The patent taxation system is established by the Tax Code, put into effect by the laws of the constituent entities of the Russian Federation and applied in the territories of these constituent entities of the Russian Federation.

Individual entrepreneurs who have switched to a patent taxation system are recognized as taxpayers.

The transition to a patent taxation system or a return to other taxation regimes by individual entrepreneurs is carried out voluntarily

From 01/01/2021, the changes provided for by Federal Law dated 23/11/2020 No. 373-FZ come into force:

- PSN payers, like UTII payers, are given the right to reduce the amount of tax calculated for the tax period by insurance premiums;

- The list of activities in respect of which PSN can be applied has been expanded, including those that were used within the framework of UTII: parking lot activities, repair, maintenance and washing of vehicles;

- The area restrictions for retail trade and catering services have been increased from 50 to 150 square meters. m.

Who has the right to apply the patent tax system

^To the top of the page

15 for the tax period for all types of business activities carried out by an individual entrepreneur (Article 346.43 of the Tax Code of the Russian Federation)

The patent tax system does not apply:

- in relation to types of business activities carried out within the framework of a simple partnership agreement (joint activity agreement) or a property trust management agreement (clause 6 of Article 346.43 of the Tax Code of the Russian Federation);

- in relation to the sale of goods not related to retail trade (sale of excisable goods specified in subparagraphs 6 - 10 of paragraph 1 of Article 181 of the Tax Code of the Russian Federation, as well as the sale of medicines, footwear and clothing items, clothing accessories and other items subject to mandatory labeling by identification means products made from natural fur (full list in clause 1, clause 3, article 346.43 of the Tax Code of the Russian Federation).

Replaces taxes

^To the top of the page

The use of the patent taxation system provides for exemption from the obligation to pay (clause 10, clause 11 of Article 346.43 of the Tax Code of the Russian Federation):

- Personal income tax

In terms of income received from the implementation of types of business activities in respect of which the patent tax system is applied - Property tax for individuals

In terms of property used in carrying out types of business activities in respect of which the patent tax system is applied - VAT

Excluding VAT payable: - when carrying out types of business activities in respect of which the patent tax system does not apply

- when importing goods into the territory of the Russian Federation and other territories under its jurisdiction

- when carrying out transactions taxed in accordance with Articles 161 and 174.1 of the Tax Code of the Russian Federation

Types of business activities in respect of which the patent tax system can be applied

- repair and tailoring of clothing, fur and leather products, hats and textile haberdashery products, repair, tailoring and knitting of knitwear according to individual orders of the population

- shoe repair, cleaning, painting and sewing;

- hairdressing and beauty services;

- washing, dry cleaning and dyeing of textiles and fur products;

- production and repair of metal haberdashery, keys, license plates, street signs;

- repair of electronic household appliances, household appliances, watches, metal products for household and household purposes, objects and products made of metal, production of finished metal products for household purposes according to individual orders of the population;

- repair of furniture and household items;

- services in the field of photography;

- repair, maintenance of motor vehicles and motor vehicles, motorcycles, machinery and equipment, vehicle washing, polishing and provision of similar services;

- provision of motor transport services for the transportation of goods by road by individual entrepreneurs who have the right of ownership or other right (use, possession and (or) disposal) of vehicles intended for the provision of such services;

- provision of motor transport services for the transportation of passengers by road by individual entrepreneurs who have the right of ownership or other right (use, possession and (or) disposal) of vehicles intended for the provision of such services;

- reconstruction or repair of existing residential and non-residential buildings, as well as sports facilities;

- services for installation, electrical, sanitary and welding works;

- services for glazing balconies and loggias, cutting glass and mirrors, artistic glass processing;

- services in the field of preschool education and additional education for children and adults;

- services for supervision and care of children and the sick;

- collection of containers and recyclable materials;

- veterinary activities;

- leasing (hiring) of own or leased residential premises, as well as leasing of own or leased non-residential premises (including exhibition halls, warehouses), land plots;

- production of folk arts and crafts;

- services for the processing of agricultural, forestry and fishery products into human food and animal feed, as well as the production of various intermediate products that are not food products;

- production and restoration of carpets and rugs;

- repair of jewelry, costume jewelry;

- embossing and engraving of jewelry;

- activities in the field of sound recording and publishing of musical works;

- cleaning services for apartments and private houses, activities of households with hired workers;

- activities specialized in the field of design, decoration services;

- conducting physical education and sports classes;

- porter services at railway stations, bus stations, air terminals, airports, sea and river ports;

- paid toilet services;

- services for preparing and supplying dishes for special occasions or other events;

- provision of services for the transportation of passengers by water transport;

- provision of services for the transportation of goods by water transport;

- services related to the marketing of agricultural products (storage, sorting, drying, washing, packaging, packing and transportation);

- services related to the maintenance of agricultural production (mechanized, agrochemical, land reclamation, transport work);

- landscape improvement activities;

- hunting, catching and shooting of wild animals, including the provision of services in these areas, activities related to sport and amateur hunting;

- engaging in medical activities or pharmaceutical activities by a person licensed for these types of activities, with the exception of the sale of medicinal products subject to mandatory labeling by means of identification, including control (identification) marks in accordance with Federal Law No. 61-FZ of April 12, 2010 “ On the circulation of medicines";

- carrying out private detective activities by a licensed person;

- rental services;

- excursion tourist services;

- organization of rituals (weddings, anniversaries), including musical accompaniment;

- organizing funerals and providing related services;

- services of street patrols, security guards, watchmen and watchmen;

- retail trade carried out through stationary retail chain facilities with trading floors;

- retail trade carried out through stationary retail chain facilities that do not have sales floors, as well as through non-stationary retail chain facilities;

- public catering services provided through public catering facilities;

- public catering services provided through public catering facilities that do not have a customer service area;

- provision of services for slaughter and transportation of livestock;

- production of leather and leather products;

- collection and procurement of food forest resources, non-timber forest resources and medicinal plants;

- processing and canning of fruits and vegetables;

- production of dairy products;

- crop production, services in the field of crop production;

- production of bakery and flour confectionery products;

- fishing and fish farming, recreational and sport fishing;

- forestry and other forestry activities;

- translation and interpretation activities;

- activities for caring for the elderly and disabled;

- collection, processing and disposal

- cutting, processing and finishing of stone for monuments;

- development of computer software, including system software, software applications, databases, web pages, including their adaptation and modification;

- repair of computers and communications equipment;

- livestock farming, livestock farming services;

- operation of vehicle parking;

- grain grinding, production of flour and cereals from wheat, rye, oats, corn or other grains;

- pet care services;

- production and repair of cooper's utensils and pottery according to individual orders of the population;

- services for the production of felted shoes;

- services for the production of agricultural implements from customer material according to individual orders of the population;

- engraving work on metal, glass, porcelain, wood, ceramics, except jewelry for individual orders of the population;

- production and repair of wooden boats according to individual orders of the population;

- repair of toys and similar products;

- repair of sports and tourist equipment;

- services for plowing gardens on individual orders of the population;

- services for sawing firewood on individual orders of the population;

- assembly and repair of glasses;

- production and printing of business cards and invitation cards for family celebrations;

- bookbinding, stitching, edging, cardboard works;

- repair services for siphons and autosiphons, including charging gas cartridges for siphons.

A complete list of activities is listed in the law on the application by individual entrepreneurs of the patent tax system of the constituent entity of the Russian Federation in which business activities will be carried out.

Combining the patent taxation system with other taxation systems

^To the top of the page

The provisions of Chapter 26.5 of the Tax Code of the Russian Federation do not prohibit individual entrepreneurs from combining several tax regimes.

When applying the patent taxation system and carrying out types of business activities in respect of which an individual entrepreneur applies a different taxation regime, the individual entrepreneur is obliged to keep records of property, liabilities and business transactions in accordance with the procedure established within the framework of the applicable taxation regime (clause 6 of Article 346.53 Tax Code of the Russian Federation).

The procedure for transition to a patent tax system

^To the top of the page

To obtain a patent, an individual entrepreneur must submit to the tax authority an application for a patent in the form approved by Order of the Federal Tax Service of Russia dated December 9, 2020 No. KCh-7-3/ [ email protected] “On approval of the application form for a patent, procedure its completion, the format for submitting an application for a patent in electronic form and the invalidation of the order of the Federal Tax Service dated July 11, 2017 No. ММВ-7-3/ [email protected] .”

Patent application form pdf (268 kb)

Download

Format for submitting a patent application in electronic form docx (71 kb)

Download

Procedure for filling out an application for a patent docx (43 kb)

Download

Patent application diagram xsd (37 kb)

Download

At the same time, individual entrepreneurs also have the right to apply for a patent in the following form:

Application form for a patent, approved by order of the Federal Tax Service of Russia dated July 11, 2017 No. ММВ-7-3/ [email protected] pdf (237 kb)

Download

Format for submitting an application for a patent in electronic form doc (213 kb)

Download

Procedure for filling out an application for a patent docx (51 kb)

Download

Patent application diagram xsd (36 kb)

Download

An application for a patent must be submitted no later than 10 days before the application of the patent tax system.

When carrying out activities at the place of residence,

the Application is submitted to the tax authority at the place of residence

When carrying out activities on the territory of a municipal entity, city district, federal city or constituent entity of the Russian Federation in which the entrepreneur is not registered for tax purposes, the Application is submitted to any territorial tax authority of the municipal entity, urban district, federal city or constituent entity of the Russian Federation at the location planned implementation of entrepreneurial activities by an individual entrepreneur

An individual entrepreneur who has lost the right to use a patent taxation system or has ceased business activities in respect of which a patent taxation system was applied before the expiration of the patent has the right to again switch to a patent taxation system for the same type of business activity no earlier than from the next calendar year ( paragraph 2 of article 346.45 of the Tax Code of the Russian Federation)

The application can be submitted in person or through a representative, sent by mail with a list of attachments, or transmitted electronically via telecommunications channels.

What taxes does the patent tax system replace?

The patent taxation system involves replacing the single tax with the payment of taxes only in relation to activities for which this tax regime is applied. The single tax that an entrepreneur pays for obtaining a patent replaces 3 taxes: VAT, personal income tax and personal property tax. However, if an entrepreneur imports products into the territory of the Russian Federation, then such an operation will be subject to VAT in the general manner, regardless of whether he applies a patent or not.

An entrepreneur with a patent must pay insurance premiums for himself.

Read more about them here. See also: “The individual entrepreneur was closed before the patent expired: how to calculate the percentage in the Pension Fund of Russia.”

In addition, he charges insurance premiums to the wage fund of his employees. Moreover, starting from 2021, he must do this on a general basis and at general tariffs. Until 2021, there was a benefit for individual entrepreneurs on PSN: the tariff for compulsory pension insurance was 20%, and there was no need to transfer social and health insurance contributions at all, with the exception of activities related to retail trade, public catering and leasing of premises (subclause 9 clause 1, subclause 3 clause 2 of article 427 of the Tax Code of the Russian Federation).

Read about insurance premium rates in the article “Insurance premium rates for 2021 - 2021 in the table.”

Russian laws allow the combination of several tax regimes. In this case, the individual entrepreneur must keep records separately for each type of activity (tax regime).

Grounds for refusal to issue a patent

^Back to top of page

- discrepancy in the application for a patent of the type of entrepreneurial activity with the list of types of entrepreneurial activity in respect of which a patent taxation system has been introduced on the territory of a constituent entity of the Russian Federation

- indication of the validity period of a patent that does not comply with clause 5 of Art. 346.45 of the Tax Code of the Russian Federation (a patent is issued at the choice of an individual entrepreneur for a period from one to twelve months inclusive within a calendar year)

- violation of the conditions for the transition to a patent taxation system established by the second paragraph of clause 8 of Article 345.45 of the Tax Code of the Russian Federation

An individual entrepreneur who has lost the right to use a patent taxation system or has ceased business activities in respect of which a patent taxation system was applied before the expiration of the patent has the right to again switch to a patent taxation system for the same type of business activity no earlier than from the next calendar year ( paragraph 2, clause 8, article 346.45 of the Tax Code of the Russian Federation)

- the presence of arrears of tax payable in connection with the use of the patent tax system

- failure to fill in required fields in a patent application

Who to pay and how much

A patent is issued for a period of 1 month to 1 year. When receiving a patent for 1-5 months, the tax amount is paid within 25 days from the date of issue of the patent. If the PSN provides for a period of 6 to 12 months, the tax amount can be divided into parts. 1/3 of the share is paid into the budget within the first 25 days, the remaining amount no later than 30 days before the patent expires.

The tax rate is fixed. The estimated income for certain types of activities in the constituent entities of the federation is taken as a basis. 6% is calculated from this amount - this will be the cost of the patent for the month. Individual entrepreneurs on PSN are exempt from paying VAT, personal income tax and property tax. There are still fixed payments to the Pension Fund and the Social Insurance Fund. Please note that the cost of a patent is not reduced by the amount of contributions to extra-budgetary funds, as with UTII and the simplified tax system.

It is also necessary to note the reduction in tax payments for employees from 22 to 20 percent. In the Social Insurance Fund and the Federal Migration Service you do not have to pay for employees.

Registration procedure

^To the top of the page

Registration of an individual entrepreneur as a taxpayer applying the patent taxation system is carried out by the tax authority to which he applied with an application for a patent, on the basis of the specified application within five days from the date of its receipt (clause 1 of Art. 346.46 Tax Code of the Russian Federation).

The date of registration is the date of commencement of the patent.

The amount of tax does not depend on the amount of income actually received by an individual entrepreneur and is determined based on the amount of potential annual income established for each type of activity.

We recommend!

The application can be easily filled out and sent to the inspectorate using the “Personal Account of an Individual Entrepreneur”.

Three simple steps:

- On the main page of the Personal Account of an individual entrepreneur, select the “All services” button.

- In the “Changing the taxation system” block, select the PSN tab and the document “Application for a patent”.

- Add information about the patent, sign and send to the tax authority (if you have an enhanced qualified electronic signature).

If an individual entrepreneur carries out business activities in a constituent entity of the Russian Federation in which he is not registered at his place of residence, then an application can be submitted to the tax authority with which he was registered as a UTII payer.

You can read more about the tax regime in a special section:

Go to the page “Patent taxation system”

Taxable period

^To the top of page 1 calendar year If a patent is issued for a period of less than a calendar year, the tax period is the period for which the patent was issued.

In 2021, the tax period is a calendar month.

In the event of termination of a business activity in respect of which the patent tax system was applied before the expiration of the patent, the tax period is recognized as the period from the beginning of the patent until the date of termination of such activity.

Eligibility

Before choosing what is beneficial - the simplified tax system or a patent, it is worth checking whether the criteria that allow the use of one or another system are met. This is especially true for already operating individual entrepreneurs who receive a certain amount of revenue and have entered into employment contracts with hired employees.

There are restrictions for special regimes - for a patent in Art. 346.45 of the Tax Code of the Russian Federation, for the simplified tax system in Art. 346.12-346.13 Tax Code of the Russian Federation. Main criteria:

- the maximum amount of revenue per year for a patent is 60 million rubles, for the simplified tax system - 150 million rubles;

- the average number of employees under a patent is no more than 15 people, under the simplified tax system - no more than 100 people.

In addition, the patent system in 2021 is valid only for 64 types of activities, and only if regional legislation on PSN has established the possibility of their application. A patent cannot be applied to trade in goods subject to mandatory labeling. The simplified tax system can be applied to almost all types of activities, with some exceptions listed in Art. 346.12 Tax Code of the Russian Federation.

You can switch to the “simplified” system only from the beginning of the year by submitting a corresponding notification to the Federal Tax Service Inspectorate no later than December 31. The tax period under the simplified tax system is one year.

The validity period of a patent (also known as the tax period) is from 1 to 12 months within a calendar year, while an individual entrepreneur can acquire several patents for different types of business.

Tax calculation procedure

^To the top of the page

Tax base is the monetary expression of the annual income potentially received by an individual entrepreneur for the type of business activity in respect of which the patent taxation system is applied, established for a calendar year by the law of the constituent entity of the Russian Federation.

Tax rate 6%

The laws of the constituent entities of the Russian Federation may establish a tax rate of 0% for two years for individual entrepreneurs registered for the first time and carrying out activities in the production, social or scientific spheres, as well as in the field of consumer services to the population (Clause 3 of Article 346.50 of the Tax Code of the Russian Federation) . The validity period of these tax holidays is until 2023.

According to the laws of the Republic of Crimea and the federal city of Sevastopol, the tax rate can be reduced in the territories of the relevant subjects for all or certain categories of taxpayers (clause 2 of Article 346.50 of the Tax Code of the Russian Federation):

- in the period 2015 - 2021 — up to 0%;

- in the period 2021 - 2021 - up to 4%.

Tax payment

^To the top of the page

Payment procedure

The validity period of a patent is less than 6 months - in the amount of the full amount of tax no later than the expiration date of the patent

The validity period of a patent from 6 to 12 months - in the amount of 1/3 of the tax amount no later than ninety calendar days after commencement of the patent; - in the amount of 2/3 of the tax amount no later than the expiration date of the patent.

If the tax amount is recalculated in connection with the termination of an individual entrepreneur's business activity in respect of which the PSN is applied, then the amount of tax subject to additional payment is paid no later than 20 days from the date of deregistration of the taxpayer with the tax authority.

Please pay attention! In case of non-payment or incomplete payment of tax, the tax authority, after the expiration of the established period, sends to the individual entrepreneur a demand for payment of tax, penalties and fines.

Go to Service “Fill out payment receipt”

Budget revenue classification codes

Patent validity period for foreign citizens

The patent is issued to foreign citizens who do not require a visa to cross the Russian border. In Art. 13.3 of Law No. 115-FZ describes how to apply for a patent, what documents must be submitted for this, and what may be the grounds for refusing to issue a patent.

The validity period of a patent is limited to 12 months, with the minimum period for which a patent is issued being one month. The number of months that a foreigner’s work patent is valid depends on the time interval during which the person made payments in the form of fixed advances on personal income tax.

The patent expires the day after the expiration of the period for which advance payments of income tax were made.

Loss of the right to use the patent tax system

^Back to top of page

- if, from the beginning of the calendar year, the taxpayer’s income from sales for all types of business activities to which the patent tax system is applied exceeded 60 million rubles

When applying simultaneously the patent taxation system and the simplified taxation system, income from sales under both tax regimes is taken into account.

- if during the tax period the average number of employees for all types of business activities in respect of which PSN exceeded 15 people

- if during the tax period an individual entrepreneur carrying out business activities in the field of retail trade sold goods that were not related to retail trade in accordance with paragraphs. 1 clause 3 art. 346.43 Tax Code of the Russian Federation

An application for loss of the right to use the patent tax system is submitted to the tax authority within 10 calendar days from the date of the occurrence of the circumstance that is the basis for the loss of the right to use the patent tax system (clause 8 of Article 346.45 of the Tax Code of the Russian Federation).

Application form for loss of the right to use the patent taxation system (form No. 26.5-3), approved by order of the Federal Tax Service of Russia dated July 12, 2019 No. MMV-7-3 / [email protected] pdf (753 kb)

Download

An individual entrepreneur who has lost the right to use a patent taxation system or has ceased business activities in respect of which a patent taxation system was applied before the expiration of the patent has the right to again switch to a patent taxation system for the same type of business activity no earlier than from the next calendar year ( Clause 8 of Article 346.45 of the Tax Code of the Russian Federation).

The application form for termination of business activity (form No. 26.5-4) was approved by Order of the Federal Tax Service of Russia dated December 14, 2012 No. MMV-7-3/ [email protected]

Patent taxation system: pros and cons

We asked entrepreneurs and experts to share their experiences with patents and find out what they want from the tax system.

Dmitry Gudovich, head of accounting customer service, Modulbank

The advantage of PSN is its ease of accounting. Using this system, an entrepreneur can keep a book of income, but there is no need to submit it to the tax office for certification. PSN allows you to clearly determine income by recording the date of receipt of money. Paying for a patent makes it possible not to spend money on other taxes. Of course, this rule is valid only for the period of validity of the patent, the minimum period of which is one month. This is convenient for those individual entrepreneurs who work seasonally.

Another advantage is that when receiving cash, you can use a strict reporting form (SSR) instead of a cash register. The main thing is not to forget that the BSO is issued for each fact of receiving cash.

Despite the advantages, PSN also brings difficulties. Predicting the success of a business, especially in this day and age, is not easy. Therefore, paying taxes upfront may not pay for itself.

The cost of a patent depends on the basic profitability, which is calculated by the state based on statistics and expert market assessments. Changing market conditions prevent its adequate assessment.

Despite its ease of use, PSN has its drawbacks. One of the main problems is that there are too many nuances in entrepreneurship. For example, a salon with five hairdressers and one with ten hairdressers are two different salons with different levels of income and expenses. As the number of employees increases, income and expenses change disproportionately. The list of activities on the PSN will be expanded starting in 2021. Of course, taking all factors into account will lead to a more complicated tax regime, but we would also like some flexibility.

In general, we need to improve our tax system by bringing together all the rules for working within a particular tax regime in one law. For now, an entrepreneur needs to study several laws in order to find out the rules for working with cash received from legal entities and individuals and, accordingly, what tax regimes he has the right to apply. This applies to the entire legislative system of the Russian Federation on taxes, and not just the PSN, and implies a huge layer of work. In the meantime, we do not have transparent laws and rules, except perhaps in media reviews on the Internet. And it is not entirely clear whether this or that article is outdated, or whether the information it contains is up-to-date.

Vyacheslav Tertus, head of DELUS LLC

I live in Sevastopol and therefore managed, without leaving the city, to change three states in which I was engaged in accounting, therefore I can act as an expert on taxation issues.

With PSN, there is no need to keep accounting records and you don’t have to use cash registers. An entrepreneur is exempt from a number of taxes: personal income tax, personal property tax, VAT with some exceptions. The tax rate is 6% (and in Crimea and Sevastopol 3%) and does not depend on the amount of income actually received by the entrepreneur, but is determined based on the amount of potential annual income established for each type of activity, determined by the law of the constituent entity of the Russian Federation. The calculation of the cost of a patent is carried out in the patent itself, which is clear to the payer. In general, the advantages of using the patent system are its simplicity, transparency and the possibility of use in many types of business.

Among the disadvantages of the patent taxation system are: restrictions on the types of activities and the number of employees (no more than 15 people), income up to 60 million per year (next year up to 120 million per year), the obligation to keep a book of income and expenses and apply strict forms reporting. The validity period of a patent is one year, which forces entrepreneurs to visit the tax office annually to confirm the right to use the patent system. Usually all this happens in December, which is not the most pleasant time to visit an inspection.

If the patent is not paid on time or the payment amount is less than the established one, then the individual entrepreneur loses the right to use the patent. It is possible to switch again to a patent taxation system for the same type of business activity no earlier than next year. An example from life: an entrepreneur got into an accident and became incapacitated for some time, and was late in paying for a patent. Now he is forced to fire all employees and stop business activities in order to switch to OSNO. If the business was low-margin and sales fell even further, an unexpected switch to OSNO could kill the business.

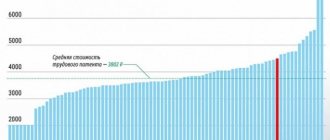

This graph describes the level of income and payment of taxes and fees under PSN, UTII, simplified tax system (3% of income) for an entrepreneur without employees engaged in retail trade in a retail outlet with an area of 11 sq.m. Switching from a patent system to any other does not make sense, since the simplified tax system requires a cash register, and UTII is too expensive.

Nina Makogon, founder of the PR agency HAVAR Communications

A few months ago I needed to register a legal entity, and I was unable to use the PSN because advertising services are not provided for in this section of the regulations. In this regard, we decided to apply the standard simplified tax system, which made it possible to select an expanded list of service names.

Before using the patent system, I carefully studied all its pros and cons. Positive aspects: optional accounting and a simplified tax calculation system (produced by the tax authority directly in the patent), which implies exemption from VAT, personal income tax and personal property tax. In order to use the PSN, the type of activity of your company must be included in the Classifier of types of business activities in respect of which the law of the subject provides for the use of the patent system. Advertising agencies are not yet included in this classifier.

I am satisfied with the simplified tax system, since my turnover does not exceed 60 million rubles. per year, I have less than 100 employees on staff, and the residual value is less than 100 million rubles.

An important point that few people know: if your company has several representative offices or branches, you do not have the right to work under the simplified tax system.

There are two options for a simplified taxation system: 6% of income and 15% of profit. In my opinion, the first option simplifies life and relieves the entrepreneur of the need to confirm the existence of expenses.

For me, as the owner of a PR agency, it is important that all types of activities that my company offers on the market are included in the patent system. Otherwise, I simply do not have the right to use it legally. The rates are quite reasonable and allow the business to grow. If the rules of the patent system change, I will be happy to switch to it. Especially if you don’t have to buy patents for each type of activity.

Stanislav Borodin, commercial director at the Legal Services Center

Advantages of PSN: simplicity of accounting reporting, no need to submit a declaration to the tax office, switching to PSN is possible at any time during the activity, it is possible to use PSN in conjunction with other taxation systems (USN, UTII, OSNO), instead of a cash register, you can use a cash printer, tax convenient to pay: 1/3 in the first month and 2/3 a month before the end of the tax period.

Negative points: only an individual entrepreneur can switch to PSN; the list of types of entrepreneurial activities is established by the constituent entities of the Russian Federation, but not less than 47 types specified in Art. 346.43 of the Tax Code of the Russian Federation, in order to switch to PSN it is necessary to meet certain requirements (in the case of a retail store: the area of the sales floor should be no more than 50 sq.m), the total income of the entrepreneur for all types of activities is limited to 60 million rubles. in year.

When making a decision, it is necessary to determine the expected level of income for a certain period. For a retail store in Moscow in 2015, the expected income for one year is 2 million rubles. If an entrepreneur expects to receive annual income in excess of this amount, then it makes sense to switch to PSN.

For example, in 2014 our store received an income of 7 million rubles. With a simplified tax system of 6%, we had to pay a tax of 420,000 rubles. (7000,000/100*6), but using PSN, we paid 120,000 rubles. Thus, tax savings amounted to RUB 300,000.

This is a convenient taxation system for small businesses, but for some types of trade, 50 sq.m of retail space is not enough, for example, for large goods or a wide range of goods. Income of 60 million rubles. established for all subjects of the Russian Federation without taking into account the peculiarities of doing business in a particular region, which is unfair in relation to “expensive” regions.

Olga Kosets, director of the Sofiano clothing production, president of the local organization for the protection and support of small and medium-sized businesses “Business People”

PSN is quite profitable for many entrepreneurs. It's surprising that not everyone has realized this yet. The problem is that officials are not actively informing entrepreneurs about the capabilities of this system. First of all, a small entrepreneur strives in every possible way to reduce unnecessary costs, and this is understandable - all means must work, and there are few of them. The patent allows you to abandon the cash register, that is, it eliminates the need to pay for the cost of the device itself, consumables and expensive maintenance.

The patent itself works on the principle of a “travel ticket”: an entrepreneur buys it and for some time does not worry about how and what to pay for. In addition, the amount of reporting is reduced, which is very convenient.

It is important to understand that there is an ironclad rule “one type of activity - one patent.” For example, if you have a beauty salon that provides hairdressing and manicure services, then you already need several patents. If you have a grocery store, it is important to remember that you cannot obtain a patent for the sale of alcohol, since the sale of alcohol requires strict control.

In Moscow, many entrepreneurs are already beginning to feel the benefits of patents. A small store with an area of up to 50 sq.m. in Krekshino, where I am a municipal deputy, saves significantly after purchasing a patent - expenses have been reduced threefold. As a result, the money saved goes towards business development and service improvement.

Removal from the register

^Back to top

Within 5 days

- If the patent expires

, deregistration is carried out by the tax authority within 5 days from the date of expiration of the patent. - In case of loss of the right to use the patent tax system,

deregistration is carried out within 5 days from the date the tax authority receives an application for loss of the right to use the patent tax system (form No. 26.5-3 approved by Order of the Federal Tax Service of Russia dated July 12, 2019 No. MMV-7- 3/ [email protected] ) - In case of termination of business activity in respect of which the patent tax system is applied,

deregistration is carried out within 5 days from the date the tax authority receives an application for termination of business activity in respect of which the patent tax system was applied (form No. 26.5-4 approved by Order of the Federal Tax Service of Russia dated 12/14/2012 No. ММВ-7-3/ [email protected] )

The date of deregistration is the date of transition of an individual entrepreneur to a general taxation regime (to a simplified taxation system, to a taxation system for agricultural producers (if the taxpayer applies the appropriate taxation regime)) or the date of termination of business activity in respect of which the patent taxation system was applied.

What are the validity periods and how to extend?

The migration authority must issue a work patent to a foreign citizen or notify him of the refusal to issue it no later than ten days after the citizen has submitted an application for a patent.

The patent itself is issued for a period of one to three months, but at the same time it can be extended up to a period of 12 months.

The total duration of a patent renewal must not exceed twelve months from the date it was originally issued. The patent renewal is carried out for the period of personal income tax payment in the form of a fixed advance payment. Otherwise, the patent expires on the day following the last day of the period within which the above tax was paid.

The general renewal procedure is extremely simple. To renew a patent, you do not need to contact the migration authority - you just need to pay the personal income tax for the corresponding period.

After the twelve months within which the extension can be carried out have expired, the foreign citizen has the right to apply to the migration authorities for renewal of the patent, which can also be extended in the future up to 12 months.

Step-by-step instructions for obtaining a patent

^To the top of the page

Transition to a patent tax system

1

Submit an application

10 days before the start of business activity, we submit to the tax authority an application for the transition to a patent tax system

You can fill out and print the application yourself:

To obtain a patent, an individual entrepreneur must submit to the tax authority an application for a patent in the form approved by Order of the Federal Tax Service of Russia dated December 09, 2020 No. KCh-7-3/ [email protected] “On approval of the application form for a patent, the procedure for filling it out, the format submitting an application for a patent in electronic form and declaring the order of the Federal Tax Service dated July 11, 2017 No. ММВ-7-3/ [email protected] .”

Patent application form pdf (268 kb)

Download

Format for submitting a patent application in electronic form docx (71 kb)

Download

Procedure for filling out an application for a patent docx (43 kb)

Download

Patent application diagram xsd (37 kb)

Download

At the same time, individual entrepreneurs also have the right to apply for a patent in the form approved by Order of the Federal Tax Service of Russia dated July 11, 2017 No. ММВ-7-3 / [email protected]

Application form for a patent, approved by order of the Federal Tax Service of Russia dated July 11, 2017 No. ММВ-7-3/ [email protected] pdf (237 kb)

Download

Format for submitting an application for a patent in electronic form doc (213 kb)

Download

Procedure for filling out an application for a patent docx (51 kb)

Download

Patent application diagram xsd (36 kb)

Download

2 We receive a patent

Within 5 days from the date of receipt of the application for a patent, the tax authority is obliged to issue a patent to the individual entrepreneur (clause 3 of Article 346.45 of the Tax Code of the Russian Federation).

3 Tax payment

If the patent is received for a period of up to 6 months

We pay tax in the full amount of the tax no later than the expiration date of the patent.

If the patent is received for a period of 6 to 12 months

We pay tax:

- in the amount of 1/3 of the tax amount no later than ninety calendar days after the patent came into effect;

- in the amount of 2/3 of the tax amount no later than the expiration date of the patent.

4 Tax accounting

Accounting for income from sales is kept in the income book of an individual entrepreneur applying the patent tax system.

The form and procedure for filling out the income accounting book are approved by Order of the Ministry of Finance of Russia dated October 22, 2012 No. 135n

Transition order

To apply PSN from 01/01/2021, an individual entrepreneur should, no later than 10 days before the start of application of this tax regime, submit an application for a patent to the tax authority at the place of residence in form 26.5-1, approved by order of the Federal Tax Service of Russia dated 07/11/2017 No. MMV- 7-3/ [email protected]

For individual entrepreneurs who have expressed a desire to obtain a patent starting in January 2021, the deadline for filing an application for a patent has been extended until December 31, 2020 (letter of the Federal Tax Service of Russia No. SD-4-3/ [email protected] dated December 9, 2020)

Patent application form pdf (237 kb)

Download

An individual entrepreneur independently chooses the validity period of a patent - from 1 to 12 months within one calendar year