Hello, Vasily Zhdanov is here, in this article we will look at the non-current assets of an enterprise. The balance sheet, designed in the form of a two-sided “Asset-Liability” table, is developed by the Russian Ministry of Finance. Assets mean everything that the company owns and uses. Property, in turn, is divided into 2 groups depending on its functions and composition: fixed capital (non-current assets) and working capital (current assets). Let's figure out what place a company's non-current assets occupy in the company's balance sheet, what they are, and how to increase them.

Reflection in the balance sheet of property that relates to tangible non-current assets

In accordance with PBU 6/01, approved by order of the Ministry of Finance of Russia dated March 30, 2001 No. 26n, fixed assets represent a set of own property involved in the operation of the enterprise - from land and buildings to inventory. This also includes objects leased with the condition of being included on the balance sheet of the lessee.

In the balance sheet they are divided:

- on material exploration assets that arise only from organizations engaged in the development of natural resources and can be depreciated during the process of their creation;

- OS;

- profitable investments in materiel, which are fixed assets owned by the enterprise, but not exploited by it in its own production, but transferred for this purpose to the outside.

According to clause 35 of PBU 4/99, the cost of operating fixed assets is shown in the balance sheet minus depreciation on them. Those. data on fixed assets in non-current assets consists of balances on accounts 01, 03 and 08 (for tangible exploration assets) reduced by depreciation amounts (account 02). If the fixed assets data listed on account 08 does not correspond to the analytics highlighted in the balance sheet, then they may be:

- attached to the balances of the fixed assets used when their amount is insignificant (up to 5%) compared to the residual value of the fixed assets;

- allocated to an additionally entered separate line in non-current assets;

- are shown in the line “Other non-current assets”.

In simplified reporting (Appendix 5 to Order No. 66n), it is allowed to reflect on 1 line both the residual value of operating fixed assets and existing unfinished investments in them.

Part of the property of an economic entity that meets the following criteria is classified as tangible non-current assets:

- used in the economic activities of the enterprise;

- long-term use of the property (more than twelve months);

- the business entity receives income from the fact that these assets are used in the business process;

- property has value and physical form;

- property is subject to the process of partial write-off of its value to the cost of the product produced (or work performed, or services provided).

In the balance sheet of an economic entity that belongs to small businesses, the line “Tangible non-current assets” reflects the indicator obtained as the difference between the debit balances of accounts 01 “Fixed assets”, 03 “Income-generating investments in tangible assets” and the credit balance of account 02 “Depreciation” fixed assets".

To the amount received is added the indicator reflected in account 08 “Investments in non-current assets” in relation to expenses for construction in progress.

The indicator obtained as a result of calculations reflects the amount of fixed assets available to a small business entity.

As intangible assets, those assets are recognized that meet the conditions for classifying them as non-current, have a certain value, but do not have a physical form.

Trademarks, licenses, cost of software, etc. can be taken into account as intangible assets as part of non-current assets of small businesses.

The line “Intangible financial and other non-current assets” in the balance sheet of small businesses reflects:

- results of developments and research;

- investments in intangible assets that are unfinished.

Regulatory and legislative acts on the topic

| Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n Order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66n clause 20 PBU 4/99 | The procedure for reflecting information about non-current assets in the lines of the balance sheet |

| Order of the Ministry of Finance of the Russian Federation of October 31, 2000 No. 94 | About the formation of line 1190 |

| PBU 19/02 | On reflecting financial investments in the balance sheet |

| PBU 14/2007 | Reflection in the balance sheet of intangible assets |

| PBU 6/01 | On the reflection in the balance sheet of transport and other fixed assets, as well as profitable investments in material assets |

| PBU 14/2007 | Regulation of intangible assets |

| PBU 17/02 | Regulation of research and development results |

| PBU 24/2011 | Regulation of intangible search assets |

| PBU 24/2011 | Regulation of tangible exploration assets |

| PBU 19/02 | Regulation of financial investments |

| PBU 18/02 | Regulation of deferred tax assets |

Core and non-core assets

There are also core and non-core resources, depending on the direction of the enterprise. Core resources are property and funds used directly in the production and marketing of products. These are almost all savings corresponding to the type of activity of the enterprise, without which development and profit making are impossible.

Non-core resources are any property and funds that are not currently used by the enterprise and only generate expenses. A similar situation can be caused by:

- Privatization;

- Repurposing, transition to a new market segment;

- Buying out cheap property from a bankrupt entrepreneur.

The best example of a non-core asset is the property of debtors, which the bank seizes to pay off the debt. Usually banks try to sell such property as quickly as possible, but this can be difficult to do in a short time, so banks are forced to maintain this ballast for some time.

Classification of non-current assets

In order to manage assets and extract maximum profit from their use, organizations classify assets according to a number of criteria. Based on the nature of servicing the company’s activities, the following types of VA are distinguished:

- operating or production – directly used for the manufacture of products

- investment – aimed at investing in the development of subsidiaries or creating new sources of income

- non-production – social and domestic facilities

Based on the form of ownership, a distinction is made between leased and own VAs. The first group includes property that the enterprise disposes of under the right of use granted by the lease agreement. The second category includes objects acquired by the company using its own or borrowed funds.

Often, VA organizations act as collateral when obtaining a bank loan. According to the form of collateral, they are divided into:

- movable – can be seized from the enterprise by the creditor (vehicles, equipment)

- immovable – cannot be seized by the creditor during the pledge process (land, building)

According to the degree of liquidity, intangible assets are classified as illiquid property. For example, a company's goodwill cannot be sold to another business. Although such a scenario can be realized during a merger or acquisition of one company by another.

Classification of current assets

OA organizations are classified according to various criteria. By type of financing there are:

Gross OA is the total amount of property of an enterprise formed from the company’s own finances and borrowed money. Those. in balance.

CHOA=OA-KZ, where

OA - data from reporting in the “Total” column

KZ - short-term loans aimed at purchasing assets

NOA = 174,405 = 1,057,561 – Seligdar PJSC for 2021

NOA = 11,861,567 - 9,449,254 = 2,412,313 – Seligdar PJSC for 2017

SOA=CHOA-DZ, or

SOA=OA-KZ-DZ, where

SOA = 1,057,561 - 2,739,605 = -1,682,044 (for 2021)

SOA = 2,412,313 - 4,764,990 = -2,352,677 (for 2021)

A negative indicator of own current assets characterizes the financial condition of the company from the negative side. This means that the company does not have enough equity capital and operates on borrowed money. For normal operation, it is necessary that your own working capital not only be greater than zero, but also exceed the cost of inventories (the number in the “Inventories” column). At the end of 2021, they amounted to more than 11.5 billion rubles.

Composition of non-current assets

According to the financial statements, the VA includes the property of an enterprise with a service life of more than a year. Such property does not lose its consumer properties as a result of operation, so it is used for a long time. VA can be divided into three large groups - financial, intangible and tangible.

According to the financial report, the VA category includes:

- fixed assets

- intangible assets

- investments

- Deferred tax assets

- securities

- other VA

Non-current assets are company property that is used many times. This includes objects that have been in use for more than a year. Their cost is more than 15 times the minimum wage, excluding taxes.

Non-current assets may include:

- funds received from the main activities of the enterprise;

- intangible assets;

- unfinished objects;

- equipment and machinery;

- long-term investments.

This list is not exhaustive. Let's look at each of the component categories. Material VA may include:

- building;

- Earth;

- equipment, vehicles;

- furniture that has been in use for more than a year;

- resources in the form of animals and plants;

- trade equipment;

- equipment stored in enterprise warehouses;

- property leased to another person.

Among financial VAs we can highlight:

- bonds with a long-term maturity period;

- shares purchased for the purpose of receiving dividends;

- providing loans;

- various investments.

Intangible non-current assets are:

- Database;

- software developed by the company;

- rights to own land and subsoil;

- licenses to carry out work;

- various patents.

Regardless of which object is being considered, its period of use must exceed a year. If the operating time is shorter, the property will be classified as current assets.

These include:

- land;

- buildings (main and non-permanent), structures;

- machines, machine tools, equipment, complex office equipment, instrumentation, vehicles;

- furniture, office equipment, tools with a service life of more than a year;

- unfinished capital construction;

- animals and perennial plants;

- trade equipment (counters, cash registers, showcase refrigerators, etc.);

- equipment along with spare parts that was purchased but not installed;

- property leased/rented;

- library collections;

- other material resources.

A company's assets can be considered non-current if their value can be determined. Also, these resources must comply with the established cost limits - it must exceed 10,000 rubles. Without this, such assets are defined as “low value”, and, even if they last more than a year (for example, a telephone), they are accounted for as current assets in the form of inventories.

Disposal of objects from attachments

An asset for which investments in its value have been completed is most often removed from account 08 by putting it into operation. Depending on the type of property created (OS or intangible assets), this is recorded by posting Dt 01, 03 - Kt 08 or Dt 04 - Kt 08. Acquired objects that do not require modification are accepted for operation immediately after receipt, and those requiring additional work and created by one from existing methods or reconstructed (modernized) - after completion of all work and drawing up a commissioning or acceptance certificate from reconstruction (modernization). For these reasons, acquired assets are almost never found in the balances of account 08, while those created, especially over a long period, are usually present in these balances.

For information on the specifics of reflecting investments in non-current assets in the balance sheet, read the material “On which line should the balance of account 08 be reflected in the balance sheet?” .

At the same time, other disposal transactions may arise:

- Dt 91 - Kt 08 - when writing off ineffective R&D or contribution to the development of natural resources, as well as other unfinished investments, the further development of which is impractical;

- Dt 90, 91 – Kt 08 - when selling unfinished investments;

- Dt 99 - Kt 08 - for losses that occurred in emergency situations;

- Dt 94 - Kt 08 - when identifying the perpetrators of damage caused to objects of unfinished investments;

- Dt 79 - Kt 08 - when transferring unfinished investments to other divisions of the same person.

Accounting for non-current assets at an enterprise

OS accounting

For accounting purposes, VA is reflected separately for each position. Property is taken onto the balance sheet at its original cost, which includes:

- price of the object

- transportation costs

- costs of bringing the facility to working condition

For example, a company bought a lathe for 39,000 rubles. Delivery and installation costs amounted to 11,000. A machine with an initial cost of 50,000 (39,000 11,000) will be taken into account.

The reporting reflects the residual value of the VA. That is, depreciation is subtracted from the original total cost, which in turn is included in the cost of manufactured products.

Each enterprise is required to conduct an inventory of property, work in progress and inventory annually. This norm is contained in Order of the Ministry of Finance No. 34n dated July 29, 1998.

Accounting for investments in non-current assets

The chart of accounts for account 08 provides not only for the reflection of the facts of construction and purchase of objects, but also other transactions for the receipt of assets into the enterprise. For example, a contribution to a management company, transfer of property free of charge, etc.

All actual costs incurred that are directly related to the process of receiving fixed assets and intangible assets and further bringing them to a usable state are recorded in the debit of account 08. These include:

- Payment amounts for invoices presented by suppliers;

- Costs incurred during transportation and installation of objects;

- Commissioning work when retrofitting or bringing the facility to working condition;

- Customs and government duties;

- Registration fees established by law, other identical payments necessary to acquire rights to property;

- Other expenses directly related to the receipt/purchase of non-current assets and bringing them into working condition.

So, on active account 08 the costs that form the cost of the future or reconstructed property are collected. They are reflected in the debit of the account.

The credit of the account records the transfer of the object into operation, documented with the appropriate documentation, according to the initial cost generated on account 08. Those. upon completion of the capital investment process and the object is fully brought to a state in which it will work productively, its initial value, formed by the debit of account 08, is written off from the loan in correspondence with the debit of accounts 01 “OS”, 04 “Intangible assets”, etc.

Basic transactions for transferring the initial cost of an object prepared for use:

Where is the revaluation of non-current assets recorded: line 1340

Balance sheet line 1340 “Revaluation of non-current assets” is specially set aside to reflect the results of the revaluation of fixed assets and intangible assets. The amount indicated in it corresponds to the credit balance of account 83, since the revaluation of non-current assets is included in equity capital.

Its postings accompanying the revaluation procedure are generated:

| Operations | D/t | K/t |

| The value of the asset was increased at the first revaluation | 01, 04 | 83 |

| Added depreciation amount for it | 83 | 02, 05 |

| The cost of the object was reduced during the first markdown | 91 | 01, 04 |

| Reduced depreciation | 02, 05 | 91 |

| Disposal of property that was previously overvalued | 83 | 84 |

Further revaluations are carried out from the replacement cost of objects, increasing the amount of additional capital when revaluing, or assigning the amount of the markdown to other expenses.

Accounting for investments in non-current assets

Related publications

In the process of activity, each company increases its production capacity and invests in its own development. Such costs are taken into account in account 08 “Investments in non-current assets”, which summarizes information about the company’s expenses incurred in the purchase or production of objects that will later be taken into account as fixed assets (fixed assets) and intangible assets (intangible assets), or will increase the value of existing ones units of property, improving their quality characteristics.

Investments in non-current assets represent a combination of costs for:

- creation of fixed assets, for example, for the construction of buildings;

- reconstruction associated with an increase in the size of the operating system, expansion and technical re-equipment of existing property;

- acquisition of fixed assets and intangible assets.

Which assets are overvalued and why?

Revaluation is possible for long-term financial investments, fixed assets and intangible assets. It is practiced to smooth out the difference between the original price of an object and its market value at a certain point in time. It is believed that a five percent gap between these two indicators is a reason for revaluation. It should be noted that revaluation is not a mandatory procedure; it may not be carried out until the need arises. However, the company does not have the right to revalue the property whenever it wants. This decision must be recorded in the UP.

All property of the company may be subject to revaluation, or categories of similar items may be formed, which the company has the right to determine independently.

There are many reasons for revaluation. For example, an organization plans to sell part of its assets, or wants to attract investment, for which it needs to obtain a loan, etc. In addition, companies have to control the value of net assets, which should not fall below the size of the company's authorized capital.

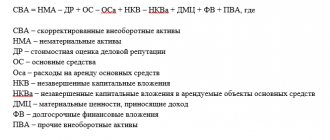

How are adjusted non-current assets calculated?

Let us assume that the financial statements contain the following data as of the reporting date of the end of the year:

Intangible assets (p. 1110) – 55,000 rubles, OS (p. 1150) – 930,000 rubles;

- profitable investments in MC (p. 1160) – 42,000 rubles;

- Finnish investments (p. 1170) – 88,000 rubles;

- other VNA (equipment requiring installation, p. 1190) – 110,000 rubles.

In addition, from the explanations of the income statement it is known that:

- business reputation of the company - 31,000 rubles;

- costs for leased operating systems – 15,000 rubles;

- unfinished capital investments – 77,500 rubles;

- similar unfinished investments for the lease of fixed assets - 5,200 rubles.

Calculation of SVNA indicators:

- NMA. 55,000 – 31,000 = 24,000 rubles;

- OS. 930000 – 15000 = 78000 rub.;

- Unfinished capital investments. 77500 – 5200 = 72300 rub.;

- Profitable investments in MC, completely. 42,000 rub.;

- Financial investments are long-term, completely. 88,000 rub.;

- The equipment is the same as other VNA, completely. 110,000 rub.

SVNA = 24000 + 78000 + 72300 + 42000 + 88000 + 110000 = 414300 rub.

When analyzing financial condition, as a rule, indicators are calculated for the previous 3 years, and, if necessary, for a longer period.

On a note. Regulatory documents provide for analysis at least 2 years before the bankruptcy of a business entity. The rules (order 367) recommend the calculation of quarterly indicators of financial and economic condition and for the period of bankruptcy procedures, in dynamics.

The results are presented in the form of tables for ease of perception and subsequent calculations of coefficients characterizing the economy of the research object.

Non-current asset turnover

The turnover rate of non-current assets is a coefficient that is equal to the ratio of the price of manufactured or sold goods after taxes to the average annual cost of fixed assets.

This coefficient reflects how much is the total return on the use of each ruble that was invested in the operating system, that is, how effective is the investment of money.

The formula for non-current assets (their turnover ratio) is as follows:

Turnover ratio = profit from sales of goods / average annual cost of fixed assets at the beginning of the reporting period.

According to the old accounting form. The balance indicator is calculated as follows:

Turnover rate = line 010 / 0.5 * (line 120n + line 120k), in which:

- Line 010 – line of the profit and loss statement according to Form 2;

- Lines 120n and 120k – book lines. balance sheet in Form 1 at the beginning and end of the reporting period.

According to the form of the new account. The balance indicator is calculated as follows:

Turnover rate = line 2110 of form 2 / ((line 1150n of form 1 + line 1150k of form 1) / 2).

What do other non-current assets mean on the balance sheet?

In the balance sheet of an enterprise, non-current assets are reflected in the first section and include fixed assets, intangible assets, long-term financial investments, and other non-current assets.

The regulations on accounting and financial statements (PBU) strictly define the criteria on the basis of which the company’s property can be classified as one or another category of assets. Others include those that cannot be registered as part of any of the first three groups. However, the period for their circulation must exceed 12 months.

Other non-current assets include:

- Investments in non-current assets. Investments aimed at creating the company's fixed capital.

- Equipment requiring installation. In some cases, equipment can be put into operation only after preparatory work: assembly and installation with mandatory fastening to the foundation or supports.

- Future expenses. These are costs that an enterprise incurs in one period of time, but they are attributed to production over a certain period of time. For example, an enterprise purchased materials for routine repairs. If these expenses are immediately attributed to the cost of production, this can significantly increase the price of goods. Therefore, it is more expedient to include these payments in deferred expenses, gradually writing them off as production expenses.

Analysis and accounting examples

In the balance sheet, other non-current assets are reflected in line 1190. To determine the amount, the balances of the accounts presented in the table are used.

Analytical accounting is carried out in the context of each specific object or counterparty (in the case of settlements).

Let's look at a specific example. Absolut LLC, as part of the technical re-equipment of production, purchases machines worth 890 thousand rubles, including VAT of 135,762.71 rubles.

In the process of developing the project, the company attracted a specialized organization, the cost of whose services amounted to 70,000 rubles, including VAT - 10,677.97 rubles. Transport costs – 20,000 rubles, including VAT 3,050.85 rubles.

| 07 – equipment for installation | 60 – settlements with suppliers and contractors | 754 237,29 | Balancing expenses for the purchase of equipment |

| 19 – VAT on purchased assets | 60 | 135 762,71 | VAT reflection |

| 07 | 60 | 59 322,03 | accounting for consulting expenses |

| 19 | 60 | 10 677,97 | VAT reflection |

| 07 | 60 | 16 949,15 | accounting of transport costs |

| 19 | 60 | 3 050,85 | VAT reflection |

| 68 – calculations for taxes and fees | 19 | 149 491,53 | VAT credit on purchased assets |

The value of other assets in itself is unlikely to say anything. Much more information can be obtained by analyzing the dynamics of this indicator.

If the amount in the accounts for accounting for other non-current assets has increased, it is possible:

- A serious investment process has begun, which may have a positive impact on the company's performance in the future.

- The scope of the enterprise's activities is expanding.

- Some departments are ineffective. For example, they purchased equipment, but cannot carry out installation.

- Suppliers do not fulfill their obligations. For example, an advance payment for new equipment was made on time, but the machines have not yet arrived.

If the number of other non-current assets has decreased, the following options are possible:

- New buildings, structures, and production equipment were put into operation.

- Costs incurred previously were included in production expenses.

- Suppliers have fulfilled their obligations under already paid contracts.

In general, an increase in line 1190 of the balance sheet should always be under the strict control of the company's management. A decrease most often indicates a decrease in the volume of immobilized funds that cannot generate profit.

A qualitative analysis of the condition and dynamics of other assets can only be carried out in the context of specific expense items.

For example, the balance on account 60 (settlements with suppliers) has increased: this may indicate completely different situations.

And if money was paid to suppliers, but nothing was received in return, then an increase in the account balance means a deterioration in the company’s financial position.

Accounting for investments in non-current assets

Accounting for such capital investments is carried out based on actual costs incurred. Often, investments in non-current assets are long-term investments, since the main feature of classifying property as non-current assets is their impressive service life (over 1 year), which means that a company, by investing in their acquisition or production, takes them out of circulation for a long time .

Accounting is kept on account 08, to which, depending on the company’s activities and planned actions, separate sub-accounts can be opened for the acquisition of, for example, plots of land, natural resource objects, intangible assets, individual PF objects that do not require installation and subsequent modification. Separate sub-accounts take into account the construction and construction of environmental facilities, R&D, as well as the raising of young livestock and the purchase of adult animals for the main herd.

Analytical cost accounting is carried out for each purchased, constructed or reconstructed facility, grouping costs according to the cost structure in accordance with the estimate documentation. For example, when constructing a building, analytics strictly divides the costs for each section of the compiled and approved estimate and detailed design, such as:

- earthworks;

- construction and installation work;

- hidden work;

- installation of electrical equipment;

- plumbing work;

- finishing of the building;

- landscaping.

Revaluation of non-current assets (fixed assets and intangible assets): how to take into account?

Commercial companies have the right to revalue homogeneous categories of fixed assets at current (replacement) cost no more than once a year. The procedure is carried out by recalculating the initial value of the object (or already the replacement value, if this is not the first revaluation) and the amount of depreciation accrued during the period of its use. Those. simultaneously with the change in the value of the fixed asset/intangible asset, the amount of accrued depreciation is proportionally recalculated.

Revaluation pursues the goal of bringing the accounting value of an asset as close as possible to its market value, which, based on market realities, can either increase or decrease. Therefore, depending on various circumstances, both an additional valuation (increase in value) and a markdown, i.e. its reduction, can be carried out. The results of the revaluation of fixed assets and intangible assets are reflected in the company’s accounting:

- The additional valuation is recorded in additional capital (account 83);

- The markdown is included in the financial result as another expense (account 91).

When disposing of fixed assets or intangible assets, their increased value from additional capital is transferred to retained earnings.

Answers to frequently asked questions on the topic “Non-current assets of an enterprise”

Question: An intangible asset is not recognized as such on the balance sheet if the company cannot document the existence of rights to use it. What documents confirm the right to own and use intangible assets?

Answer: Depending on what kind of intangible asset we are talking about, the right to it can be proven by providing a registered patent, certificate, some other document of protection, as well as documents that confirm the transfer of the exclusive right to a means of individualization or the result of an intellectual property activities without an agreement, or such an agreement.

An example of calculating the amount of line 1190 of a balance sheet asset

In the balance sheet they are divided:

- on NMA;

- R&D;

- intangible exploration assets that arise only in organizations engaged in the development of natural resources and can be depreciated during the process of their creation.

The cost of operated intangible assets in accordance with clause 35 of PBU 4/99 in the balance sheet is shown minus depreciation on them. Those. data on intangible assets in non-current assets consists of balances on accounts 04 and 08 (for intangible exploration assets) reduced by depreciation amounts (account 05). If the data on intangible assets listed on account 08 does not correspond to the analytics highlighted in the balance sheet, then they may be:

- added to the balances of used intangible assets when their amount is insignificant (up to 5%) compared to the residual value of intangible assets;

- allocated to an additionally entered separate line in non-current assets;

- are shown in the line “Other non-current assets”.

In simplified reporting (Appendix 5 to Order No. 66n), it is allowed to reflect on 1 line both the residual value of operated intangible assets and existing unfinished investments in them.

Non-current assets can enter an organization in different ways:

- Purchase. The organization itself can purchase the asset it needs

- Production. The asset can be created by the company itself. In this case, the organization will receive exactly what it needs

- A non-current asset may be at the disposal of the company as a contribution to the authorized capital

No matter how the asset ends up in the organization, you need to have correctly completed documentation on hand and register it correctly.

Not all organizations have other non-current assets at their disposal, therefore, in the absence of indicators, the line may remain empty.

The line is filled with amounts that are not included in other similar lines. Typically, insignificant values are shown here that should be reflected in accounting, but do not have much meaning.

Indicators that are significant are reflected separately and are not included in the calculation of the amount on line 1190. The financial statements have a fairly large number of users, the most important of which are the owners of the organization. Often they understand little about accounting, but must have complete and detailed information about the availability of property, cash and other assets; they bought a trademark for 400,000 rubles. VAT is 66,666.67 rubles and is included in the total amount. To formalize the transaction, documents were collected and submitted to the appropriate authority. In this case, costs were incurred in the amount of 5,000 rubles. Registration did not finish until the end of the year.

| Wiring | Explanation | Sum |

| D 08 K60 | Expenses that the company incurred during the purchase | 333333,33 |

| D19 K60 | VAT accounting | 66666,67 |

| D68 K19 | VAT to be reduced | 66666,67 |

| D08 K76 | Accounting for registration costs | 5000,00 |

333333.33 5000.00 = 338333.33 rubles. This amount must be entered in line 1190.

Methods for receiving enterprise assets

Incoming non-current assets, the organization can:

- buy ready-made, not requiring additional investments in them;

- receive without payment as a result of a gift or discovery;

- receive as a contribution to the management company;

- build (create) independently (in an economic way);

- create (construct) with the involvement of a third party organization (contractor);

- create (construct) in a mixed way: buy part of it or hire a third-party (contractor) organization for the work, and do the rest on your own (in your own way).

But even if you purchase a completely finished object, there may be additional costs that need to be included in its price.

If a receipt transaction is accompanied by VAT, then depending on whether the recipient works with it, the following situations of accounting for this tax are possible:

- it is allocated to account 19 if the recipient works with VAT, and this tax is indicated in the receipt documents;

- it is not allocated if the recipient works with VAT, but this tax is not included in the receipt documents;

- it is included in the price if the recipient works without VAT; the exception here will be the operation of receipt of a contribution made by property to the management company; the tax allocated in the transfer documents cannot be taken into account by the recipient working without VAT in the value of the property or taken as a deduction.

Profitable and financial investments (part 1)

Property that is rented or leased is also reflected in the balance sheet at its residual value on line 1160. Financial investments mean deposits in capital assets purchased by the Central Bank of other organizations. Line 1170 reflects the initial cost of long-term investments (circulation period more than 12 months). Information is entered from the debit balance of the account. 58, count. 55, count. 73. If an organization creates reserves for a decrease in the value of such assets, then they should also be accounted for on line 1170.

Financial investments also include issued interest-free loans. Their amount is reflected not in line 1170, but as part of accounts receivable (1190). The cost of shares purchased from the founders should also be reflected not in investments, but in liabilities (p. 1320).

Current liabilities in the balance sheet are line 1500 of the balance sheet

Often, accountants, when filling out tables characterizing the financial condition of an organization, encounter difficulties when it is necessary to indicate current liabilities, because this concept is absent in regulatory documents on accounting and taxation.

To determine where current liabilities are reflected on the balance sheet, let us turn to the meaning of this term. The Financial Dictionary defines current liabilities as accounts payable due within the next 12 months. In other words, current liabilities are synonymous with current liabilities.

https://www.youtube.com/watch?v=u1NjIGJ1NWs

Fixed assets (non-current assets of the enterprise)

We list the types of long-term operating company property that can be classified as fixed assets:

- buildings, structures, structures;

- subsoil, water complexes and other environmental management facilities;

- equipment, power and working machines;

- plots of land;

- regulating and measuring devices and instruments;

- capital investments in objects that were leased;

- Computer Engineering;

- capital investments in fundamental improvements of land plots (reclamation works such as drainage and irrigation);

- transport;

- on-farm roads;

- household and production equipment, tools, accessories;

- perennial plantings;

- breeding, productive, working livestock.

Classification of balance sheets

According to the way the data is reflected, the balance sheet can be:

- static (balance) - compiled for a specific date;

- dynamic (revolving) - compiled by turnover for a certain period.

In relation to the moment of compilation, balances are distinguished:

- introductory - at the beginning of activity;

- current - compiled as of the reporting date;

- liquidation - upon liquidation of an organization;

- sanitized - when rehabilitating an organization approaching bankruptcy;

- dividing - when dividing an organization into several companies;

- unifying - when organizations merge into one.

Based on the volume of data on organizations reflected in the balance sheet, balance sheets are distinguished:

- single - one organization at a time;

- consolidated - based on the sum of data from several organizations;

- consolidated - for several interrelated organizations, internal turnover between which is excluded when preparing reports.

According to its purpose, the balance sheet can be:

- trial (preliminary);

- final;

- predictive;

- reporting.

Depending on the nature of the source data, there is a balance:

- inventory (compiled based on the results of the inventory);

- book (compiled only according to registration data);

- general (compiled according to accounting data taking into account the results of the inventory).

By way of data reflection:

- gross - including data from regulatory items (depreciation, reserves, markup);

- net - with the exception of these regulatory articles.

Balance sheets may vary depending on the legal form of the company (balance sheets of state, public, joint, private organizations) and the type of its activity (main, auxiliary).

Based on frequency, balances are divided into monthly, quarterly, and annual. They can have either full or abbreviated form.

The balance sheet table can be of 2 types:

- horizontal - when the balance sheet currency is defined as the sum of its assets, and the sum of assets is equal to the sum of capital and liabilities;

- vertical - when the balance sheet currency is equal to the value of the organization's net assets (i.e., the amount of capital), and the net assets, in turn, are equal to the assets of the enterprise minus its liabilities.

To learn how to prepare a balance sheet for a small business, read the article “Balance Sheet for Small Businesses (Features).”

Intangible and tangible

Although the tangible and intangible search assets of an enterprise are interconnected, they are displayed in two different items of the balance sheet:

| Intangible search assets | Material prospecting assets |

| These include: ● results of assessing the feasibility of mineral extraction from a commercial point of view; ● the right (with a license) to search, evaluate deposits, and explore mineral resources; ● results of sampling and exploration drilling; ● information obtained during geophysical, geological, topographical research; ● other information about the subsoil. | These include assets used in the search, evaluation and exploration of mineral resources: ● transport; ● equipment (tanks, pumps, drills); ● structures such as piping systems. |

Assets and liabilities

To better understand the assets of an enterprise, you need to know what the concept of liability means. Accounting statements necessarily reflect assets and liabilities. Assets are property (things or money) that always generate and increase income. Liabilities are assets that satisfy daily needs, but require depreciation and repair costs.

For clarity, let's look at examples. A man has saved up 2,000,000 rubles and plans to use it at his own discretion. There are two available options for implementing these tools:

- Option 1. Deposit 2,000,000 rubles. on a bank deposit at 10% per annum. After a year, you can withdraw 2,200,000 rubles from the account, that is, make a profit of 200,000 rubles;

- Option 2. For 2,000,000 rubles. buy a one-room apartment. Repairs will cost 200,000 rubles, furniture and furnishings will cost another 200,000 rubles. Payment for utilities every month is approximately 4,000 rubles. This means that 48,000 rubles will be spent on housing and communal services per year. Consequently, the purchase of an apartment brought costs amounting to 448,000 rubles.

The company's liabilities are:

- Loan repayment.

- Purchase of raw materials.

- Issuing wages to employees.

- Payments to the state.

- Investments in your authorized capital for further activities.

The ideal option is when the indicators for assets by the end of the billing period exceed the indicators for liabilities or are at least equal to them. In this situation, we can say that the business is developing successfully. If the situation is different, it is worth analyzing the effectiveness of the strategy being pursued. When the return on active resources is negative for a long time, the company faces bankruptcy.