More and more businesses and individuals are choosing a virtual form of payment. The fact is that it is not a low-cost option and is produced much faster, regardless of time and days of the week. Payment by bank transfer is very convenient and practically not limited by regulatory documents. Therefore, it is gradually replacing conventional cash payments. More detailed information is provided below.

What is non-cash?

A form of non-cash payment is the movement of funds through the accounts of clients of banking or credit organizations in electronic form. Any payment for goods by bank transfer is carried out only through specialized organizations that have licenses to perform banking operations.

Bank transfer is available to absolutely all persons, regardless of the form of their activity. As a rule, at the end of the working day, account holders are provided with a statement of their cash flow activity for the day, which allows them to control all transactions. But if necessary, such a statement can be requested from a credit institution at any time.

Cashless payments and payments

The very first non-cash settlements and payments were settlements and payments using checks and bills. Afterwards, clearing houses were introduced - organizations that carry out transactions between different banks. Then, in most developed countries, giro payments spread as a subtype of non-cash payments (through giro banks, commercial banks, savings banks).

Non-cash payment transactions are the main type of banking operations. There are collection, transfer, and letter of credit operations.

Non-cash payments and payments are regulated by law. In Russia, this is the Civil Code of the Russian Federation (from Article 861 to Article 885), the Federal Law “On the Central Bank of the Russian Federation”. The federal law “On Banks and Banking Activities” and other regulations also apply.

Regulation of non-cash payments

Payment by bank transfer is subject to only three regulatory documents that fully control their implementation. The main one is the Civil Code of the Russian Federation, Chapter 46 of which describes all the basic requirements for permitted non-cash forms of money circulation.

Further, the bank transfer obeys:

- regulations on the issue of payment cards;

- Regulations on the rules for making money transfers.

The first document was approved by the Central Bank on December 24, 2004 and reveals the procedure for the legal implementation of acquiring. This concept defines the non-cash payment for services or goods that is familiar to many ordinary citizens.

The second document was approved only on June 19, 2012 by the Bank of Russia and contains all the necessary detailed descriptions of possible forms of non-cash payments and requirements for them. Everything contained in the provision fully complies with the norms of the Civil Code.

Any payment by bank transfer must be carried out in strict compliance with all of the listed regulatory documents, but such control is not an obstacle to the growing popularity of non-cash money circulation among the entire population.

Principles of organization

The presented payment method is one of the important tools for the development of the country's market economy. It is voluntary in nature, allowing you to transfer and receive wages, savings from deposits and other income without visiting financial institutions. Continuity of money transfers is ensured by the principles on which the organization of non-cash payments is based:

- Enterprises and organizations participating in operations themselves choose their form, regardless of the scope of their activities.

- The client's rights to manage funds are not limited.

- Transactions are implemented on a first-come, first-served basis.

- Payments are transferred from account to account if funds are available.

- Makeup for brown eyes with drooping eyelids step by step with photos

- How to stop nosebleeds

- Delicious eggplant snacks in adjika for the winter without sterilization

Advantages of non-cash payments

First of all, payment by bank transfer requires minimal documents in comparison with regular cash payments between organizations. Many companies choose this form of payment because it makes it possible to avoid large fines due to errors in registering cash discipline and using cash registers.

Large organizations are also increasingly invoicing their clients by bank transfer, instead of taking cash from them. This allows companies to save significantly, since servicing such operations is much cheaper.

The obvious benefit of such calculations for ordinary citizens is the convenience of transactions. The fact is that you can carry them out simply by having a payment bank card and the ability to access the Internet, and commissions for money transfers between accounts are not always charged or amount to minimal losses.

Such virtual settlements also have benefits for the state, because it allows you to constantly monitor all cash flows in real time. In addition, a decrease in the turnover of the living money supply reduces the possibility of inflation in the country.

In general, the advantages of non-cash payments are clearly visible to everyone, and most importantly, they can be carried out at any time of the day, on any day of the week and completely regardless of the geography of the transfer.

What is cashless payment

The presented payment format is implemented by money transfers through bank accounts without the use of paper currency and coins. It can be used by legal entities, individuals and entrepreneurs. The concept of non-cash payments implies the use of payment cards, bills and checks to carry out transactions. The transfer of payments occurs between the parties to the property relationship or with the help of an additional entity represented by a credit institution.

Essence

Organizing financial transactions using this type of payment is beneficial to banks and the state, because allows you to avoid a sharp increase in treatment delays. The essence of non-cash payments is the implementation of payments by transferring currency to accounts intended to replace cash. By using a non-cash form of payment at an enterprise, you can get rid of cash registers and comply with the rules for their use.

Advantages and disadvantages

The main advantage of this payment method is its flexibility. Non-cash money can be stored in special accounts for an unlimited time. Bank documents can be connected to the transaction at any time. They establish and confirm the fact of the transaction. Enterprises that use non-cash payments are freed from the need to constantly transfer money to the bank.

The main disadvantage of the method is its dependence on the bank. A non-cash transfer cannot be carried out if the holder of the funds has problems with their turnover. Owners of regular and special accounts will have to pay the bank a commission for transactions performed. The pros and cons of non-cash payments compensate each other, making this payment method the most convenient in the realities of our time.

Types of bank transfer payments for individuals

Ordinary citizens may think that bank transfers are only transfers between accounts, but in fact there are 6 types of them. Most are available only to legal entities and organizations and are controlled by the same regulatory documents.

The most common form of payment available to civilians is in the form of an electronic transfer. It represents the transfer of funds from the payer’s personal bank account to the recipient’s account through a banking operator. The recipient can be an individual or an organization, the main thing is that such a right is described in the agreement between the account holder and the bank. The payer can only be a private person.

Another form of payment, which, like the previous one, is regulated by the law “On the National Payment System” is direct debit. It represents the debiting of funds from the owner’s account at the request of the recipient, but only if this is permitted by the agreement between the account owner and the credit institution. Most often, such payments are mandatory fees for servicing a bank card or account.

Rules for non-cash payments

Financial law regulates all monetary transactions between entrepreneurs, individuals and legal entities, shops, and other institutions. For these purposes, rules for non-cash payments were developed, the main one of which states that money should be debited from the client’s account only by his order. Payment documents used for transactions must contain:

- TIN of the account owner;

- name and account number of the credit institution;

- name of the payer's bank;

- account number and BIC of the transfer recipient.

Payment by bank transfer

Money transfer is carried out using one of the methods listed above. The correspondent account reflects the details of the sender and recipient of the funds, the amount of the transfer and the name of the paid service or product. Therefore, if the seller does not fulfill his obligations, the non-cash payment will be returned to the buyer with the exception of the banking system commission.

Refund to buyer

The customer has the right to return or replace goods purchased in the store. Refunds to the buyer by bank transfer are carried out upon presentation of the product, receipt, warranty card, and identity documents. Scans of the listed documents must be sent to the store’s mail. The transfer of funds to a client may be refused in the following situations:

- the product is a food product and is of good quality;

- documents on the transfer of funds are lost;

- the purchase belongs to the list of non-replaceable products.

Purchase returns

Products of inadequate quality must be sent by the client to the store warehouse. The return of goods by bank transfer is stipulated in the contract of each enterprise separately. The company can compensate for the costs of sending the goods if such a clause is included in its rules. Non-cash forms of payment involve the transfer of money to the buyer's current account immediately after sending the products back to the seller.

Most common form

Individual entrepreneurs pay by bank transfer most often by means of a payment order. Even individuals who do not have a current account with a credit institution can use this form. Payment involves the preparation and transfer to the bank of a certain document - an order, detailing the amount, recipient and time frame within which the transfer must be made. All this is carried out at the expense of the payer.

The validity period of the order is officially 10 days, not taking into account the moment of submission of the document, but in practice everything happens much faster. Only incorrect execution of the order can slow down the receipt of funds.

The most secure form

The most secure form of non-cash payment is payment through a letter of credit. It represents an inconvenience for the payer, since it requires a separate opening of a letter of credit, even if this bank already has a current account, but all this is for the sake of security.

The payer must transfer a certain amount for goods or services to an open account and oblige the bank to pay them to the recipient only if certain conditions are met. That is, until the recipient gives the credit institution confirmation that he has fully fulfilled his obligations under the transaction, he will not receive the money. In this case, the bank acts as an uninterested third party and guarantees the legality of the transaction.

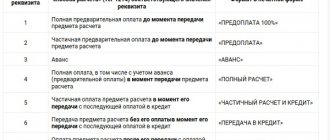

Types of non-cash payments

Payments of this type are classified according to various criteria. Depending on the economic nature, remittances are needed to pay for non-commodity transactions and to purchase goods or services. Payments can be intra-republican and interstate. Funds transferred within the state are divided depending on the region and locality. The following types of non-cash payments are also distinguished:

- guaranteed, in which the collateral is the funds reserved in the budget account;

- non-guaranteed;

- transfers with instant debiting of funds from the account;

- payments with deferred transfer of money.

Cash-non-cash payment

Conventionally, cash/non-cash payment determines settlements through checkbooks, since after debiting funds from the drawer’s account, it may imply issuing them in cash or transferring them to a bank account. This form of payment is more common in Europe and the USA and is carried out only after confirming the identity of the bearer of the check and receiving information about the presence of an amount sufficient for the transfer in the drawer’s account, and, of course, after confirming the authenticity of the check.

Another form of non-cash payment is a transfer through collection or collection order. It is carried out only when the recipient of the funds provides the bank with confirmation of the account owner’s monetary obligations to it. In essence, this is debt collection and it occurs even without timely notification to the account owner. As a rule, the debtor learns about the withdrawal after the transfer has been made.

Forms of non-cash payments

The characteristics, structure, and meaning of payment transactions are determined by their type. Depending on the variety, they can be used by enterprises and individuals. In the Russian financial system, the following forms of non-cash payments are distinguished:

- transfers using payment requests and orders;

- letter of credit payments;

- payments through check books;

- collection settlements;

- payments by electronic money transfer;

- money transfers by direct debit.

What is non-cash based on?

First of all, all non-cash payments must be carried out in accordance with laws and regulations. In addition to the general rules, each credit institution is obliged to act only within the framework of a valid agreement between the bank and the account owner. Going beyond the scope of the document is allowed only when signing a new agreement. In addition, the bank does not have the right to influence the choice of payment form for the participants in the transaction.

Any invoice issued for payment by bank transfer, a sample of which can be obtained directly from a credit institution, must be supported by a sufficient amount of funds in the payer’s account. In addition, money transfer operations must be carried out within a specified period, otherwise sanctions or fines may be imposed on the culprit. And, of course, every account owner has the right of acceptance, which means that even the state is prohibited from debiting money from the account without prior notification.

Implementation principles

Compliance by business firms and banks with established rules ensures that this type of payment meets modern requirements such as reliability, efficiency, and speed of transactions. For this purpose, principles for implementing wire transfers were developed. The procedure for making non-cash payments is determined by the following principles:

- The principle of acceptance. Without obtaining the consent or notification of the cash account holder, funds cannot be debited. This rule even applies to requests from government agencies.

- The principle of freedom of choice. Payment participants can conduct transactions in any form convenient for them. Financial organizations cannot influence the choice of non-cash payment methods.

- The principle of legality. All operations must be carried out within the framework of current legislation and regulated by it.

- The principle of urgency of payment. Any transfer of funds must be carried out within the time frame established by the payer. If they were violated, then sanctions fall on the bank.

These principles not only lie in making payments without withdrawing currency, but also in their implementation. The payer's current account must always have the required amount of funds to carry out transactions. All transactions are always carried out on the basis of an agreement between the bank and the account holder. You can go beyond the scope of the agreement only if a new contract is concluded with the client.

Types of accounts

Any non-cash payment is permissible only if you have a bank account with the required amount on it. The only exception is payment by means of a payment order, which is permitted by law and can be carried out even in the absence of a bank account, but only by individuals. To conduct business, you must have a bank account.

There are several varieties of them:

- Current account. Available for use by ordinary citizens and has no relation to business activities.

- Deposit. Allows individuals and organizations to receive income from their own funds.

- Checking account. Opens for commercial activities of citizens, entrepreneurs or organizations, except for credit.

- Budget. Used only by legal entities for the distribution of budget funds.

- Special accounts. These include clearing, collateral, letters of credit and other accounts. They can open to everyone.

- Correspondents. Available only to credit institutions.

Funds control

For individuals, keeping track of the movement of funds in an account allows them to keep bank statements, but for organizations it is more and more difficult. They use books of income and expenses, in which they record data on payment orders, collection transactions, memorial orders, and so on. Analytics of special accounts is carried out using statements of letters of credit, deposits, check transactions and other forms of payments.

The bank should tell you in detail how to issue an invoice for payment by bank transfer to the account holder, as well as inform about possible fines. They are imposed both on the credit institutions themselves and on paying agents if they fail to fulfill their obligations on time.

How to choose a bank

Criteria for selecting an acquiring bank:

- the amount of commission for using the service;

- timing of crediting funds to the account;

- duration of terminal replacement in case of breakdown;

- the presence of special conditions (the possibility of reducing the percentage when a certain amount is reached, reducing tariffs when paying with a card issued by the acquiring bank, etc.).

In most cases, the quality of the services provided depends on the size of the commission, so the pursuit of a low rate is not always justified.