Sometimes organizations need to buy or sell foreign currency. The situation can be many things. For example, you import or export goods, send employees on business trips abroad, repay a loan in foreign currency, etc.

Current legislation obliges organizations to revaluate currency balances into rubles at the established rate. If an exchange rate difference arises in a positive direction for you, it is reflected as other income in accounting and as non-operating income in NU. The amount of the negative difference is taken into account in the same way, only for expenses.

In this article, we will use an example to look at how currency conversion operations are carried out in 1C 8.3 and consider their transactions, namely the purchase and sale of currency.

Preliminary setup 1C

Before you start working with currency, you need to configure the program.

In the event that a transfer between a foreign currency and ruble account takes more than a day, you will need to use an intermediate account.

Our team provides consulting, configuration and implementation services for 1C. You can contact us by phone +7 499 350 29 00 . Services and prices can be seen at the link. We will be happy to help you!

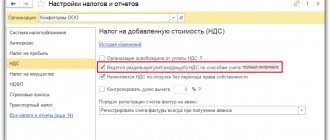

From the “Main” section, go to your company’s accounting policies.

In the window that opens, find the item called “Account 57 “Transfers in transit” is used when moving funds” and mark it with a flag. This add-on does not need to be enabled.

It is also recommended to check the installation of another add-in. In the "Administration" menu, select "Functionality". In the settings window that appears, open the “Calculations” tab and check whether the checkbox for “Calculations in foreign currency and monetary units” is checked. We already had it installed by default.

How to get

The frequency and form of providing current account statements is established by the bank independently, in accordance with its own regulations and current legislation.

Regular reports on account cash flows are provided by the banking institution in the following ways:

- personally to the client when visiting a financial institution;

- by post;

- via email;

- in online format.

Urgent statements are issued:

- by a bank manager in person;

- in the user’s personal account on the official website of the institution;

- by telephone;

- via SMS;

- using an ATM.

To receive an urgent statement, you will need to submit a corresponding application to the bank. In addition, it is necessary to take into account the presence of commissions for generating statements on demand, which may be provided for by bank tariffs.

The standard application for an extract contains:

- Full name, registration address - for individuals, full and abbreviated names - for organizations;

- indication of the requested time period;

- the reason for the application;

- date of the document, signature of the applicant.

If the client loses the original statement, the bank can provide a copy of the document upon request.

Loading exchange rates

In the “Directories” section, select “Currencies”.

You will see a list of all currencies added to the program with their rates. In this form, click on the “Download exchange rates...” button.

The program will prompt you to select those foreign currencies for which you need to download rates. Select the checkboxes and click on the “Download and Close” button. The default is the current date, but it can be changed.

Now you can proceed directly to our example of selling and buying currency in 1C 8.3.

What is a bank statement?

An account statement is a financial reference document that allows you to track all transactions (expenses and receipts) for a day or for a certain period. Receiving such a certificate can confirm or refute the fact of crediting/writing off funds, as well as justify the calculation of income tax.

Let's look at what it contains and how it works.

There is no specific form in which a bank statement must be provided that is specified in any law or regulation. However, there is a list of information that the document must absolutely contain:

- The name of the financial institution and its main details – BIC and correspondent account;

- Client's name and current account;

- Date of preparation;

- Date of previous statement;

- Account balances at the beginning and end of the day;

- All transactions of incoming and outgoing funds.

Moreover, each operation reflected in the document contains:

- date;

- No. of the document on the basis of which the transaction was carried out;

- counterparty account and correspondent bank details;

- amount.

Statements are generated daily for the current accounts of companies and entrepreneurs. But you need to pick it up yourself, at a convenient time. Some banks also practice other methods of receiving, which we will discuss below.

You will have to request an account statement for an individual; no one will generate it automatically. In this case, the account owner himself determines for what period the document will be generated. The receipt time in this case is determined by the bank’s conditions and can range from several minutes to 3 business days. The same period is provided for account statements of legal entities and individual entrepreneurs, if the period for which they are compiled exceeds the standard cash day.

You can see a sample statement below.

Sale of currency

Write-off of foreign currency

Let's consider an example when our organization needs to sell $7,000 to Sberbank for rubles. Initially, a payment order is created in 1C and, based on it, debited from the current account. We will not consider the payment order itself, and will immediately move on to processing the write-off, since it is this order that makes the necessary transactions.

Specify “Other settlements with counterparties” as the type of transaction. The recipient in our case is PJSC Sberbank. We have already concluded an agreement with him with settlements in USD. It is selected in the card of this document. The picture below shows a card of this agreement.

We will also write off accounting account 52 (Currency accounts) and settlement account 57.22 (Sales of foreign currency). In addition, you must indicate your organization and bank account.

Let's review the document and look at its postings. You can see that not only the write-off itself was reflected, but also exchange rate differences.

If the currency has changed its value since the last currency transaction, a posting will be added to 1C for calculating the revaluation of currency balances (if revaluation is configured).

Receipt to the current account

After the bank receives $7,000, it will transfer it to us in ruble equivalent. The program takes into account the document receipts to the current account.

The receipt is filled in automatically after unloading from the client bank. However, it is recommended to check the completed details, especially the account and amount.

The movements of this document are shown in the figure below.

The essence and definition of transactions in foreign currency

In order to separate the company's funds, expressed in national and foreign banknotes, it is necessary to open appropriate accounts in the so-called authorized commercial banks. All transactions on these accounts will be reflected by the accounting service in 52 positions, which will be discussed further.

If we try to define the concept of “currency transactions,” then they should be understood as actions aimed at fulfilling or otherwise terminating obligations expressed in the currency of another state, as well as using the currency of another state as a means of payment.

Such transactions include:

- actions for the purchase and sale of banknotes of other states;

- use of foreign banknotes as a means of payment;

- fulfillment of foreign economic obligations in Russian rubles;

- import and export of foreign banknotes.

Such transactions occur:

- in case of conversion of monetary resources from one currency to another by business entities and citizens;

- when using foreign banknotes for making payments on the international market.

There are a lot of regulatory documents adopted at different levels of government that regulate the procedure for conducting transactions in foreign currency on the territory of the Russian Federation. One of the key documents in this area is the national law “On Currency Regulation and Control”.

There are a lot of criteria that allow you to classify such operations. If we take the object as a basis, we can distinguish transactions in the national currency of the Russian Federation and foreign currency, as well as transactions with national and foreign securities.

Based on the subjects of this type of transaction, transactions are divided into transactions between residents and non-residents of the Russian Federation.

If we talk about control over transactions with foreign banknotes, it is carried out by agents and government bodies, including the Russian Central Bank and the Ministry of Finance.

As for the accounting of assets and liabilities denominated in foreign currency, this procedure is reflected in a special Regulation approved by the relevant order of the national Ministry of Finance.

Features of document formation

Statements in most cases are issued the next day after the movement of money through the organization’s bank account. The important features of document formation are two columns in which debit and credit are reflected. The first reflects funds debited from the account, the second - credits made to the account.

The company's account with a credit institution is a settlement account, in other words, the bank stores money belonging to the client on it. When considered a debtor, the financial institution displays the account balance as accounts payable. Due to the fact that the company's account for the bank is passive, the balance of funds is displayed in the loan statement. Financial assets written off from the organization’s account reduce the debt of the credit institution, so the debt to the client becomes less. For an organization, it's exactly the opposite.

Procedure for working with a current account statement

Upon receipt of a bank report on incoming and outgoing transactions on the account, the enterprise accountant checks and processes the document in accordance with the established procedure:

- Selection and attachment to the report of all documentary evidence.

- Reconciliation of reporting information with primary documentation. If errors are detected, immediately notify the banking organization.

- Making marks indicating accounting account codes.

- Selection of primary documents according to the order of transactions indicated in the statement.

Upon completion of processing, the extract must be filed with the primary documentation.

Primary analysis of bank statements on an account allows you to:

- control the current state of the account, making timely adjustments to its functioning;

- automate accounting in the company;

- Conveniently archive and systematize document flow.

When individuals may need a bank statement

The activities of banking organizations are aimed at providing financial services to companies and individuals. Any citizen can have a current account in the chosen bank, as well as a plastic card linked to it, all transactions for which are reflected in the statement.

For the convenience of users, banks provide a confirmation document in a mini format that can be printed at an ATM.

There are a number of situations in which bank clients need to receive an extended statement. These include:

- visa application;

- obtaining a loan;

- confirmation of financial position at the conclusion of the transaction;

- other circumstances requiring documentary evidence of trustworthiness and absence of debts.

To receive a statement, an individual must contact the bank directly, presenting an identification document and a banking service agreement.

Where to get a statement if the bank is closed

Let's say a customer purchased a car in 2021. In 2021, the tax organization asked it to report and present an extract confirming the origin of the money. At this point, the client may face the problem of presenting a statement, since many banks have gone bankrupt. Let's figure out what to do in such a situation and how to get an extract.

The first thing to do is find out who has been appointed by the temporary administration . To do this you need:

- go to the official website of the Central Bank;

- enter the “Banking Sector” section;

- select “Liquidation of credit organizations.

A list will open in which you need to select the name of the bank where the account was opened and view the order appointing a temporary administration. Then contact them to receive an extract.

You can obtain information through the official website of the DIA , in the “liquidation of banks” section.

It is important to take into account that according to clause 1 of Article 189.27 of Federal Law No. 127 of October 26, 2002, the temporary administration works for 6 months. In some cases, the period may be extended to 18 months.

You can obtain an extract from the curator. The report on the website will indicate his phone number and full name.

Doubts about electronic statements

Is a bank account statement required to be printed? This question is a cornerstone for many accountants whose enterprises have implemented an electronic document management system, for example:

- 1C accounting system;

- “client-bank” with a credit institution and one of the existing systems - with tax and regulatory structures.

The situation is aggravated by many factors:

- Regulatory:

- there is no legal provision that would directly prohibit or permit the storage of a document in electronic form;

- The general rule of Article 9 of Federal Law No. 129 applies, according to which a business entity, at the request of an authorized official, is obliged to produce and provide primary documentation for verification at its own expense.

- Actual:

- when switching to an online service system, banks are massively refusing to issue statements, offering clients, if necessary, to print and certify them themselves;

- electronic document management is usually implemented by medium and large institutions, many of which have not one, but several current accounts, through which more than 100 transactions are carried out daily - paper statements have the appropriate length;

- the rules for storing these documents require that supporting documents be attached as attachments, which in most cases will also have to be printed; all this heap of papers needs to be stapled and stored, and this means extra costs for office supplies, archive maintenance, and employee wages.

Tips for those who use electronic statements

Legal policies and regulations are gradually moving towards computerization of financial and tax reporting. This is evidenced by the fact that every year the state is expanding the circle of persons required to submit reports to the Federal Tax Service and extra-budgetary funds in electronic form. Today, the question of whether a bank statement from a current account can be in digitized form clearly implies a positive answer.

The absence of printed statements gives the document flow some specificity. With paper accounting, bank statements with paper invoices attached to them, issued by counterparties for payment, must be filed and transferred for storage. Electronic or mixed document flow presupposes, accordingly, the existence of a digitized archive. However, this process is subject to proper registration by local regulations (manager’s order, regulations, instructions), and archival files must be certified.

Not only people fail, but also technology. The server or hard drive may fail. There is one more issue - organizational. The peculiarity of the “client-bank” system is that in the event of a reorganization of a bank branch (enlargement or, on the contrary, separation), as well as the liquidation of a branch and the transfer of a client for service to another, the “old” documents will disappear from access. Therefore, you need to take care of regular (ideally daily) archiving of data to external media.

The organization is expected to ensure that this data is retained for a sufficiently long period of time. They can be requested at any time not only when checking the account owner, but also to analyze the work of the counterparty. As already noted, in accordance with Art. 40.1 dated December 2, 1990 No. 395-1, financial institutions are required to save data on transactions performed for 5 years. Organizations can rely on this period or on the general limitation period - 3 years.

It must be remembered that a bank statement may always be required for your own needs or to be provided to the tax authority for the purpose of conducting an on-site or counter audit. Therefore, whether paper or digital documents, they should always be at hand and organized into an easy-to-find system.

Tinkoff Bank current account statement

Tinkoff Bank is a special bank that does not have offices and operates only remotely. It is especially convenient for bank clients to work using Internet Banking. It has a lot of functions that make the work of entrepreneurs much easier.

The statement received from the bank contains basic information:

- Billing period;

- Outgoing balance;

- Amounts of expenses and revenues;

- Dates and times of all bank transactions.

The statement can be obtained almost instantly in the user’s personal account. If the user does not have Internet banking configured, you can download a special application on the bank’s website and create your account.

What information is included in the statement?

Bank account statements may differ slightly in appearance because they are printed on different technologies. It is more important to find out what information is indicated in the statement.

- “Posting date” – the date of the transaction on the client’s account;

- “Recipient’s account” – recipient’s current account number;

- “VO” – type of financial transaction;

- “Nom. doc. Bank” – incoming document number;

- “Nom. doc. Client” – payment document No.;

- “BIC bank corr” – BIC of the recipient’s bank;

- "Corr. Account” – a corresponding bank account;

- “Payer’s account” – payer’s account number;

- “Debit” (client arrival);

- “Credit” (customer expense).