Fixed assets (FPE) may be written off over time for various reasons. OSes can simply become unusable, they can be sold or even donated. How to process various asset disposal transactions in accounting, see below.

First of all, any disposal of fixed assets must be documented and all details of the operation must be indicated in the documents.

When the asset is worn out, a write-off act is drawn up, which is signed by members of a specially created commission.

To register the disposal of fixed assets, there are unified forms of acts. The main form is OS-4, it is suitable for the vast majority of OS. If you need to write off a car, use act OS-4a. For group write-off of fixed assets, form OS-4b is used.

Write-off of OS as a result of physical or moral wear and tear

Wear and tear can be physical - this can include the failure of equipment due to a long period of use.

Obsolescence can be moral - for example, computer technology often becomes obsolete, so companies write off obsolete computers and replace them with modern ones.

The write-off of OS due to wear and tear is recorded with the following entries:

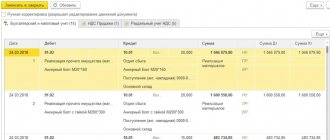

Debit 01 subaccount “Disposal” Credit 01 - the original cost is written off;

Debit 02 Credit 01 subaccount “Disposal” - accrued depreciation is written off;

Debit 91 Credit 01 subaccount “Disposal” - the residual value is written off.

Write-off procedure

An organizational and administrative document (for example, an order) when writing off fixed assets can be drawn up in order to confirm the intention or consent of management that the fixed asset will be written off from accounting.

However, such a document is not mandatory. The need to compile it is determined by the peculiarities of the activities of a particular organization, its scale, management style, document flow procedures and other factors. More often, we talk about an order to write off fixed assets in the case when an asset is written off due to moral or physical wear and tear. It is usually preceded by the preparation of a document confirming that the object is unsuitable for further use and containing recommendations for its decommissioning. As an example of such a document, we can consider a defective write-off statement, the form of which we presented in a separate material.

| Limited Liability Company "Ekostor" 121351, Moscow, st. Kuntsevskaya, 26 TIN 7731332719 / KPP 773101001 Order No. 3/OS-17 Moscow 09/05/2017 Due to the failure of a fixed asset item, Shredder Kobra 300.2 HS (0.8x9.5 mm) (inventory No. 05692) and the economic infeasibility of repairing it, based on the defective statement dated August 31, 2017 No. 2 I ORDER: 1. Commission consisting of Deputy General Director for General Issues N.G. Plugova. (chairman), accountant S.P. Myakinina, warehouse manager V.A. Shcheglov. by 09/08/2017, draw up a Kobra 300.2 HS Shredder (0.8x9.5 mm) (inventory No. 05692) for the fixed asset object in accordance with form No. OS-4; 2. Write off the fixed asset item Shredder Kobra 300.2 HS (0.8x9.5 mm) (inventory No. 05692) from accounting within the same period; 3. Entrust control over the execution of this order to the chief accountant O.R. Nesterova. General Director Mokhov O.L. The order has been reviewed by: Plugov N.G. ________________ Myakinina S.P. _____________ Shcheglov V.A. _______________ Nesterova O.R. ______________ |

We invite you to familiarize yourself with: Temporary registration procedure

https://www.youtube.com/watch?v=ytadvertiseru

Based on the order to write off a fixed asset, a write-off act can be drawn up either in an independently developed or in a unified form. For example, according to form No. OS-4, a sample for filling it out in relation to the situation discussed in the example was given in a separate consultation.

During the inventory, goods that are subject to spoilage and expired are identified, as well as those on which an expiration date should be indicated, but in fact it is not. All these goods are classified as unusable and withdrawn from trade.

Write-off of goods that have become unusable is carried out on the basis of:

- Civil Code of the Russian Federation, art. 469, 470, 472;

- Federal Law-2300-1 dated 07/02/92

According to the norms of the Civil Code, the seller is obliged to offer the buyer only high-quality, usable goods. The sale of goods with an expired expiration date is prohibited, and this period must be set in such a way that the consumer can use the product before its expiration.

The Federal Law “On the Protection of Consumer Rights” requires the transfer to the buyer of goods that meet the mandatory requirements for it (Article 4), and also names goods on which the manufacturer must indicate an expiration date: medicines, household chemicals, cosmetics, perfumes, products (Article . 5).

Goods that are expired or do not have an expiration date indicated on the packaging are returned by the trading establishment to the supplier, destroyed or disposed of.

Federal Law No. 446 dated November 28, 2018 introduced a ban on the return of perishable goods of good quality (with a shelf life of less than a month). Requests for refunds or replacements for items subject to perishable deterioration have also been prohibited since the end of last year.

If the unusable product is not returned to the supplier, it is destroyed or disposed of. Without the participation of third parties, this can be done in relation to spoiled products or goods whose exact origin is unknown. In other cases, an expert assessment from a supervisory government agency (veterinary, merchandising, etc., depending on the type of product) is required.

Inventory is carried out according to rules No. 49 of 06/13/95. Damaged goods are not included in the inventory, but are entered in the write-off act according to f. TORG-16 (15) or using an independently developed form reflected in the LNA. When using unified forms, it is recommended to fill out both acts. TORG-15 documents the fact of damage, the TORG-16 act records the withdrawal from trade circulation and further actions in relation to the goods: recycling, destruction.

We suggest you read: We bought an apartment and don’t receive property taxes

On a note! When disposed of, the product can still be processed and used; if destroyed, further processing is not possible.

The destruction of goods, in addition to the act signed by the commission and the conclusion, is formalized by a separate order. If damage or impossibility of further use of the goods is detected, explanations are taken from financially responsible persons. These actions allow us to identify the reason why the product has become unusable, for example:

- expiration date missed;

- damage due to the negligence of responsible persons;

- force majeure situation.

Depending on it, transactions are reflected in tax and accounting.

“Overdue” goods and the costs of their disposal can be taken into account without any problems in the NU, when reducing the tax base. This is stated in letters of the Ministry of Finance No. 03-03-06/1/53901 dated 08/23/17, No. 03-03-06/1/30409 dated 05/26/16 and a number of others. Likewise - spoilage within the limits of loss norms. The unsuitability of the goods, as a result of the negligence of the guilty persons, is compensated by these guilty persons in accordance with Chapter. 39 Labor Code of the Russian Federation. Losses of goods are first reflected in non-operating expenses (Tax Code of the Russian Federation, Art. 265), and then as non-operating income (Tax Code of the Russian Federation, Art. 250).

https://www.youtube.com/watch?v=ytpressru

The situation of damage during a natural disaster makes it possible to include the cost of damaged goods in expenses (Article 265-2-6), as well as the fact of failure to identify those responsible for the damage to goods (ibid., paragraph 5). This fact must be confirmed by a certificate of termination of the criminal case (letter 16 -15/065190 dated June 25, 2009, Federal Tax Service in Moscow).

When writing off unusable goods, account 94 is used, reflecting shortages and losses of inventory items.

Sale of fixed assets

Fixed assets may also be disposed of as a result of sale. For example, you can implement obsolete operating systems. Or, for example, a company decides to update equipment in a workshop and first sells machines that are physically worn out, and then uses the proceeds to purchase new equipment.

When selling a fixed asset, it is important to fill out all the documents correctly and make the correct entries.

It is customary to formalize the sale of OS using OS or OS-1 acts.

Example. OJSC MTZ sells Opel cars. Depreciation for Opel is 231,000 rubles. The initial cost of the Opel car is 783,000 rubles, the residual cost is 552,000 rubles (783,000 - 231,000). The Opel sale price is set at 512,000 rubles.

The accountant of MTZ LLC made the following entries:

Debit 62 Credit 91 - 512,000 - proceeds from the sale of Opel;

Debit 91 Credit 68 - 78,101.69 - VAT on proceeds from the sale of Opel (512,000 x 18/118);

Debit 01 subaccount “Disposal” Credit 01 - 783,000 - the original cost of Opel is written off;

Debit 02 Credit 01 subaccount “Disposal” - 231,000 - depreciation accrued for Opel during the period of operation at MTZ LLC is written off;

Debit 91 Credit 01 subaccount “Disposal” - 552,000 - the residual value of Opel is written off.

Tax reporting on time and without errors! We are giving access for 3 months to Kontur.Ektern!

Try it

Rules for drawing up an order for writing off fixed assets

It is mandatory that an order be drawn up taking into account certain standards.

In this case, you need to take into account a package of documentation that will allow you to legally carry out the planned procedure. In each case, the order to write off a fixed asset is the most important document.

Regardless of the reasons for the planned procedure, a specially created commission must meet and conduct the necessary checks in order to confirm that the asset will no longer be profitable for the organization.

The commission always includes employees of the enterprise . The obligatory persons are: an accountant, as well as an employee who is responsible for the safety of the company’s property.

The composition of the full commission must be approved by the head of the enterprise.

The order provides the basis for further activities.

It is expected that members of the commission will conduct special inspections and assess the condition of the property, determine the possibility and feasibility of restoring the property.

After this, the reasons for further liquidation will be determined.

It is mandatory to identify all elements used as individual spare parts for the company’s business activities.

If the unsuitability of the operating facility has been confirmed by specialists, the manager must confirm this fact in a special order, which will allow measures to be taken to liquidate the fixed asset with the correct execution of the relevant act.

Free transfer (donation) of fixed assets

When transferring free of charge, it is important to charge VAT. You can donate (transfer) the operating system either to your employee or to a third party. The OS must be donated according to the contract. A gratuitous transfer is reflected in accounting at the market value of the fixed assets on the date of donation.

Example. MTZ LLC presented an Opel car to employee of the year A.T. Burov. The Opel car had previously been used by the company for three years. Depreciation for Opel is 231,000 rubles. The initial cost of the Opel car is 783,000 rubles, the residual cost is 552,000 rubles (783,000 - 231,000). The market value of the Opel car on the date of gratuitous transfer is 512,000 rubles.

Postings:

Debit 01 subaccount “Disposal” Credit 01 - 783,000 - original cost written off;

Debit 02 Credit 01 subaccount “Disposal” - 231,000 - accrued depreciation written off;

Debit 91 Credit 01 subaccount “Disposal” - 552,000 residual value written off;

Debit 91 Credit 68 - 92,160 - VAT is charged on the market value (512,000 x 18%).

Postings

Standard transactions for damage to goods will be as follows:

- 94/41 – damaged goods written off;

- 41/42 reversal – the trade margin is reversed;

- 96, 44/94 – allocation of costs due to the created reserve for product losses or to increase sales costs (within the limits of loss norms);

- 91-2, 73/94 - attribution of costs to the perpetrators or to other expenses if the culprit is not identified;

- 73/98 – if there is a difference between the price recorded for the goods and the amount collected from the culprit;

- 98/91-1 – attribution of this difference to other income.

We invite you to read: Taxes have arrived for three years

If the volume of damaged goods exceeds natural loss, VAT is restored: 94/68.

Unusable goods with expired expiration dates are reflected in the following entries:

- 91, 90/41 – if the product is disposed of;

- 94/41 – if the goods are destroyed.

Reasons for writing off computer equipment: examples

Our publication is devoted to the disposal of office equipment included in the OS, so we will add just a few words about how to write off a computer costing less than 40,000. Such equipment is usually included in the inventory and is written off as costs during commissioning.

The main criterion for writing off OS is the loss of necessary useful qualities used for production purposes. The classic reasons for such a loss are physical and moral wear and tear, as well as breakdown or damage that cannot be eliminated. Legislators have approved very short useful lives (USL) for depreciation calculations for office equipment - 3 - 5 years. We will not dwell on physical wear and tear, since it is associated with an understandable situation when the SPI of office equipment has expired and write-off is carried out legally. Let's talk about obsolescence.

Office equipment, to a much greater extent than other groups of operating systems, is subject to rapid obsolescence. This is due to the rapid development of computer technology and often leads to the fact that the company’s fleet of working computers requires modernization or complete renewal in order to make production profitable. And periodically repeated modernization of equipment does not always satisfy the increasing requirements of new software products, so we can talk about obsolescence of the object.