What is being checked

Since the only significant indicator in the form is the number of employees and there are no taxes or fees due on it, the question arises - why is it required?

The fact is that the number of personnel determines the form in which some reports and declarations are submitted - paper or electronic. For example, calculation of 6-NDFL to the Federal Tax Service, form 4-FSS to the Social Insurance Fund are submitted exclusively in electronic form if the number of employees exceeds 25 people, and electronic tax returns are required for numbers of more than 100 people.

The average headcount is one of the criteria for classifying an entity as a small (or micro) business. Also, NCs have established restrictions on the number of:

- with UTII;

- for the possibility of using the simplified tax system;

- when filing a patent.

To track whether the subject has the right to apply such a regime, as well as for other similar purposes, a form has been introduced.

Why is SSC needed?

Many accountants and HR specialists know that the SCH is a small report on the number of people working in an organization or on the staff of an individual entrepreneur. The report form was approved by Federal Tax Service Order No. MM-3-25/ [email protected] dated March 29, 2007 and looks like this:

from ConsultantPlus experts.

Previously, the average number of employees of individual entrepreneurs without employees was always submitted using the same form. The form looks simple, but you need to take into account the specifics of counting the number of workers. The calculation instructions are given in the instructions set out in the letter of the Federal Tax Service No. CHD-6-25 / [email protected] dated April 26, 2007.

Objectives of the report:

- control over the number of full-time employees in order to correctly determine the status of a person (small, large enterprise, etc.);

- clarification of the method of submitting and compiling reports (some entities now submit them only electronically);

- simplification of control over the payment of insurance premiums.

Thus, the SSC for individual entrepreneurs without employees or with employees allows tax authorities to control certain aspects of the taxpayer’s economic activities.

Average number of employees of individual entrepreneurs without employees

The form for calculating the average headcount was approved by the Federal Tax Service of the Russian Federation (order of the Federal Tax Service of the Russian Federation dated March 29, 2007 No. MM-3-25/ [email protected] ). Recommendations for filling out are given in the letter of the Federal Tax Service dated April 26, 2007 No. ChD-6-25 / [email protected] , and the calculation procedure is contained in the order of Rosstat No. 772 dated November 22, 2017.

The number includes all employees registered under an employment contract, and does not include:

- working under civil contracts;

- employees on maternity and child care leave;

- external part-time workers.

The number of employees for each day of the period is calculated and divided by the number of days of the same period. The form is annual, so the data is taken for a year.

Important: an individual entrepreneur may not have employees at the beginning and end of the year, but during the annual period, people were hired and fired. In this case, calculation is necessary, since the average number of employees may not be zero (0.5, according to arithmetic rules, is rounded to 1), and then the entrepreneur is required to submit information. The fine for failure to submit is 200 rubles (clause 1 of Article 126 of the Tax Code).

How to fill

The current form was approved by order of the Federal Tax Service No. MM-3-25/ dated March 29, 2007. The methodology for calculating the SSC was approved by Rosstat Order No. 772 dated November 22, 2017. The letter of the Federal Tax Service No. CHD-6-25/ dated April 26, 2007 indicates how to fill out the average number of individual entrepreneurs without employees: entrepreneurs without employees do not submit reporting information to the tax office.

Other entrepreneurs calculate reporting information as follows: the number of employees present for each day during the month is summed up and divided by the number of calendar days in the month. The data for each month is summed up and divided by 12; no exceptions or deductions are provided.

The calculation takes into account only personnel with whom the employer is obliged to enter into employment contracts. According to the norms, individual entrepreneurs without employees submit the average number only if there were employees on staff during the reporting period. The inclusion of the individual entrepreneur himself without hired employees in the SSC is not required.

The certificate does not take into account personnel who:

- carries out labor activities outside the Russian Federation;

- transferred to another organization;

- placed under a student agreement;

- is on maternity leave, etc.

Read more: “Average number of employees: report to the tax office.”

If the average number of individual entrepreneurs without employees turns out to be “zero”

If there were no employees, the number is zero - is the entrepreneur himself included in the number? An individual entrepreneur is not a hired employee, he does not enter into an employment contract with himself, therefore, when calculating the number of “workers”, he is not included in their number. In paragraph 3 of Art. 80 of the Tax Code directly states that the form must be submitted by “an entrepreneur who hired employees during the specified period.”

Thus, the average number of employees of individual entrepreneurs without employees does not give up.

Submission deadlines

Information on the average number of employees must be submitted to the tax office no later than January 20, 2021 (inclusive). This is what it says in paragraph 3 of Art. 80 Tax Code of the Russian Federation. This report will be for 2017, since the document is submitted once a year.

All organizations are required to comply with the deadline requirement - LLC, CJSC, PJSC, etc.). Moreover, regardless of the presence or absence of workers.

If the registration procedure for a legal entity has been completed quite recently, then the report is sent before the 20th day of the month, which comes after the month of opening.

For more information, see “When to submit a report on the average headcount for 2021.”

As for businessmen, information on the average number of employees of individual entrepreneurs is submitted provided that:

- are registered as an employer;

- use hired labor.

They are subject to a similar deadline requirement (except for the rule of the next month after creation/reorganization).

The individual entrepreneur’s report in question is submitted to the Federal Tax Service at the place of residence.

If the tax office still requests a report

There are situations when one year an individual entrepreneur had hired employees, but the next year they no longer have them. Checking whether everyone has reported, tax officials find such individual entrepreneurs and send requests to submit a document or provide explanations (information). You should not ignore such a requirement to avoid a fine. To prevent this from happening, it is enough to write a letter in response stating that there are no hired employees, the average number of employees is “0”. At the end of the letter, you can point out that in such a situation, an entrepreneur without employees is not obliged to provide the requested information, referring to clause 3 of Art. 80 Tax Code of the Russian Federation.

When there is no staff: do individual entrepreneurs pass the average payroll?

Often, businessmen independently conduct their business affairs, without hiring people or attracting family members (friends) without concluding an employment contract. In this case, you do not need to submit the report in question. A similar rule applies when concluding contracts only of a civil nature.

Exemption from taking the average salary for individual entrepreneurs without employees is possible on the basis of clause 3 of Art. 80 Tax Code of the Russian Federation. This norm establishes the circle of persons who are required to submit a report to the Federal Tax Service on the average number of personnel per year: legal entities and individual entrepreneurs using hired labor.

Thus, only merchants who entered into an employment contract face a fine for failure to submit a report or violation of a deadline. Individual entrepreneurs without employees do not submit the average number of employees for 2021. Therefore, if you receive a notification with such a requirement, you need to inform the tax authorities about the error.

Read also

11.12.2017

Formulas for calculating the average number of employees

Calculating the average headcount of an organization is not very complicated; however, it sometimes causes some difficulties. To do this, let's look at a calculation example in more detail.

The average number of employees for a calendar year is calculated based on the average number of employees for calendar months. In this case, it is necessary to sum up the 12 obtained indicators and divide by 12, that is:

Average average (year) = [ Average average (January) + Average average (February) + Average average (March) + Average average (April) + Average average (May) + Average average (June) + Average average (July) + Average average (August) + Average average (September) + Average average (October) + Average average (November) + Average average (December) ] / 12

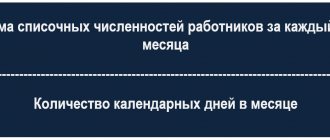

As for the average headcount for the month, it is calculated by summing up all employees who fully worked for the entire month and dividing the result by the number of calendar days. The calculation looks like this:

Average cost (month) = the sum of all employees who worked fully for the month / number of calendar days

Even if some employees were on annual leave, on a business trip or sick, they still need to be taken into account, since they are on the organization’s staff. Those employees who are external part-time workers, on maternity leave, on leave at their own expense, on civil law contracts, sent for off-the-job training and receiving a scholarship, as well as the individual entrepreneur himself are not taken into account. .

When calculating the average number of employees, in most cases, a fractional result is obtained, which must be rounded to a whole number. This is done according to the rules of mathematics:

- a decimal point of 5 or more is rounded up by adding a whole unit;

- decimal places of 4 and less are rounded down without adding a whole unit.

If the organization has employees who work at more than one rate, for example, 1.25 or 1.5, they must be counted as one person, that is, 1 is taken into account for the calculation. For part-time employees, they are counted in proportion to the time they work. In this case, the following calculation of the average number of employees working part-time is made:

Average working hours (part-time work per month) = number of person-hours worked / length of working day / number of working days of the month

The length of the working day can also be different for enterprises: a 40-hour week or an 8-hour working day is considered standard, but there can also be a 20-hour week and a 4-hour working day, etc.

In the case when, for some reason, an individual entrepreneur did not carry out production activities, for these months the average number of employees is taken equal to 0.

Features for individual entrepreneurs: average headcount with and without employees

Until 2014, all individual entrepreneurs were required to submit to the tax authorities information on the average number of employees hired to perform any job duties. Since 2014, this obligation has been abolished at the legislative level (Article 80 of the Tax Code of the Russian Federation). Thus, only those individual entrepreneurs who have hired employees on the basis of employment contracts are required to submit information.

If, for example, an entrepreneur uses the labor of his family members without formalizing labor relations, then these people are not used to calculate the average headcount. In this case, if there are no hired employees, reporting for delivery is not required.

So, if the activity is registered as an individual entrepreneurship, you need to remember the following points:

| Paragraph | A comment |

| Submitting a report on the average number of employees | Responsibilities of entrepreneurs using hired labor on the basis of an employment contract |

| State authorities for receiving reports | To the tax office at the place of registration |

| Report submission deadline | – no later than the 20th day of January of the year following the reporting year; – no later than the 20th day of the month following the month in which the individual entrepreneur was registered |

| Responsibility for failure to submit a report | Liability includes a fine of 200 to 500 rubles. |

Why does the individual entrepreneur not include himself in the certificate?

Despite the fact that changes to the Tax Code were made more than seven years ago, entrepreneurs do not cease to worry and ask how to fill the average number of individual entrepreneurs without employees. In theory, a working individual entrepreneur can include himself in the form, but from the explanations of the Ministry of Finance and the Federal Tax Service it follows that this is not necessary, since:

- An individual entrepreneur does not have the right to conclude an employment contract with himself, and according to the instructions of Rosstat, information is submitted about those employees with whom the employment contract is concluded;

- in accordance with Art. 2 of the Civil Code of the Russian Federation, an entrepreneur organizes his own business, a business at his own peril and risk, the purpose of his activity is to make a profit, and he has the right to act on his own behalf when concluding transactions and in court, but this activity cannot be classified as labor activity.

What is the average headcount?

This is a statistical parameter that may not coincide with the actual number of people employed by the entrepreneur. It is calculated using a special formula. In fact, this is the arithmetic average of all working persons over a certain period of time. For a report, this period is usually a calendar year, that is, 12 months. The average number of employees of individual entrepreneurs with employees is also necessary to determine the right to apply simplified taxation systems. In particular, the simplified tax system and UTII, where such restrictions exist. At the same time, the average number of employees when opening an individual entrepreneur is always zero. The entrepreneur himself, who is actually the owner of the business and does not receive a salary, does not need to be taken into account in this case. Thus, the answer to the common question of whether an individual entrepreneur is included in the average number of employees is negative. In addition, there are a number of employees who also cannot be included in the calculation.