Fixed assets, otherwise called fixed assets , capital, property assets, etc., are part of the national welfare. That which takes part in the production process for quite a long period, without essentially changing, but only wearing out and losing value, gradually transfers its value to the products produced.

The lion's share of the national property of our state is concentrated in the form of fixed assets. They are very diverse, so it is necessary to understand their composition, know which groups a particular asset can be classified into, and also according to what principle they can be distributed.

We consider all issues related to the classification of an enterprise’s assets – its fixed assets.

On what basis can fixed assets be classified?

To analyze the composition of the operating system, various grouping bases are used. Everything a business owns can be viewed in different contexts:

- industry of application – means for the production of goods, provision of services or performance of work;

- property – property assets can be divided according to their forms of ownership into public, private, etc.;

- involvement - according to the degree of involvement in the activities of the enterprise, one can distinguish directly used operating systems, backup, spare, repaired, reconstructed, mothballed, etc.;

- source – own property, rented, leased, etc.;

- territory - fixed assets on the balance sheet of a particular enterprise, industry, district, republic, territory, region, city or any other structural territorial unit;

- age – a certain depreciation group, that is, division depending on the maximum useful life;

- form of existence – tangible and intangible funds (according to the all-Russian classifier).

Let's look at the most common grounds for classifying fixed assets.

Funds depending on their purpose

According to the function that property funds perform, they can be divided into two large independent groups:

- production assets: those that are used and/or created in the process of the enterprise’s activities;

- non-productive assets : those that help serve production without directly affecting the quantity of product produced.

Funds related to production are reproduced through additional capital investments, just like non-production ones. The main difference between these types of property assets is that the former are directly related to the enterprise’s products, while the latter affect it only indirectly, influencing the work culture of employees.

Groups of production assets

For convenience, production fixed assets, which can be classified as material

- Building (except for those intended for housing):

- garages;

offices;

- workshops;

- housings;

- warehouses;

- hangars;

- outbuildings, etc.

- Buildings, structures - what is necessary for production:

- bridges;

- paths;

- overpasses;

- fencing;

- forests;

- roads, etc.

- Communication means – provide the transfer function:

- communication lines;

- overpasses;

- pipelines;

- heating networks;

- power lines, etc.

- cars and equipment:

- all kinds of devices;

- any units;

- engines;

- measuring technology;

- analyzing instruments;

- laboratory equipment;

- Computer Engineering.

- Tools – all intended for use for more than 1 year:

- devices;

- work supplies;

- household equipment.

- Transport – all forms and types of vehicles, including those used for internal movement in production:

- road transport owned by the company;

- railway rolling stock;

- water vehicles;

- punishments;

- trolleys;

- trolleys;

- loaders, etc.

- Livestock – working and breeding. The composition of fixed assets does not include the cost of feed, young animals and livestock intended for slaughter, since these funds are used for less than a year, and therefore belong to working capital, not fixed assets.

- Perennial plantings:

- parks;

- orchards;

- forest protection strips;

- berry plantations, etc.

- Plots of land are real estate owned by the organization.

Their cost as an operating system includes not only the construction component, but also the costs of communications (ventilation, heating, water supply, gas pipeline, etc.).

IMPORTANT ! In each economic sector, these groups have their own specifications: for example, in agriculture, the composition of fixed assets for the same groups may differ significantly from industrial.

Determination of fixed assets of an enterprise

When making accounting entries for the inclusion of any objects in the enterprise’s property as fixed assets, it is necessary to determine whether they meet the following requirements:

- Each separate unit can be used for the production or internal needs of the enterprise, or rented out to them for a fee;

- The useful life of such property is more than 12 calendar months, or exceeds the production cycle period if it is obviously longer than 12 months;

- The acquisition of a property did not imply its subsequent resale;

- The operation of the facility is economically beneficial, that is, it directly or indirectly increases the income of the enterprise.

Regulatory accounting procedures IFRS 16, Order of the Ministry of Finance No. 186n dated December 24, 2010. oblige to simultaneously comply with all conditions for registering property as fixed assets. It is also worth noting that an equally “popular” criterion for introducing objects into fixed assets is the cost indicator.

Indeed, already at the time of receipt, focusing on the Decree of the Government of the Russian Federation of February 12, 1993 N 121 on the implementation of the State program for the transition of the Russian Federation to the accounting and statistics system accepted in international practice in accordance with the requirements of the development of a market economy, it is easy to identify those property objects that the cost of which is above the threshold of 40 thousand rubles.

This criterion cannot be applied to weapons, agricultural machinery and productive livestock. These assets are classified as fixed assets regardless of their value.

So, fixed assets are material assets used by an enterprise for a long time to make a profit. However, for accounting and tax accounting, including accounting entries and accounting documentation, one definition of the essence of fixed assets is clearly not enough.

It is important to divide objects into categories of use - groups and types of operating systems.

Active and passive fixed assets

If this type of property assets directly affects the process of producing products, providing services, performing work, determining the result in terms of quantity and quality, then it is classified as active .

Examples include tools, equipment, transmission media, etc.

Those fixed assets that only create the necessary conditions for the production process, but are not directly involved in it, are considered passive .

These are fixed assets such as buildings, transport, structures, structures, etc.

The average annual value of each of these groups of fixed assets determines the production structure of fixed assets , that is, their ratio in the system of material assets. The production structure reflects the natural-material approach to the classification of fixed assets.

NOTE! A structure in which the share of active operating systems prevails over passive ones is considered more effective.

Share of the active part of fixed assets

Shows what part of the total cost of existing fixed assets is their active part (participating in the production of products). The active part of fixed assets is machinery, equipment and vehicles. The growth of this indicator in dynamics is usually regarded as a favorable trend.

Calculation formula:

Share of the active part of fixed assets = cost of the active part of fixed assets / cost of fixed assets

Share of the active part of fixed assets (2014) = 473,734/474,684 = 0.998

Share of the active part of fixed assets (2013) = 388,593/389,550 = 0.998

Author: Erkina Tukhtaeva

asked a question in the section

Accounting, Audit, Taxes,

the share of the active part is determined as the ratio of the active part of fixed assets to the cost of fixed assets and received the best answer

Answer from Elena Monosova [active] The main production assets are usually divided into two parts: the active and passive part. The active part of fixed assets usually includes those assets that are directly involved in the production process (machinery and equipment), vehicles and tools. The passive part of fixed assets includes those means that ensure the normal functioning of the production process. On average, for production, the active part of fixed assets is 60%, and the passive part is 40% of the total composition of fixed assets. The most important factors influencing the structure of fixed production assets are: the nature of the products produced, the volume of output, the level of automation and mechanization, the level of specialization and cooperation, the climatic and geographical conditions of the location of enterprises. In addition, all fixed assets are divided into fixed production assets and fixed non-productive assets. The main production assets include those that are directly involved in the production process (machines, equipment, machine tools, etc.) or create the conditions for the production process (industrial buildings, pipelines, etc.). The main non-productive assets (funds) include residential buildings, children's and other cultural and community service facilities for workers, which are on the balance sheet of the enterprise. Unlike means of production, they do not participate in the production process and do not transfer their value to the product, because it is not produced. Despite the fact that non-production fixed assets do not have a direct impact on production volume or the growth of labor productivity, a constant increase in these assets is inextricably linked with improving the well-being of the enterprise’s employees and increasing the material and cultural standard of their lives, which ultimately affects the results of the enterprise’s activities.

The balance of fixed assets (fixed assets) looks like equality:

He + P = V + Ok

- It

is the availability of fixed assets at the beginning of the reporting period - P

– receipt of fixed assets during the period - B

– disposal of fixed assets during the period - OK

The balance sheet of fixed assets may contain clarifying categories: major repairs, increase/decrease in the value of fixed assets as a result of revaluation and disposal due to dilapidation:

He + Pp + K + D = Vp + U + Sun + Ok

- He

- pp

- TO

- D

- VP

- U

- Sun

- Ok

– availability of fixed assets at the end of the period.

In this case, all elements of equality are given at the original cost of fixed assets. The balance of fixed assets at historical cost is closely related to the balance at their cost, taking into account depreciation:

(He – In) + Pp + K + D – I = Vp + U + Sun – Iv + (Ok – Ik)

- It

is the availability of fixed assets at the beginning of the period - In

- the amount of depreciation that falls on the balance of fixed assets at the beginning of the period - Pp

– receipt of fixed assets as a result of purchase - K

– cost of major repairs (reconstruction, modernization) performed during the period - D

– increase in the value of fixed assets as a result of revaluation - I

– the amount of depreciation accrued for the period (minus depreciation on retired fixed assets) - Вп

– disposal of fixed assets as a result of their sale - U

– reduction in the value of fixed assets as a result of markdown - Sun

- disposal as a result of write-off due to disrepair (and other reasons: transfer to the composition of MNMA or to the composition of current assets, etc.) - Iv

- the amount of depreciation that falls on retired fixed assets - Ok

– availability of fixed assets at the end of the period - IK

is the amount of depreciation that falls on the balance of the fixed asset at the end of the period.

The residual value of fixed assets can be expressed by the formula:

Ost = Ostn + P + K – Vo – I

- Residual

– residual value of fixed assets at the end of the period - Ostn

– residual value of fixed assets at the beginning of the period - P

– receipt of fixed assets for the period - K

– cost of major repairs (reconstruction, modernization) performed during the period - В

– residual value of fixed assets disposed of during the period - And

– the amount of depreciation accrued for the period.

In order to analyze the property status, it is advisable to draw up such balances in the context of all types (groups) of fixed assets, highlighting their active part.

Based on the data from these balances, generalized indicators of their condition are determined - suitability coefficients, retirement coefficients and renewal coefficients. If such balances are compiled by groups of fixed assets, all these coefficients can be determined accordingly for each group.

Working capital balance

The current assets balance sheet looks similar to what a simplified fixed assets balance sheet looks like:

He + P = V + Ok

- It

is the availability of working capital at the beginning of the reporting period - B

– disposal of working capital during the period - Ok

– availability of working capital at the end of the period.

P

– receipt of working capital during the period

In order to analyze the property situation, it is advisable to draw up such balances in the context of all types (groups) of working capital: by materials, finished products, goods, etc.

Determination of the average annual value of property.

To calculate the average availability of fixed assets over the period, a simplified approach is sometimes used - the arithmetic average method.

The arithmetic mean is defined as half the sum of data on the availability of fixed assets at the beginning and end of the analyzed period. But more accurate information about the average annual cost of fixed assets is obtained in a different way. It is advisable to calculate the average annual value of fixed assets as the quotient of dividing by 12 the half-sum obtained by adding (and dividing by 2) the cost of fixed assets in force on January 1 of the reporting year and on January 1 of the year following the reporting year, as well as the value of these assets for each first the number of the remaining eleven months of the analyzed year.

Determining the average cost of fixed assets for an intermediate period (quarter, half-year, 9 months) is carried out by dividing by the number of months of the analyzed period half the value of the fixed assets on the 1st day of the first month following the end of the period, as well as the cost of fixed assets on every 1st day the remaining months of this period.

The average annual (and average for any intermediate period) cost of standardized current assets is calculated in a similar way. Standardized current assets include: inventories, work in progress, finished goods; in this case, construction materials purchased by developers for the purpose of capital construction are excluded from inventories. Non-standardized current assets include cash and all types of receivables

In some cases, if the enterprise is small and the movement of fixed assets is not so intense, simplification is used in calculating the average annual cost of fixed assets. Namely, instead of divisor 12, divisor 4 is used, i.e., not by the number of months, but by the number of quarters in the year.

Sometimes the average annual value of fixed assets is determined based on their average annual value for the previous calendar year.

The average annual cost of fixed assets for the previous calendar year (if we take the simplified, “quarterly” version) is determined as the amount divided by four:

- half the cost of fixed assets as of January 1 of the previous calendar year;

the value of fixed assets as of April 1 of the previous calendar year;

Which value of fixed assets should be taken into account - initial or residual (balance sheet) - depends on the purpose for which this calculation is carried out.

So, if the average annual cost of fixed assets is calculated to determine the capital productivity

, the calculation of the average annual cost of fixed assets should be based on their initial cost, because otherwise, if we take the balance sheet (residual) value into account, the capital productivity indicator will be simply absurd: the more worn out fixed assets are, the higher their profitability. The profitability of fixed assets (capital productivity) cannot increase due to their deterioration.

If the average annual cost of fixed assets is calculated to determine the capital intensity

, the calculation of the average annual cost of fixed assets can be based on both their initial and residual value, depending on the purposes of the analysis - here it is impossible to give unambiguous advice.

If the average annual cost of fixed assets is calculated to determine the capital-labor ratio

, in contrast to the capital productivity indicator, on the contrary, it is advisable to take their book (residual) value as a base. The initial cost of worn-out objects will unreasonably inflate the capital-labor ratio.

Basic criteria for assessing property status

- Serviceability ratio of fixed assets.

Shows what part of the original cost of fixed assets has not yet been worn out, in other words, has not yet been transferred to the product:Kg = (Pst – I)/Pst

- Kg

– shelf life coefficient

Pst

– initial cost - Kg

- And

- wear and tear.

The formula for calculating the suitability coefficient can be presented differently:

Kg = Ost/Pst

- Kg

– shelf life coefficient - Residual

value - Pst

– initial cost.

Since the serviceability coefficient and the wear rate are interrelated (Kg + Ki = 1), the serviceability coefficient of fixed assets can be calculated in another way:

Kg = 1 – Ki

- Kg

– shelf life coefficient - Ki

– wear coefficient.

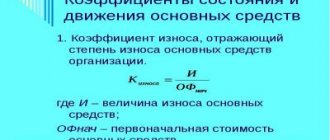

. Shows the degree of depreciation of fixed assets, i.e. the share of the cost of fixed assets subject to write-off as expenses of subsequent periods:

Ki = I/Pst

- Ki

– wear coefficient

I

– wear

– initial cost.

And since the wear coefficient is an addition (up to 100%) to the serviceability coefficient, it can also be calculated as the difference between one and the serviceability coefficient:

Ki = 1 – Kg

Both the wear rate and the serviceability rate are rather conditional indicators of the technical condition of fixed assets. This is due to many reasons: inflation rates, fluctuations in market prices for similar assets, a subjective approach to determining the service life, etc. However, the value of such a conditional coefficient as a depreciation coefficient above 0.5 is considered undesirable. Accordingly, the suitability coefficient should not be lower than this value.

Shows what part of the fixed assets available at the end of the period consists of new objects:

Ko = Pstp/Pstk

- Ko

– renewal coefficient

Pstp

- the initial cost of fixed assets received during the period

– initial cost of fixed assets at the end of the period

For different groups of fixed assets (groups of production facilities, their active part and groups of facilities operated in the non-production sector), it is advisable to calculate separate renewal coefficients. It also makes sense to calculate them separately for all received groups of objects and separately for those put into operation. In the latter case, such a coefficient is usually called the input coefficient

.

In addition, when analyzing, it is advisable to compare the renewal rate of the active part of fixed assets with the renewal rate of all objects on the balance sheet. This way it becomes clear which part is responsible for the update. If the renewal of fixed assets does not occur at the expense of their active part, then this may negatively affect the capital productivity indicator.

Renewal of fixed assets can occur both through the acquisition of new facilities and through the modernization of existing ones. Therefore, in this case, the renewal factors should be calculated separately.

A variation of the renewal coefficient is the automation coefficient:

Ka = Psta/Pst

- Ka

– automation coefficient - Psta

– initial cost of automated objects - Pst

is the initial cost of all existing fixed assets.

Shows what part of fixed assets was retired during the reporting month.

Kv = Pstv/Pstn

- Kv

- fixed asset retirement ratio

Pstv

- the initial cost of fixed assets disposed of during the period

– the initial cost of fixed assets available at the beginning of the period

For different groups of fixed assets (groups of production facilities, their active part and groups of facilities operated in the non-production sector), it is advisable to calculate separate retirement rates. It also makes sense to calculate them separately for all retired objects and separately for liquidated ones. In the latter case, this coefficient is usually called the liquidation coefficient

.

In addition, when analyzing, it is advisable to compare the retirement rate of the active part of fixed assets with the retirement rate of all objects. In this way, it becomes clear at the expense of which part the disposal occurs.

Shows what part of the total cost of existing fixed assets is their active (participating in production) part:

Yes = Psta/Pst

- Yes

– share of the active part of fixed assets (ratio)

Psta

– average annual cost of fixed assets belonging to the active part

– the cost of fixed assets on the balance sheet (average annual).

The share of the active part of fixed assets does not have to be calculated in an average annual value. In this case, you should take into account the balance of fixed assets at the end of the analyzed period, without calculating their average annual value.

The growth of this indicator in dynamics means a favorable trend.

Reflects the profitability of the use of fixed assets involved in the production of products and shows how many products are produced for each ruble of the cost of fixed assets:

Fo = Vp/OPF

- FO

– capital productivity (return on production assets)

Vp

– volume of production for the year

.

Calculation of the average annual cost of fixed assets when determining the capital productivity indicator should be based on their original cost, and not on the balance sheet (residual). Otherwise, you will get an absurd result: the more dilapidated the equipment is, the higher the return on assets - this should not happen.

An indicator inverse to the capital productivity indicator. Shows how many fixed assets, on average, are accounted for for each ruble of the cost of manufactured products.

Fe = OPF/Vp

- Fe

– capital intensity

OPF

– cost of fixed production assets (average annual)

is the volume of production for the year.

When calculating the average annual cost of fixed assets to determine capital intensity, you can take both their initial and residual value as a basis, depending on the purposes of the analysis.

Shows the level of equipment of personnel with labor tools, their technical equipment:

Fv = OPF/Ssch

- Fv

– capital-labor ratio

OPF

– cost of fixed production assets (average annual)

– the average number of workers employed in production.

When calculating the average annual cost of fixed assets to determine the capital-labor ratio, it is advisable to take their balance sheet (residual) value as a base. The initial cost of dilapidated objects will greatly embellish the capital-labor ratio - this cannot be allowed.

We can also say that the capital-labor ratio shows the cost of a workplace

.

It is advisable to analyze the capital-labor ratio both for the enterprise as a whole and in the context of production and technological processes.

A low capital-labor ratio may indicate that an enterprise is lagging behind in mastering advanced technologies, which leads to a loss of competitiveness. The growth of the capital-labor ratio is the most important factor in increasing labor productivity.

However, one should not think that the growth of the capital-labor ratio always reflects a favorable trend. There is a so-called capital-labor ratio, and it is determined individually for each enterprise. This limit is formed depending on how much the increase in the capital-labor ratio results in an increase in labor productivity. Therefore, the following condition must be met:

- ∆Fv > 0

- ∆Pt > 0

If, with an increase in the capital-labor ratio, the increase in productivity turns out to be above zero, then the use of technical means is considered effective and the limit of the capital-labor ratio has not yet arrived. It should be noted that it is advisable to determine the capital-labor ratio limit in the same way as the indicator itself - not only for the enterprise as a whole, but also for individual production and technological processes - which is more important. The maximum capital-labor ratio for the enterprise as a whole depends on the capital-labor ratio of each individual process.

At the same time, when analyzing the capital-labor ratio, it is necessary to pay attention to external factors of labor productivity growth. It is possible that the growth of labor productivity is no longer influenced by the capital-labor ratio, but by the growth of productivity at enterprises in related industries or other circumstances. There are quite a lot of factors for the growth of labor productivity and one should not rush to attribute all the “merits” to the capital-labor ratio.

Shows the specific weight of material resource consumption per unit of production. It is measured in physical units (technological indicator), in monetary terms and as a percentage (economic indicator). The economic value of the material intensity indicator is calculated as the share of the cost of consumed material resources in the price of a unit of production:

Me = M/Vp x 100%

- Me

– material consumption

M

– cost of raw materials and materials used for production

– volume of production for the analyzed period

Thus, material intensity shows how many material and raw material costs are incurred for each ruble of product output.

Sometimes it is advisable to calculate material intensity as the share of the cost of material resources in the cost of manufactured products. In this case, the denominator of the formula indicates the volume of output not in sales prices, but at its cost.

The cost (monetary) indicator of material intensity is defined as the difference between the cost (or selling price) of a unit of production of one type or another and the cost of the material and raw materials expended on its production. In this case, the averaged values of these components of the formula are taken into account.

The excess of the actual material intensity indicator over its standard indicator indicates the presence of reserves for reducing the standard material intensity, which, in turn, indicates an increase in production profitability.

Standard material consumption is established depending on the industry sector of the enterprise.

The share of working capital in assets

- the formula for calculating it will be discussed in the article - shows the ratio of current assets to the total assets of the company, including non-current assets. Let us consider the features of calculating this indicator in more detail.

Fixed assets classified as non-productive

The purpose of funds determines their role in the production process.

Funds intended to have a direct impact not on the production process itself, but in one way or another to influence personnel, are considered non-productive .

Their main function is to ensure the well-being of employees, compliance with working conditions and culture, thereby indirectly increasing its efficiency. Such basic means include:

- homes;

- administrative buildings;

- cultural buildings and structures (clubs, stadiums, gyms, canteens, etc.);

- medical premises and equipment, etc.

The concept of fixed and working capital

Fixed assets

REFERENCE! More specifically, fixed assets include all structures, buildings, equipment, machinery and others, which make up the majority of capital investments at the primary stage of the enterprise’s life cycle.

Working capital of the enterprise

Working capital includes all material assets that are expressed in monetary form and are directly involved in the production process, but this can only be done once. The cost of working capital is fully transferred to the cost of goods. For example, fixed assets are machines and other equipment with the help of which the production process takes place, and working capital are raw materials and supplies, without which the product will not be produced.

REFERENCE! The expression of working capital is almost always in cash and is used to carry out ongoing activities.

What is the difference between fixed assets and working capital?

- Fixed assets are buildings, structures, furniture, equipment, machines that are directly involved in the production cycle, but do not transfer their elements to the finished product. The difference between working capital is that they are included in the final result entirely; their consumption occurs in the process of one completed production cycle.

- The cost of fixed and working capital is included in the cost of goods. The difference is that fixed assets are included in it in the form of depreciation and are only partially reflected in the price, while working capital is included in the cost in full. The final cost of the product for consumers depends largely on the cost of materials and raw materials.

- Fixed assets can be replaced with new ones only after their cost has been fully recovered. This process usually takes several years. Current assets, in turn, are sold immediately. Accordingly, for the next production cycle they need to be purchased again.

Intangible fixed assets

Assets that are not expressed in material form, but nevertheless have a cost characteristic, constitute a special group of fixed assets of an enterprise. They are called produced assets rather than production assets .

These may include:

- expenses for exploration work (for example, during mining);

- computer software;

- Database;

- original works related to various types of art;

- scientific technologies, developments;

- any objects of intellectual property.

Inactive fixed assets

The composition of fixed assets, or rather, their value, includes not only the above groups of material objects, but also those that have become part of the owner’s property in an unfinished, non-working form, or those for which payment is made in installments and is not available at the time of settlement. fully produced.

Such assets are not yet capable of being active in the production process, but their value is already increasing the composition of fixed assets. Such “deferred” fixed assets include:

- unfinished construction projects;

- equipment that is not fully installed and ready for use;

- not fully paid assets;

- plantings that have not yet begun to bear fruit;

- bee colonies (but not the beekeeping products they produce);

- laying hens (raised for egg production), etc.

In the process of scientific and technological progress, with the development of economic science, changes in government policy and under the influence of other factors, approaches to the classification of fixed assets may be periodically updated: their composition, membership in one or another group may change, and new grounds for association and accounting may appear.

Fixed assets of the enterprise. Economic essence

All assets held by an enterprise, regardless of their form, constitute its assets. During the activity of an enterprise, its assets participate in the production process of producing products (works or services) and directly and indirectly, participating in ensuring the internal functions of the enterprise.

Based on the method of transferring the price of assets into the cost of finished products, they can be defined as current and fixed.

The cost of the former, fully used during one production cycle, is transferred directly to products, according to their consumption in physical form.

The latter participate in the production activities of the enterprise for a long period of time and form the cost of goods indirectly, with the transfer of a conditional part of their value in the share of depreciation, which corresponds to the estimated waste (wear and tear) of assets.

According to the principle of materialization, fixed assets are divided into two types - intangible and tangible funds. Intangible assets of an enterprise imply intangible objects of an intellectual nature with certain rights to their use.

Material assets, otherwise known as fixed assets, are objects that have a physical embodiment and are used by an enterprise during several production cycles.

The most important point that should be paid attention to when defining an object as the main means is its isolation in constructive and functional terms. Only a certain device or a group of objects and devices that are a single complex, capable of acting independently in production, can be considered suitable for recognition in accounting as an object of fixed assets.