Conditions for writing off and restoring VAT

Organizations purchasing goods and materials, paying for services or stages of work, receive VAT as part of their cost. Within the framework of the general taxation system, tax amounts are accepted for deduction in accordance with the rules of paragraph 1 of Art. 171 Tax Code of the Russian Federation. Namely, the amount of VAT on incoming goods and services is credited provided:

- goods are accepted for accounting;

- Inventories are used in activities subject to VAT;

- the operation has documentary confirmation: UTD, invoice, customs declaration from customs.

In practice, it looks like this: the acquisition is justified by documents that provide the right to deduction. The tax amount and the cost of the goods before tax are indicated on the invoice. The goods, intangible assets, fixed assets are credited to the balance sheet.

The goods are used in taxable transactions in the main activities of the organization: resold or released into production. If a transaction is carried out without tax (VAT is not charged), then the accounting policy must establish separate accounting for such transactions.

Let's remember the basics

VAT is a mandatory tax for all Russian companies that have chosen a common taxation system. For various types of goods and services it is 0/10/18%. The bottom line is that you already include this VAT in the price for the buyer. And he pays for it including tax. And at the end of the reporting period, all VAT must be calculated and paid to the budget.

But since you also buy part or all of the goods/services in Russia and, probably, from companies that pay VAT, you pay it to them, also including tax. Therefore, part of the quarterly tax can be deducted. That is, collect primary documents (invoices) indicating the added value paid for the quarter and pay to the budget the difference between how much was sold and how much was bought during the period. This is how primitive the scheme for calculating VAT payable for a quarter looks like.

There are several points in the law when the tax that you have already accepted as a deduction (because you bought the goods) needs to be restored and paid to the budget.

What are the requirements for the restoration of paid VAT amounts?

Restore the amount of paid tax in the accounting records, as required by the standard of clause 3 of Art. 170 of the Tax Code of the Russian Federation is mandatory in the following situations:

- the goods are contributed to the authorized or equity capital;

- the cost of inventory items decreases;

- used in activities that are not subject to tax;

- a subsidy was received from the budget for inventory items.

When an organization contributes shares or a share in the form of goods, inventory, fixed assets, and intangible assets to the authorized capital, it will be necessary to restore part of the previously accepted tax for deduction. The transaction is reflected in the sales ledger. The amount of restored VAT is calculated in proportion to the residual value of the contribution.

Financing goods purchased with budget money implies a benefit for the organization. If a transaction is made under a subsidy program, and the VAT amount was included in the report, then it must be returned to the budget and reflected in accounting.

The law does not provide for deduction and reimbursement for goods, and, accordingly, the restoration of VAT amounts in the presence of specific conditions:

- goods, intangible assets, fixed assets are not subject to VAT;

- the transaction was completed outside the Russian Federation;

- the seller is exempt from calculating and paying tax on the basis of Art. 145 of the Tax Code of the Russian Federation.

Considering the nuance that all circumstances do not provide tax for payment, there is no need to return VAT to the treasury.

Note! Until the end of 2021, this rule applied to federal subsidies. From 01/01/2017, when financing from the local treasury, VAT amounts are restored to payment.

When is it necessary to restore VAT?

1. When acquired property or assets are transferred to the authorized capital or contribution (if it is an investment partnership).

2. When the acquired assets are subsequently used in the following operations:

- Any actions with assets that are not subject to taxation or exempt from it.

- When sold outside the Russian Federation.

- When acquiring assets by persons who are not VAT payers.

- Upon subsequent transfer of assets for free use.

- Upon further transfer, not for sale or for use in activities not related to business.

3. When paying advances for upcoming deliveries.

4. In the event of a decrease in the cost of delivery as a result of a price reduction or a decrease in quantity.

5. In case of reimbursement of costs for purchased goods/services with the participation of government subsidies.

As you can see, there are no direct indications that VAT needs to be restored when writing off goods.

Recover VAT if the goods are damaged

For cases of intentional or accidental damage to property, accounting provides for the following operations:

Dt 19 Kt 68/2 – for the amount of VAT that we restore for payment;

Dt 91/2 kt 19 – the amount of tax (recovered and paid) is included in other expenses;

Dt 94 Kt 41 – the cost of the goods, which is fixed in an act that indicates the volumes of broken, broken, spoiled, expired goods and materials;

Dt 44 Kt 94 – the cost of losses is included in the cost of sales.

In practice, losses in such cases are included in expenses and are repaid at the expense of the organization. Unless otherwise provided by the internal regulations document or the agreement on liability. On this basis, losses are covered by the employee.

Accounting for VAT in case of shortage or theft of goods

Shortages or theft of inventory items are identified during the inventory process. The actual condition of materials in the organization is entered into the comparison sheet INV - 19. The basis for checking storage locations is an order in the form INV - 22. If inventory and materials are not sufficient in accounting and in fact, the reason for this is:

- underdelivery from the counterparty (reflected in the claim to the supplier);

- established fact of theft;

- natural rates of loss of inventory items.

Based on the results, the culprit is identified, at whose expense the organization’s losses will be written off.

If the damage is compensated by the culprit, the following entries are used:

Dt 94 Kt 10, 41 – for the amount and quantity of missing inventory items;

Dt 73 Kt 94 – damage written off at the expense of the culprit;

Dt 70 Kt 73 – the amount of damage is withheld from earnings;

Dt 91/2 Kt 94 - the amount of damage is charged to other expenses (if the culprit of the theft is not identified).

The question remains: how will VAT be restored when goods are written off in such cases? Practice is not clear-cut.

The tax service inclines organizations to restore and additionally pay VAT, which was accepted for offset in previous periods on inventory and other property. This position is supported by the Ministry of Finance in letter No. 03-03-06/1/1997 dated 01/21/2016.

Based on the list of rules under which VAT must be returned to the budget (clause 3 of Article 170 of the Tax Code of the Russian Federation), we will not see theft, shortage, or damage to goods and materials. Each case is considered individually by fiscal structures. For example, the same Ministry of Finance previously clarified that writing off inventory items due to a breakdown does not entail additional VAT payment. Even if the object is damaged and disabled. This is stated in letter No. 03-07-11/15015 dated March 19, 2015.

Although the Federal Tax Service of Russia itself later stated that it is not necessary to restore VAT when damage to the organization’s property was caused in an emergency situation (theft, fire). You can find out opinions about this in letter No. GD-4-3/ [email protected]

Judicial practice is developing in favor of organizations that risk challenging the position of the financial service. The arbitration also builds its arguments on the basis of the norms named in Art. 170 Tax Code of the Russian Federation.

The behavior of organizations in such cases is divided. The safest thing to do, some believe, is to restore and pay additional tax. The rest, relying on the positive practice of the FAS, decide to argue that the need for the Federal Tax Service’s requirement to restore VAT when writing off goods is unnecessary.

Note! The reason why they are required to pay additional tax is stated as follows. If a product is written off for any reason, not counting sales, it is not used in activities subject to VAT.

Should VAT be restored when writing off fixed assets? | "Garant-Service-Bryansk"

Often, due to the economic situation, a company has to write off excess property. The question arises whether VAT should be restored. Judging by existing arbitration practice, no.

Some inspectors believe that when writing off under-depreciated fixed assets, the amounts of VAT previously legally accepted for deduction are restored in the part attributable to the residual value of such property. Let's try to understand the legitimacy of this approach.

Legislation

Deductions of VAT amounts presented by company sellers when purchasing fixed assets are made in full after the said property has been registered*(1).

When selling a fixed asset that is subject to VAT, the amount of tax previously accepted for deduction is not restored. After all, the Tax Code establishes a closed list of grounds under which VAT amounts previously accepted for deduction are subject to restoration*(2):

— transfer as a deposit or shares; — further use for operations: not subject to VAT, or the place of sale of which is not recognized as Russia, or which are not recognized as sales, or carried out within the framework of UTII and the simplified tax system or in activities for which an exemption has been obtained; — transfer by the buyer of an advance payment; — change in shipping cost downwards; — further sale with a tax rate of 0 percent;

— receiving subsidies from the federal budget to reimburse costs associated with paying for purchased goods (works, services), including tax, as well as to reimburse the costs of paying tax when importing goods into Russia.

As you can see, the list of grounds for VAT restoration does not include the sale of a fixed asset.

Explanations from officials

Previously, representatives of the Russian Ministry of Finance said that previously accepted for deduction VAT amounts on acquired fixed assets written off before the end of the depreciation period are restored*(3).

Officials explained this by saying that the tax is subject to restoration in cases where the acquired fixed assets are not used in taxable activities.

Later, the department clarified its point of view on operations related to the implementation of OS * (4). Officials said that the previously deductible VAT on fixed assets sold should not be restored. VAT is restored in cases of further use of property in non-taxable transactions. Meanwhile, when selling property, taxes are charged.

Arbitration practice

Inspectors continue to argue that when selling fixed assets with a residual value, the previously made VAT deduction becomes redundant and must be restored. They explain this by the fact that the fixed asset, if sold, is excluded from the subsequent production activities of the company.

Arbitration practice is entirely on the side of firms. And this is not surprising. After all, the arguments of those people who believe that if a fixed asset is sold, even at a loss, will not have to be reinstated are much more convincing. As mentioned earlier, the list of grounds for reinstating the value added tax does not include the sale of fixed assets.

At the same time, officials also do not refer to the unreasonableness of deducting VAT during periods of property acquisition.

Therefore, the tax authorities’ argument that when writing off fixed assets with a residual value, the previously made deduction becomes redundant is regularly rejected by the courts *(7).

As we can see, the Tax Code does not contain rules obliging a company that has written off a fixed asset from its balance sheet due to its sale at a loss to restore the amount of VAT from the under-depreciated part.

If it is decided to restore VAT

If the company decides not to argue with the tax authorities and restores the tax, then the amount of tax to be restored must be calculated based on the residual (book) value without taking into account revaluation. In this case, the recoverable VAT can be taken into account for income tax as part of other expenses associated with production and sales * (9).

The amount of tax to be restored is calculated based on the residual (book) value without taking into account revaluation. In our case, the residual value of the fixed asset is:

100,000 - 20,000 = 80,000 rubles. Therefore, the recoverable part of the VAT: RUB 80,000. x 18% = 14,400 rub.

The company takes this amount into account when calculating income tax as part of other expenses.

Accounting for recovered VAT amounts in the purchase ledger

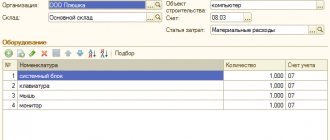

The tax is entered into the purchase book when goods are received at storage locations, based on an invoice or UPD. Reflected by the “Receipt” operation, where the details of the supplier’s documents, the name of the product, its price and quantity, the amount of input tax, and the total cost are indicated.

A transaction is automatically created:

Dt 68 Kt 19 – tax credited.

1 Option for tax recovery

The goods are written off directly using the “Write-off of Inventory and Materials” document. Created on the basis of capitalization, indicating the reasons for the operation. For example, “writing off materials due to theft, wear and tear, impossibility of use or sale. VAT has been restored." The reversal entry will appear after posting the document.

2 Tax restoration option

In the section of typical regulatory operations, you need to select “VAT recovery”. In the header, select where you want to reflect the tax amount. In our case, VAT will be reflected in the sales book. The tabular part is intended for information about the incoming document, on the basis of which the organization charges additional tax.

To write off VAT as expenses, you will need to check the box in the window; the posting of the write-off of losses will be reflected in accounting after posting the document.

This function is also used to reflect the restored VAT amount in the purchase book.

Reporting on recovered VAT amounts

The restored tax itself will be reflected in an additional sheet of the sales book. The amount that is restored for payment is entered in section 3 of line 090. If the restored tax is related to real estate, you will need to draw up Appendix No. 1 in addition to section 3.

It is compiled separately for each property. It is provided to the tax office as part of the reporting for the 4th quarter of the reporting year and only once a year. This is indicated by paragraph 39 of the letter of the Federal Tax Service of Russia dated December 20, 2016 No. ММВ-7-3 / [email protected] ). The appendix contains a calculation of the amount of VAT that is restored on real estate. The total amount of tax on line 080 of Appendix No. 1 is transferred to line 090 of section 3 of the report for the year. The details of the export tax and the procedure for its restoration can be read in a separate topic.