What the law says

The Tax Code of the Russian Federation, as well as its norms devoted to simplifications, does not say whether state duty is accepted as expenses under the simplified tax system. At the same time, companies and individual entrepreneurs using the simplified tax system are faced with this mandatory payment everywhere: in court, in the tax service, and in other structures. That is, it can be argued that without paying state duties, activities under the simplified regime are virtually impossible.

However, we can safely conclude that the state duty under the simplified tax system is included in expenses on the basis of subclause. 22 clause 1 art. 346.16 Tax Code of the Russian Federation. This paragraph lists the costs that, in the final calculation, reduce the single tax on the simplified tax system.

This norm mentions only taxes and fees paid in accordance with tax legislation. So is the state duty an expense under the simplified tax system? Definitely - YES!

Issues related to state duty are regulated by Chapter 25.3 of the Tax Code of the Russian Federation. Based on paragraph 1 of Art. 333.16 of the Code, the state duty refers specifically to fees when applying to:

- Government structures.

- Local authorities.

- Other bodies and/or officials who are legally authorized to perform legally significant actions.

There should be no controversy as to whether state duty is taken into account in expenses under the simplified tax system when a document or a duplicate of it is issued to a simplifier for a fee. Yes, this is equated by law to legally significant actions.

As follows from the meaning of sub. 22 clause 1 art. 346.16 of the Tax Code of the Russian Federation, state duty is accepted as expenses under the simplified tax system in any amount upon its transfer to the treasury to the appropriate account.

Another important point: the state duty is taken into account in expenses under the simplified tax system also when calculating the advance payment.

Expenses for a simplifier arise only from the date of its state registration as an individual entrepreneur or legal entity. Therefore, up to this point, the state duty paid for the initial registration is the personal costs of the founder (owner). Therefore, it cannot be taken into account on the simplified tax system.

A simplifier can save a little when installing an advertising structure. The state duty is included in the costs of the simplified tax system if it is transferred for this service, permitted by local authorities. For 2021, its size is 5,000 rubles.

At the same time, the simplifiers have no right to attribute the fee for the right to install and operate an advertising structure as expenses. The Ministry of Finance and the Federal Tax Service believe there, since clause 1 of Art. 346.16 of the Tax Code of the Russian Federation there is no corresponding position (letters dated 09/01/2014 No. 03-11-06/2/43627 and dated 08/06/2014 No. GD-4-3/15322).

Accounting entries for accounting for state duties in expenses under the simplified tax system

An important point: according to the regulations of Article 333.40 of the Tax Code of the Russian Federation, before recording transactions for accrual of fees in accounting, you must remember that in some cases the amount of the paid duty can be returned, but it can also be offset against other mandatory payments to government agencies at the request of the payer. Based on this, it follows:

Before the actual commission of a legally significant action on the part of government agencies (or if it is refused), the state duty cannot be taken into account as an expense either in tax or accounting.

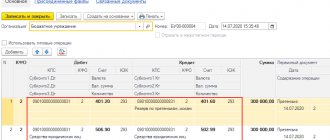

The state duty collected when interacting with government bodies is reflected in accounting in a special subaccount to account 68.

The entries for this subaccount are as follows:

- Dt 68 / Kt 51 (50) - payment of state duty;

- Dt 20, 23, 25, 26, 29, 44, 91 / Kt 68 - charge of state duty;

- Dt 91 / Kt 68 - payment of state duty is included in non-operating costs in case of refusal to perform a legally significant action;

- Dt 08 / Kt 68 - increase in the initial cost of the depreciable object by the amount of the state duty;

- Dt 51 / Kt 68 - return of the amount of paid state duty to the company’s bank account.

Court fee

By virtue of subparagraph 31 of paragraph 1 of Article 346.16 of the Tax Code, simplifiers with the object “income minus expenses” can take into account the costs of:

- Court expenses.

- Arbitration fees.

Thus, the costs of state fees to the court can always be taken into account on the simplified tax system. Moreover, simplifiers do this on the date of payment, and not on the date of entry into force of the court decision (clause 1 of Article 346.17 of the Tax Code of the Russian Federation).

To be more precise, the obligation to pay court fees arises due to the filing of a claim. Accordingly, such a state fee can be included in the expenses of the simplified tax system on the day the court issues a ruling to accept the application for proceedings.

It also happens that at first the simplifier attributed the state duty to the expenses of the simplified tax system, which he paid under a civil law agreement. However, a court decision was subsequently issued, which, among other things, returned the paid state duty to him. What should I do? It must be included in income. Letters of the Ministry of Finance of Russia dated March 20, 2014 No. 03-11-11/12250 and dated May 17, 2013 No. 03-11-06/2/17357 insist on this. Moreover, on the date of actual receipt of money from the other (losing) party.

Also see “Bank services under the simplified tax system “income minus expenses”.

Read also

17.04.2017

How to take into account the cost of state duty for income tax purposes and under the simplified tax system

Tax accounting of state duty depends on its type.

The state duty for registering rights to real estate and for registering cars both under the OSN and under the simplified tax system is taken into account depending on when it is paid:

- if before the facility is put into operation, it is included in the initial cost of the operating system;

- if after putting the facility into operation, it is taken into account in expenses at a time.

The state fee paid by an organization when filing an application, statement of claim, complaint (appeal, cassation or supervisory) in court (arbitration or general jurisdiction), both under the OSN and under the simplified tax system, is taken into account in expenses.

The state fee, which the court decides to reimburse the defendant, is taken into account:

1) the defendant has expenses:

- in case of OSN - on the date of entry into force of the court decision;

- under the simplified tax system - on the date of payment;

2) the plaintiff’s income:

- in case of OSN - on the date of entry into force of the court decision;

- under the simplified tax system - on the date of receipt of money.

In other cases, both under the OSN and under the simplified tax system, the state duty is taken into account in expenses on the payment date, which always coincides with the accrual date.

This also applies to state fees for state registration:

- changes made to the organization's charter (Unified State Register of Legal Entities);

- real estate lease agreement concluded for a period of at least one year;

- rights to land plots.

Accounting for fixed assets under the simplified tax system for income and under the simplified tax system for income minus expenses - Kontur.Accounting

When purchasing fixed assets for a business, their cost must be properly taken into account in expenses. This is important for the correct formation of the tax base. The procedure for tax accounting of these amounts depends on the moment of purchase of the property, its value and service life. We will tell you about the rules for writing off expenses for the purchase of fixed assets in a simplified manner.

What are fixed assets?

Tax accounting of fixed assets is relevant for individual entrepreneurs and organizations using the simplified tax system with the object of taxation “Income minus expenses.” The purchase of property reduces the tax base under the simplified tax system of 15%, so it is important to correctly take into account the costs of fixed assets in expenses, and there is a certain procedure for this.

Fixed assets are assets that were purchased not for subsequent sale for profit, but for conducting business activities.

In 2021, the cost of a fixed asset must be more than 100,000 rubles for tax accounting purposes and more than 40,000 rubles for accounting purposes, and the period of use must be more than a year (Article 256 of the Tax Code of the Russian Federation).

The main purpose of a fixed asset is to generate economic profit. The criterion of 100,000 rubles applies only to property that has been in operation since 2021.

Property worth less than 40,000 rubles with a useful life of more than a year is considered a material expense and can be immediately written off as an expense. Property valued between 40,000 and 100,000 is considered material and does not need to be depreciated and must be expensed either straight-line over its useful life or all at once.

The Ministry of Finance believes that material expenses should be written off uniformly, that is, materials worth up to 100,000 rubles are either written off all at once, or all gradually. But if the fixed asset was purchased and put into operation under the simplified tax system before 2016, when the price limit of 40,000 rubles was in effect, then write-off of expenses must continue according to the usual scheme.

We explain this circuit below.

As a rule, fixed assets include buildings and structures for various purposes, environmental management facilities and land plots.

At the same time, land plots are considered a fixed asset, even if their value is below 100,000 rubles, since land is a non-consumable asset.

Fixed assets may include working machines, measuring, computing and regulatory equipment, transport, tools, and intellectual property. Even a capital investment in a leased property can be considered a fixed asset.

Accounting for fixed assets in expenses

Like all expenses that can be recognized as expenses, the amount for the acquisition of a fixed asset must be paid in full, the expenditure must be documented and, if necessary, ownership of the fixed asset must be registered.

Fixed assets are registered at their original cost, which includes:

- The purchase amount under the contract, including VAT, delivery and setup costs.

- Customs duties and government duties.

- Payment for the services of a consultant, lawyer, intermediary, which were necessary when purchasing a fixed asset.

Fixed assets are accepted for accounting in section 2 of the Accounting Book. Calculations must be carried out separately for each object. Due to the fact that the service life of different funds may vary, in this case the write-off procedure will be different.

Information on objects is reflected for each quarter, as of the last date of the period. After this, the final data from the last line in table 2 of section must be transferred to section 1 of KUDiR, also on the last day of the quarter, in column 5: “Expenses taken into account when calculating the tax base.”

If the fixed asset was purchased under the simplified tax system

If you purchased a fixed asset while on a simplified basis, then you can write it off completely before the end of the year. The Ministry of Finance recommends writing off the cost of purchasing an OS evenly.

A fixed asset begins to be expensed in the quarter when it has been fully paid for, documented, and began to be used in business. In this case, you need to write off its cost every quarter until the end of the calendar year.

For example, a fixed asset was purchased and put into operation in November, and its entire cost will be expensed on December 31.

If a fixed asset is purchased in installments, then expenses are written off based on the funds actually paid. It is allowed to wait until the fixed asset is paid in full and write off expenses after that.

If the fixed asset was purchased before the transition to the simplified tax system

The write-off period for a fixed asset that was purchased before the transition to the simplified system depends on its service life: up to 3 years, from 3 to 15, or more than 15 years. The period is determined according to the Classification established by Government Decree No. 1 of January 1, 2002. In this case, the residual value of the fixed asset, which is relevant at the beginning of the application of the simplified tax system, is taken into account.

Further, if VAT was deducted on a fixed asset, then it must be restored and paid. Residual VAT is calculated in proportion to the residual value of the fixed asset in the last quarter before the transition and is taken into account as part of other expenses. Calculation using the formula:

Recovered VAT = VAT deductible × Residual value of fixed assets / Initial cost of fixed assets

This amount will not be taken into account in the initial cost of the fixed asset.

Further write-off of expenses depends on the useful life of the fixed asset.

- If the useful life is less than 3 years, expenses are written off during the first year of application of the simplification in equal shares.

- If the useful life is from 3 to 15 years, then in the first year of application of the simplified tax system 50% of the cost is written off, in the second - 30%, in the third - 20%.

- If the useful life is more than 15 years, the cost is written off over 10 years in equal shares (Article 346.16 of the Tax Code of the Russian Federation).

Recalculation of the tax base when selling the simplified tax system

An enterprise can not only acquire, but also sell fixed assets. If you sell the OS after the period it is supposed to last (3, 10 or 15 years), then you do not need to adjust the costs. Therefore, there is benefit in selling the property after the service life specified by the Classification.

If the product has served you for less than 3, 10 or 15 years, you will have to recalculate the tax base. The recalculation is done as follows. Determine the amount of depreciation charges (the algorithm is prescribed in Article 259 of the Tax Code of the Russian Federation).

The amount must be determined for the years when you took into account the cost of the fixed asset in the expenses for the simplified tax system.

If depreciation turns out to be less than the amounts that you took into account in expenses, the company will need to pay arrears, penalties and submit updated declarations for previous years.

There are no special sections in the Accounting Book where the recalculation of the tax base could be reflected, so the company draws up a certificate of recalculation in free form. In KUDiR in section 2 you need to indicate what date the fixed asset was sold and reflect the amount of depreciation charges relating to this year - for the month in which the property was sold.

Fixed assets under the simplified tax system are difficult to account for without an accounting program or web service that automates calculations. Circuit.

Accounting is a simple and convenient service for maintaining accounting, calculating salaries and sending reports for individual entrepreneurs and organizations on the simplified tax system, OSNO, UTII.

Use the service for free during the first month of operation, do your accounting with us and get rid of the routine!

Try for free

Companies and individual entrepreneurs do not always work under the same tax regime for many years; sometimes it has to be changed. In this article we will tell you what are the reasons for changing the taxation system (TSS), how and in what time frame to change the tax regime.

KUDiR is a book of income and expenses, a mandatory tax document for all organizations and entrepreneurs using the simplified tax system. We'll tell you how to maintain KUDir for the simplified tax system of 6% in 2021.

Combining tax regimes helps optimize the company's operations and save on taxes. Does the law allow combining the simplified tax system and the OSNO? This is discussed in the article.

Source: https://www.B-Kontur.ru/enquiry/334

Reimbursement of legal expenses is included in the expenses according to the standard

This norm mentions only taxes and fees paid in accordance with tax legislation. So is the state duty an expense under the simplified tax system? Definitely - YES! Since 2013, organizations using the simplified tax system are required to keep accounting records in full. You will have to forget about keeping tax records on your own.

The point here is this. The services provided by a notary can be divided into actions that must be notarized without fail, and those that do not require mandatory notarization. According to the first, both public and private notaries charge state fees at rates in accordance with Article 333.

However, a court decision was subsequently issued, which, among other things, returned the paid state duty to him. What should I do? It must be included in income.

Let's try to figure out in what cases it is necessary to include returned amounts in income and in what cases not. What refundable amounts are not income Organizations and individual entrepreneurs using the simplified tax system when calculating tax take into account income from sales and non-operating income. 1 tbsp. 346.15, articles 249, 250 of the Tax Code of the Russian Federation.

Mainly, this paragraph requires the economic justification of the costs incurred in order to include them in the base for reducing the simplified tax system tax.

Therefore, the inspectorate and the courts do not have legal grounds to recognize the costs incurred by the company for legal services as not economically justified due to the fact that its structure has a legal service that performs similar functions.

When paying a fee after putting this property into operation, the provisions of paragraph 2 of Article 346.17 of the Tax Code of the Russian Federation come into force, according to which the state duty should be included in one-time costs under the simplified tax system.

According to the current tax legislation, it really turns out that the tax base must be increased by the amount of state duty reimbursement, since when applying the simplified tax system, a single tax is imposed on all income received by the organization (both from the sale of goods and services it produces, and from other sources).

Also, having chosen the income minus expenses system, the payer of the simplified tax system in 2019 is obliged to keep a book of income and expenses and take into account in it all income received and expenses incurred during the year. Based on these records, the final amount of tax that an entrepreneur or organization must pay is determined.

For profit tax purposes, the amount of state duty paid when filing a claim in court is taken into account at a time......

The list of expenses under the simplified tax system in 2021 has certain criteria, which are specified in Article 346.16 of the Tax Code of the Russian Federation. What expenses are the principle of the simplified tax system “Income minus expenses”? What are the expenses? Where can I find a complete list of simplified taxation system expenses for 2019? You will learn all this below in our article.

Please note that if the state duty is reimbursed to a legal entity by court decision, the amount must be included in the company’s income. This opinion is shared by the Ministry of Finance of the Russian Federation in its letter dated May 17, 2013 No. 03-11-06/2/17357. If the fee is paid when registering a vehicle or during the registration procedure for real estate acquired by a company, then the state duty increases the amount of the cost of property subject to depreciation, and therefore reduces the tax base in accordance with the provisions of paragraph 3 of Article 346.16 of the Tax Code of the Russian Federation.

The above rules also apply to the amount of compensation for legal costs by the defendant (subclause 31, clause 1, article 346.16 of the Tax Code of the Russian Federation).

As follows from the meaning of sub. 22 clause 1 art. 346.16 of the Tax Code of the Russian Federation, state duty is accepted as expenses under the simplified tax system in any amount upon its transfer to the treasury to the appropriate account.

During 2014-2015, the individual entrepreneur (USN D-R) included the amount of capitalization income (excess goods in the warehouse) in income for the NOB. For shipped capitalization (surplus), buyers paid individual entrepreneurs. And the individual entrepreneur re-included the capitalization (surplus) in......

This also applies to state fees for state registration:

- changes made to the organization's charter (Unified State Register of Legal Entities);

- real estate lease agreement concluded for a period of at least one year;

- rights to land plots.

So, there is the Tax Code, explanations from the Ministry of Finance, comments from lawyers and financiers, and entrepreneurs again and again make the same mistake in this situation. The result is fines for errors in accounting and for underestimating the tax base.

Are state duties included in expenses during simplification?

The list of costs taken into account when determining the single tax during simplification is indicated in Art. 346.16 Tax Code of the Russian Federation. According to sub. 31 clause 1 of the above-mentioned article, the state duty under the simplified tax system, income minus expenses, reduces the tax base. But according to paragraph 2 of Art. 346.16 of the Tax Code of the Russian Federation, costs must meet the requirements of paragraph 1 of Art. 252 of the Code.

First of all, this paragraph mentions the economic feasibility of expenses. This means that as a result of paying the state duty, some significant result must be obtained. Otherwise, the fee paid cannot be considered an expense.

This applies, for example, to situations where, when submitting an application to make changes to the Unified State Register of Legal Entities, the registration action was refused due to an error made by an employee of the enterprise when filling out the form. In this situation, the paid state fee is not returned to the legal entity, but cannot be accepted as expenses.

IMPORTANT! In case of reimbursement of state duty to an enterprise by a court decision, the amount received must be included in income. This is how the Ministry of Finance of the Russian Federation interprets the norms of the code in letters dated 02/20/2012 No. 03-11-06/2/29, dated 05/17/2013 No. 03-11-06/2/17357.

Read about what expenses are accepted for accounting under the simplified tax system.

As part of what costs during simplification is the state duty taken into account?

How the state duty is accepted as an expense under the simplified tax system depends on the action for which the duty was paid. If the state fee is paid for filing a lawsuit, registering changes in the Unified State Register of Legal Entities, issuing duplicate documents or other similar actions, then such a fee is included in the costs for determining the simplified tax according to the norms of subsection. 22 clause 1 art. 346.16 Tax Code of the Russian Federation.

Check out this publication for a list of tax deductible expenses.

But if the state duty is paid to register a vehicle or register real estate, then such a fee will increase the amount of depreciable property and will reduce the tax base in accordance with the procedure described in paragraph 3 of Art. Code 346.16. But this applies only to those fees that were paid before the depreciable property was put into operation. If the fee is paid after, then the state duty is included in the expenses under the simplified tax system at a time in accordance with clause 2 of Art. 346.17 Tax Code of the Russian Federation.