Do I need to take it?

This report is sent to the Federal Tax Service by tax agents who paid income to individuals. This is not only wages, but also:

- dividends;

- material aid;

- rent under lease agreements with individuals;

- other taxable payments.

If there were no such payments, there is no need to submit 6-NDFL to the tax office. But if during the accounting year the company paid income and withheld income tax, it will have to report to the Federal Tax Service: the first section reflects the information on an accrual basis.

IMPORTANT!

The Tax Code of the Russian Federation and the letter of the Ministry of Finance No. BS-4-11 / [email protected] dated 08/01/2016 indicate whether it is necessary to submit 6-NDFL if there are no employees - no, the organization has the right not to report to the territorial inspection. If there are no employees, then there are no accruals and no basis for calculation.

6-NDFL for the 3rd quarter of 2021

6-ndfl_za_3_kvartal_2019.jpg

Related publications

In October, at the end of the 3rd quarter, tax agents will once again have to report on the personal income tax calculated and withheld from the income of individuals. The current form of Calculation 6-NDFL was approved by order of the Federal Tax Service of the Russian Federation dated October 14, 2015 No. ММВ-7-11/450 (as amended on January 17, 2018), for the 9 months of 2021 it is necessary to report on it.

In this article, we will tell you how to fill out the 6-NDFL for the 3rd quarter of 2021, what timeframe the calculation is due, and give an example.

Deadline for submitting 6-NDFL for the 3rd quarter of 2021

All current quarterly reports in Form 6-NDFL are submitted no later than the last day of the month following the reporting period. The annual calculation is submitted no later than April 1 of the following reporting year. If the deadline coincides with a non-working weekend or holiday, it is postponed to the next weekday.

For 6-NDFL for the 3rd quarter of 2021, the deadline will be October 31, 2019. This is a working day (Thursday), so this deadline will not be postponed.

For tax agents who have paid income to 25 individuals or more, only an electronic form for submitting the Calculation is provided. The rest can submit 6-NDFL on paper.

Violation of delivery deadlines may result in a fine of 1,000 rubles. (for each month of delay, including partial), and for failure to comply with the electronic form, when necessary, the fine is 200 rubles. (Article 119.1, 126 of the Tax Code of the Russian Federation).

Filling out 6-NDFL for the 3rd quarter of 2019

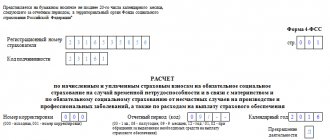

Instructions for filling out Calculation 6-NDFL are contained in the same Federal Tax Service order No. ММВ-7-11/450. The Calculation includes a title page and two sections, with:

“Section 1” includes generalized indicators of the amounts of accrued income and personal income tax, contributed incrementally from the beginning of the year;

“Section 2” reflects the indicators of only the last 3 months (i.e. data from the last quarter).

On the title page, in the “Submission period” field, the code “33” is indicated, which corresponds to nine months, “Tax period (year)” - 2019.

When filling out “Section 1” in 6-NDFL for the 3rd quarter, you need to take into account the following features:

Section 1 is drawn up for each tax rate separately, except for lines 060-090. For example, if the tax was withheld at rates of 13% (residents) and 30% (non-residents), you will have to fill out two Section 1. If there is more than one page in Section 1, the indicators of lines 060-090 (summed for all rates) are indicated only on the first of them .

The amount of income (line 020) includes, incl. and dividends paid, in addition they need to be highlighted in line 025. The “dividend” personal income tax is reflected in the same way (including in line 040, highlighted in line 045).

Line 050 – the amount of advance payments paid by foreign workers acquiring a patent for the right to work in the Russian Federation.

Line 080 includes only the tax that the agent did not withhold from “in-kind” income or material benefits, due to the lack of cash payments from which deduction could be made.

If the same person quit and was rehired during the reporting period, in line 060 he is counted as one individual.

“Section 2” of form 6-NDFL for the 3rd quarter (an example of completion is given below) is drawn up taking into account the provisions of Art. 223, 226 of the Tax Code of the Russian Federation, including:

“Date of actual receipt of income” (line 100) – indicates the last day of the month for which the salary was accrued. For financial assistance, vacation pay and sick leave, this date will be the day they are paid to the employee; for “in-kind” income – the day of their transfer; for business trips – the last day of the month of approval of the advance report; according to the financial benefit from saving on interest - the last day of each month of the loan term.

The “tax withholding date” on line 110 is the day on which the income was paid to the individual.

“Tax transfer deadline” in line 120 is indicated as the next day (working day) after the day of transfer of income to an individual; for vacation and sick leave – the last day of the month of payment to an individual.

The amount of income in line 130 is shown without reduction for tax deductions.

“The amount of withheld tax” in line 140 is reflected regardless of whether it was transferred to the budget or not.

6-NDFL for the 3rd quarter: example of filling

Let's look at how to fill out form 6-NDFL using an example.

During January-September 2021, 10 employees received income at Spectr LLC. Of these, three use the standard deduction for a child (1,400 rubles per month). In April, the company paid dividends to the founder in the amount of 40,000 rubles, and on July 1, one employee was paid vacation pay in the amount of 23,700 rubles. The applicable personal income tax rate is 13%. Salaries in the company are paid on the 5th. For convenience, we present all the calculated data in the table below.

What are the possible risks if you decide not to submit a zero report?

The calculation is submitted only if the company made payments to individuals subject to income tax. If there are no payments in any month of the accounting year, then zero personal income tax reports are not required to be submitted to the tax office.

But the tax authorities do not have information about whether the organization made payments to employees or not. The fact that there are no such payments and the company has not lawfully submitted a report must be notified to the Federal Tax Service. This can be done in simple written form by bringing the letter in person, sending it by mail or electronically.

If you do not do this, the tax authorities will decide that the taxpayer did not report unlawfully. In this case, the inspectorate will block the company's bank accounts.

To correctly report on personal income tax, use the instructions and samples from ConsultantPlus for free. Experts have discussed how to fill out the form in different situations.

Is it possible to send a blank report?

The calculation is filled in with a cumulative total from the beginning of the year. Before you find out from the Federal Tax Service whether you need to submit 6-NDFL with zero reporting, you need to check whether there have been payments previously. That is, if an organization paid taxable income in the 1st or 2nd quarter of 2021, then submit the calculations for the 1st quarter, and for six months, and for 9 months, and for the year. Such clarifications are given by the Federal Tax Service in letter No. BS-4-11/ [email protected] dated 03/23/16.

Instead of a letter to the Federal Tax Service about the absence of an obligation to submit calculations, the company has the right to submit zero reports 6-NDFL. In this case, the Federal Tax Service is obliged to accept it (letter of the Federal Tax Service No. BS-4-11 / [email protected] dated 05/04/16).

How to fill out zero 6-NDFL

Here's how to submit zero personal income tax reporting (filling out rules):

- On the title page indicate the name of the company and its details, the period for which the report is being filled out, and the Federal Tax Service code to which it is submitted.

- In all lines of sections 1 and 2 that provide total indicators, enter “0”.

If accruals were made during the year, the organization is required to submit a report for 9 months. The first section indicates cumulative indicators from the beginning of the year.

Submission form: paper or electronic. Institutions with 10 or fewer employees submit a report on paper. If there are more than 10 people on staff, then the organization submits the reporting form electronically (325-FZ dated September 29, 2019).

How to fill out 6‑NDFL in 2021 and when to submit it to the Federal Tax Service

The procedure for filling out is prescribed in the Order of the Federal Tax Service of the Russian Federation dated October 14, 2015 No. ММВ-7-11/ [email protected] The report does not cancel the annual form of the 2-NDFL certificate that is familiar to everyone. The main difference between the two forms is in the order in which the data is reflected: the 2-NDFL certificate is submitted separately for each individual to whom income was paid, and the 6-NDFL certificate is submitted for the organization as a whole.

Quarterly reporting reflects the total income paid to all individuals. The data in section 1 of form 6-NDFL is shown on an accrual basis from the beginning of the year. In section 2 - for the last 3 months.

Reporting must be submitted at the place of registration of the organization or individual entrepreneur. For each separate division, a separate 6-NDFL calculation is submitted at the place of its registration (letter of the Ministry of Finance of the Russian Federation dated November 19, 2015 No. 03-04-06/66970, letter of the Federal Tax Service of the Russian Federation dated December 28, 2015 No. BS-4-11 / [email protected] ) .

Small firms with up to 10 employees are allowed to submit 6-NDFL reports on paper.

If the number exceeds 10 people, you will have to report electronically. This norm applies from 01/01/2020 in accordance with the amendments made to the Tax Code by Federal Law dated 09/29/2019 No. 325-FZ.

The Kontur.Extern system will help you easily and quickly send reports via telecommunication channels.

Fill out and submit 6-NDFL reports online without errors. 3 months of Kontur.Externa for you for free!

Try it

Deadlines for submitting 6-NDFL

Form 6-NDFL must be submitted no later than the last day of the month following the reporting quarter. And the annual calculation is no later than March 1 of the year following the expired tax period (taking into account clause 2 of Article 230 of the Tax Code as amended by Federal Law No. 325-FZ of September 29, 2019).

Taking into account weekends and holidays in 2021, the following reporting deadlines are provided:

- For 2021 - no later than 03/02/2020

- for the first quarter of 2021 - until 04/30/2020;

- for the six months - until July 31, 2020;

- nine months - until 02.11.2020.

Procedure for filling out 6-NDFL

Below you will find brief instructions for filling out 6-NDFL.

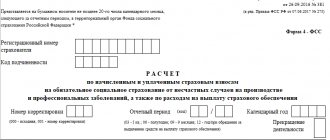

Form 6-NDFL contains a title page and two sections.

If the organization has separate divisions, the checkpoint and OKTMO of such divisions must be indicated on the title page. In any case, the TIN is assigned to the parent organization.

How to fill out Section 1 “Generalized indicators”

This section should show the amount of accrued income broken down by tax rate. The amount of accrued dividends is recorded on a separate line. Information about dividends is necessary for the Federal Tax Service to compare it with the figures reflected in the income tax return.

Section No. 1 of the 6-NDFL calculation can be placed on several pages if the organization uses different personal income tax rates.

How to fill out line 070 of form 6-NDFL

Accountants often ask about the procedure for filling out line 070 6-NDFL. We'll tell you what's included below.

Line 070 6-NDFL includes the total amount of tax withheld on an accrual basis from the beginning of the year. It is important that personal income tax is withheld. For example, in line 070 of the report for the first quarter of 2021, there is no need to reflect the tax on the March salary if it was paid in April (letters of the Federal Tax Service of Russia dated 08/01/2016 No. BS-4-11 / [email protected] , dated 07/01/2016 No. BS -4-11/ [email protected] ).

How to fill out Section 2 “Dates and amounts of income actually received and withheld personal income tax”

In the second section, you need to group income by date of receipt. For each group, you need to note the dates of tax withholding and transfer to the budget.

Since 2021, for some types of income, a new procedure has been in force for determining the date of their receipt by an individual (Article 223 of the Tax Code of the Russian Federation). Thus, income in the form of material benefits for using a loan must be determined on the last date of each month. If the employee used the loan during the first quarter, lines 100 and 130 must reflect the material benefit as of 01/31/2020, 02/29/2020 and 03/31/2020. Personal income tax on income is reflected in line 140.

Passing personal income tax to 6-personal income tax

There are situations when income is accrued in one quarter and paid out in the next. Calculation and deduction of personal income tax occur in different quarters. This situation is typical for March, June, September and December salaries.

If a company has a pass-through tax, it must be recorded in the withholding quarter. For vacation pay, bonuses and sick leave, a different scheme is provided - the tax is reflected in the period when the income is paid.

Updated calculation

Organizations and individual entrepreneurs must submit an updated calculation in form 6-NDFL if errors are found in the primary report or false information is provided.

The indication of the updated calculation is written on the title page in the “adjustment number” field (001, 002, 003, etc.).

Responsibility

The following types of penalties are provided for tax agents:

- Late submission of personal income tax reports threatens the taxpayer with a fine of 1,000 rubles. A fine is assessed for each full or partial month of delay in the report (clause 1.2 of Article 126 of the Tax Code of the Russian Federation);

- when submitting a personal income tax report 10 days after the deadline, the Federal Tax Service may block the bank account of an organization or individual entrepreneur (clause 3 of article 76 of the Tax Code of the Russian Federation);

- for false information in form 6-NDFL, the company will pay 500 rubles (Article 126.1 of the Tax Code of the Russian Federation);

- If the company violates the procedure for submitting a report in electronic form, it will be fined. The fine will be 200 rubles.