The simplified tax system Income option is especially popular among entrepreneurs without employees, because with small revenue the tax can be reduced completely, i.e. to zero. How to do this is shown in the examples below, but first read about the main features of the simplified tax system 2018.

The most important thing about the simplified tax system 2021

In the simplified system there are two objects of taxation:

- income, standard rate 6%

- income reduced by expenses, standard rate 15%

You can choose a taxable object only once a year, so you need to understand in advance what business expenses you may have. If you started working on the simplified tax system Income, where expenses are not taken into account, and then your costs increased sharply, then you will be able to switch to the simplified tax system Income minus expenses only from the new year.

The standard tax rates indicated above can be reduced by regional laws to 1% for the simplified tax system for Income and up to 5% for the simplified tax system for Income minus expenses. For example, in one of the regions there is a standard rate of 6% for the simplified tax system Income and only 5% for the simplified tax system Income minus expenses, but only for construction. As you can see, the second option is more profitable, even if the share of costs is small.

By establishing such preferential rates for certain types of activities, the authorities seek to develop some direction in their region, most often this is production or construction. Therefore, before choosing a simplified taxation object, study the regional law; it is possible that a preferential rate applies to your type of activity. You can find out these features at the Federal Tax Service or the economic department of the local administration.

The main limitation on the ability to apply the simplified system is related to the amount of income received during the year. Initially, this amount was 60 million rubles, but in the period from 2021 to 2021 another limit is in force - 150 million rubles.

Another important limitation is set for the number of employees - no more than 100 people. In principle, most individual entrepreneurs meet these conditions and therefore have the right to work under a simplified regime.

Tax deduction for the purchase of cash registers

Individual entrepreneurs who use the UTII or PSN taxation system can receive a tax deduction for the purchase of an online cash register entered in the cash register register (in accordance with Federal Law No. 349 of November 27, 2017).

The amount of the deduction is determined based on the amount of the following expenses:

- acquisition of equipment;

- purchase of a fiscal drive;

- software;

- related work (bringing the cash register in compliance with the requirements).

The deduction is no more than 18 thousand rubles for each unit of equipment. The law comes into force on January 1, 2021 and applies to cash registers that are registered from February 1, 2021 to July 1, 2021. In the case of entrepreneurs in the retail and catering sectors who have employees with an employment contract, the conditions are different. Such individual entrepreneurs can receive a deduction when registering a cash register in the period from February 1, 2021 to July 1, 2021.

How to pay tax on a simplified system

The tax that simplifiers pay is called single. Personal income tax and income tax are not paid under the simplified tax system. VAT, in addition to that which is paid when importing goods into the territory of the Russian Federation, is also not charged. The basic tax is calculated based on the results of the calendar year and entrepreneurs must pay it no later than April 30 of the following year. For example, the simplified tax system tax for 2021 must be paid no later than 04/30/2019.

However, during the year there are reporting periods, at the end of which part of the tax must be paid in advance, i.e. in advance. These payments are called advance payments. Deadlines for their payment:

- for the first quarter - April 25

- for the half year - July 25

- for nine months - October 25

This is the official name of the reporting periods, associated with the calculation methodology, but in practice it is easier to assume that advance payments are made for each quarter. Moreover, they must be entered only if the entrepreneur received income in the reporting quarter. If there was no income, then you don’t need to pay anything.

All advance payments that were paid during the year are taken into account when calculating tax for the year. In addition, every entrepreneur, regardless of the chosen tax regime, is required to pay insurance premiums for himself. These payments also reduce the tax amount.

For the convenience of paying taxes and insurance premiums, we recommend opening a current account. Moreover, now many banks offer favorable conditions for opening and maintaining a current account.

Individual entrepreneur taxes on OSNO

Entrepreneurs on the general taxation system must pay the following taxes to the budget:

- personal income tax (NDFL) on income paid to employees;

- value added tax (VAT) on goods (services) sold;

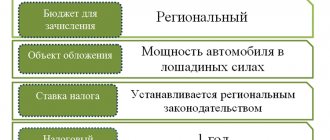

- transport tax if the entrepreneur has transport;

- property tax if the entrepreneur uses property that has a cadastral valuation for non-commercial activities;

- water tax if an entrepreneur uses water resources to generate his income.

Personal income tax (NDFL) combines two taxes: income tax and personal income tax. For individual entrepreneurs, a tax rate of 13% is applied. To calculate the tax amount, the formula is used:

- Tax amount = (total revenue for the year – total confirmed costs) * 13%

or

- Tax amount = (total revenue for the year – total amount of unconfirmed costs) * 20%

For example, the total amount of revenue for the year of an entrepreneur is 1,500,000 rubles, the total amount of confirmed expenses is 700,000 rubles.

Tax amount = (1,500,000 - 700,000) * 13% = 104,000 rubles.

Let's slightly change the condition of the example: the total amount of revenue for the year of the entrepreneur is 1,500,000 rubles, the total amount of unconfirmed expenses is 700,000 rubles.

Tax amount = (1,500,000 - 700,000) * 20% = 160,000 rubles.

The legislation of the Russian Federation does not allow the use of both deductions. Therefore, the entrepreneur, having previously considered both options, must determine for himself which deduction is more profitable for him - 13% or 20%.

Individual entrepreneur insurance premiums 2021

Contributions for oneself are the amounts that an individual entrepreneur pays for his pension and health insurance. Until 2021, contributions were paid to special extra-budgetary funds: PRF and Compulsory Medical Insurance, but then the function of collecting them was transferred to the Federal Tax Service.

Thus, individual entrepreneurs do not pay insurance premiums to the Pension Fund for themselves in 2021. In practice, other concepts are now used:

- contributions to compulsory pension insurance (OPI)

- contributions for compulsory health insurance (CHI)

The amount of individual entrepreneurs’ contributions for themselves is established by the state, and the following amounts are planned for 2018: 26,545 rubles for compulsory health insurance and 5,840 rubles for compulsory medical insurance. The deadline for their payment is December 31 of the current year, but it is more convenient to pay them in installments in order to immediately reduce advance payments.

In addition to these fixed amounts, which all entrepreneurs are required to pay regardless of the amount of income received in the business, there is one more additional contribution. It is 1% of annual income over 300,000 rubles.

Let's assume that an entrepreneur earned 830,000 rubles in 2021. Then the additional contribution will be (830,000 – 300,000 = 530,000) * 1%)) 5,300 rubles. In total, together with the fixed amount of insurance payments, he needs to transfer 37,685 rubles to the budget.

Next, as promised, we will show with examples how entrepreneurs pay the simplified tax system for different objects of taxation. And for those who still have questions or for those who want to get advice from a professional, we can offer a free consultation on taxation from 1C specialists.

Individual entrepreneur taxes in 2021: changes in laws and other innovations that I started collecting

Good afternoon, dear individual entrepreneurs!

I started collecting all the changes for individual entrepreneurs for 2021. Here I collect information on new laws, changes in taxes and fees for individual entrepreneurs, and so on...

Since everything is constantly changing, this article will also be updated over time with new data as it becomes available. And there is no doubt that there will be many changes in 2021.

Therefore, I immediately recommend subscribing to my blog news on this page.

So let's get started

For convenience, all changes will be divided into semantic blocks separated by horizontal lines.

It is clear that repetition is inevitable on many points, and some changes will be duplicated.

New laws

An interesting law for those entrepreneurs who will become individual entrepreneurs in December

An interesting bill has appeared on the State Duma website, which proposes changing the first tax period for individual entrepreneurs that open from December 1 to December 31. That is, if a certain person became an individual entrepreneur from December 1 to December 31, then for the first time he will report for the period from the date of registration in December of the current year until the end of the next year. It has already been approved and is in effect.

Read more:

IP on the simplified tax system in 2021:

Maximum annual income of an individual entrepreneur on the simplified tax system

in 2021, the income of individual entrepreneurs on the simplified tax system cannot be more than 150 million rubles per year. By the way, this income limit for individual entrepreneurs on the simplified tax system coincides with 2021, so the number of 150 million rubles will remain fixed until 2021.

Please note that the deflator coefficient is equal to “1” until 2020.

Read more here:

It is possible that the simplified tax system tax rates will be reduced to:

- 3% for individual entrepreneurs on the simplified tax system “income”

- 8% for individual entrepreneurs using the simplified tax system “income minus expenses”

The corresponding bill has been under consideration in the State Duma for a long time. There were rumors that rates under the simplified tax system would be reduced in 2021, but this did not happen... And it is possible that it will be promptly adopted by the 2021 elections (I have such suspicions)

Read more about this bill here:

https://dmitry-robionek.ru/zakon/snizhenie-nalogov-ip-na-usn-2017.html

Update. This bill was rejected, you can forget about 3% and 8% for everyone. But in the regions of the Russian Federation, authorities can independently set reduced tax rates for the simplified tax system:

By the way, I recently launched a calculator to calculate tax according to the simplified tax system for individual entrepreneurs at the simplified tax system of 6%. You can watch the video instructions and then check it in action.

Fixed contributions for compulsory pension and health insurance:

I wrote a separate and large article on this matter, which can be found here:

But preliminary data for today is as follows

Update: a bill has appeared, according to which it is proposed to untie individual entrepreneurs' insurance premiums from the minimum wage from January 1, 2021. Accordingly, the calculations are as follows:

- Contributions to the Pension Fund for oneself (for pension insurance): 26,545 rubles

- Contributions to the FFOMS for yourself (for health insurance): 5840 rubles

- Total for 2021 = 32,385 rubles

- Also, do not forget about 1% of the amount exceeding 300,000 rubles of annual income

In this case, the maximum amount of a fixed contribution to compulsory pension insurance will be:

Update: a bill from the Government of the Russian Federation has appeared, according to which it is proposed to delink insurance premiums for individual entrepreneurs from the minimum wage from January 1, 2018. Accordingly, the calculations are as follows:

8 * 26545 = 212,360 rubles

Launched an individual entrepreneur insurance premium calculator for 2021

I made the first version of the insurance premium calculator for individual entrepreneurs “for myself” for 2021. You can already estimate them for yourself for 2018.

The calculator itself is here:

Minimum wage (Minimum wage)

According to the latest data, the minimum wage for 2021 will be 9,489 rubles. More details here:

But please note that starting from 2021, the minimum wage no longer affects the amount of mandatory contributions of individual entrepreneurs “for themselves”.

A good bill has appeared, which proposes to amend Article 430 of the Tax Code of the Russian Federation in order to “unlink” the amount of fixed payments of individual entrepreneurs “for themselves” from the size of the minimum wage.

That is, it is proposed to calculate the amount of fixed contributions of individual entrepreneurs based not on the value of the minimum wage (which increases every year), but on a certain variable that will be approved by the government annually.

You can read more about this bill here:

IP on UTII

UTII extended until 2021

The most pleasant thing for individual entrepreneurs on UTII will be that 2021 will NOT be the last year for this special regime. Let me remind you that it was previously planned to limit the validity of UTII until January 1, 2018.

Fortunately, UTII has been extended until 2021:

Individual entrepreneur on UTII and online cash registers

Important update: There will be a delay in the transition to online cash registers until July 1, 2021. But not for everyone. Read more here: https://dmitry-robionek.ru/zakon/otsrochka-po-onlajn-kassam-ip-na-psn-envd-2018-2019.html

But there is bad news: July 1, 2021 will be the last day when individual entrepreneurs on UTII (or PSN) are required to start using online cash registers. Of course, this applies to those individual entrepreneurs on UTII (or PSN) who previously had the right not to use cash registers when making cash payments.

There is a ghostly hope that this date will be postponed to 2021, since at the beginning of 2021 the State Duma received a corresponding bill:

A new bill has appeared in the State Duma on postponing the date of transition to online cash registers for individual entrepreneurs on PSN and UTII to 2021 (!)

In general, I have a lot of articles on the topic of online cash registers on my blog, which are all collected in a separate section:

Current account and cash handling

Update! They have again given a deferment for individual entrepreneurs selling beer until July 1, 2021. Be sure to read this article if you are an individual entrepreneur on PSN or UTII and sell alcoholic beverages:

IP on a patent (PSN)

Still the same problems with online cash registers, which are completely similar to those for individual entrepreneurs on UTII. Therefore, I advise you to read the articles using the links from the previous information block for individual entrepreneurs on UTII.

Also, now if the individual entrepreneur did not manage to renew the patent in time, then this will not lead to the loss of the right to use the PSN.

Details here:

Update. Please note that a new form for obtaining a patent has been introduced. Read more in a separate article:

Tax deduction for the purchase of online cash registers for individual entrepreneurs on PSN and UTII

Yes, for individual entrepreneurs on PSN and UTII they were allowed to make a tax deduction in the amount of no more than 18,000 rubles for each purchased online cash register.

Read more in my other article:

Or just watch the video where I explain everything in detail:

Addition to the video about how to notify the Federal Tax Service to receive a deduction:

- New form of UTII declaration (taking into account tax deductions at online cash desks)

- And for individual entrepreneurs on PSN, they developed a new form of notification of tax deductions, which was introduced by order of the Federal Tax Service of Russia dated March 18, 2019 No. ММВ-7-3 / [email protected]

A resort fee will be introduced

Yes, this will happen in May 2021. Now few people know about it, but the law has already been adopted and individual entrepreneurs who are engaged in the hotel business in the following regions of Russia will face it:

- in the Altai region;

- in the Republic of Crimea;

- in the Stavropol Territory;

- in the Krasnodar region.

Read the full article about the resort fee here:

BSO

Another important point that few people remember. The fact is that SSR (Strict Reporting Forms) are on their last days.

And starting from July 1, 2021, all BSOs will have to switch to electronic format.

Accordingly, new equipment will have to be purchased for the BSO. Details in this article:

Important update: There will be a delay in the transition to online cash registers until July 1, 2021. But not for everyone. Read more here: https://dmitry-robionek.ru/zakon/otsrochka-po-onlajn-kassam-ip-na-psn-envd-2018-2019.html

The list of activities that need to be notified to supervisory authorities has been updated

Yes, few of the individual entrepreneurs remember that after the grand opening of the individual entrepreneur, it would still be a good idea to notify the supervisory authorities when starting certain types of activities. And, in fact, this list was updated back in 2017...

But I’m sure that the vast majority of individual entrepreneurs don’t even know what kind of list this is.

Therefore, I recommend that you read this short article:

https://dmitry-robionek.ru/sovet/spisok-vidov-dejatelnosti-po-kotorym-nuzhno-uvedomljat-nadzornye-organy.html

Rosstat approved 23 reports for 2021. What do you need to submit for IP?

Rosstat recently published a new order, which contains as many as 23 reports (more precisely, statistical forms), which will be submitted by legal entities and individual entrepreneurs from 2018. Do not rush to flinch, since not all of them will have to be taken by the individual entrepreneur.

Read more here:

Tax holidays

Yes, you can still get it. But only for those entrepreneurs who are registering as individual entrepreneurs for the first time. And they fulfill the following requirements, without which it is impossible to obtain this benefit:

- An individual entrepreneur should be opened in your name for the first time. That is, if you close your current individual entrepreneur and in good faith come for the benefits you are entitled to, like a newly opened individual entrepreneur, then you will be refused. Moreover, no more than two years have passed since the registration of the individual entrepreneur, and the registration itself occurred AFTER the REGIONAL law on tax holidays came into force.

- You must work in one of these three areas: industrial, social, scientific.

- Moreover, the share of income from such types of activities should be AT LEAST 70% of the total income of the individual entrepreneur.

- Your region must have a local law that allows tax holidays.

A more detailed article on tax holidays can be found here:

Also, pay special attention to this article:

Self-employed citizens

In May 2021, a discreet announcement appeared on the Federal Tax Service website that they had begun accepting citizens who want to do business, but without opening an individual entrepreneur (or LLC). All you have to do is submit an application and sleep peacefully.

Let me remind you that at the moment the following three types of activities are available to the self-employed:

- For the supervision and care of children, sick persons, persons over 80 years of age, as well as other persons in need of constant outside care according to the conclusion of a medical organization;

- For tutoring;

- Cleaning residential premises, housekeeping;

- Other types of services established by the law of the constituent entity of the Russian Federation (that is, local authorities can add their own types of activities).

You can read more about the self-employed in this article:

Useful services

Generating receipts and payment orders for payment of insurance premiums on the Federal Tax Service website

The Federal Tax Service website has a convenient service with which you can create receipts (or payment orders) for payment of insurance premiums:

https://service.nalog.ru/payment/payment.html

There used to be a similar service on the official website of the Pension Fund, but it closed after the Federal Tax Service took under its wing the collection of insurance premiums to the Pension Fund and the Federal Compulsory Compulsory Medical Insurance Fund.

A new service will appear on the Federal Tax Service website called “Transparent Business”

In fact, with the help of this service it will be possible to find out the tax secrets of legal entities. At the time of testing the service, there was no data on individual entrepreneurs.

Here's what you can learn from it:

- on the amounts of arrears and debt for penalties and fines (for each tax and fee);

- about tax offenses and penalties for their commission;

- on special tax regimes applied by taxpayers;

- on the taxpayer’s participation in a consolidated group of taxpayers;

- on the average number of employees of the organization for the calendar year;

- on the amounts of income and expenses according to the accounting (financial) statements for the year;

- on the amounts of taxes and fees paid by the organization in a calendar year (for each tax and fee) without taking into account the amounts of taxes (fees) paid in connection with the import of goods into the customs territory of the Eurasian Economic Union, the amounts of taxes paid by the tax agent.

It will have to start working on June 1, 2021. Read more here:

“Individual Personal Account” has become accessible from the phone

IP LC is now possible from smartphones. The application developers released two versions to the public back in the spring:

- for Android phones

- for iPhone and iPad

To log in, you can use the same login and password that you use to log into your IP account on a regular computer.

Read more:

PS The article is constantly updated as information becomes available. If you have any data on changes for individual entrepreneurs in 2017, please share them in the comments below.

Good luck!

Best regards, Dmitry Robionek

Don't forget to subscribe to new articles for individual entrepreneurs!

And you will be the first to know about new laws and important changes:

Subscribe to news by email

Dear readers!

A detailed step-by-step guide to opening an individual entrepreneur in 2021 is ready. This e-book is intended primarily for beginners who want to open an individual entrepreneur and work for themselves.

This is what it's called:

“How to open an individual entrepreneur in 2021? Step-by-Step Instructions for Beginners"

From this manual you will learn:

- How to properly prepare documents for opening an individual entrepreneur?

- Selecting OKVED codes for individual entrepreneurs

- Choosing a tax system for individual entrepreneurs (brief overview)

- I will answer many related questions

- Which supervisory authorities need to be notified after opening an individual entrepreneur?

- All examples are for 2021

- And much more!

Find out the details!

Dear entrepreneurs!

A new e-book on taxes and insurance contributions for individual entrepreneurs on the simplified tax system of 6% without employees is ready for 2021:

“What taxes and insurance premiums does an individual entrepreneur pay under the simplified tax system of 6% without employees in 2021?”

The book covers:

- Questions about how, how much and when to pay taxes and insurance premiums in 2021?

- Examples for calculating taxes and insurance premiums “for yourself”

- A calendar of payments for taxes and insurance premiums is provided

- Frequent mistakes and answers to many other questions!

Find out the details!

Dear readers, a new e-book for individual entrepreneurs is ready for 2021:

“Individual Entrepreneurs on the simplified tax system 6% WITHOUT Income and Employees: What Taxes and Insurance Contributions must be paid in 2021?”

This is an e-book for individual entrepreneurs on the simplified tax system of 6% without employees who have NO income in 2021. Written based on numerous questions from individual entrepreneurs who have zero income and do not know how, where and how much to pay taxes and insurance premiums.

Find out the details!

Calculation of tax payments on the simplified tax system Income

For example, let's take a typical entrepreneur who provides household services himself, for example, sewing and repairing clothes at home. His expenses are small, because the fabric and accessories are paid for by the customer, and there is no need to spend money on rent either.

Income is unstable throughout the year; there is a circle of regular customers who order things from time to time. However, for 2021, income from sewing and repairing clothes amounted to 540,000 rubles. Let's see how many taxes and contributions need to be paid on this turnover if an individual entrepreneur works on the simplified tax system Income.

We will not use an academic formula for the calculation, because it is difficult for beginners in accounting. But the option we propose is easier to understand in practice, and all payments will be exactly the same as according to the accounting rules.

So, during the year the income received:

- in the 1st quarter – 83,000 rubles

- in the 2nd quarter – 119,000 rubles

- in the 3rd quarter – 52,000 rubles

- in the 4th quarter – 286,000 rubles

The advance payment for the 1st quarter amounted to (83,000 * 6%) 4,980 rubles, but in March the individual entrepreneur paid part of the insurance premiums for himself in the same amount. The advance payment is completely reduced by the contributions paid, so there is no need to transfer anything to the budget.

The advance for the second quarter is equal to (119,000 * 6%) 7,140 rubles, while in May 7,000 rubles were paid for oneself. We find that the advance payment will be only 140 rubles.

In the third quarter, the calculated advance payment (52,000 * 6%) was 3,120 rubles, with 3,020 rubles paid as contributions in September. You need to transfer 100 rubles to the budget as an advance.

In the last quarter, the entrepreneur paid additional mandatory contributions, taking into account those already paid:

- total fixed amount of contributions 32,385 rubles

- paid quarterly (4,980 + 7,000 + 3,020) = 15,000 rubles

- paid an additional 17,385 rubles

The total amount of the single tax for the year is equal to (540,000 * 6%) 32,400 rubles, while 240 rubles of the advance payment and 32,385 rubles of fixed contributions are deducted from this amount. We find that the amount of tax payable is: 32,400 – 240 – 32,385 = -225 rubles, i.e. an overpayment has occurred. This amount can be offset against future payments or returned from the budget. But for this you need to write an application to the Federal Tax Service, so such a small overpayment can be neglected.

But if the individual entrepreneur did not pay contributions quarterly, then first he would have paid all the calculated advance payments (4,980 + 7,140 + 3,120) in the amount of 15,240 rubles. Then, in December, contributions would be paid in a one-time amount of 32,385 rubles. In this case, the calculated balance of tax payable would be (32,400 – 15,240) 17,160 rubles. This calculated amount is reduced by the contributions paid (17,160 – 32,385

To prevent this from happening, we recommend immediately reducing the calculated advance payments using insurance premiums paid in installments throughout the year.

As for the additional insurance premium in the amount of (540,000 - 300,000) * 1%) 2,400 rubles, the individual entrepreneur has the right to pay it next year - until April 1. In this case, the additional contribution will reduce the advance payment paid for the 1st quarter of 2021.

Calculation of tax payments using the simplified tax system Income minus expenses

For those simplifiers who have chosen this object of taxation, the procedure for reducing tax is different. Insurance premiums paid for oneself do not reduce the calculated tax, but are simply taken into account along with other expenses of the individual entrepreneur.

For example, let’s take an entrepreneur who opened a small retail outlet. His expenses are already significant: purchasing goods, renting premises, transportation costs, etc. The tax rate is standard - 15%.

In the table we will record the income and expenses of individual entrepreneurs by quarter. Contributions paid for yourself quarterly will be indicated separately.

Period

| Income | Expenses, no fees | Paid fees | |

| 1 sq. | 320 000 | 243 000 | 6 500 |

| 2 sq. | 382 000 | 196 000 | 10 000 |

| 3 sq. | 158 000 | 84 000 | 3 000 |

| 4 sq. | 570 000 | 310 000 | 12 885 |

| Total | 1 430 000 | 833 000 | 32 385 |

We calculate advance payments payable:

- for the first quarter – (320,000 – 243,000 – 6,500) * 15% = 10,575 rubles

- for the second quarter – (382,000 – 196,000 – 10,000) * 15% = 26,400 rubles

- for the third quarter – (158,000 – 84,000 – 3,000) * 15% = 10,650 rubles

The calculated taxes for individual entrepreneurs in 2021 from our example will be (1,430,000 – 833,000 – 32,385) * 15% = 84,692 rubles, but of this amount 47,625 rubles have already been paid in advance. You need to pay an additional 37,067 rubles.

But the calculation of the additional insurance premium, which will be paid next year, is based on all income without taking into account expenses, i.e. (1,430,000 – 300,000) * 1% = 11,300 rubles. The injustice of this approach has already been noted by the Supreme Court, but the necessary changes to the Tax Code of the Russian Federation have not yet been made.

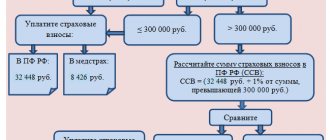

Insurance premiums for individual entrepreneurs for themselves

Insurance premiums are not tax payments, but these are the amounts that individual entrepreneurs are required to pay to the budget under any taxation regime. To plan his business, an entrepreneur needs to know how much he will have to transfer to pay contributions, regardless of whether he receives income.

The amount of contributions for individual entrepreneurs in 2021 will be calculated not from the minimum wage, as in previous years, but from a fixed amount established by the Government:

- for compulsory pension insurance - 26,545 rubles

- for compulsory medical insurance - 5,840 rubles

In total, the fixed amount of contributions for individual entrepreneurs in 2021 will be 32,385 rubles, provided that his annual income does not exceed 300,000 rubles.

If your income is higher, then you will have to pay an additional contribution to pension insurance in the amount of 1% from the difference. For example, with an annual income of 1 million rubles, the additional contribution will be (1,000,000 – 300,000 = 700,000) * 1%) = 7,000 rubles.

Entrepreneurs who hire staff pay the same amount of contributions for themselves as individual entrepreneurs in 2021 without employees.

Personal contributions transferred by an entrepreneur to the budget in most cases reduce his tax payments, but this possibility depends on the chosen taxation system. Below we will look at the tax regimes for individual entrepreneurs in 2021 and the procedure for reducing taxes.

Pros and cons of being an entrepreneur

There are the following advantages of entrepreneurship:

- Registration with the registration authorities follows a simplified procedure. It is enough to fill out and submit to the Federal Tax Service an application drawn up in the prescribed form. You only need to attach to it a copy of your identity document and a receipt confirming payment of the state duty. The registration fee is 800 rubles, which is significantly less than the state duty when registering an enterprise. In addition, the registration procedure through government services is available. In this case, the fee will be only 560 rubles.

- An entrepreneur does not need to register in all places where he carries out his activities; he can register in one region and work in others. In this case, he does not need to carry out any actions to register.

- Existing legal norms for an entrepreneur establish an order of magnitude lower liability for violation of the law.

- Also, individual entrepreneurs are given the right to carry out accounting according to a simplified scheme. This is not affected by the applicable tax systems. The tax accounting registers provided for by law are required to be filled out.

- Individual entrepreneurs under the general regime pay taxes in quantity and amounts significantly less than a legal entity.

- If a subject decides to close a business, he can do this in a short time, because he does not need to go through the liquidation procedure provided for legal entities. In addition, the fee for deregistration as an individual entrepreneur is only 160 rubles.

Do not forget about the negative aspects that may arise when carrying out activities as an individual entrepreneur, these include:

- Entrepreneurs do not have the opportunity to attract outside investment to develop their business. This is due to the fact that the individual entrepreneur does not have an authorized capital, and this person cannot increase it by attracting additional founders.

- If an entrepreneur incurs a debt in the process of doing business, he will be liable for it even if the individual entrepreneur is closed.

- An entrepreneur must submit all declarations and reports at the place of his registration. This rule is quite problematic to follow if the individual entrepreneur does business in another region. The problem is partly solved by using electronic document management when sending reports. But do not forget that inspectors of the Federal Tax Service can call taxpayers to give explanations. Then the entrepreneur will have to go to his place of registration.

- Certain types of activities defined by law are not available to an entrepreneur, that is, there are restrictions on types. All such directions are established in the relevant legal acts.

- An individual entrepreneur must understand that he will not be able to fully sell his business to another person, as can be done with an LLC. Only property is available for transfer, but various permits are valid only in relation to a strictly defined person. Therefore, if necessary, they will have to be issued again.

- Citizens registered as individual entrepreneurs have the obligation to calculate insurance premiums for themselves. Fixed payments will need to be paid to the budget even if there is no actual activity, but the individual entrepreneur is open.

- If an entrepreneur is an employer, then he is required to register in this status with the Social Insurance Fund.

- An entrepreneur must manage all processes independently when carrying out his activities.

Taxation systems for entrepreneurs in the Russian Federation

It is generally accepted that the tax burden of Russian small businesses is too high. In fact, this is not true. If you choose the right taxation system, the financial burden of an entrepreneur will be even less than that of an employee with his salary.

The following types of taxation for individual entrepreneurs are currently in effect in Russia:

- general OSNO system

- simplified simplified taxation system in the “Income” and “Income minus expenses” options

- single tax on imputed income UTII

- PSN patent system

- unified agricultural tax Unified Agricultural Tax

Each tax system differs in the procedure for calculating and paying taxes, while for the same type of activity under different regimes there will be different amounts payable. An example of calculating the tax burden for a store is in this article, and our users can get such a calculation for their business for free.

When choosing taxation for individual entrepreneurs and comparing tax payments under different regimes, it is necessary to take into account the possibility of reducing the calculated amounts by contributions paid for yourself.

| Types of taxation for individual entrepreneurs | Possibility to take into account paid contributions |

| BASIC | Included in expenses, reducing the tax base for tax calculation |

| PSN | Are not taken into account and do not reduce the value of the patent |

| UTII | Reduce the calculated quarterly tax |

| Unified agricultural tax | Included in expenses, reducing the tax base for tax calculation |

| USN Income | Reduce the calculated advance payment and taxes of individual entrepreneurs on the simplified tax system at the end of the year |

| USN Income minus expenses | Included in expenses, reducing the tax base for tax calculation |

An important feature of UTII and simplified tax system Income is that contributions paid by individual entrepreneurs in 2021 without employees for themselves can reduce the calculated payment to zero.

For example, the tax on UTII in 2021 for the quarter amounted to 7,800 rubles, while the entrepreneur paid part of the contributions for himself in the amount of 8,100 rubles in this quarter. The tax payment of 7,800 rubles is completely reduced by the contributions paid, so there is no need to transfer anything to the budget. Individual entrepreneur taxes on the simplified tax system are reduced in a different order, but can also be reduced to zero.

The right to choose a tax regime for individual entrepreneurs in 2021 remains declarative, i.e. The entrepreneur must contact the tax office with the appropriate application:

- on UTII

- to obtain a patent (PSN)

- to the simplified system (USN)