Registration of funds disbursement for reporting

In order to release money to the account, either an order from the manager or an application from the employee certified by the manager must be issued.

Sample order from a manager for reporting

Sample application for reporting

The basis for issuing money must indicate:

- FULL NAME. and the position of the employee to whom the money is given.

- Purpose of issuance.

- Amount.

- The period for which funds are issued.

Based on the specified document, the accountant will either issue cash from the cash register or transfer it to the employee’s card.

Example

Let's look at how settlements with accountable persons are displayed in NU and BU.

From the cash desk of the enterprise on April 25, 2016, a sum of funds was provided to the office manager of the conditional LLC in the amount of 2,000 rubles for a period of 4 days for the purchase of office supplies. On the same day, the accountant issued the accountable amounts based on an application signed by the manager: DT71 KT50 - 2000 rubles.

On 04/27/16, the office manager purchased office supplies worth 1000 rubles, filled out an advance report, provided checks to the accounting department and returned the rest of the amount to the cashier. The accountant prepares the following records:

DT50 KT71 — 1000 rub. – the balance of funds has been deposited into the cash register.

DT10 KT 71 – 1000 rub. – stationery items are taken into account.

How to report for accountable money

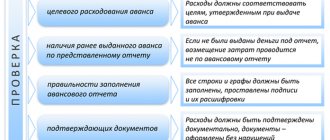

After the day before which the report was issued, the employee must either report on the expenditure of money or return the unspent amounts. The employee must submit an advance report to the accounting department after the deadline for issuing money on account, no later than three working days. If the return date occurred during the employee’s absence (vacation or business trip), then the report must be submitted within three days after returning to work.

The company can approve the advance report form independently, providing it with all the mandatory details named in Article 9 of Law 402-FZ, or you can use the form approved by the State Statistics Committee in Resolution No. 55 dated 01.08.2001.

Advance report form

Along with the advance report, the employee must provide documents confirming the expenses incurred.

Features of returning money to the cash desk by an accountable person

Organizations (IP) can issue funds on account in two ways:

- transfer to an employee’s account or corporate card (letter of the Ministry of Finance of the Russian Federation dated October 5, 2012 No. 14-03-03/728);

- issuing cash (directive of the Bank of Russia “On the procedure for conducting cash transactions...” dated March 11, 2014 No. 3210-U).

If an employee has not used all the accountable money issued to him, he must return it within the time period established for this by the employer (clause 6.3 of instruction No. 3210-U).

The amount of the refunded amount is determined based on the results of verification and approval of the advance report on the amounts spent. Such a report must be drawn up no later than the number of working days approved by the organization from the expiration date for which the money was issued (clause 6.3 of instruction No. 3210-U).

ATTENTION! From November 30, 2020, the requirement to submit a report within 3 working days has been canceled.

From November 30, 2020, other changes to reporting and cash register came into effect. ConsultantPlus experts spoke in more detail about the innovations. Get trial access to the K+ system and go to the review material for free.

The issuance period is fixed in the application drawn up by the employee for the issuance of an advance, or in the employer’s administrative document on the issuance of money on account. From 08/19/2017 (instruction of the Bank of Russia dated 06/19/2017 No. 4416-U), the completion of an application by an employee is no longer a mandatory condition for the payment of accountable amounts. It can be carried out on the basis of an administrative document of the head of the legal entity (or individual entrepreneur).

You will find an example of such a document in ConsultantPlus. Trial access to the legal system is free.

IMPORTANT! Directive No. 3210-U applies its rules only to the rules for issuing and returning funds in cash. For non-cash payments for accountable amounts, its provisions do not apply, and an employer using this method must approve the procedure for settlements with accountables by an internal document.

How to recover accountable funds from the director

There is often a situation where the head of a company does not report in a timely manner for the amounts taken into account.

Unreturned accountable money, from the point of view of tax authorities, must be classified as employee income and personal income tax must be calculated from it (clause 8 of the Federal Tax Service Letter No. SA-4-7/23263 dated December 24, 2013).

With the consent of the employee, unreturned money may be collected from his salary. One month is allotted for this from the expiration date for which the report was issued (Article 137 of the Labor Code of the Russian Federation). If the employee does not agree with the withholding, or the collection period has expired, the disputed amounts can be recovered through the court. This must be done within the usual limitation period established by Article 196 of the Civil Code of the Russian Federation, that is, three years.

We are changing the regulations on conducting cash transactions

Enterprises should update the regulation on working with imprest amounts to take into account the latest changes since November 30, 2020.

Employees have the right to receive accountable funds in cash at the enterprise's cash desk. It is also allowed for the company to issue money to a bank card, including to the employee’s salary card (instruction No. 3073-U, letter of the Ministry of Finance No. 03-11-11/42288 dated July 25, 2014). To make this possible, the procedure for settlements with reporting employees should be recorded in the company's accounting policies.

Money is issued through the cash desk in accordance with the following requirements:

- When preparing cash documents, the accountant must be guided by the provisions of instructions No. 3210-U.

- Money is issued to an accountable person on the basis of an order (or other administrative document) or upon his written application. As stated in the letter of the Central Bank of the Russian Federation No. 29-1-1-OE/2064 dated 09/06/2017, the order is signed by the director, the date and registration number are indicated in the order.

- The period for which money can be issued for accountability is established in the administrative document for its issuance. The reporting period is established by the management in the reporting provisions. During this time, the accountable is obliged to report or return the money to the organization.

- The issuance of money for reporting from the cash register is formalized by an expenditure order, the return of the balances of accountable amounts is formalized by receipt orders. It is also possible to issue money for reporting by transferring it to the applicant’s bank card (letter of the Ministry of Finance No. 03-11-11/42288 dated 08/25/2014). It is allowed to return the money to the accountable by transferring funds to the company's current account. The possibility of non-cash accountable payments is fixed in the accounting policy.

- There is no limit on the amounts that can be reported. The enterprise has the right to issue money to the accountable person in any amount. The settlement limit (RUB 100,000 per agreement) must be taken into account only when making payments between enterprises. In this regard, there have been no changes for accountable persons.

- Issuing money on account to a person who has a debt is permissible by order of management.

- Organizations and individual entrepreneurs have the right to issue money not only to those employees who work on the basis of a permanent employment contract, but also to those who are in civil legal relations with the enterprise (letter of the Central Bank of the Russian Federation No. 29-1-1-6/7859 dated 10/02/2014 ).

- The issuance of cash is formalized by posting Dt 71 Kt 50, and when transferring funds to a card - by posting Dt 71 Kt 51.

Accounting of imprest amounts

In accordance with the Chart of Accounts, accounting of settlements with accountants is kept on account 71. The debit of the account reflects the employee's debt for funds received.

When the report is approved, the accountable amounts are written off from the credit of account 71 to the debit of the corresponding accounting accounts. Accounting entries

| Contents of operation | Debit | Credit |

| A report was issued to the employee | 71 | 50, 51 |

| Advance report submitted | 10, 20, 25, 26, 44, 60, 76, 91 | 71 |

| Return of unspent accountable amounts | 50, 51 | 71 |

Return of accountable amounts to the current account, postings

Receipt of funds to the organization's current accounts in accounting is documented by the following transactions:

Dt 51 Kt 71 - unused accountable funds were received into the organization’s bank account.

Dt 52 Kt 71 - unused accountable funds were received in the foreign currency account of the organization’s company.

Dt 73 Kt 51, 52 - the amount of the bank commission for the transfer was returned to the employee.

Dt 91 Kt 73 - bank commission is recognized as an expense.

The last two entries are recorded in accounting if the local act of the enterprise stipulates the possibility of compensating the bank’s commission.

Basic provisions

Accountable amounts include expenses:

- business trips;

- for the economic needs of the institution;

- representative.

The main regulatory document regulating mutual settlements with accountable persons is Directive of the Central Bank of Russia No. 3210-U dated March 11, 2014. Accountable money is issued only to employees of the organization with whom employment or civil law contracts have been concluded. Due to the introduction of online cash registers, we were worried that we would use other documents to report on those accountable. But nothing fundamentally has changed.

IMPORTANT!

Until August 19, 2017, there was a ban on debtor employees, that is, employees who were in debt were prohibited from giving money on account. The changes approved by the new Directives No. 4416-U dated August 19, 2017 canceled the ban.

What else do you need to know about issuing money on account to an employee of an organization?

The organization has the right to allocate funds to both full-time employees and contractors. But with the latter, sometimes difficulties arise that are associated with the preparation of an advance report.

It happens that the contractor turns out to be dishonest and, taking advantage of the fact that he is not registered in the organization and funds cannot be withheld from him, simply refuses to fulfill his obligations to submit a cost report. This behavior creates many difficulties for accountants.

We advise issuing funds to such companies only after documents on financial responsibility have been signed with them. In addition, the contract can specify special conditions according to which, if the company does not report on the expenditure of funds on time, the contractor will be charged interest for each day of delay.

It is important to know how to register money correctly.

We recommend the following:

- when transferring funds to a card, the accounting employee must indicate the purpose of the funds (accountable);

- in the application it is necessary to indicate the form of issuing money (cash or transfer to a card);

- explain to the reporting employee all the rules, explain that he does not have the right to transfer funds to third parties;

- issue funds to the employee only after an application has been drawn up, otherwise management faces a fine of 50 thousand rubles;

- if the funds were spent in foreign currency, then they must be indicated in rubles in the report.

In the latter case, it is also important to provide paper that will confirm the exchange rate at the time of spending the money.

If the employee does not have such a document on hand, then conversion for reconciliation will be carried out at the current exchange rate of the Central Bank of the Russian Federation.

An employee can receive new funds only after confirming the intended use of the previous amount. If he has unpaid debts due to this fact, then the company does not have the right to transfer money to him, otherwise it will face a fine.

What should an accountant remember about money issued for reporting?

It is necessary to ask a person to report on expenses only when the employee has received the funds in advance. If it turns out that he spent his personal money, which the company subsequently compensated, then no report is required. All you need is a completed application for reimbursement of expenses, received receipts, invoice checks, and so on.

If the employee does not submit the necessary documents, then during the audit, tax officials will consider the accountable money as the citizen’s income. This means that personal income tax will be charged on them.

If not all funds have been spent, then the accountable employee can return them in any way that is convenient for him:

- cash through the cash register;

- transfer to the company account.

But it happens that some difficulties arise with the bank itself. Sometimes he may not accept cash if the company initially transferred it to your card.

How to choose an outsourced accountant?