Article 164 of the Tax Code of the Russian Federation allows not to impose value added tax on the sale of goods outside the Russian Federation, that is, the tax rate for this transaction is zero. In this case, the exporting company, along with the tax return, must, within 180 days, submit to the fiscal authority documents confirming the right to use a 0% rate. Next, we will tell you how to carry out the necessary operations in 1C in order to satisfy all the requirements of current legislation.

VAT not confirmed - pay tax

Elena Aleksandrovna Emelyanenko, leading expert consultant at PRAVOVEST

The procedure for determining the tax base when carrying out export operations raises numerous questions among exporting organizations. For example, what should an accountant do if the documents confirming an export delivery were not collected on time?

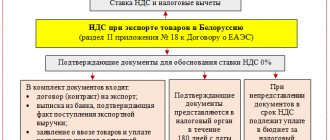

When selling goods exported outside the Russian Federation, organizations must, within 180 days from the date of shipment (transfer) of goods, submit to the tax authority simultaneously with the declaration the documents provided for by the Tax Code of the Russian Federation, to justify the application of the zero VAT rate. By submitting a VAT return at a rate of 0 percent with a package of documents to the tax authority before the expiration of the established period, the exporter confirms not only the validity of the application of this tax rate, but also the very fact of the sale of goods (work, services) in the territory of the Russian Federation. Therefore, if an organization has not collected a complete package of documents on the 181st day, then it is considered that it was unable to confirm real exports and a zero VAT rate. In this case, the sale of goods (work, services) is subject to VAT in accordance with the generally established procedure, and the exporting organization needs to:

- charge VAT on export proceeds of undocumented shipments;

- reduce the accrued tax by the amount of input VAT on purchased (accepted for registration) goods (work performed, services provided) used for the production and (or) sale of goods for export;

- pay accrued VAT to the budget minus input VAT;

- accrue and pay “penalties for each calendar day of delay in fulfilling the obligation to pay tax, starting from the day following the tax payment date established by law”;

- submit a tax return for the tax period in which the day of shipment (transfer) of goods falls.

Counting date Accountants are often faced with the question: from what point should they count the 180 days required to submit a declaration and a package of documents to the tax authority? In para. 2 clause 9 art. 167 of the Tax Code of the Russian Federation states that the 181st day is counted from the date of placing goods under the customs regime of export, that is, from the day of release of goods by the customs authority, confirmed on the customs declaration. Sometimes the declaration of Russian goods is formalized by the customs authority on the basis of a temporary declaration. Article 138 of the Customs Code (hereinafter referred to as the Labor Code of the Russian Federation) stipulates that in the case of periodic declaration, a temporary customs declaration is first submitted to the customs authority, and after the goods leave the customs territory of Russia, a full customs declaration is submitted. Currently, the Tax Code of the Russian Federation does not specify which customs declaration should be used to calculate the 180-day period. Federal Law No. 119-FZ of July 22, 2005 “On Amendments to Chapter 21 of Part Two of the Tax Code of the Russian Federation...” amended Art. 165 Tax Code of the Russian Federation. The word “cargo” was excluded from it and only the concept of “customs declaration” was left. It follows from this that when selling goods for export that are subject to a special declaration procedure using periodic declarations, the calculation of the 180-day period established by the Tax Code for collecting documents confirming the legality of applying a VAT rate of 0 percent must be made from the one stamped on the temporary declaration the date of placement of goods under the customs export regime.