Who is required to take the RSV

Persons paying benefits to employees are required to report quarterly on accrued insurance premiums (Article 431 of the Tax Code of the Russian Federation). The absence of payments to employees does not exempt the organization from submitting the DAM to the inspection. The Ministry of Finance and the Federal Tax Service explain that in this case, a zero calculation for insurance premiums is filled out (letter of the Ministry of Finance No. 03-15-07/17273 dated March 24, 2017, letter of the Federal Tax Service No. GD-4-11 / [email protected] dated April 2, 2018) .

The need to submit the DAM is not canceled, even if the duties of the general director are performed by the sole owner without concluding an employment contract, and there are no other employees in the organization yet. In this case, section 3 of the report provides personalized information about the general director.

Use the free instructions for filling out insurance premium calculations from ConsultantPlus. Experts told us how to fill out forms correctly in different situations.

Which sections to include in the zero calculation

Let’s assume that the accountant decided not to take risks and submit a zero calculation for the 2nd quarter of 2021 to the INFS. But what sections should it include? Letter No. BS-4-11/6940 of the Federal Tax Service of Russia dated April 12, 2017 states that the “empty” calculation should include:

- title page;

- Section 1 “Summary of the obligations of the payer of insurance premiums”;

- subsection 1.1 “Calculation of the amounts of insurance contributions for compulsory pension insurance” and subsection 1.2 “Calculation of the amounts of insurance contributions for compulsory health insurance” of Appendix 1 to Section 1;

- Appendix 2 “Calculation of the amounts of insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity” to section 1;

- Section 3 “Personalized information about insured persons.”

How to fill out a report for organizations affected by COVID-19

For payers operating in the industries most affected by the spread of the new coronavirus infection, a zero rate of insurance premiums has been established for April - June 2021 (Article 3 of Federal Law No. 172-FZ of 06/08/2020).

Instructions on how to correctly fill out the calculation of insurance premiums for companies that are exempt from social contributions (letter of the Federal Tax Service No. BS-4-11/9528 dated 06/09/2020):

- Fill out the RSV title page as usual.

- In section 1, enter zeros in all totals.

- In lines 001 “Tariff code” of appendices 1 and 2 to section 1, enter “21”.

- When indicating the amount of payments, the tax base and the amount of accrued insurance premiums in Appendices 1 and 2, follow the rule: in the first column reflect the amounts of the first quarter, in the second, third and fourth columns enter zeros.

- When filling out line 130 of section 3 “Category code of the insured person”, indicate “KV”. In lines 140, 150, 160 and 170, enter zeros.

Sample of filling out the form according to KND 1151111

Below we present examples of filling out sheets for some sections. For more information on the procedure for filling out the calculation form for KND 1151111, read the article: “DAM for the 2nd quarter of 2021 (sample of completion).”

Title page

Section 1

Appendix 1 Section 1

Subsection 1.2

The video material provides information about the features of filling out the DAM in 2021:

Do entrepreneurs without employees rent out the DAM?

Not only organizations, but also individual entrepreneurs are recognized as payers of social contributions. An entrepreneur has the right to hire employees, but sometimes conducts business without hiring employees. You will not have to submit calculations for insurance premiums if the individual entrepreneur does not have employees. In this case, tax officials have the right to demand an explanation. Explain to them in writing that you are working without hiring employees.

If an individual entrepreneur has employees, but they are not working (on leave without pay, on maternity leave), then the entrepreneur submits a zero RSV.

In what form is the RSV submitted?

The form used to submit a zero calculation for insurance premiums to the tax office was approved by Federal Tax Service Order No. ММВ-7-11/ [email protected] dated 09.18.2019 as amended by Order No. ED-7-11/ [email protected] dated 10.15.2020. It also, in Appendix 2, describes in detail the rules and procedure for filling out the reporting form.

IMPORTANT!

Submit reports for the 4th quarter of 2021 using the updated form. The new form was approved in the order of the Federal Tax Service No. ED-7-11 / [email protected] dated 10/15/2020. The main change in the structure of the report is the inclusion of information on the average number of employees on the title page.

The reporting form is submitted to the tax office at the location of the organization. In addition to this report, payers of insurance premiums must submit two more personalized accounting forms to the Pension Fund of the Russian Federation:

- monthly SZV-M;

- annually SZV-STAZH.

Download the unified calculation of insurance premiums for 2020

Let us remind you that the new DAM form should have been officially approved in the 1st quarter of 2021. But this did not happen, and employers submitted payments on the same form throughout 2021. On October 8, 2019, Federal Tax Service Order No. ММВ-7-11/ [email protected] , which approved the new DAM form, was finally officially published. But we will submit the report using the new form starting from the 1st quarter of 2020.

In other words, for the entire period of 2021 we submit the DAM on the same form. You can download the RSV form from the link:

Starting with reporting for the 1st quarter of 2021, we submit the DAM on a new form, download here:

Download the Procedure for filling out the DAM using the new form, starting with reporting for the 1st quarter of 2021:

The article was updated in accordance with current legislation 01/14/2020

How to pass a zero RSV

Starting from 2021, the DAM is provided to the tax office at the location of the organization. Previously, the report was submitted to the Pension Fund.

Here's how to send a zero calculation for insurance premiums (Article 431 of the Tax Code of the Russian Federation):

- by mail;

- in electronic form via TKS;

- submit it during a personal visit to the tax office.

The DAM is submitted on paper only if the number of employees of the company does not exceed 10 people (clause 10 of Article 431 of the Tax Code of the Russian Federation).

Example

LLC “Company” does not operate. The company has 26 employees. All of them have been on leave without pay since 01/01/2020.The LLC sends the RSV in electronic form through the TKS operator, signing with an electronic digital signature of an authorized person. The report sending service checks how correctly the report is completed. If after filling out the zero calculation for insurance premiums is not uploaded, you need to check the correctness of filling.

Uniform calculation form for insurance premiums 2020

In paper format, the calculation of insurance premiums KND 1151111 is submitted by employers who in the previous reporting period had an average number of employees to whom payments are made of no more than 25 people.

In this case, a single calculation for employee insurance premiums can be sent by mail, providing it with a list of the contents and accompanied by a receipt. Another option is to simply submit the document to the Federal Tax Service; this can be done either by the individual entrepreneur himself or the head of the organization, or by an authorized person vested with these powers (having a power of attorney).

If a company or individual entrepreneur has more than 25 hired employees, then a single calculation of insurance premiums must be submitted to the Federal Tax Service, in accordance with clause 10 of Article 431 of the Tax Code of the Russian Federation), in electronic form.

When to take it

The DAM is submitted to the tax office no later than the 30th day of the month following the reporting quarter. If the last day of delivery falls on a non-working weekend or holiday, then the deadline is postponed to the next first working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation). This is when zero reporting is submitted for calculation of insurance premiums (clause 7 of Article 431 of the Tax Code of the Russian Federation):

| Period | Last day of delivery |

| 4th quarter 2020 | 01.02.2021 |

| 1st quarter 2021 | 30.04.2021 |

| Half year 2021 | 30.07.2021 |

| 9 months 2021 | 01.11.2021 |

| 4th quarter 2021 | 31.01.2022 |

What are the sanctions for failure to submit the DAM?

In Art. 431 indicates how to submit a zero calculation for insurance premiums - in paper and electronic form. If an organization violates the deadline, procedure or form of submission, tax authorities will issue a fine.

Despite the fact that a company that does not carry out activities reflects zero indicators in the report, tax authorities have the right to apply the following sanctions to it:

- The minimum fine for failure to submit a report is 1000 rubles. (Article 119 of the Tax Code of the Russian Federation);

- administrative fine for an official of an organization - from 300 to 500 rubles. (Article 15.5 of the Code of Administrative Offenses of the Russian Federation);

- suspension of transactions on bank accounts (clause 6 of Article 6.1, clause 3.2 of Article 76 of the Tax Code of the Russian Federation);

- fine for failure to comply with the electronic form for submitting a report - 200 rubles. (Article 119.1 of the Tax Code of the Russian Federation).

How to fill out the RSV correctly

Order No. ММВ-7-11/ [email protected] indicates which zero RSV sheets should be submitted to taxpayers:

- title page;

- section 1;

- subsections 1.1 and 1.2 of Appendix 1 to Section 1;

- appendix 2 to section 1;

- section 3.

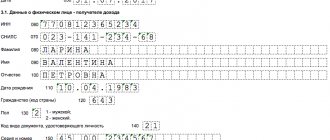

The report must indicate the name, INN and KPP of the organization, the period for which the DAM is submitted, and the tax authority code. Enter zeros in all fields with amount indicators. Section 3 indicates the data of the organization’s employees (at least the general director). Due to the lack of accruals, subsection 3.2 does not need to be filled out.

If errors are identified in the unified calculation of insurance premiums

Sometimes an employer meets the deadline for submitting documentation to the regulatory authority, but then discovers some errors in it. Or the information reflected in the calculation turned out to be incomplete. Then, as the Tax Code dictates (clause 1 of Article 81 of the Tax Code of the Russian Federation), it is imperative to submit an updated calculation of insurance premiums to the Federal Tax Service.

The updated document must contain those sections and appendices to them that were filled out in the original version of the calculation, only taking into account corrections, additions, and clarifications.

Particular attention is paid to section 3. There is no need to rewrite data for all insured persons in the updated calculation. It includes only new data on those employees for whom inaccurate (erroneous or incomplete) information was recorded in the first version of the document.

The Federal Tax Service, in its letter dated June 28, 2017 N BS-4-11/ [email protected] , explained how to adjust data on insured persons in calculations of insurance premiums:

1. If errors are detected in personal data, subsections 3.1 and 3.2 must be filled out in duplicate. The first copies must include:

- for subsection 3.1 - information from the original calculation, with the same errors;

- for subsection 3.2 - value “0”.

In the second copies you must enter:

- for subsection 3.1 - correct information about the individual, correcting the mistakes;

- for subsection 3.2 - information on payments in favor of an individual and accrued contributions for compulsory pension insurance.

Moreover, in the version with incorrect data, you must enter the correction number 1. In the information with correct (corrected) data, the correction number will be 0.

2. If for individual insured persons it is necessary to change the indicators in subsection 3.2, then section 3 for such persons with subsection 3.2 correctly filled out should be included in the updated calculation. If after this the total amount of calculated insurance premiums changes, then section 1 must also be changed.

3. If the insured persons were mistakenly not indicated in the initial calculation, then Section 3 must be filled out for them and included in the updated calculation. At the same time, it is necessary to adjust the indicators of section 1.

4. If any persons are included in the initial calculation by mistake, then section 3 should be included in the updated calculation. In it, “0” must be indicated in all lines of subsection 3.2. Section 1 will also be subject to downward adjustments.