In practice, to speed up payments by counterparties for shipped goods, various systems of discounts and incentives are used. For example, a 10% discount for prepayment of goods. Sources of formation of receivables Let us highlight the main sources of formation of receivables:

- debts of buyers and customers;

- advances issued;

- debts of subsidiaries;

- debts of the founders for contributions to the authorized capital;

- bills;

Types of receivables Based on the maturity of obligations, receivables are divided into:

- Short-term accounts receivable – payments due within 12 months.

- Long-term accounts receivable – payments due over 12 months.

Video lesson “Settlements with buyers and customers.

The amount is ridiculous, but there is a lot of fuss

The most common are the debt of buyers for products shipped but not paid for (work, services), and the debt of suppliers for listed advances that were not covered by deliveries. Let's see how writing off debtors' debts affects the calculation of income tax, VAT and the simplified tax system: The nature of the debt Income tax VAT simplified tax system Indebtedness of the buyer for goods sold, work services Written off debt is included in expenses in the full amount (including VAT) (Letters from 07/24/2013 No. 03-03-06/1/29315, dated 08/03/2010 No. 03-03-06/1/517)1. If a reserve for doubtful debts was created for tax accounting purposes: - the written off debt reduces the amount of the reserve (regardless of whether this debt participated in the formation of the reserve or not) (Letter of the Ministry of Finance dated July 17, 2012 No. 03-03-06/2/78, paragraphs 2 items 2 items

Statute of limitations

Determining the limitation period is a key issue that is relevant for both the creditor and the debtor when determining the period for debt write-off. It begins to flow from the moment when the creditor became aware of the violation of contractual obligations by the debtor (Civil Code of the Russian Federation, Art. 200-1). It is possible to restore the statute of limitations only in certain, exceptional cases that are not applicable to the relationship between the parties to the contract in practice (Civil Code of the Russian Federation, Article 205).

The law recognizes each individual agreement as a separate obligation. The limitation period is also calculated separately for each contract. The deadline for filing a claim may be suspended, for example, if the legal act regulating the dispute has been suspended (Civil Code of the Russian Federation, Article 202).

Quite often, the statute of limitations can be interrupted, in other words, “stretched,” and last more than 3 years. The debtor’s administration can recognize the debt (Civil Code of the Russian Federation, Art. 203) in one of the following ways (according to the text of post. No. 43 of the Plenum of the Supreme Court of September 29, 2015):

- by partially paying for it;

- by sending a letter to the creditor with a request to defer payment or delay delivery of goods or services;

- by signing the act of mutual settlement, reconciliation of settlements;

- acknowledging the debt in an official letter addressed to the business partner;

- changing the text of the agreement, from which it follows that the debtor has recognized his debt.

During this period, the accountant cannot write off accounts payable as overdue. The term can be interrupted only during the period established by law for the limitation period, and not after its completion. At the same time, recognition of the debt in part (including payment) is not equal to recognition of the debt as a whole. In addition, if the agreement stipulates repayment in parts, by making periodic payments, then recognition of one part (including its payment) does not interrupt the statute of limitations for other parts of the total debt.

Example: A company signed an agreement with a counterparty for the installation and debugging of new software. The work acceptance certificate was signed by the parties on May 15, 2021. Payment for services must be made, according to the agreement, no later than May 23, 2021. The limitation period begins to count from May 24, 2021. It will expire on May 24, 2022. Please note: the accounts payable actually arose on May 15, 2021, when the act was signed, but the statute of limitations is counted from that specified in the agreement.

On a note! The period during which the statute of limitations is interrupted and resumed cannot exceed 10 years (Civil Code of the Russian Federation, Art. 196-2).

In what cases can the running of the limitation period be changed?

According to Art. 203 of the Civil Code of the Russian Federation, the limitation period is interrupted if the debtor has taken any steps indicating his consent to acknowledge the debt. These steps could be:

You can find more complete information on the topic in ConsultantPlus. Full and free access to the system for 2 days.

- partial repayment of debt;

- the debtor's request for a deferred payment;

- acceptance of collection order;

- payment of interest on the principal debt;

- signing a statement of reconciliation of accounts.

The statute of limitations is suspended if, due to circumstances beyond their control, the parties are unable to fulfill the obligations associated with repaying the debt during the following period (Article 202 of the Civil Code of the Russian Federation):

- six months;

- the entire limitation period - if its duration is no more than 6 months.

The limitation period may be terminated if the debt obligation itself has been terminated, in accordance with Art. 414-419 of the Civil Code of the Russian Federation, in the following cases:

- debt write-off by the creditor;

- death of an individual acting as a debtor or creditor, if payment of the debt cannot be transferred to other persons;

- liquidation of a person acting as a debtor or creditor, if payment of the debt cannot be transferred to other persons;

- innovations of obligations;

- termination of debt by decision of a government agency.

The duration of the limitation period cannot exceed 10 years (Clause 2 of Article 196 of the Civil Code of the Russian Federation).

Write-off of receivables and payables

The amount written off is recognized as non-operating income. Control over the execution of the order is assigned to the chief accountant. The sample can be downloaded here. Procedure The procedure for writing off short-circuits takes place in four stages:

- Identification of the amount of overdue debt during the inventory at the end of the reporting period.

- Drawing up an accounting certificate for the identified shortcomings.

- Issuance by the director (manager) of the company of an order to write off debt on the basis of regulatory documents.

- Making appropriate changes to accounting and tax accounting by the accounting department.

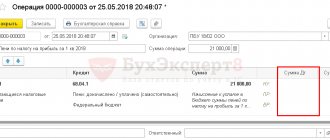

In accounting, write-off is carried out on the basis of the following entry: Debit 60 – Credit 91-1 Taxation Tax accounting requires registration of arrears during the period when the statute of limitations expired.

We write off an overdue creditor in accounting

Write-off of expired debt, in accordance with clause 10.7 of PBU 9/99, is documented by posting:

Dt 60 (66, 68, 69, 73, 76) Kt 91.1 - expired debt written off, where:

- accounts 60, 66, 68, 69, 73, 76 - settlements with suppliers, for loans and borrowings, with the budget and extra-budgetary funds, personnel, various creditors and debtors;

- account 91.1 - “Other income”.

Accounts payable are written off separately for each counterparty and each debt obligation. If the agreement specifies the accrual of interest or penalties in case of untimely fulfillment of obligations, then they are also taken into account separately.

Interest accrued for late payment of debt is written off as follows:

Dt 76/pr Kt 91.1 - interest arising as a result of non-payment of debt is written off,

where account 76/pr - “Interest taken into account as part of debt with an expired statute of limitations.”

Overdue debt denominated in foreign currency is recalculated into rubles at the official exchange rate of the Central Bank of Russia at the time of write-off. The resulting exchange differences are written off in accordance with paragraphs. 11, 13 PBU 3/2006 as part of other income or losses at the time of write-off of the principal debt.

Reflection of the write-off of accounts payable in accounting

Written off accounts payable generates income, which is reflected in accounting in account 91, subaccount “Other income” (clauses 7 and 10.4 of PBU 9/99 “Income of the organization”). The wiring will be like this:

Debit 60 (62, 66, 67, 70, 71, 76) Credit 91, subaccount “Other income”,

– the amount of accounts payable with an expired statute of limitations is written off.

Such an entry is made on the date of approval of the inventory results (part 4 of article 11 of the Federal Law of December 6, 2011 N 402-FZ “On Accounting”, clause 10.4 and paragraph 4 of clause 16 of PBU 9/99).

Since paragraph 78 of the Regulations states that accounts payable must be written off in the reporting period in which the statute of limitations for them has expired, based on inventory data, a written justification for the reason for the write-off and an order.

How to write off accounts payable from previous years in accounting

In accounting, “overdue” KZ is subject to accounting as a credit to account 91 (subaccount 1) as part of other income.

Depending on which account a specific short-term loan was accounted for, the write-off of accounts payable will be documented by posting D 60 (62, 66, 67, 70, etc.) K 91-1.

Postings when writing off faults and faults

This operation is carried out only if the commission makes a decision on which the appropriate procedure needs to be carried out. All overdue indicators are indicated on account 0.401.10.173. It is used in all cases when it is necessary to write off a creditor or debtor in a government institution. The regulations specify various points:

- 150 (instruction 174n);

- 178 (inst. 183n);

- 167 (162n).

Unclaimed credit is written off from the balance sheet when an inventory is taken and an accounting control act is signed. This difference from a similar procedure performed in commercial enterprises is very important. After all, the whole order of actions changes because of this, and the wiring is completely different.

The following entries are made:

- Dt 2.302.25.000 Kt 2.401.10.173 - this means writing off unclaimed credit debt.

- Dt 20, which implies the removal of short-term or additional liability from the main balance sheet.

Only a trained person with suitable qualifications and education should carry out all calculations and fill out the relevant documents. The document can be drawn up either by a full-time accountant or by someone invited for one-time work from an agency specializing in the preparation of reporting documents.

If non-professionals or incompetent persons work with documentation, then inconsistencies may arise, which will entail not the best consequences. Of course, this state of affairs is not desirable for any enterprise.

Account 62 in accounting. writing off accounts receivable. postings

Written off debt is included in non-operating expenses regardless of the fact of creating a reserve for doubtful debts in tax accounting, since receivables for prepayment to a supplier are not considered doubtful for tax accounting purposes and, accordingly, are not included in the formation of the reserve. (Letter from the Ministry of Finance of Russia dated June 30, 2011 No. 07-02-06/115) VAT on the advance payment, previously accepted for deduction, must be restored during the period of writing off receivables (Letter of the Ministry of Finance dated 04/11/2014 No. 03-07-11/16527) Written off debt is not taken into account in expenses (Letters Ministry of Finance dated March 30, 2012 No. 03-11-06/2/49, dated December 12, 2008 No. 03-11-04/2/195) As can be seen from the table, the procedure for including written-off receivables into expenses when applying the general taxation system depends on whether the organization created a reserve for doubtful debts in tax accounting or not.

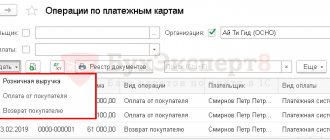

Writing off accounts receivable in 1C 8.3: step-by-step instructions

Using an example with postings, we will study how to write off accounts receivable in 1C 8.3.

The accounts include receivables from Azbuka Comfort LLC dated October 28, 2015 in the amount of RUB 159,300. For doubtful debts, the Organization previously created a reserve in the accounting and accounting departments.

On October 30, we conducted an inventory of settlements with the counterparty. Expired debts were written off against the reserve.

Formation of a settlement inventory report

Carry out an inventory of settlements with the counterparty and reflect its results in 1C with the document Settlements Inventory Act through Sales - Settlements with counterparties - Settlements Inventory Acts.

Reflect the amount of debt for which the statute of limitations has expired in the column Incl. the statute of limitations has expired .

Debt write-off

Write off the debt using the document Debt adjustment through Sales - Settlements with counterparties - Debt adjustment.

Please indicate in the form:

- Type of operation - Debt write-off ;

- Write off - Buyer's debt ;

- Buyer (debtor) is the counterparty whose debt is written off.

Clicking the Fill will display all receivables from the counterparty in the tabular section.

Now let’s select the accounts receivable write-off account in the debt adjustment: on the Write-off account , indicate account 63 and fill out the analytics (contract and unpaid sales document) for which the reserve was created.

If a debt reserve was not created, then create the Write-off account as follows:

- Account - 91.02: account where income will be reflected;

- Other income and expenses - an article with the Type of article - Write-off of receivables (payables) .

If the reserve was created only according to accounting records, then you will need to adjust the transactions or use the document Transaction entered manually .

Postings

Learn more about the regulatory framework for writing off accounts receivable

Advantages and disadvantages

The importance of managing accounts payable is that its condition is reflected in the solvency and liquidity indicators of the enterprise.

Simply put, a large volume of non-recoverable but not written off accounts payable reduces the solvency and financial attractiveness of the company.

But writing off loan debts has both advantages and disadvantages. It is beneficial to write off accounts payable in order to increase the taxable profit of the organization.

For example, during the reporting period the organization experienced losses, the amount of which exceeded the amount of debt.

It will be unprofitable to write off accounts payable in the tax period in which a profit was received that significantly exceeds the amount of the debt.

It will not be possible to compensate the debt through losses upon write-off. All non-operating income must be included in the tax base.

Therefore, it is more expedient for an organization to extend the limitation period, if possible, which will allow the write-off to be completed during a period with a lower tax burden.