From January 1, 2021, the UTII tax regime was finally abolished. The last time you had to report was for the 4th quarter of 2021 - before January 20, 2021. If you have to submit a declaration now, then only the updated one for 2021 and earlier periods. How to do this, in what time frame and are there any special features? The answers to these and other important questions are in our material.

A calculator will help you choose a new tax system.

UTII declaration form download free (excel)

Delivery conditions

The updated tax return for UTII is submitted to the same place where you submitted the primary report - to the Federal Tax Service at the place of business of the entrepreneur or at his location (if it is impossible to accurately determine the specific place of activity - for example, for taxi services).

The tax declaration of individual entrepreneurs and organizations was filled out based on the results of each quarter - no later than the 20th day of the month following the reporting quarter (clause 3 of Article 346.32 of the Tax Code of the Russian Federation).

If after submission you notice that the submitted declaration contains errors, some data is not reflected, or there is inaccurate information that led to an underestimation of the tax amount, you need to correct the submitted report. This can be done by filing an amended tax return for the same period.

You can also submit an updated return if there is no understatement of the tax amount.

Where to take it

There are two options:

- at the place of registration;

- at the place of business activity.

At the location or registration of individual entrepreneurs, only enterprises engaged in:

- delivery and distribution trade;

- cargo transportation;

- transportation of passengers;

- placement of advertising information.

If structural units are located within the area of activity of one Federal Tax Service, you only need to submit one declaration for the enterprise as a whole. If there are branches that are located in the territory under the jurisdiction of another inspection, you must register with this tax authority and provide quarterly tax data in the prescribed form. This provision is confirmed by judicial practice. An organization is required to register (and also report on tax calculations in the form of a declaration) with each tax authority in whose department the territory in which its separate (structural) unit operates is located.

When to submit an updated declaration

The consequences in the form of sanctions and inspections depend on the moment of submission of the updated declaration.

If you made mistakes that led to an understatement of the tax amount, then after submitting the updated declaration you will have to pay the arrears to the budget and transfer penalties. But liability can be avoided if the following conditions are met:

- submit an amendment before the tax payment deadline if you noticed and corrected an error before the tax authority found it;

- pay the arrears and penalties and submit an update before you find out that the tax office has found errors and ordered inspections;

- submit an updated declaration after an on-site inspection, as a result of which no errors or distortions were found.

If the amount of tax was not underestimated in the primary declaration, then the declaration will be considered submitted without violating the deadline (paragraph 2, paragraph 1, article 81 of the Tax Code of the Russian Federation).

Section 1 and example of tax calculation for the 3rd quarter

Completing this section completes the declaration. It contains information about the amounts of tax payable to the budget and consists of several blocks of lines 010 and 020. Each block corresponds to the OKTMO code.

Line 010 indicates this code.

Line 020 – tax amount. If the declaration contains information on several OKTMO codes, then the amount for line 020 is determined as the share corresponding to a specific code. To do this, the total amount of tax payable (line 050 of section 3) is multiplied by the quotient of dividing the amount of accrued tax for a specific code (the sum of lines 110 of section 2 by code) by the total amount of accrued tax (line 010 of section 3). If a businessman operates within one municipality, then the indicator of line 050 of section 3 is simply transferred to this line without any adjustments.

Section 1 must be certified by the signature of the responsible person.

Checks of updated declarations

After receiving the updated declaration, the tax office has the right to check the period for which it was submitted. To do this, they begin an on-site inspection. It can even cover a period that extends beyond the three calendar years preceding the year the decision on the inspection was made.

We also note that during a desk audit of the clarification in which the amount of UTII was reduced, the tax office may require clarification. They must be submitted within five days.

If you submit an updated declaration two years after the deadline established for the initial declaration, then during a desk audit the tax office has the right to request:

- primary and other documents confirming changes in information in the relevant indicators of the declaration;

- analytical tax accounting registers on the basis of which such indicators are formed, before and after their changes.

Fines for late submission of UTII declarations

The standard fine for failure to submit a UTII return on time is 5 percent of the accrued tax. The fine cannot be more than 30 percent of the tax amount and cannot be less than 1,000 rubles (Article 119 of the Tax Code of the Russian Federation).

Tax return UTII

Home / Tax returns

Zero declaration on UTII

The opinion of the Ministry of Finance on this matter is clear: Chapter 26.3 of the Tax Code of the Russian Federation does not provide for the submission of “zero” declarations on UTII (letter of the Ministry of Finance dated July 3, 2012 No. 03-11-06/3/43).

The absence of economic activity under the imputed regime is the basis for deregistration under UTII in the manner prescribed by current legislation.

If the taxpayer was not deregistered under UTII, then stopping business activities, even if there is no physical indicator, is the basis for paying imputed tax and filing full (not zero) reporting.

In this case, the tax is calculated based on the size of the individual. indicator reflected in the reporting for the previous period in which activities were still ongoing (letter of the Ministry of Finance dated October 24, 2014 No. 03-11-09/53916).

Failure to fulfill tax payment obligations will entail the collection of arrears on UTII, as well as the accrual of fines and penalties.

However, there are clarifications from the Federal Tax Service, published on the official website of the tax service on September 19, 2016 (https://www.nalog.ru/rn32/news/activities_fts/6167481/), based on the decision of the Supreme Arbitration Court of the Russian Federation, according to which the submission of a zero declaration is possible .

This situation arises if the use or ownership of property, without which it is impossible to carry out the imputed activity, is terminated. The precedent under consideration is the termination of the lease agreement for retail space by the lessor.

But, if the taxpayer nevertheless decides to submit a zero return, with a high degree of probability he will have to defend his position in court.

Therefore, if a business entity does not want to incur additional expenses for paying taxes and submitting unnecessary reports in cases where activities for some reason were suspended or terminated completely, the most reliable way to avoid claims from regulatory authorities is to submit an application for deregistration under UTII.

Penalty for late submission of declaration

If the taxpayer does not submit the declaration on time, then the sanctions will range from 5% to 30% of the amount of unpaid tax reflected in the report for each full or partial month of delay, but not less than 1,000 rubles.

Moreover, if the imputed tax itself is paid on time, then failure to submit a declaration within the prescribed period will result in a fine of 1,000 rubles.

Responsibility for the delay in the UTII report imposed on the head of the legal entity of the Code of Administrative Offenses of the Russian Federation can range from 300 to 500 rubles.

Moreover, if the deadline for submitting the declaration is exceeded by more than 10 working days, the regulatory authorities may suspend operations on the current account of the business entity.

Programs and services for report preparation

A UTII declaration can be prepared using the following software and online services:

| Software name | Website |

| “Taxpayer Legal Entity” (free program from the Federal Tax Service) | https://www.nalog.ru/rn77/program/5961229/ |

| "Taxpayer PRO" | https://online.nalogypro.ru |

| "Bukhsoft" | https://online.buhsoft.ru |

| "1C" | 1c.ru |

| "Kontur.Accounting" | https://www.b-kontur.ru/lp/envd |

| "Sky" | nebopro.ru |

| "My business" | https://www.moedelo.org/landingpage/reporting-ednvd/ |

Did you like the article? Share on social media networks:

- Related Posts

- Sample of filling out a UTII declaration for an LLC

- Sample of filling out the simplified taxation system “income” declaration

- Sample of filling out the Unified Agricultural Tax declaration for an LLC

- Sample of filling out the UTII declaration for individual entrepreneurs

- Tax return for simplified tax system in 2021

- Tax return of the Unified Agricultural Tax

- Explanatory note to the tax return for UTII

- Sample declaration of the simplified tax system “income minus expenses”

Discussion: 3 comments

- andrey:

04/20/2018 at 13:43Has the new UTII declaration been approved yet?

Answer

Alexei:

04/23/2018 at 03:34

Hello. Not yet, they took it using the old form (Letter of the Ministry of Finance dated February 20, 2018 No. SD-4-3/ [email protected] ).

Answer

01/10/2019 at 19:21

Hello, can you tell me in the new declaration form, in section 4, if you didn’t buy a cash register, do you need to put dashes everywhere or can you not fill it out at all?

Answer

Leave a comment Cancel reply

The procedure for filling out the UTII declaration

Submit the updated UTII declaration on the form that was valid in the period for which you are adjusting the report. The rules for document execution are specified in the Order of the Federal Tax Service of Russia dated June 26, 2018 No. ММВ-7-3/ [email protected] Filling out a tax return for UTII occurs after calculating the tax, which is made according to the following formula:

UTII = (Tax base * Tax rate) - Insurance premiums. Let us recall that

Tax base = Imputed income = Basic profitability * Physical indicator

The basic yield is adjusted (multiplied) by coefficients K1 and K2.

Which physical indicator to use depends on the type of activity and is determined by Art. 346.29 Tax Code of the Russian Federation.

In the updated declaration, indicate the correct tax amounts calculated taking into account changes and additions. The difference between taxes does not need to be reflected in the declarations.

Deadlines for filing UTII returns and paying taxes

Taxpayers under the Unified Tax on Imputed Income must submit reports to the tax office quarterly. Based on the calculation in the declaration, tax payment is also made at the end of each quarter.

In this case, the reporting deadline is the 20th day of the month following the reporting quarter. And the payment terms have been shifted by 5 days, i.e. this is the 25th of the same month.

Deadlines for filing UTII returns and paying taxes in 2021:

| Taxable period | Reporting deadlines, up to | Tax payment deadlines, until |

| IV quarter 2021 | January 22, 2021 | January 25, 2021 |

| I Quarter 2021 | April 20, 2021 | April 25, 2021 |

| II Quarter 2021 | July 20, 2021 | July 25, 2021 |

| III Quarter 2021 | October 22, 2021 | October 25, 2021 |

| IV Quarter 2021 | January 21, 2021 | January 25, 2021 |

Attention! If the date of submission of the declaration or payment of the tax falls on a weekend, then the date of submission or payment will be the first working day after this weekend.

Deadline for filing the UTII declaration for the 1st, 2nd, 3rd, 4th quarter of 2021

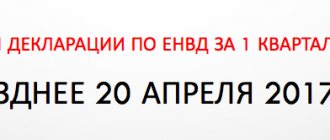

All entrepreneurs who have chosen this tax regime are required to file a declaration. It does not matter whether you carried out your business activities during the reporting period or not.

The report must be submitted by the 20th day of the month following the previous quarter. Thus, the declaration must be submitted by April 20, July 20, October 20, and January 20. This is how you will report each quarter. Moreover, the tax must be paid before the 25th of the corresponding month.

In a situation where the final deadline for filing a declaration falls on a weekend, it is automatically moved to the next Monday. However, it is strictly not recommended to delay submitting the declaration until the last day. After all, late submission of a report is a violation of the law and entails penalties. Those entrepreneurs who do not submit declarations at all cannot avoid a fine.

Filling rules

All amounts must be integers. If there are kopecks, they should be rounded to rubles.

All pages must be numbered.

When filing a paper declaration, you need to use only blue or black paste.

Each cell is intended exclusively for one character.

Don't fix anything. Do not use concealer or other similar products. If you make a mistake, use a new form.

The text must be written in block capital letters.

Dashes must be placed in cells that are left empty for some reason.

All sheets of the document must be separate. They cannot be stapled or stitched. Information should only appear on one side of each sheet.

( Video : “How to fill out a tax return: UTII”)