Why keep records?

Institutions need to keep track of waybills in order to standardize, plan and control the consumption of fuel and lubricants.

In the main areas where information on the costs of fuels and lubricants is required, accountants calculate the standard cost of products, works or services, and also analyze deviations between the actual and standard consumption of fuels and lubricants in order to identify savings or overruns. Regulatory authorities often turn to this area of accounting to assess how effectively inventories are used in an institution. All business transactions must be documented in accounting with primary accounting documents (clause 1 of Article of the Federal Law of December 6, 2011 No. 402-FZ). One of the main functions of waybills in accounting is to confirm the legality and correctness of the write-off of fuels and lubricants.

Basic moments

A waybill is an official document regulated by relevant bylaws and subject to accounting.

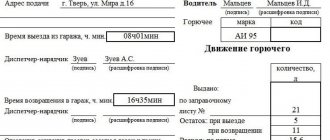

The waybill reflects the following indicators:

Work trip

- Document Number

- document date

- vehicle data

- information about its owner

- car driver information

- fuel consumption

- current car mileage

- exact route of the car

- place of departure (where you left) and place of arrival (where you went)

- exit time and time of return of the car to the garage

- speedometer data at the beginning and end of the working day

- the dispatcher's signature confirming the time of departure and arrival of the vehicle

- date and time of pre-trip inspection

- signature of the medical professional who performed the pre-trip medical examination

- number of flights

- TTN numbers used for transportation

The waybill consists of two parts. The first is the main sheet, which reflects the calculation of fuel consumption. The second part is a tear-off coupon, which is the main document according to which the customer of the work is billed for the services provided. The first part must be accompanied by a TTN. The driver receives a waybill for at least one day, and the maximum period of issue is one month. The storage period for waybills is the same as for other accounting documents - five years.

How to work with forms

Order of the Ministry of Finance of Russia dated March 30, 2015 No. 52n defines the rules for drawing up primary documents in accounting, however, there is no waybill in the album of unified forms of primary accounting documentation for budgetary organizations. In such a situation, the form approved by the State Statistics Committee of the Russian Federation of November 28, 1997 No. 78 “On approval of unified forms of primary accounting documentation for recording the work of construction machinery and mechanisms, work in road transport” is most often used. However, the document says that only motor transport enterprises are required to use this form.

Other institutions, including state-owned, budgetary, and autonomous institutions, have the right to develop their own form. The main requirement for it is the presence of mandatory information: the name of the document, the date of its preparation, the name of the institution. In addition, it is necessary to indicate the content of the operation and its measures in physical and monetary terms. The document must be signed by responsible employees. Without indicating their full name. and signature, the document is considered invalid.

However, the simplest solution is the standard form of waybill from Resolution No. 78. It includes all the information necessary to write off fuel and lubricants and does not raise questions from regulatory authorities.

I would like to note that waybills are not strict reporting forms, so you can use both printed forms and printed forms from accounting reference systems.

General provisions

The procedure for working with waybills is always the same.

More details about the rules for filling them out can be found in Order of the Ministry of Transport No. 152. First, a responsible employee is appointed by order of the director, who is responsible for distributing such papers among shifts. Most often, the role of such a specialist is played by a senior mechanic, who reports to all the company’s drivers. To take into account the movement of a working vehicle and control its fuel consumption, the accounting department maintains a special journal. It reflects data on the issuance of new waybills and the write-off of old ones. Such a journal is drawn up according to Form 8. A sample of it can be seen here.

The following data is reflected in the log:

- The number of each waybill.

- Dates when the sheets were issued to the driver.

- The number of the garage where the car is parked.

- Notes.

- Signatures of the responsible person.

There is no need to enter the registration number of the car in this document; there is no need for this. When an accountant accepts a waybill, he must indicate the date of acceptance.

When an accountant accepts a waybill, he must indicate the date of acceptance.

Typical mistakes of accountants

A mandatory requirement for a waybill, as, indeed, for any document, is its correct execution. There are several points where accountants make mistakes most often.

For example, there is no single rule for how long a waybill should be issued, and the absence of such a rule raises many questions. In letter dated 02/03/06 No. 03-03-04/2/23, the Russian Ministry of Finance allows for weekly and even monthly preparation of the document, if this period allows for organizing the accounting of time worked and fuel consumption. However, this recommendation does not apply to filling out waybills within the framework of the statutory activities of budgetary organizations. Therefore, we recommend that institutions rely on the instructions of Rosstat. In a letter dated 02/03/05 No. IU-09-22/257, Rosstat indicates that the waybill is drawn up for a period of one day (one shift). A longer period is permissible only if the driver is on a business trip.

Often accountants do not consider it necessary to fill out all the columns on the back side of the waybill. This concerns the indication of destinations: often specific points are replaced with general phrases - “Trips around the city”, etc. They do not allow us to confirm that the transport was used for official purposes and the expenses are of a production nature (letter of the Ministry of Finance of Russia dated February 20, 2006 No. 03-03- 04/1/129). Regulatory authorities recognize the absence of specific destinations in the waybill as a violation. It would also be a mistake to not have the driver’s signature on each line indicating the place of departure and destination, the time of departure and return of the car to the parking lot/garage.

Pay attention to the section “Fuel Movement”. Based on the columns “Normal consumption” and “Actual consumption”, gasoline is written off. Pay actual consumption strictly according to the meters. When filling out the standard gasoline consumption per 100 km, take as a basis the order of the Ministry of Transport of Russia dated March 14, 2008 No. AM-23-r (as amended on July 14, 2015), which defines all fuel and lubricant consumption standards for road transport. They also apply to budgetary institutions.

Making changes to the waybill, as well as to most primary documents, is permissible only with the consent of participants in business transactions (clause 5 of Article of Federal Law No. 402-FZ) and with the obligatory indication of the date. This means that corrections must be certified by the signature of the same persons who originally signed the documents.

General procedure for maintaining a travel log

The dispatcher distributes waybills between drivers only for one day (shift). An exception may be long business trips - in this case, a waybill is issued for the entire duration of the trip.

When handling waybills, the following rules must be taken into account:

- The accounting department must keep the waybill for at least 5 years;

- It is undesirable to make changes and adjustments to the waybill for one or another indicator (for example, gasoline consumption), however, if such a need exists, the correction must be secured with the signatures of two responsible persons (say, the driver and the mechanic);

- In order for the accounting department to write off fuel and lubricants, it is necessary that fuel payment receipts be attached to the sheet;

- if the driver uses his personal vehicle in the interests of the organization, this information must also be reflected in the waybill for the driver to receive subsequent compensation.

The waybill is the main document for accounting that certifies the legality of the driver’s expenses. If any of the columns is left blank, the costs may be considered unconfirmed.

Accounting automation tools

Special automated systems for recording waybills and fuels and lubricants will help the accountant avoid the above-mentioned mistakes. They will remind you of the required fields, track the correctness and timing of the use of standards, and compliance of actual fuel consumption with the standard. In addition, such programs allow you to quickly fill out any number of waybills, which significantly facilitates the work of an accountant.

The more complex the accounting of fuels and lubricants in an organization, the greater the capabilities the automated system should have. When choosing a program, make sure it can:

- maintain a unified register of waybills;

- take into account the receipt and consumption of fuel and lubricants by vehicles, drivers and types of fuel and lubricants;

- take into account fuel consumption according to consumption standards or actual consumption based on the data from waybills, taking into account seasonality and road conditions;

- control deviations of actual costs for fuels and lubricants from the normative ones (saving modes, excessive consumption of fuels and lubricants);

- generate reports on drivers, types and brands of fuels and lubricants, on vehicles by division (department);

- prepare printed forms of the necessary reports on mileage and operating time, on the movement of fuel and lubricants, on issued auto parts and much more.

Get a free demo version of the service for filling out and accounting for waybills

1C:Enterprise 8: 1C Vehicle Management (1C UAT)

Automation of management and operational accounting in motor transport organizations

- Management and operational accounting in motor transport enterprises

- Warehouse and logistics management

- Transport management

- Management of orders, statements and processing of travel documents

Read more Try for free

Let's look at the instructions for reflecting fuel and lubricants accounting manipulations in accounting. 1C Accounting program, formed on the 1C:Enterprise 8.3 platform. The table discusses the document flow depending on the company’s option for purchasing fuel and lubricants.

| Accounting operation | Employee reporting | Purchasing coupons for fuel and lubricants | Receipt of fuel and lubricants with distribution according to fuel cards |

| Acceptance of fuel and lubricants for registration |

|

|

|

| Write-off of fuel and lubricants for waste | Request-invoice |

Learn more about the table.

Accounting for fuel and lubricants

Fuels and lubricants purchased for the economic needs of the institution, according to Instruction No. 157n, are accounted for as part of inventories on account 0 105 X3 000 “Combustibles and lubricants”.

Organizations that use coupons for fuel and lubricants account for them separately - in account 0 201 05 000 “Cash documents”. Coupons can be purchased by bank transfer or through an accountable person (about accounting for monetary documents, see “Budget accounting: what are monetary documents and how to work with them in a budget institution”).

Form of the journal: your own or the state's?

To control the movement of issued waybills, an organization can keep a log of the movement of waybills in Form 8, approved by Decree of the State Statistics Committee of the Russian Federation dated November 28, 1997 No. 78. However, we would like to emphasize that from January 1, 2013, in connection with the entry into force of the Federal Law “On accounting" dated December 6, 2011 No. 402-FZ, the unified form is no longer mandatory.

An organization or individual entrepreneur has the right to develop its own journal form or supplement the unified one with the necessary information, provided that all points of the unified form are necessarily preserved.

As a rule, the journal is issued for a period of no more than 1 year, but if necessary, this period can be reduced to 1 month. The waybill journal is a primary document and its storage period is at least 5 years.

The procedure for writing off fuel and lubricants

Fuel and lubricants should be written off monthly. Use as supporting documents:

- waybill;

- advance report if gasoline was purchased in cash;

- journal for registering incoming and outgoing cash documents (f. 0310003), if the car was refueled using coupons;

- orders from the head of the institution, which approve the vehicle mileage rate, the fuel consumption limit for the month, depending on the make and model of the vehicle;

- sending an employee on a business trip in a company car.

Pay attention to the ratio of actual mileage and the established monthly limit. When writing off fuel and lubricants, be sure to take into account fuel consumption standards and mileage limits. If the car’s mileage is greater than the standards accepted by the management of the institution, and this excess is not justified by production tasks, the accountant uses exactly the approved limit when calculating gasoline consumption.

Use the data in the “Normal consumption” and “Actual consumption” columns. The data in them coincides in most cases. But if fuel consumption indicators differ, gasoline should be written off according to the lowest indicator, that is, if the norm exceeds the actual consumption, then gasoline is written off exactly according to the fact.

| Contents of operation | Debit | Credit |

| State institutions | ||

| Write-off of fuel and lubricants | 1 401 10 272 | 1 105 33 440 |

| Budgetary and autonomous institutions | ||

| Write-off of fuel and lubricants as part of income-generating activities | 2 106 34 340 | 2 105 33 440 |

| Write-off of fuel and lubricants as part of core business | 4 106 34 340 | 4 105 33 440 |

Example of waybill calculation

For example, let’s take a GAZ 3307 car, which transported goods throughout the city of Moscow. The basic fuel consumption for this car is 21 liters per 100 km, the correction factor for cities with a population of one million is 10% or 0.01.

The waybill contains the following parameters:

- vehicle mileage at the start of work – 20,000 km

- mileage figure at the end of the working day – 20,170 km

- remaining fuel before departure – 15 liters

- refilled during the trip - 60 liters

- remaining fuel at the end of the working day – 30 liters

The mileage during working hours is 20,170 km – 20,000 km = 170 km.

Now let's move on to calculating the fuel consumption rate:

- (21 l * 170 km) / 100 * 1.1 = 39.27 liters

Actual fuel consumption:

- (15 + 60) – 30 = 45 liters

The difference between the two values is:

- 45 liters – 39.27 liters = 5.73 liters

In fact, more fuel was consumed, which resulted in overconsumption. This is not a final figure; to correct it, you should check whether the fuel consumption occurred when the engine was idling, for example, during loading and unloading operations or warming up in winter.

To get the amount of fuel costs, you need to multiply the calculated fuel cost rate by its cost.

For each type of vehicle there is an approved unified form of waybill. Additionally, there is a form called 4-c. used for piecework wages, and 4-p – when paying for working hours. The rules and scheme for filling out waybills for institutions and individual entrepreneurs are reflected in the order of the Ministry of Transport of Russia under No. 152.

Top

Write your question in the form below

Tax accounting of fuels and lubricants

Accounting for travel vouchers is necessary to confirm expenses, the amount of which can be used to reduce the tax base for income tax. From a tax point of view, the cost of fuel and lubricants is included in other costs associated with production and sales. Consider the costs of fuel and lubricants as expenses for the maintenance of official vehicles (subclause 11 of clause 1 of Article 264 of the Tax Code of the Russian Federation), and these are non-standardized amounts. Moreover, these expenses require mandatory confirmation that they are economically justified. For example, a serious excess of fuel consumption from the values established by the order of the Ministry of Transport of Russia dated March 14, 2008 No. AM-23-r, may arouse the interest of regulatory authorities and lead to arrears and fines.

When calculating the amounts of expenses that reduce the tax base, it is necessary to take into account real expenses - not purchased fuel, but actually spent. These amounts are precisely what confirm the waybills, which means that they must be filled out with special attention.