses for employees, thereby stimulating their work to increase the profitability of the enterprise. But for this, an important factor remains the correct execution of it. After all, only then does the manager have a chance to achieve economic growth of his enterprise.

An example of a document in the photo below:

Employee bonus:

A salary increase is a great way to encourage an employee, instill in him a sense of responsibility and a desire to develop. But do not forget about the moral side of work. After all, only a balance of moral and material rewards can give a positive result.

From the article you will learn:

1. How to document the accrual of bonuses to employees in order to avoid problems during tax and labor inspections.

2. What premiums can be taken into account in tax expenses under OSNO and simplified tax system.

3. What legislative and regulatory acts regulate the procedure for calculating bonuses and including them in expenses for taxation.

Employees' wages, as a rule, consist of several parts: wages (for hours actually worked, for the amount of work actually completed, etc.), compensation payments and incentive payments. Incentive payments include bonuses to employees.

Splitting the salary into a fixed part and a bonus part is in the interests of both the employer and the employee. The employer has the opportunity to stimulate employees to achieve higher indicators and results, and at the same time not overpay them if such indicators are not achieved.

And for employees, the bonus part of their wages is a real opportunity to receive greater rewards for their work. That is why almost all organizations and individual entrepreneurs-employers provide for the payment of bonuses to employees, and bonuses often make up the largest part of wages.

Given this fact, the calculation and payment of bonuses is the object of increased attention during inspections by the tax inspectorate and the state labor inspectorate. How to bring the calculation of bonuses into compliance with labor and tax laws and avoid problems during audits - read on.

What the tax inspectorate is interested in regarding bonuses to employees is whether wage costs (including the payment of bonuses) are legally classified as expenses that reduce the taxable base for corporate income tax or the single tax paid in connection with the application of the simplified taxation system.

What the state labor inspectorate is interested in is whether the rights of workers have been violated when calculating and paying them wages (including bonuses).

All bonuses to employees are subject to insurance contributions to the Pension Fund, Social Insurance Fund, and Compulsory Medical Insurance Fund (Clause 1, Article 7 of Federal Law No. 212-FZ of July 24, 2009), therefore, when checking the Social Insurance Fund and Pension Fund of the Russian Federation, inspectors are usually interested in the total amount of accrued bonuses without detailed analysis.

Documentation of awards

According to the Labor Code of the Russian Federation, establishing bonuses for employees is the right of the employer, and not his responsibility. This means that the employer has the right to approve a remuneration system that provides for a bonus component (salary-bonus, piece-rate-bonus system, etc.) and document this fact.

Please note that if the employer’s internal documents establish a remuneration system that includes bonuses, then in this case the calculation and payment of bonuses to employees, according to internal agreements, is the responsibility of the employer. Failure to fulfill this obligation may result in justified complaints from employees and serious claims from the labor inspectorate.

In this regard, it is important to correctly document the procedure and conditions for bonus payments to employees.

What documents need to reflect the conditions and procedure for bonuses to employees:

1. Employment contract with the employee. Conditions of remuneration, including incentive payments, which include bonuses, are mandatory for inclusion in the employment contract (Art.

57 Labor Code of the Russian Federation). At the same time, it must clearly follow from the employment contract under what conditions and in what amount the bonus will be paid to the employee.

There are two options for stipulating bonus conditions in an employment contract: fully specify the conditions and procedure for bonuses, or make a reference to local regulations that contain this information. It is advisable to use the second option, to provide a reference to local regulations in the employment contract, because when making changes to the conditions for rewarding employees, you will only need to make appropriate changes to these documents, and not to each employment contract.

2. Regulations on remuneration, regulations on bonuses. In these local regulations, the employer establishes all the essential conditions for bonuses to employees:

- the ability to accrue bonuses to employees (remuneration systems);

- types of bonuses and their frequency (for results based on the results of work for a month, quarter, year, etc., one-time bonuses for holidays, etc.)

- a list of employees who are entitled to certain types of bonuses (all employees of the organization, individual structural units, individual positions);

- specific indicators and methodology for calculating bonuses (for example, a certain percentage of salary for fulfilling a sales plan; a fixed amount and specific holiday dates, etc.);

- conditions under which the premium is not awarded. Thus, if an employee is given a bonus for conscientious performance of job duties in a fixed amount, then the employee can be deprived of this bonus only if there are sufficient grounds (failure to perform or improper performance of duties provided for in the job description; violation of internal labor regulations, safety regulations; violation resulting in disciplinary action and etc.);

- and other conditions established by the employer. The main thing is that all the conditions for bonuses for employees in the aggregate do not contradict each other and make it possible to unambiguously determine which of the employees, when and in what amount the employer is obliged to accrue and pay a bonus.

3. Collective agreement. If, at the initiative of the employer and employees, a collective agreement is concluded between them, then it must also indicate information on the procedure for paying bonuses to employees.

! Please note: in addition to the fact that the employee signs the employment contract, the employer must, upon signature, familiarize him with the regulations on remuneration, regulations on bonuses, and the collective agreement (if any).

Inclusion of bonuses in tax expenses under OSNO and simplified tax system

Labor costs for taxation purposes under the simplified tax system are accepted in the manner prescribed for calculating corporate income tax (clause 6 p.

1, paragraph 2, art.

346.16 Tax Code of the Russian Federation). Therefore, when including labor costs (including the payment of bonuses) in expenses that reduce the taxable base for income tax and the simplified tax system, one should be guided by Article 255 of the Tax Code of the Russian Federation.

“The taxpayer’s expenses for wages include any accruals to employees in cash and (or) in kind, incentive accruals and allowances, compensation accruals related to working hours or working conditions, bonuses and one-time incentive accruals, expenses associated with the maintenance of these employees, provided for by the norms of the legislation of the Russian Federation, labor contracts and (or) collective agreements” (paragraph 1 of Art.

255 of the Tax Code of the Russian Federation). According to clause

2 tbsp. 255 of the Tax Code of the Russian Federation, accepted labor costs for tax purposes include “accruals of an incentive nature, including bonuses for production results, bonuses to tariff rates and salaries for professional skills, high achievements in work and other similar indicators.”

Expert opinion

Gusev Pavel Petrovich

Lawyer with 8 years of experience. Specialization: family law. Has experience in defense in court.

In addition, as a general rule, expenses in tax accounting are recognized as justified and documented expenses incurred by the taxpayer (Article 262 of the Tax Code of the Russian Federation).

Thus, having combined all the requirements of the Tax Code of the Russian Federation, we come to the following conclusion. Expenses for bonuses to employees reduce the tax base for income tax and the single tax paid in connection with the application of the simplified tax system, while simultaneously meeting the following conditions:

1. Payment of bonuses must be provided for in the employment contract with the employee and (or) in the collective agreement.

We discussed above the procedure for reflecting bonus conditions in an employment contract: either stipulating them in the employment contract itself, or referring to the employer’s local regulations. Not all employers conclude a collective agreement with employees, however, if one does exist, it should also provide for the possibility of paying bonuses and the procedure for bonuses.

! Please note: one order from the manager to pay bonuses is not enough to include bonuses in expenses. Bonuses for employees must be provided for in the employment contract with the employee and (or) in the collective agreement.

Otherwise, tax authorities have every reason to remove “premium” expenses and charge additional income tax or tax under the simplified tax system. This position of the tax authorities is confirmed by numerous court decisions in their favor.

2. There is a need for a direct relationship between the awarded bonus and the employee’s “production results”, that is, the bonus must be economically justified and related to the receipt of income by the organization or individual entrepreneur.

! Please note: bonuses are often awarded to employees with approximately the following wording: “For the timely and conscientious performance of their duties.” If you want to include bonuses in tax expenses, it is better not to use this wording, because the timely and conscientious performance of one’s work duties is the responsibility of the employee, and not the object of additional incentives.

In this case, the tax authorities will most likely remove such expenses. Therefore, if it is impossible to provide specific labor indicators for calculating a bonus, then it is better to indicate “For work results based on the results of the month (quarter, year, etc.).”

In this case, it is possible to defend the right to include such premiums in tax expenses.

Another point: the source of payment of bonuses. If profit is indicated as the source of payment of the premium, or as the basis for calculation, but a loss is actually received, then such premiums cannot be taken into account as expenses for taxation.

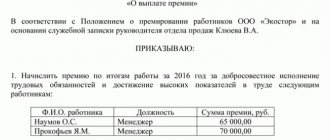

3. The accrual of bonuses must be properly completed.

The basis for awarding bonuses to employees is the bonus order. To draw up an order on bonuses, you can use the unified forms: Order (instruction) on encouraging an employee (Unified Form No. T-11) and Order (instruction) on encouraging employees (Unified Form No. T-11a), which are approved by the Resolution of the State Statistics Committee of the Russian Federation dated 05.01. 2004 No. 1 “On approval of unified forms of primary accounting documentation for recording labor and its payment.”

However, from January 1, 2013, it is not necessary to use unified forms (clause 4 of Art.

9 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting”). Therefore, an order for bonuses can be drawn up in any form that is approved by the organization.

The main thing you need to pay attention to when filling out an order for bonuses:

- the incentive motive must correspond to the type of bonus specified in the employment contract, local regulations, collective agreement (with reference to these documents);

- it should be clear from the order which employees the bonus is awarded (specific employees indicating their full name);

- the amount of the bonus for each employee must be indicated (the amount of the bonus must correspond to the calculated data);

- It is necessary to indicate the period for calculating the bonus.

4. It is better to issue bonuses to the head of an organization (who is not its sole founder) not by order of the head himself, but by the decision of the founder (general meeting of founders).

This is due to the fact that the employer in relation to the head of the organization is its founders. Accordingly, it is within their competence to establish the conditions for payment of bonuses and its amount to the manager.

Reflection of bonuses in accounting

In accounting, the accrual of bonuses is reflected in the same way as all wages in account 70 “Settlements with personnel for wages” in correspondence with cost accounts (20, 26, 25, 44). Since bonuses to employees are subject to personal income tax, bonuses are paid minus the withheld personal income tax.

If you find the article useful and interesting, share it with your colleagues on social networks!

If you have any comments or questions, write to us and we’ll discuss them!

Legislative and regulatory acts:

1. Labor Code of the Russian Federation

Expert opinion

Gusev Pavel Petrovich

Lawyer with 8 years of experience. Specialization: family law. Has experience in defense in court.

3. Federal Law No. 212-FZ of July 24, 2009 “On insurance contributions to the Pension Fund of the Russian Federation, the Social Insurance Fund of the Russian Federation, the Federal Compulsory Medical Insurance Fund”

You can find out how to familiarize yourself with the official texts of documents in the Useful sites section.

Every employee loves to receive bonuses and material rewards for the results of their work. But not all employees understand what methods the employer uses when issuing a bonus to a particular employee.

That is why disagreements and misunderstandings often arise between employees, why one receives more and the other less.

What kind of bonus systems there are, which one is more convenient and best to use in a particular company, will be discussed in today’s article.

Year-end bonus, or Secrets of the thirteenth salary

The year-end bonus, or the thirteenth salary, as we used to call it, is an excellent means of motivating staff.

It takes into account the contribution of each employee to the overall performance of the organization and helps reduce staff turnover. Today we will talk about how to create a bonus system in a company based on the results of work for the year. Many managers appreciate the benefits of year-end bonuses for employees and are actively introducing this type of incentive in their companies. The regulations on bonuses based on the results of work for the year most often have to be drawn up by personnel officers. Let's look at how to draft this provision and how it will work. What you need to know about the thirteenth salary

Before discussing specific issues with the director, you need to understand what the thirteenth salary is.

This is a bonus payment, the amount of which depends on the size of the employee’s salary and the duration of his continuous work in the organization. This bonus is paid based on the results of the calendar year (which lasts from January 1 to December 31). As a rule, remuneration is received by employees who have worked for a full year. The employer may provide reasons for which the thirteenth salary is reduced or not paid at all. Remuneration based on the results of work for the year is paid from the wage fund, material incentive fund or social development fund, depending on which source is specified in the organization’s charter. When drawing up regulations on bonuses based on the results of work for the year, read the recommendations that were approved by the Decree of the State Committee for Labor of the USSR and the Presidium of the All-Union Central Council of Trade Unions dated August 10, 1983 No. 177/P-13. True, this normative act of twenty years ago is quite outdated. Therefore, focus primarily on practice, as well as the needs and capabilities of your organization. What to discuss with the director

1. Will the provision on bonuses based on the results of work for the year be an independent document or an integral part of another local act? If you have a provision on bonuses or wages, then you do not need to draw up a separate document, but include the terms of the year-end incentives in these acts as an appendix. They can also be added to the collective agreement. But keep in mind that the procedure for changing a collective agreement is quite complicated - you need to negotiate with representatives of the labor collective (Articles 37, 44 of the Labor Code of the Russian Federation).

2. How will the remuneration be calculated?

The manager can set, for example, a percentage rate of the employee’s annual earnings or salary depending on length of service, remuneration in the amount of salary, etc. Below are different ways to calculate the annual bonus. “PREMIUM PRACTICUM”

Mechanic Nikolai A. worked at ZAO Sigma for two years. His salary is 6,000 rubles, and his annual earnings are 72,000 rubles (6,000 H 12 = 72,000). The thirteenth salary with two years of work experience at Sigma CJSC is 10 percent of annual earnings. Let’s take 72,000 as 100 percent and find out the size of Nikolai A.’s remuneration (72,000: 100) H 10 = 7,200 rubles. So, Nikolay A. will receive a remuneration of 7,200 rubles based on the results of his work for the year.

Calculation of bonuses at the end of the year depending on the employee’s annual earnings

Elena M., accountant at Rassvet LLC, has been working in the organization for three years. The remuneration based on the results of work for the year with three years of work experience here is 1.5 monthly salary. Elena’s salary is 9,000 rubles. Now let's calculate the thirteenth salary. (9000 : 2) + 9000 = 13,500 Based on the results of work for the year, the accountant will receive 13,500 rubles.

3. On what grounds can remuneration be reduced or not paid? These could be disciplinary sanctions, omissions in work, manufacturing of defective products, etc.

4. How will the annual bonus be calculated: for each employee separately or by division (department, workshop, site, etc.)?

There is a method when a certain amount is allocated for bonuses to a structural unit, which is then divided among employees depending on the annual earnings and length of service of each of them. Below is an example of how to calculate employee bonuses in this case. “PREMIUM PRACTICUM”

Three designers work in the design department of JSC “Ophelia” - Pavel D., Sergey A. and Inna K. The director allocated 50,000 rubles for the annual bonus of the department. Pavel D. has been working in the company for one year, his annual salary is 216,000 rubles. Sergey A. has been working for two years, his annual salary is 180,000 rubles. Inna K. has been working for one year, her annual earnings are 120,000 rubles. We will calculate the share of each designer depending on their experience and annual earnings. To do this, we first find out the share of each depending on earnings, then the share of each depending on length of service and, finally, find the arithmetic mean between these values. 1) We calculate the total earnings of the department for the year and find the percentage of the earnings of each designer to the total earnings: 216,000 + 180,000 + 120,000 = 516,000 Pavel D. - 216,000: 516,000 = 0.42 Sergey A. - 180,000: 516,000 = 0.35 Inna K. - 120,000: 516,000 = 0.23. 2) Now we find everyone’s share depending on their earnings: Pavel D. - 0.42 Ch 50,000 = 21,000 Sergey A. - 0.35 Ch 50,000 = 175 00 Inna K. - 0.23 Ch 50,000 = 11 500 3) We count the total number of years worked and find the percentage ratio for the length of service of each employee: 2 + 1 + 2 = 5 Pavel D. - 2: 5 = 0.4 Sergey A. - 1: 5 = 0.2 Inna K. - 2: 5 = 0.4 4) We determine the share of each depending on the length of service: Pavel D. - 0.4 Ch 50,000 = 20,000 Sergey A. - 0.2 Ch 50,000 = 10,000 Inna K. - 0.4 H 50,000 = 20,000 4) Finally, we find the arithmetic mean between the bonus depending on earnings and the bonus depending on length of service: Pavel D. - (21,000 + 20,000): 2 = 20,500 Sergey A. - (10,000 + 17 500) : 2 = 13,750 Inna K. - (11,500 + 20,000) : 2 = 15,750 So, Pavel A.’s share in the total bonus fund will be 20,500 rubles, Sergei A.’s share will be 13,750 rubles, and Inna’s share K. - 15,750 rubles.

What to include in the bonus clause

After you have discussed all the issues with the director, you will need to think about the draft regulations. First of all, determine which sections will be included. We recommend organizing the document according to the following scheme:

- 1. General Provisions. 2. Conditions for receiving remuneration. 3. Remuneration amounts. 4. Conditions under which remuneration is reduced or not paid. In the sample below you will see exactly what provisions are included in each of these sections.

In conclusion, let us remind you that before submitting the regulation for approval to the director, you need to coordinate it with the representative body of employees, if it has been created in your organization.

Familiarize all employees with the approved regulations against signature. Magazine "Personnel Affairs" December, No. 12, 2005

Bonus system and its features

What is a bonus system?

The bonus system at an enterprise is an excellent incentive to motivate employees to increase not only their productivity, but also to improve their professional knowledge and skills.

However, financial incentives do not always play a positive role on employees.

There are also situations when a poorly thought-out planning system leads to improper stimulation of employees and damage to the company as a whole and to a specialist in particular.

For example, when rewarding employees of a medical treatment institution for the number of patients they received and prescribed treatment for, you can achieve not an increase in the quality of services and attentive attitude towards patients, but the following problems:

- Workers will be interested in a large flow of patients, and accordingly the treatment they prescribe will not always be competent;

- In addition, many doctors will make “false” entries in patients’ records about visiting a doctor if they want to improve their performance and receive larger financial rewards;

- Also, specialists will try to see as many patients as possible; accordingly, less time will be spent examining patients, interviewing them and additional examinations, which will reduce the usefulness of their work for the patient;

- In addition, there are often schemes when one specialist “gives” work to another, telling the patient about the need for additional consultation with a particular specialist. There have been cases when a patient was sent around by doctors several times before treatment was prescribed.

That is why it is important to adequately approach the choice of a system of bonuses and incentives for employees as professionals.

This will not only motivate employees to develop and improve, but will also bring benefits to the company.