Are there reduced insurance premium rates for SMEs in 2021?

Federal Law No. 102-FZ dated April 1, 2020 not only introduced a reduced tariff for SMEs from April 2021, but also made amendments to the Tax Code of the Russian Federation. The list of insurance premium payers for whom reduced rates apply has been supplemented with a new category (clause 17, clause 1, article 427 of the Tax Code of the Russian Federation):

- For payers of insurance premiums recognized as small or medium-sized businesses in accordance with Federal Law No. 209-FZ dated July 24, 2007 “On the development of small and medium-sized businesses in the Russian Federation” in relation to the portion of payments in favor of an individual determined based on the results of each calendar month as an excess over the minimum wage established by federal law at the beginning of the billing period.

And also, Art. 427 of the Tax Code of the Russian Federation has been supplemented with clause 2.1, according to which for payers specified in clauses. 17, starting from 2021, the following reduced insurance premium rates apply:

1) for compulsory pension insurance:

- within the established limit value of the base for calculating insurance premiums for this type of insurance - 10%;

- above the established maximum base for calculating insurance premiums for this type of insurance - 10%;

2) for compulsory social insurance in case of temporary disability and in connection with maternity - 0%; 3) for compulsory health insurance - 5%.

Thus, SMEs in 2021 and beyond continue to apply a reduced tariff to the part of the base for a calendar month that exceeds the minimum wage.

Who, where, when and in what form submit RSV

Who should submit insurance premium payments?

Filling out the RSV form. Let's start first with who submits the Calculation of Insurance Premiums:

- persons making payments to individuals : organizations, individual entrepreneurs, individuals who are not individual entrepreneurs. The exception is individuals who make payments specified in paragraphs. 3 p. 3 art. 422 of the Tax Code of the Russian Federation (clause 1, clause 1, article 419, clause 7, article 431 of the Tax Code of the Russian Federation);

- heads of peasant farms (clause 3 of article 432 of the Tax Code of the Russian Federation).

Where should I submit my insurance premium payments?

Persons making payments to individuals submit calculations of insurance premiums to the tax authority:

- organizations - at their location and at the location of separate divisions that pay payments to individuals. If a separate division is located outside the Russian Federation, then the organization submits the calculation for such division to the tax authority at its location (clauses 7, 11, 14 of Article 431 of the Tax Code of the Russian Federation);

- individuals (including individual entrepreneurs) - at the place of residence (Clause 7, Article 431 of the Tax Code of the Russian Federation).

The heads of peasant farms submit calculations for insurance premiums to the tax authority at the place of their registration (clause 3 of Article 432 of the Tax Code of the Russian Federation).

How to tax contributions above the minimum wage at reduced rates

Every month you need to look at whether payments in favor of an individual exceed the minimum wage established at the beginning of the billing period (12,792 rubles in 2021). If they exceed, then reduced insurance premium rates are applied to part of the amount above the minimum wage according to the following scheme:

| Contributions | Bid |

| For compulsory pension insurance | And up to the maximum value of the base (1,465,000 rubles), and above - 10% |

| For compulsory social insurance in case of temporary disability and in connection with maternity | 0 % |

| For compulsory health insurance | 5 % |

When calculating insurance premiums, SMEs must indicate that they apply a reduced tariff. To do this, in Appendices 1 and 2 to Section 1, they must enter the tariff code “20”, and in Section 3, apply the category codes of the insured person: MS, VZHMS, VPMS (Order of the Federal Tax Service of the Russian Federation dated September 18, 2019 No. ММВ-7-11/ [ email protected] as amended on October 15, 2020).

How the DAM will change from 2021: average headcount, new codes and applications

Do I need to reflect the funeral benefit in the RSV 2021?

Another payment from social insurance is the so-called funeral benefit. This benefit is available to those employees whose minor family members or family members who worked for the same employer have died (in accordance with the Temporary Rules approved by Resolution of the Federal Social Insurance Fund of Russia dated February 22, 1996 No. 16). The benefit is paid on the condition that the employee (relative of the deceased) bears funeral expenses at his own expense.

Note! The employer has the right to reimburse expenses directly to the funeral service instead of benefits. In this case, these expenses will not fall into the DAM.

The funeral benefit paid and reimbursed by social insurance in the RSV is reflected in line 070 of Appendix 2 to Section 1.

The decoding of this line is given in Appendix 3, line 090.

From February 2021, the limit on this payment is 6,124.86 rubles, adjusted by the regional coefficient.

If the employer decides, on its own initiative or on the basis of labor/collective agreements, to provide financial assistance to an employee in connection with the death of a family member, then such payment is not subject to contributions. It is included in the DAM, but is excluded from the base for each type of contribution. But financial assistance paid in connection with the death of other relatives of the employee who are not considered family members is subject to contributions as standard financial assistance.

How to apply a reduced tariff - formulas from the Federal Tax Service

After the publication of the law, accountants of small and medium-sized enterprises had many questions. Here are some of them.

How to apply a reduced tariff when calculating contributions if the regulations refer to payments, and contributions are calculated from the base?

How can I distribute amounts across applications with different rate codes?

What to do if the employee’s payments amounted to 16,000 rubles (more than the minimum wage), but 5,000 of them are disability benefits, which are not subject to taxation?

What to do if the base limit has been reached? Should non-taxable payments be distributed according to tariffs in proportion to the minimum wage and the part exceeding it?

The Federal Tax Service explained how to apply the norms of 102-FZ, and published the formulas by which SMEs must calculate contributions (letter of the Federal Tax Service dated April 29, 2020 No. BS-4-11 / [email protected] ). If we adapt them to 2021, we get the following formula:

Minimum wage payments from the beginning of the year × 30% + (base from the beginning of the year - minimum wage payments from the beginning of the year) × 15% - contributions accrued from the beginning of the year.

Minimum wage payments are the amount of payments that is less than or equal to the minimum wage at the beginning of the billing period.

For example, to calculate contributions for January, February and March, perform the following calculation:

- for January: minimum wage payments × 30% + (base for January - minimum wage payments) × 15%.

- for February: minimum wage payments for 2 months × 30% + (base for 2 months - minimum wage payments for 2 months) × 15% - contributions calculated for January.

- for March: minimum wage payments for 3 months × 30% + (base for 3 months - minimum wage payments for 3 months) × 15% - contributions calculated for January-February.

Then proceed by analogy.

When the tax base reaches the limit, tax the excess amount at a reduced rate above the limit. To do this, exclude the excess amount from the base from the beginning of the year. The procedure for calculating the taxable base in the month of excess was explained by the Federal Tax Service in a letter dated July 13, 2020 No. BS-4-11/11315.

An example of filling out Appendix 3 of the calculation of insurance premiums

From the article you will learn why you fill out Appendix 3 of the calculation of insurance premiums in 2021. Using an example, we will show how to line-by-line the application and tell you what mistakes accountants make.

Why fill out Appendix No. 3 for calculating contributions?

Calculation of insurance premiums is reporting that employers in 2021 will submit quarterly on an accrual basis to the Federal Tax Service. The reporting deadline is the thirtieth day of the month following the reporting quarter. If the deadline falls on a holiday or weekend, the standard transfer rule applies.

The form (KND 1151111) and the procedure for filling it out were approved by order of the Federal Tax Service of the Russian Federation dated October 10, 2016 No. ММВ-7-11/ [email protected]

It is mandatory for everyone to provide a Title Page, Section 1 with Appendices 1 and 2, Section 3.

The remaining sections are taken as the appropriate situation arises. This is especially true for Appendix 3 of Section 1 of the Calculation of Insurance Premiums 2021. We will talk about it below; you will find a detailed example of filling out this Appendix.

Appendix 3 Calculations for insurance premiums reflects social benefits related to sick leave, maternity, funerals, child care payments and disabled people. The basic principles of filling are as follows:

- All data is cumulative;

- Empty quantitative lines are crossed out, where there are no amounts, put 0;

- Foreign workers are persons who are not citizens of the Russian Federation or the EAEU. Lines 020 and 021 were entered for them;

- In the second column of lines 010 – 031 and 070, enter the number of days, and in the remaining lines the number of benefits issued.

An example of filling out Appendix 3 of the RSV in 2021

The following types of benefits were paid to Udacha LLC, which were then reflected in Appendix 3 of the Calculation of Insurance Premiums for 2019 (all benefits were paid in the 1st quarter of the year).

Employee Insured event How much was issued

| Ramaeva K.G. (citizen of the Russian Federation) | I was in the hospital for 21 days (sick leave) | RUB 45,960 |

| Polipova O.P. | She took out maternity leave until she reaches one and a half years old (this is her first baby) | For 3 months of the 1st quarter I received 41,200 rubles. |

| Geraskina A.S. | Sick leave for pregnancy and childbirth | RUB 301,186 |

| Saltsova E.R. | Registered with the antenatal clinic early in pregnancy | RUB 613.14 |

| Barsukov Yu.B. | I applied for funeral benefits for my father, a company employee. | 5071.31 rub. |

Now you need to record all these payments in Appendix 3 of the Calculation of Insurance Premiums 2021. Let's start with sick leave.

- Column 1 – we write 1, since this is the only case we have in the reporting period;

- Column 2 – 21 (this is the number of days of illness);

- Column 3 (line 010) – 45,960.00

If sick leave was paid to an external part-time worker, it must be allocated separately. To do this, the cells of line 011 are additionally filled in. In our example, there are no such cells.

Now let’s include sick leave for pregnancy and childbirth in the RSV. This will be line 030. Everything is filled out in the same way as sick leave, but instead of the number of days we indicate the number of benefits.

- Column 1 - we write 1, since this is the only case we have in the reporting period;

- Column 2 – enter 1, because this is the only benefit of this kind;

- Column 3 – 301,186.00 – payment amount.

Further, Appendix 3 suggests entering data on women who registered in the early stages of pregnancy. In our example, there is such an employee. In the second column of line 040 we will write 1 (we have one woman who registered early), and in the third we will indicate the amount.

The next payment that needs to be reflected in the third schedule is the monthly child care allowance. To do this, we will use lines 060 and 061, since according to the conditions of the example, the baby is our first. Column 1 is formatted similarly to all previous ones; we will not dwell on it.

- Column 2 - put the number 3. This figure reflects three benefits to one person: for January, February and March 2021;

- Column 3 – reflect the total amount issued over three months – 41,200.00;

- Line 061 completely repeats 060;

- Line 062 is not filled in, since in the example there are no payments for caring for a second child.

The only benefit we have left is the funeral benefit. This data must be included in the last line of Appendix 3 - 090. This is done in exactly the same way as in the above cases. In columns 1 and 2 we write one, since there was one person and there was one payment, in column three - the amount.

To summarize, for this we add all the benefits:

45,960 + 301,186 + 613.14 + 41,200 + 5071.31 = 394,030.45 rubles. This figure must be entered in line 100, column 3. Line 110 in our case remains empty, because all payments were transferred in person.

Source: https://www.Zarplata-online.ru/art/161265-raschet-po-strahovym-vznosam-2019-primer-zapolneniya-prilojeniya-3

Calculation of insurance premiums for the 1st quarter of 2021: form and sample filling

Calculations for insurance premiums must be submitted to the Federal Tax Service no later than the 30th day of the month following the reporting (settlement) period. If the last date of submission falls on a weekend, then the calculation can be submitted on the next working day (clause 7 of Art.

The form was approved by order of the Federal Tax Service of the Russian Federation dated October 10, 2016 No. ММВ-7-11/551.

This form was used in 2021 and should be used now. The Federal Tax Service of Russia planned to adjust the calculation form and posted the project on the Unified Portal for posting draft regulatory legal acts.

What control ratios must be met in the DAM

The situation became even clearer after the Federal Tax Service published the control ratios that must be met for this category of payers in the form of the RSV (letter of the Federal Tax Service dated May 29, 2020 No. BS-4-11 / [email protected] ).

These new control ratios complement the previous list of controls for the DAM form (letter of the Federal Tax Service dated 02/07/2020 No. BS-4-11 / [email protected] ). In the list they are listed under numbers 1.193–1.199, 2.8–2.10. Then these control ratios were supplemented once again (letter of the Federal Tax Service dated June 23, 2020 No. BS-4-11/ [email protected] ).

Let us explain what the wording of these control ratios means.

| Control ratio - wording in the letter from the Federal Tax Service | What does it mean |

| If field 001 adj. 1 rub. 1 SV = 20, then the presence of adj. 1 rub. 1 SV with value 01 in field 001 is required | If there is an application with code “20” in the calculation, then there must also be an application with code “01” |

| If in subsection 3.2.1 p. 3 SV according to FL (according to SNILS + full name indicators) field value 130 = MS, then the presence of subsection 3.2.1 r. 3 SV for this FL with a value in the field of 130 = NR required | If in section 3 of an individual there is subsection 3.2.1 with the code “MS”, then subsection 3.2.1 with the code “NR” must be present |

| If in subsection 3.2.1 p. 3 SV according to FL (according to SNILS + full name indicators) field value 130 = MS, then in subsection 3.2.1 p. 3 SV for this FL with a value in field 130 = NR line 150 for each value of field 120 = minimum wage (based on a base not exceeding the limit value) | If in subsection 3.2.1 there is a line with the code “MS”, then in the line with the code “NR” for the same month the amount in column 150 (base) should be equal to the minimum wage. This requirement applies as long as the base does not exceed the limit |

Thus, the right to apply a reduced tariff appears if the base for calculating contributions for the basic tariff is not less than 12,792 rubles. If less, the reduced rate does not apply that month.

Transfer employees from the previous period and check the DAM for free

An example of entering data in line 030 of applications 1 and 2

There are no rules for filling out line 030, located in Appendices 1 and 2, the procedure for filling out the contribution report (Appendix No. 2 to Order No. MMV-7-11/ [email protected] They follow from the explanations available in the calculation form above line 030 of the corresponding appendices, and from the footnote texts contained in the lower part of the sheets of these appendices, indicated by an asterisk.

The fields provided for indicating five amounts in line 030, allocated in Appendices 1 and 2, are divided in the calculation form into two groups of lines: upper and lower. The top one assumes the reflection of two quantities:

- in the field located to the left - the total value of accruals made for the entire period from the beginning of the year;

- in the field to the right - the total amount of accruals attributable to the last quarter of the reporting period.

The bottom line has three fields designed to show the amounts corresponding to accruals for each of the three months of the last quarter. Data for them will be shown sequentially for the first, second and third month by entering them, respectively, in the left, central and right fields of the line.

Example

Let's assume that our report is generated for the 1st quarter of 2021. The total amount of income accrued to employees for the quarter of the reporting period amounted to 360,000 rubles, including for January - 120,000 rubles, for February - 110,000 rubles, for March - 130,000 rubles. Let's enter this data in line 030 of subsection 1.1, highlighted in Appendix 1.

Our example data will be displayed like this:

360 000,00

120 000,00 110 000,00 130 000,00

How to fill out a calculation: examples

Let's look at an example of how to apply a reduced tariff when calculating pension insurance contributions and filling out the calculation.

Example 1. The base is less than the minimum wage

Let's take the case mentioned above: in February, an employee received 16,000 rubles, 5,000 of which were disability benefits.

Contributions for February need to be calculated only at the basic tariff, since 16,000 - 5,000 = 11,000 (< minimum wage 12,792 rubles).

If we assume that the employee is paid 16,000 rubles every month and only in April there was a non-taxable amount of 5,000 rubles, then in section 3 you need to fill out two subsections 3.2.1.

- Subsection 3.2.1 with category code HP:

- Subsection 3.2.1 with category code MS:

Accordingly, in section 1 in subsection 1.1 of Appendix 1 with tariff code “01” these amounts will be reflected as follows:

And in Appendix 1 with the tariff code “20” - this way:

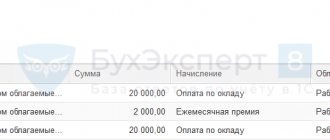

Example 2. The base is greater than the minimum wage

Let’s say an employee’s monthly payments are 20,000 rubles. In February, part of this amount was an allowance of 5,000 rubles.

In this case, the base for February is greater than the minimum wage:

20 000 — 5 000 = 15 000 > 12 792

This means that there is an excess from which contributions are calculated at a reduced rate. Let's look at the formula that the Federal Tax Service requires to calculate contributions. The payment for compulsory pension provision amounts to 3,035.04 rubles:

12 792 × 2 × 22 % + (35 000 — 12 792 × 2) ×10 % – 3 535,04 = 5 628,48 + 941,6 — 3 535,04 = 3 035,04

In the calculation in section 3 this will be reflected as follows:

Example 3. Base limit reached

The requirement for an amount equal to the minimum wage in line 150 of subsection 3.2.1 with code NR must be fulfilled only on a basis that does not exceed the size of the limit.

Let’s assume that an employee’s monthly payments are 500,000 rubles; there are no non-taxable payments. In March, we will exceed the maximum value of the base for OPS (1,465,000 rubles). The amount exceeding the limit of 35,000 rubles:

1 500 000 — 1 465 000 = 35 000

The base, which does not exceed the limit, in March is 465,000 rubles (500,000 - 35,000 > minimum wage).

Using the formula for calculating contributions using a reduced tariff, the amount payable for compulsory pension insurance for March is obtained:

38,376 × 22% + (1,465,000 - 38,376) ×10% + 35,000 × 10% – 103,070.08 (contributions for January–February) = 51,535.04 rubles.

The personalized information does not reflect the base exceeding the limit and contributions from it. Here's how to fill out subsection 3.2.1 in section 3 of the calculation with the HP category code:

And here is a sample of filling out subsection 3.2.1 with the MS category code:

The base in excess of the limit and contributions from it will be reflected in subsection 1.1 of Appendix 1 with code 20 in lines 051 and 062.

How to fill in lines “060”, “061”, “062” in the calculation of insurance premiums

- Banks

- Loans

- Insurance

- Finance

- Forex and stock exchange

The lines under consideration are included in the categorized parts of the reporting form KND 1151111.

The lines under study are included in some mandatory parts of the SV calculation (format KND 1151111), as well as minor ones, which are drawn up and submitted if necessary.

Let's look at how to fill out lines 060, 061 and 062 in the calculation of insurance premiums.

| Rubricated parts of the calculation form KND 1151111 | Category of employers who need to fill them out | The lines under consideration as part of the named categorized parts of the calculation form |

| Sec. 1 | 060 | |

| Adj. 1 to Section 1 (1.1) | Individual entrepreneurs, organizations that accrued and paid wages to employees | 060, cells 1-5; 061, cells 1-5; 062, cells 1-5 |

| Adj. 1 to Section 1 (1.2) | 060, cells 1-5 | |

| Appendix 2 to Section 1 | Employers who paid OSS fees (VN and M) | 060, cells 1-5 |

| Appendix 3 to Section 1 | Employers who made expenses for OSS purposes | 060; 061; 062 |

| Appendix 4 to Section 1 | Obligated persons who paid benefits to employees from the federal budget | 060 |

| Adj. 6 k Section 1 | Organizations and individual entrepreneurs on the simplified tax system that carry out activities in the social (or production) sphere and have the right to apply a reduced rate when calculating mandatory fees; IP on the simplified tax system and patent | 060 |

| Adj. 8 k Section 1 | Policyholders with the insurance fee payer code “12”: individual entrepreneurs on a patent, except for those working in the field of real estate rental, retail trade or public catering | 060 |

| Adj. Section 9 1 | Obligated persons who paid wages to foreign workers and stateless persons temporarily staying in the territory of the Russian Federation | 060 |

| Adj. 10 to Sec. 1 | Employers who paid full-time students money for work (services) in a construction team | 060 |

| Adj. 1 to Section 2 | Peasant farms paying fees | 060 |

| Sec. 3 (3.1) | Employers paying employees wages | 060 |

The guide to line-by-line filling is still the original source - the Procedure for filling out the calculation of SV, introduced by the order of the Federal Tax Service No. ММВ-7-11 / [email protected] dated 10.10.2016 (hereinafter referred to as the Procedure).

Table - composition of the lines under consideration in the mandatory sections of KND 1151111

| Mandatory classified parts of the calculation of SV | Information to fill out (according to the lines being studied) | Instruction on registration |

| Sec. 1 | “060” - KBK for crediting generally obligatory fees (OPS at an additional rate) | Procedure, part 5, clause 5.10 if there are several codes, then the required number of sheets of this section is drawn up with the corresponding indicators in lines “060-073”; if there is no code, dashes are added |

| Adj. 1 to Section 1 (1.1) | · “060” - the total amount of calculated OPS fees (indicator line “061” + indicator line “062”); · “061” (cells 3-5) - the amount of mandatory pension fees from a base not exceeding the maximum; · “062” (cells 3-5) - the amount of mandatory pension fees from a base exceeding the maximum, which is equivalent to the value: indicator page "051" cells 3-5 * 10/100 (for payers with tariff codes “01”, “02”, “03”) | Procedure, part 7, clauses 7.1 and 7.9, as well as clause 7.10. and 7.11 |

| Adj. 1 to Section 1 (1.2) | “060” (cells 3-5) - the total amount of calculated compulsory medical insurance fees | Procedure, part 8, clauses 8.1 and 8.7; the indicator of the row in question is equal to the value: indicator page "050" i. 3—5 * tariff (according to the payer's tariff code) |

| Adj. 2 to Section 1 | “060” (cells 1-5) - the amount of calculated OSS fees (VN and M) | Procedure, part 11, clause 11.2 and 11.12 |

| Section 3 (3.1) | “060” - INN (12 digits) assigned to the insured employee of the Federal Tax Service upon registration (if any); You can find out your personal tax identification number: in the certificate of registration with the Federal Tax Service, on page 18 of the passport if there is a proper TIN mark there, on the Federal Tax Service website through the “Find out your TIN” service | Procedure, part 22, clauses 22.8 and 22.9; |

Filling out the RSV form. Section 1

Section 1 includes summary data on the obligations of the insurance premium payer. This section reflects (Section V of the Procedure for filling out the calculation of insurance premiums):

- OKTMO code;

- amounts of insurance premiums payable for the billing (reporting) period, including for the last three months of the billing (reporting) period;

- the amount of excess in the billing (reporting) period of expenses for the payment of insurance coverage for VNIM over the amount of calculated contributions for this type of insurance, including for the last three months of the billing (reporting) period;

- the corresponding KBK, to which the amount of insurance premiums is subject to credit or reimbursement from the budget.

Filling out Appendix 1 to Section 1 of the RSV

In line 001 “Payer tariff code” of Appendix 1 to Sec. 1, you must indicate the applicable tariff code from Appendix No. 5 to the Procedure for filling out the calculation of insurance premiums (except for tariff codes “21” - “29”).

The calculation includes as many applications as 1 to Sec. 1 (or individual subsections of this application), how many tariffs were applied during the billing (reporting) period.

Reason: clause 6.4 of the Procedure for filling out the calculation of insurance premiums.

Filling out subsection 1.1 of Appendix 1 to section 1 of the DAM

In subsection 1.1 of Appendix 1 to section. 1, the amount of insurance premiums for compulsory health insurance is calculated. The data in it is reflected in the following breakdown: in total from the beginning of the billing (reporting) period, for the last three months of the billing (reporting) period, as well as for the first, second and third months of the last three months of the billing (reporting) period (Section VII of the Procedure filling out the calculation of insurance premiums).

The corresponding columns of the subsection reflect (Section VII of the Procedure for filling out the calculation of insurance premiums):

- the total number of persons insured in the compulsory health insurance system, as well as the number of persons from whose payments contributions to compulsory health insurance are calculated (including the number of persons whose payments exceeded the maximum base value for compulsory health insurance);

- amounts of payments calculated in favor of individuals and amounts not subject to contributions to compulsory pension insurance;

- the base for calculating contributions to compulsory pension insurance (including the base in amounts exceeding the maximum value);

- the total amount of contributions to be paid to the compulsory pension insurance, including a breakdown into amounts calculated from a base that does not exceed the maximum value, and from a base that exceeds this value.

Basic tariff codes (line 001):

- 01 - organization on a general regime, charging contributions at basic tariffs;

- 02 - organization on the simplified tax system with basic tariffs;

- 08 - organization on the simplified tax system with reduced tariffs, conducting preferential activities;

- 03 - UTII payer with basic tariffs.

The number of insured persons (line 010) - all employees registered in your organization, as well as those who work under the GPA. Line 010 may be larger than line 020. After all, line 010 will take into account workers on maternity leave who do not have payments subject to contributions.

The data on payments and contributions in subsection 1.1 must correspond to the data in section. 3 for all employees (clause 7 of Article 431 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service dated December 13, 2017 N GD-4-11/25417).

Filling out subsection 1.2 of Appendix 1 to section 1 of the DAM

In subsection 1.2 of Appendix 1 to section. 1 the amount of insurance premiums for compulsory medical insurance is calculated. The data in it is reflected in the following breakdown: total from the beginning of the billing (reporting) period, for the last three months of the billing (reporting) period, as well as for the first, second and third months of the last three months of the billing (reporting) period (Section VIII of the Procedure filling out the calculation of insurance premiums).

The corresponding columns of the subsection reflect (Section VIII of the Procedure for filling out the calculation of insurance premiums):

- the total number of persons insured in the compulsory medical insurance system, as well as the number of persons from whose payments contributions to compulsory medical insurance are calculated;

- amounts of payments accrued in favor of individuals and amounts not subject to compulsory health insurance contributions;

- base for calculating contributions to compulsory medical insurance;

- amounts of compulsory medical insurance contributions payable.

Filling out Appendix 2 to Section 1 of the RSV

In Appendix 2 to section. 1 the amount of contributions for VNIM is calculated. The data in it is reflected in the following breakdown: in total from the beginning of the billing (reporting) period, for the last three months of the billing (reporting) period, as well as for the first, second and third months of the last three months of the billing (reporting) period (Section XI of the Procedure filling out the calculation of insurance premiums).

The specified Appendix reflects (Section XI of the Procedure for filling out the calculation of insurance premiums):

- number of persons insured against accidents;

- amounts of payments calculated in favor of individuals and amounts not subject to VNIM contributions;

- amounts of payments exceeding the maximum base for contributions in the event of VNiM;

- base for calculating contributions for VNIM;

- calculated amount of contributions for VNIM;

- the amount of expenses for the payment of insurance coverage for VNiM and the amount of these expenses that was reimbursed by the Federal Social Insurance Fund of the Russian Federation;

- the amount of insurance premiums for VNIM subject to payment, or the amount of excess of expenses incurred over the amount of calculated contributions for VNIM.

In the “Payment attribute” field, put “2” (offset system), if you calculate and pay employee benefits yourself. If employees receive benefits directly from the Social Insurance Fund, put “1” (direct payments).

In line 070, indicate accrued benefits at the expense of the Social Insurance Fund. The date of payment of the benefit and the period for which it was accrued do not matter. For example, child care benefits for March were accrued on June 30 and paid on July 9. It must be shown in column 5 of line 070.

The amount in column 1 of line 070 of Appendix 2 must be equal to the amount in column 3 of line 100 of Appendix 3 to section. 1. Calculate the indicator for column 2 of line 090 using the formula (Letter of the Federal Tax Service dated November 20, 2017 N GD-4-11/ [email protected] ):

If the result comes with a “+” sign, that is, contributions to VNiM exceeded benefits from the Social Insurance Fund, in column 1 of line 090, put the sign “1”. If the value of the indicator turns out to be with the sign “-“, put the sign “2” (Letter of the Federal Tax Service dated 04/09/2018 N BS-4-11 / [email protected] ).

In the same order, calculate and fill out columns 4, 6, 8, 10 of line 090.

Appendix 2 section. 1 calculation should be filled out taking into account the following features (Letters of the Federal Tax Service of Russia dated 04/09/2018 N BS-4-11 / [email protected] , dated 08/23/2017 N BS-4-11/ [email protected] ):

- the amounts of expenses reimbursed by the Federal Social Insurance Fund of the Russian Federation (line 080) are reflected in the columns corresponding to the month in which they were actually reimbursed;

- the indicators of line 090 in the corresponding columns are determined as follows: line 090 = line 060 - line 070 + line 080. The resulting indicator for line 090 is always reflected in a positive value. If it is greater than or equal to 0, the row attribute 090 has the value "1". Otherwise - “2”.

Filling out Appendix 3 to Section 1 of the DAM (if benefits were accrued)

In Appendix 3 , reflect only benefits from the Social Insurance Fund accrued in 2021. The date of payment of the benefit and the period for which it was accrued do not matter. For example, reflect a benefit accrued at the end of June and paid in July in the calculation for the six months. Reflect the sick leave benefit, which is open in June and closed in July, only in calculations for 9 months.

Do not indicate benefits at the expense of the employer for the first three days of the employee’s illness in Appendix 3.

Enter all data on a cumulative basis from the beginning of the year (clauses 12.2 - 12.4 of the Procedure for filling out the calculation).

In column 1, indicate on lines 010 - 031, 090 the number of cases for which benefits were accrued. For example, in line 010 - the number of sick days, and in line 030 - maternity leave. On lines 060 - 062, indicate the number of employees to whom benefits were accrued (clause 12.2 of the Procedure for filling out the calculation).

In column 2, reflect (clause 12.3 of the Procedure for filling out the calculation):

- in lines 010 - 031 and 070 - the number of days for which benefits were accrued at the expense of the Social Insurance Fund;

- in lines 060 - 062 - the number of monthly child care benefits. For example, if during the entire six months you paid benefits to two employees, put 12 in line 060;

- in lines 040, 050 and 090 - the number of benefits.

Filling out the RSV form. Section 3

Fill it out separately for each employee. Please specify:

- in field 040 - a serial number that you define yourself. This can be either the number of personalized information in order (1, 2, 3, etc.) or the employee’s personnel number (Letter of the Federal Tax Service dated January 10, 2017 N BS-4-11 / [email protected] );

- in field 050 - the date of payment;

- in line 120 - for a Russian employee the code is “643”, for a foreigner - the code of his country from OKSM;

- in line 140 - code of the type of document identifying the employee. If it is a Russian passport, write “21”;

The category code of the insured person (column 200) for citizens of the Russian Federation is “NR”. Codes for foreigners: temporarily staying - VPNR, temporarily residing - VZHNR. If you pay contributions at reduced rates on the simplified tax system, the codes will be different: citizens of the Russian Federation - PNED, temporarily staying foreigners - VPED, temporarily residing foreigners - VZhED.

In columns 210 - 250, show payments to the employee and accrued contributions to compulsory pension insurance from a base not exceeding the limit for the 2nd quarter - monthly and in total.

Section 3 must be completed for all insured persons for the last three months of the billing (reporting) period, including persons in whose favor payments were accrued during the reporting period within the framework of employment relationships and contracts listed in clause 22.1 of the Procedure for filling out the calculation of insurance premiums .

The procedure for filling out the details in section. 3 explained by the Federal Tax Service of Russia in Letter dated December 21, 2017 N GD-4-11/ [email protected]

In subsection 3.1 section. 3 indicates the personal data of the individual who is the recipient of the income: full name, tax identification number, SNILS, etc. (clauses 22.8 - 22.19 of the Procedure for filling out the calculation of insurance premiums).

the SZV-M form , which was accepted by the Pension Fund of Russia (Letter of the Federal Tax Service of Russia dated October 31, 2017 N GD-4-11/22115).

If an individual has not reported the TIN, you can use the online service “Find out TIN” on the website of the Federal Tax Service of Russia. When there is no information about the TIN, on page 060 section. 3 calculations are marked with a dash. The tax authority will accept such a calculation (Letter of the Federal Tax Service of Russia dated November 16, 2017 N GD-4-11 / [email protected] , clause 2.20 of the Procedure for filling out calculations for insurance premiums).

In subsection 3.2 section. 3 indicates information about the amounts of payments calculated in favor of an individual, as well as information about accrued insurance premiums for compulsory health insurance (clauses 22.20 - 22.36 of the Procedure for filling out calculations for insurance premiums).

For persons who did not receive payments for the last three months of the reporting (calculation) period, subsection 3.2 section. 3 does not need to be filled out (clause 22.2 of the Procedure for filling out the calculation of insurance premiums).